eScore

bbrown.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Brown & Brown has a professional corporate website with a solid technical foundation for SEO, including dedicated country sections. However, its digital presence is that of a significant challenger rather than a market leader, often overshadowed by larger competitors like Marsh McLennan and Aon. The content strategy is moderately aligned with the user journey but is weaker at the top of the funnel, missing opportunities to capture problem-aware prospects with authoritative, niche-specific content hubs.

A strong foundation for geographic SEO with dedicated sections for different countries, reflecting their global physical footprint.

Develop comprehensive content hubs around their high-margin 'National Programs' and 'Specialties' to attract niche, high-value clients and establish dominant authority in those segments, moving beyond a generalist digital presence.

The brand effectively communicates its core value proposition as a supportive, long-term partner on a client's 'growth journey,' which is a strong differentiator. Messaging is well-segmented for different audiences, such as the aspirational tone for US enterprises versus the practical tone for UK professionals. However, the messaging relies heavily on abstract corporate language ('solutions,' 'capabilities') and lacks the tangible proof (case studies, testimonials) needed to fully substantiate its claims and humanize the brand.

The core messaging theme of supporting a client's 'growth journey' is a powerful and unique narrative that elevates the brand beyond a simple insurance vendor.

Inject tangible proof points into the messaging by creating a 'Client Stories' section with specific case studies and testimonials that demonstrate exactly how Brown & Brown has facilitated client growth.

The website's conversion experience is its most significant weakness, suffering from a passive design approach that de-emphasizes key conversion elements. Primary calls-to-action often use 'ghost button' styles that lack visual prominence and are easily overlooked, increasing cognitive load. Furthermore, high-friction elements like the long, single-step 'Request a Quote' form create significant barriers to lead generation, a problem that is exacerbated on mobile devices.

The information architecture is logical at a high level, with a clear primary navigation and mega menu that helps users understand the breadth of services offered.

Redesign all primary CTAs (e.g., 'Get in Touch', 'Request a Quote') to use a solid, high-contrast color (the brand's vibrant green) and implement a multi-step form for quote requests to reduce initial friction.

The company demonstrates a very mature and robust approach to credibility and risk, reflecting its status as a large, publicly-traded global firm. Its legal compliance framework is a strategic asset, with region-specific privacy policies (GDPR, CCPA), excellent cookie consent management, and a strong commitment to accessibility (WCAG 2.1 AA). Required regulatory disclosures, such as FCA authorization in the UK, are clearly displayed, building significant trust and reducing litigation risk.

Proactive and sophisticated data privacy management, including region-specific policies and honoring Global Privacy Control (GPC) signals, which builds significant trust.

Modify data collection forms for UK/EU users to include a separate, unticked checkbox for marketing consent to move from a very good GDPR posture to a fully compliant one.

Brown & Brown's primary competitive advantage is its unique decentralized operating model, which fosters an entrepreneurial culture, agility, and deep local client relationships—a moat that is difficult for larger, more bureaucratic competitors to replicate. This is powerfully combined with a proven, prolific M&A strategy that consistently adds new capabilities and drives growth. However, the company has lower brand recognition and invests less in proprietary global technology platforms compared to the 'Big Three' (Marsh, Aon, Gallagher).

The decentralized operating model combined with a successful M&A integration capability creates a 'best-of-both-worlds' advantage: the local touch of a small firm with the resources of a global one.

Invest in a unified digital client portal to mitigate the risk of a disjointed customer experience, which is a key vulnerability of the decentralized model.

The business is highly scalable, built on a proven 'acquisition-led compounding growth' model. This M&A engine, which is a core competency, allows for rapid expansion of revenue and market presence. The business model demonstrates high operational leverage and strong unit economics, evidenced by consistent organic revenue growth (10.4% for 2024) and high client retention, leading to a favorable LTV/CAC ratio. The primary constraint is the operational complexity of integrating numerous acquisitions.

A highly effective and disciplined M&A strategy serves as the primary growth engine, allowing for rapid and continuous scaling of the business.

Establish a dedicated M&A integration 'Center of Excellence' to standardize the 100-day plan for technology, culture, and processes, accelerating synergy realization from acquisitions.

Brown & Brown's business model is exceptionally coherent and time-tested, centered on a decentralized structure that empowers local teams while leveraging centralized resources. The revenue model is resilient, with highly recurring commission streams from renewals, supplemented by high-margin fees. The strategic focus on M&A as a primary growth driver is clear and well-executed, consistently fueling expansion into new markets and specialties. The model effectively aligns the interests of employees (through an ownership culture) and shareholders.

The symbiotic relationship between a disciplined M&A strategy and a decentralized, entrepreneurial culture creates a powerful, coherent, and self-reinforcing business model.

Systematically expand the high-margin, fee-for-service risk management and advisory practice to diversify revenue away from the commission-based model, which is susceptible to insurance market cycles.

As one of the world's largest insurance brokerages, Brown & Brown has significant market power, particularly in the middle-market segment. Its active M&A strategy demonstrates a clear growth trajectory relative to smaller competitors. However, its market power is challenged by the top-tier global firms (the 'Big Three'), which have greater scale, brand recognition, and influence over industry trends and pricing. The company acts more as a highly influential major player than a market-setter.

A strong focus on acquiring and developing deep expertise in specialized niches gives the company significant pricing power and leverage within those specific markets.

Create and publish a flagship annual 'Middle Market Business Risk Report' to establish data-driven thought leadership, thereby increasing its influence on market conversations currently dominated by larger rivals.

Business Overview

Business Classification

Insurance Brokerage

Risk Management Consulting

Insurance

Sub Verticals

- •

Property & Casualty

- •

Employee Benefits

- •

Personal Insurance

- •

Specialty Programs

- •

Wholesale Brokerage

Mature

Maturity Indicators

- •

Publicly traded company (NYSE: BRO) since 1993.

- •

Founded in 1939, demonstrating long-term operational history.

- •

Consistently strong revenue growth, reporting $4.8 billion for the full year 2024.

- •

Aggressive and systematic M&A strategy, with over 500 agency acquisitions in its history.

- •

Global presence with over 700 locations and more than 23,000 employees worldwide following recent acquisitions.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Commissions

Description:Earned as a percentage of premiums paid by clients to insurance carriers for policies placed by Brown & Brown. This is the largest source of revenue, derived from new policies and renewals across all segments.

Estimated Importance:Primary

Customer Segment:All Segments (Retail, Programs, Wholesale)

Estimated Margin:Medium

- Stream Name:

Fees for Services

Description:Direct fees charged to clients for services such as risk management consulting, claims administration, and other specialized advisory services that are not tied to a specific insurance policy placement.

Estimated Importance:Secondary

Customer Segment:Commercial, Public, and Enterprise Clients

Estimated Margin:High

- Stream Name:

Contingent Commissions

Description:Additional commissions received from insurance carriers based on achieving specific pre-determined goals, such as volume, profitability, or growth of the business placed with them.

Estimated Importance:Tertiary

Customer Segment:N/A (Carrier-dependent)

Estimated Margin:High

Recurring Revenue Components

- •

Annual policy renewals

- •

Retainer-based consulting agreements

- •

Multi-year service contracts

Pricing Strategy

Commission-Based & Fee-for-Service

Value-Based Premium

Opaque

Pricing Psychology

- •

Relationship Pricing

- •

Bundling of Services

- •

Expertise Signaling

Monetization Assessment

Strengths

- •

Highly diversified revenue across multiple insurance lines (P&C, Benefits, etc.) and customer types, reducing dependency on any single market.

- •

Significant recurring revenue from policy renewals provides stability and predictability.

- •

Successful M&A strategy continuously adds new revenue streams and expands market presence.

Weaknesses

High dependency on a commission-based model, which can be sensitive to economic downturns (clients reducing coverage) and a soft insurance market (lower premiums).

Fee-based revenue, while high-margin, is a smaller portion of the overall business.

Opportunities

- •

Expand high-margin, fee-based risk management and ESG consulting services.

- •

Develop proprietary data analytics products to offer clients benchmarking and risk modeling services for a fee.

- •

Leverage technology to create efficiencies and offer tiered service levels (e.g., a digital-first service for smaller clients).

Threats

- •

Compression of commission rates due to increased competition from both traditional brokers and Insurtech startups.

- •

Regulatory changes that could impact commission structures or disclosure requirements.

- •

Disintermediation by Insurtech platforms that connect clients directly with carriers.

Market Positioning

Trusted advisor providing tailored, comprehensive risk solutions through a decentralized, entrepreneurial service model that combines global capabilities with local expertise.

Major Player

Target Segments

- Segment Name:

Commercial Enterprises (Mid-to-Large Market)

Description:Established businesses, public entities, and quasi-public organizations requiring complex property & casualty, employee benefits, and specialty risk management solutions.

Demographic Factors

- •

Mid-to-high annual revenue

- •

Multiple operating locations (national or international)

- •

Significant employee base

Psychographic Factors

- •

Value expertise and long-term relationships

- •

Risk-averse

- •

Seek strategic partners, not just vendors

Behavioral Factors

- •

Complex buying process involving multiple stakeholders (CFO, HR Director, Risk Manager)

- •

Focus on total cost of risk, not just premium

- •

Loyalty to brokers who provide excellent service and claims advocacy

Pain Points

- •

Managing complex and evolving risks (e.g., cyber, climate).

- •

Controlling rising insurance and employee benefit costs.

- •

Ensuring regulatory compliance across different jurisdictions.

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Small and Medium-sized Enterprises (SMEs)

Description:Small businesses, self-employed individuals, and trade professionals needing a range of essential insurance coverages like public liability, professional indemnity, and employer's liability.

Demographic Factors

- •

Lower annual revenue

- •

Typically owner-operated

- •

Localized operations

Psychographic Factors

- •

Time-poor and resource-constrained

- •

Seek simplicity and reliability

- •

Value personalized service from a local expert

Behavioral Factors

- •

Direct purchasing decision-maker (owner/founder)

- •

Price-sensitive but reliant on broker advice

- •

Often purchase bundled insurance packages

Pain Points

- •

Lack of in-house expertise to understand insurance needs.

- •

Finding affordable, yet comprehensive, coverage.

- •

Feeling underserved by larger financial institutions.

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Individuals (Personal Lines)

Description:Individuals and families requiring personal insurance products such as home, auto, and other personal property coverage.

Demographic Factors

Asset owners (home, vehicles)

Varying income levels

Psychographic Factors

Seek peace of mind and financial protection

Value convenience and a smooth claims process

Behavioral Factors

Increasingly comfortable with digital channels for quotes and service

Comparison shopping based on price and coverage

Pain Points

- •

Navigating the complex and often confusing process of buying insurance.

- •

Dealing with impersonal service from large direct insurers.

- •

Ensuring they have adequate coverage without overpaying.

Fit Assessment:Good

Segment Potential:Medium

Market Differentiation

- Factor:

Decentralized Operating Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Aggressive M&A and Integration Capability

Strength:Strong

Sustainability:Sustainable

- Factor:

Entrepreneurial, Merit-Based Culture

Strength:Moderate

Sustainability:Sustainable

- Factor:

Deep Niche and Specialty Program Expertise

Strength:Strong

Sustainability:Sustainable

Value Proposition

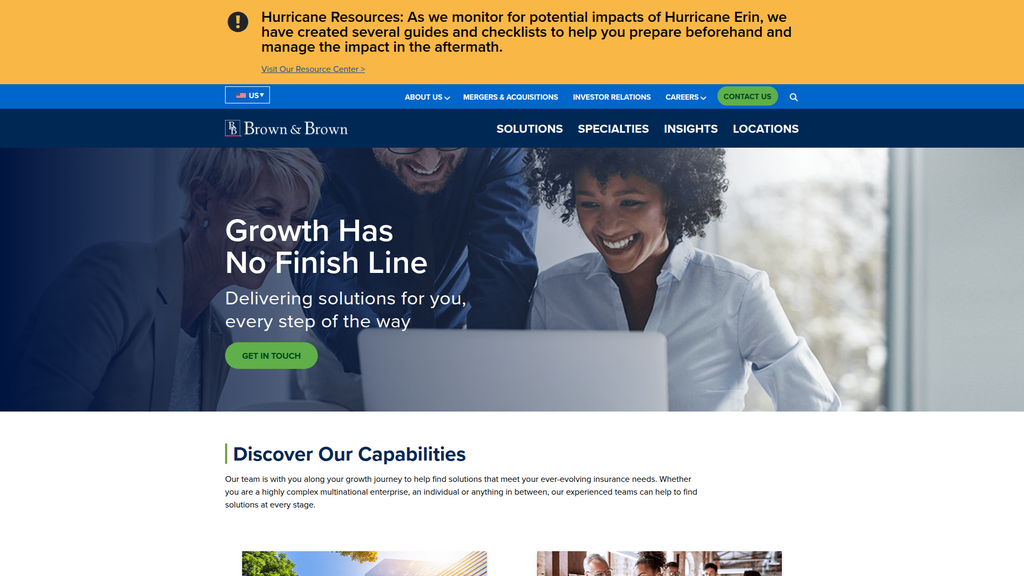

To be a trusted partner on your growth journey, delivering innovative insurance solutions and expert risk management with the personalized service of a local team and the resources of a global leader.

Good

Key Benefits

- Benefit:

Customized Insurance and Risk Solutions

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Dedicated sections for 'Property and Casualty', 'Employee Benefits', 'Personal Insurance', and 'Specialties' on the website.

Specific pages for niche segments like 'Trade & Professionals'.

- Benefit:

Expertise and Thought Leadership

Importance:Important

Differentiation:Somewhat unique

Proof Elements

'News & Insights' section featuring articles, podcasts, and webinars.

Emphasis on experienced teams and specialized knowledge.

- Benefit:

Scalable Service for All Growth Stages

Importance:Important

Differentiation:Unique

Proof Elements

Messaging targets a wide range from 'an individual' to a 'highly complex multinational enterprise'.

The tagline 'Growth Has No Finish Line' reinforces this commitment.

Unique Selling Points

- Usp:

A decentralized, entrepreneurial culture that empowers local teams to provide agile, responsive service while leveraging the strength of a global organization.

Sustainability:Long-term

Defensibility:Strong

- Usp:

Proven expertise in acquiring and successfully integrating specialized agencies, constantly expanding capabilities and talent.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

Protecting personal and business assets from financial loss due to unforeseen events.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Navigating the complexity of the insurance market to find appropriate and cost-effective coverage.

Severity:Major

Solution Effectiveness:Complete

- Problem:

Managing and mitigating evolving business risks in areas like cybersecurity, liability, and climate change.

Severity:Major

Solution Effectiveness:Partial

Value Alignment Assessment

High

The value proposition directly addresses the core market need for risk transfer and management. The emphasis on specialization and expertise aligns with the increasing complexity of risks in the commercial sector.

High

The messaging effectively resonates with both large enterprises that require sophisticated solutions and SMEs that value trusted, local advice, aligning with their distinct pain points.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Insurance Carriers (Underwriters)

- •

Reinsurance Companies

- •

Managing General Agents (MGAs)

- •

Technology Platform Providers (e.g., Agency Management Systems)

- •

Industry Associations

Key Activities

- •

Client Consultation & Risk Assessment

- •

Negotiation with Insurance Carriers

- •

Policy Placement & Administration

- •

Claims Advocacy & Management

- •

Mergers & Acquisitions

- •

Development of Specialty Programs

Key Resources

- •

Broker Talent and Expertise

- •

Carrier Relationships and Market Access

- •

Brand Reputation and Trust

- •

Proprietary Technology and Data Analytics

- •

Capital for Acquisitions

Cost Structure

- •

Employee Compensation and Benefits (Primary Cost Driver)

- •

Technology and IT Infrastructure

- •

Office Leases and Facilities

- •

Marketing and Business Development

- •

Errors & Omissions (E&O) Insurance

- •

Regulatory and Compliance Costs

Swot Analysis

Strengths

- •

Strong and consistent financial performance with diversified revenue streams.

- •

Proven, aggressive M&A strategy that fuels growth and expands capabilities.

- •

A unique decentralized culture that fosters an entrepreneurial spirit and local market responsiveness.

- •

Deep expertise in specialty niches and programs, creating higher-margin opportunities.

Weaknesses

- •

Potential for cultural dilution or integration challenges with the high velocity of acquisitions.

- •

Decentralized model could lead to operational inconsistencies or inefficiencies without strong central oversight.

- •

Dependence on commission-based revenue makes it susceptible to insurance market cycles and economic pressures.

Opportunities

- •

Further expansion into high-growth international markets.

- •

Investing in or acquiring Insurtech companies to enhance digital capabilities, data analytics, and client experience.

- •

Growing the fee-based consulting business, particularly in emerging risk areas like ESG and cyber.

- •

Market consolidation continues to provide a rich pipeline for strategic acquisitions.

Threats

- •

Intense competition from other large global brokers (e.g., Marsh McLennan, Aon) and private equity-backed consolidators.

- •

Emergence of Insurtech startups and direct-to-consumer models threatening traditional broker roles.

- •

A prolonged 'soft' insurance market could compress premium rates and, consequently, commission revenues.

- •

Increased regulatory scrutiny on broker compensation and transparency.

Recommendations

Priority Improvements

- Area:

Digital Client Experience

Recommendation:Accelerate the development of a unified, data-driven digital platform for clients. This platform should provide self-service options for smaller clients and sophisticated risk management dashboards for larger enterprises, creating efficiencies and a consistent brand experience across acquired entities.

Expected Impact:High

- Area:

Post-Acquisition Integration

Recommendation:Develop a 'Center of Excellence' for technology and operations to streamline the integration of newly acquired agencies. This would accelerate the adoption of best practices, harmonize core systems, and unlock cross-selling opportunities faster.

Expected Impact:Medium

- Area:

Talent Development

Recommendation:Formalize a company-wide 'Next Generation Leadership' program to attract and retain top talent. This should focus on developing skills in data analytics, consultative selling, and leadership to ensure a sustainable talent pipeline that can navigate the future of the industry.

Expected Impact:High

Business Model Innovation

- •

Launch a proprietary data and analytics service, leveraging anonymized claims and policy data to offer clients paid benchmarking, risk modeling, and predictive analytics services.

- •

Develop a 'Brokerage-as-a-Service' platform that offers smaller, independent agencies access to Brown & Brown's market access, technology stack, and back-office services for a subscription or fee-per-use basis.

- •

Create captive insurance management services for mid-market clients, moving beyond a pure brokerage role to help them create their own insurance vehicles, generating a stable, high-margin fee income.

Revenue Diversification

- •

Systematically expand the fee-for-service risk management and advisory practice, with a focus on non-insurable risks like supply chain, reputation, and ESG strategy.

- •

Build or acquire a Managing General Agent (MGA) in a key specialty area to capture underwriting profit in addition to distribution commissions.

- •

Invest in Insurtech startups that are developing complementary technologies and establish reseller or partnership agreements to offer their services to Brown & Brown's client base.

Brown & Brown, Inc. operates a highly successful and mature business model, firmly positioned as a major player in the global insurance brokerage industry. The company's core strength lies in its unique synthesis of a decentralized, entrepreneurial culture with a disciplined and aggressive M&A strategy. This allows it to maintain the agility and client-centricity of a local firm while leveraging the scale, resources, and market access of a global enterprise. Its diversified revenue streams across various segments and client types provide significant resilience against market volatility.

The strategic evolution of the business model should be focused on two key pillars: digitalization and service expansion. While the current model is robust, it faces long-term threats from Insurtech-driven disintermediation and commission compression. To mitigate this, Brown & Brown must evolve from a pure intermediary to a more integrated risk advisor. The primary strategic imperative is to invest in a unified digital client experience that can streamline service delivery, unlock data-driven insights, and create operational leverage across its vast network of offices.

Furthermore, a deliberate strategy to grow high-margin, fee-based consulting services will be critical for future revenue optimization and reducing dependence on commission cycles. By innovating around data monetization, platform services, and deeper risk advisory, Brown & Brown can solidify its value proposition, enhance client retention, and build a more sustainable competitive advantage for the next decade.

Competitors

Competitive Landscape

Mature

Moderately concentrated at the top, with a few global players (Marsh McLennan, Aon, Gallagher) holding significant share, but highly fragmented overall with thousands of smaller, regional, and specialized firms.

Barriers To Entry

- Barrier:

Regulatory Licensing & Compliance

Impact:High

- Barrier:

Building Carrier Relationships

Impact:High

- Barrier:

Client Trust and Relationship Building

Impact:High

- Barrier:

Capital Requirements for M&A

Impact:Medium

- Barrier:

Specialized Expertise & Talent Acquisition

Impact:Medium

Industry Trends

- Trend:

Digital Transformation & Insurtech Adoption

Impact On Business:Requires significant investment in technology to improve client experience, operational efficiency, and data analytics to remain competitive with both large brokers and nimble startups.

Timeline:Immediate

- Trend:

Market Consolidation (M&A)

Impact On Business:This is a core part of Brown & Brown's growth strategy. Continued consolidation creates both acquisition opportunities and larger, more formidable competitors.

Timeline:Immediate

- Trend:

Increased Demand for Specialization

Impact On Business:Clients are seeking deep expertise in niche areas like cyber insurance, climate risk, and professional liability. This plays to Brown & Brown's strengths in specialized programs but requires continuous talent development.

Timeline:Immediate

- Trend:

Data Analytics and AI for Risk Management

Impact On Business:Large competitors are leveraging proprietary data to offer advanced risk modeling. Brown & Brown needs to enhance its analytical capabilities to provide similar value-added services beyond traditional brokerage.

Timeline:Near-term

- Trend:

Talent Scarcity

Impact On Business:An aging workforce and competition from other financial and tech sectors make attracting and retaining top talent a significant challenge, impacting service quality and growth potential.

Timeline:Near-term

Direct Competitors

- →

Marsh & McLennan Companies (MMC)

Market Share Estimate:Leading (Typically #1 globally by revenue)

Target Audience Overlap:High

Competitive Positioning:Global leader in risk, strategy, and people, focusing on large, complex, and multinational clients with a data-driven, consultative approach.

Strengths

- •

Unmatched global scale and brand recognition.

- •

Deep expertise across a wide range of industries and risk types.

- •

Extensive proprietary data and analytics capabilities (Marsh Analytics).

- •

Strong relationships with global insurance carriers.

- •

Diversified revenue streams from consulting (Mercer, Oliver Wyman).

Weaknesses

- •

Potential for bureaucracy and slower decision-making due to size.

- •

Higher cost structure may make them less competitive for mid-market clients.

- •

Integration challenges from large-scale acquisitions can impact client service consistency.

- •

Can be perceived as less agile than smaller competitors.

Differentiators

- •

Comprehensive suite of services beyond brokerage (e.g., management consulting).

- •

Industry-leading research and thought leadership.

- •

Global reach capable of servicing the world's largest corporations.

- →

Aon plc

Market Share Estimate:High (Typically #2 globally by revenue)

Target Audience Overlap:High

Competitive Positioning:Positions itself as a professional services firm providing data-driven insights on risk, retirement, and health to protect and enrich the lives of people globally.

Strengths

- •

Strong global presence and brand recognition.

- •

Advanced data analytics and technology platforms (e.g., Aon's CoverWallet for SMEs).

- •

Leader in human capital and employee benefits solutions.

- •

Highly innovative in creating new risk transfer solutions (e.g., intellectual property).

- •

Strong M&A and strategic partnership capabilities.

Weaknesses

- •

Complex organizational structure.

- •

High-profile failed merger with WTW created some market uncertainty.

- •

Can face similar large-company agility challenges as MMC.

- •

Premium pricing for services.

Differentiators

- •

Emphasis on data and analytics to make better decisions ('Aon United').

- •

Focus on 'new-age' risks like IP, cyber, and pandemic risk.

- •

Strong integration of health, wealth, and commercial risk solutions.

- →

Arthur J. Gallagher & Co. (AJG)

Market Share Estimate:Significant (Top 3-4 globally)

Target Audience Overlap:High

Competitive Positioning:Culturally-focused broker serving mid-market to large clients with a community-based, ethical approach. Known for its strong sales culture and M&A integration.

Strengths

- •

Very strong and distinct corporate culture ('The Gallagher Way').

- •

Successful and prolific M&A strategy, particularly in the middle market.

- •

Deep niche industry expertise.

- •

Strong organic growth performance.

- •

Balanced portfolio across property/casualty and employee benefits.

Weaknesses

- •

Less global reach than MMC or Aon.

- •

Brand recognition may be lower than the top two outside of core markets.

- •

Potential for cultural dilution or integration friction with rapid M&A.

- •

Historically less emphasis on proprietary high-tech platforms compared to Aon.

Differentiators

- •

Emphasis on ethics and a unique corporate culture as a competitive advantage.

- •

Strong focus on the middle-market client segment.

- •

Decentralized model empowering local brokers, similar to Brown & Brown.

- →

Hub International

Market Share Estimate:Significant (Top 10 globally)

Target Audience Overlap:High

Competitive Positioning:A leading North American broker focused on providing tailored solutions through specialized industry practices, particularly for middle-market companies.

Strengths

- •

Aggressive and successful M&A strategy driving rapid growth.

- •

Deep specialization in key industries (e.g., Transportation, Construction, Healthcare).

- •

Strong presence across North America.

- •

Privately held, which can allow for longer-term strategic focus without public market pressure.

Weaknesses

- •

Limited global footprint compared to MMC, Aon, and AJG.

- •

Brand is less of a household name globally.

- •

Potential integration and consistency challenges from high volume of acquisitions.

- •

Highly leveraged due to private equity ownership model.

Differentiators

- •

Organized around industry-specific 'HUBs' to provide deep expertise.

- •

Strong focus on the North American middle market.

- •

Private equity backing enables aggressive growth posture.

Indirect Competitors

- →

Insurtech MGAs & Digital Brokers (e.g., Embroker, Coalition, Next Insurance)

Description:Technology-first companies that use data and AI to offer specialized insurance products (like cyber or D&O) or business insurance directly to SMEs, often with a streamlined digital purchasing experience.

Threat Level:Medium

Potential For Direct Competition:High, especially in the small to mid-market (SME) segment where digital-first solutions are gaining traction.

- Name:

HR & Payroll Platforms (e.g., Gusto, Zenefits)

Description:These platforms embed employee benefits brokerage services directly into their HR and payroll software, simplifying the process for small businesses and capturing clients at a key administrative touchpoint.

Threat Level:Medium

Potential For Direct Competition:Medium, primarily by eroding the employee benefits client base in the small business sector.

- Name:

Professional Employer Organizations (PEOs) (e.g., TriNet, ADP TotalSource)

Description:PEOs co-employ a company's staff and handle all HR functions, including sourcing and administering employee benefits. They compete by offering a fully outsourced HR solution, of which insurance is a key component.

Threat Level:Low

Potential For Direct Competition:Low, as they offer a fundamentally different, all-encompassing service model rather than just brokerage.

- Name:

Direct-to-Business Insurance Carriers

Description:Established insurance carriers that are increasingly building out their own direct sales channels to sell business insurance online, bypassing brokers for simpler risks and smaller accounts.

Threat Level:Low

Potential For Direct Competition:Medium, as they could disintermediate brokers for less complex, high-volume commercial lines.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Decentralized Operating Model

Sustainability Assessment:Brown & Brown's model empowers local leaders, fostering entrepreneurialism, agility, and deep client relationships, which is hard for centralized competitors to replicate.

Competitor Replication Difficulty:Hard

- Advantage:

Proven M&A Integration Capability

Sustainability Assessment:The company has a long and successful history of acquiring and integrating smaller brokerages, making it a preferred acquirer and a key driver of consistent growth.

Competitor Replication Difficulty:Medium

- Advantage:

Strong, Stable Culture and Leadership

Sustainability Assessment:Long-term family leadership and a consistent culture provide stability and a clear strategic vision that is difficult for competitors, especially those driven by private equity, to match.

Competitor Replication Difficulty:Hard

Temporary Advantages

{'advantage': 'Expertise in Niche Programs', 'estimated_duration': '1-3 Years. While currently a strength, competitors can acquire or develop similar expertise in high-growth niches over time.'}

Disadvantages

- Disadvantage:

Lower Brand Recognition vs. 'Big Three'

Impact:Major

Addressability:Difficult

- Disadvantage:

Potential for Disjointed Digital Client Experience

Impact:Major

Addressability:Moderately

- Disadvantage:

Less Investment in Proprietary Global Tech Platforms

Impact:Major

Addressability:Difficult

Strategic Recommendations

Quick Wins

- Recommendation:

Optimize Digital Lead Capture Forms

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Amplify Thought Leadership Content

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Launch Targeted Digital Ad Campaigns

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Develop a Unified Digital Client Portal

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Invest in a Centralized Data Analytics Hub

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Establish a Formalized Insurtech Partnership Program

Expected Impact:Medium

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Strategic Acquisitions in Data/Analytics and Insurtech

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Build a Cohesive Global Brand Identity

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Develop Proprietary Risk Management Technology

Expected Impact:High

Implementation Difficulty:Difficult

Solidify Brown & Brown's position as the premier alternative to the 'Big Three' for upper-middle-market and specialized large accounts, emphasizing a superior, relationship-based service model powered by its decentralized structure, but increasingly enabled by centralized technology and data insights.

Differentiate through a 'Best of Both Worlds' approach: the local expertise, agility, and personal touch of a regional broker combined with the national resources, carrier access, and specialty programs of a global powerhouse. This narrative directly counters the bureaucracy of larger competitors and the limited capabilities of smaller ones.

Whitespace Opportunities

- Opportunity:

Develop a 'Digital-First' Brokerage Model for Underserved SME Niches

Competitive Gap:Many Insurtechs lack deep brokerage expertise, while traditional brokers are often inefficient in serving smaller, specialized commercial clients.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Create Integrated Risk & Benefits Solutions for the Distributed Workforce

Competitive Gap:Few brokers have holistically addressed the unique confluence of risks (cyber, liability, workers' comp) and benefits challenges created by permanent remote and hybrid work models.

Feasibility:High

Potential Impact:Medium

- Opportunity:

Offer Brokerage-as-a-Service via APIs

Competitive Gap:Vertical SaaS platforms (e.g., in construction, logistics, healthcare) want to embed insurance offerings but lack the brokerage licenses and expertise. Brown & Brown could power this through APIs.

Feasibility:Low

Potential Impact:High

Brown & Brown operates in the mature and highly competitive insurance brokerage industry, where it has carved out a strong position as the 6th largest broker of U.S. business. The market is dominated at the top by global behemoths like Marsh & McLennan, Aon, and Gallagher, which compete on scale, global reach, and increasingly, proprietary data analytics. Brown & Brown's key sustainable competitive advantage is its unique decentralized operating model, which fosters an entrepreneurial culture, deep client relationships, and agility—a stark contrast to the potential bureaucracy of its larger rivals. This model, combined with a highly effective M&A strategy, has fueled consistent growth.

The primary competitive threats come from two directions. First, the larger global brokers who are investing heavily in technology and data, potentially creating a service gap in sophisticated, analytics-driven risk management. Second, a wave of nimble Insurtech startups and digital-first competitors are targeting the less complex, high-volume SME market with streamlined user experiences, threatening to erode the lower end of the client base.

Brown & Brown's key challenge is to leverage its strengths while mitigating its weaknesses. The decentralized structure that makes it agile can also lead to a fragmented digital client experience and slower adoption of centralized technologies. While its brand is strong within the industry, it lacks the broad global recognition of the top-tier competitors, which can be a disadvantage when pursuing the largest multinational accounts.

Strategic whitespace exists in bridging the gap between traditional brokerage and modern Insurtech. There is a significant opportunity to develop a 'digital-first' service model for specialized SME segments that larger brokers find inefficient and Insurtechs lack the expertise to serve. Furthermore, offering integrated solutions for emerging risks, such as those associated with a distributed workforce, could create a new, defensible market niche.

To succeed, Brown & Brown must pursue a dual strategy: continue to lean into its cultural and structural advantages in the mid-to-large account space while strategically investing in technology to unify its client experience, enhance data analytics capabilities, and build a more efficient service model for smaller clients. This involves not just acquiring companies, but acquiring technology and talent that can be scaled across its network, turning its decentralized model into a technologically enabled competitive weapon.

Messaging

Message Architecture

Key Messages

- Message:

Growth Has No Finish Line

Prominence:Primary

Clarity Score:Medium

Location:Homepage Hero Banner (US)

- Message:

Delivering solutions for you, every step of the way

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Sub-headline (US)

- Message:

Our team is with you along your growth journey to help find solutions that meet your ever-evolving insurance needs.

Prominence:Secondary

Clarity Score:High

Location:Homepage Body Copy (US)

- Message:

Secure Your Trade and Professional Ventures with Specialised Insurance Coverage

Prominence:Primary

Clarity Score:High

Location:Service Page Hero Banner (UK)

- Message:

The Trade and Professional team at Brown & Brown aim to find our customers comprehensive insurance cover that meets the individual needs of each business.

Prominence:Secondary

Clarity Score:High

Location:Service Page Body Copy (UK)

The message hierarchy is generally effective. The US homepage leads with a broad, aspirational concept ('Growth') and then narrows down to supportive partnership ('every step of the way') and specific capabilities. The UK service page is more direct, leading with the specific solution ('Specialised Insurance Coverage') for a targeted audience, which is appropriate. The hierarchy successfully guides different audiences from abstract concepts to concrete services.

Messaging is consistent in its core premise of providing tailored solutions through an expert team. However, the tone and framing shift significantly between the broad US homepage and the specific UK service page. The US site focuses on an aspirational 'growth journey,' while the UK site is grounded in practical risk mitigation ('minimise your risk and uncertainty'). This is an effective adaptation for different audiences rather than a problematic inconsistency.

Brand Voice

Voice Attributes

- Attribute:

Supportive Partner

Strength:Strong

Examples

- •

Our team is with you along your growth journey...

- •

Delivering solutions for you, every step of the way

- •

...our team at Brown & Brown will take the time to understand these needs...

- Attribute:

Expert & Experienced

Strength:Moderate

Examples

- •

...our experienced teams can help to find solutions...

- •

Julie Turpin Shares Insightful Perspective...

- •

Secure Your Trade and Professional Ventures with Specialised Insurance Coverage

- Attribute:

Corporate & Professional

Strength:Strong

Examples

- •

highly complex multinational enterprise

- •

Investor Relations

- •

Mergers & Acquisitions

Tone Analysis

Reassuring

Secondary Tones

- •

Aspirational

- •

Professional

- •

Helpful

Tone Shifts

The tone shifts from aspirational and conceptual on the US homepage to practical and direct on the UK trade professionals page.

Voice Consistency Rating

Good

Consistency Issues

The voice is consistently professional but lacks a strong, distinctive personality that would differentiate it from competitors. It occasionally relies on generic corporate language like 'delivering solutions' and 'capabilities'.

Value Proposition Assessment

Brown & Brown acts as a long-term, trusted partner that provides customized insurance and risk management solutions to support clients at every stage of their growth, from individuals to multinational enterprises.

Value Proposition Components

- Component:

Scalability & Versatility

Clarity:Clear

Uniqueness:Somewhat Unique

Evidence:Addresses audiences from 'a highly complex multinational enterprise, an individual or anything in between.'

- Component:

Long-Term Partnership

Clarity:Clear

Uniqueness:Unique

Evidence:Framed as a 'growth journey' rather than a transactional service.

- Component:

Tailored Expertise

Clarity:Somewhat Clear

Uniqueness:Common

Evidence:Mentions 'experienced teams' and finding 'comprehensive insurance cover that meets the individual needs of each business.'

The primary differentiator is the framing of insurance as a component of a 'growth journey'. This positions Brown & Brown as a strategic partner rather than just a vendor, which is a powerful narrative. However, the website messaging could do more to substantiate this claim with concrete examples or case studies showing how they've facilitated growth. Major competitors like Marsh McLennan and Aon also emphasize partnership, but the 'growth' angle is a potentially strong hook for Brown & Brown.

The messaging positions Brown & Brown as a more relationship-focused and adaptable partner compared to potentially more rigid, larger competitors. It targets a wide market, from individuals to large enterprises, suggesting they can offer the personalized service of a smaller firm with the resources of a large one. This 'best of both worlds' position is appealing but requires more proof to be fully credible.

Audience Messaging

Target Personas

- Persona:

C-Suite/Decision-Maker at a Large Enterprise (US Homepage)

Tailored Messages

- •

Growth Has No Finish Line.

- •

...highly complex multinational enterprise...

- •

Mergers & Acquisitions

Effectiveness:Somewhat

- Persona:

Small Business Owner / Self-Employed Professional (UK Page)

Tailored Messages

- •

Secure Your Trade and Professional Ventures with Specialised Insurance Coverage

- •

Trade and Professional Insurance is a type of insurance coverage that is designed to meet the unique needs of self-employed individuals and small businesses...

- •

Ready to help minimise your risk and uncertainty?

Effectiveness:Effective

Audience Pain Points Addressed

- •

The complexity and constant evolution of insurance needs.

- •

The financial risk of unforeseen circumstances (e.g., legal liabilities, property damage).

- •

The need for specialized coverage for unique trades and professions.

Audience Aspirations Addressed

- •

Continuous business and personal growth.

- •

Financial stability and peace of mind.

- •

Focusing on core work without worrying about potential risks.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Ambition / Aspiration

Effectiveness:Medium

Examples

Growth Has No Finish Line

- Appeal Type:

Security / Peace of Mind

Effectiveness:High

Examples

- •

Our team is with you along your growth journey...

- •

Ready to help minimise your risk and uncertainty?

- •

Trade & Professional Insurance can provide the peace of mind you need...

Social Proof Elements

- Proof Type:

Expertise & Thought Leadership

Impact:Moderate

Evidence:The 'News & Insights' section featuring articles, podcasts, and webinars from company leaders.

Trust Indicators

- •

Professional website design

- •

Clear articulation of services

- •

Thought leadership content (News & Insights)

- •

Prominent contact and location information

- •

Mention of 'trusted team' and 'experienced teams'

Scarcity Urgency Tactics

None observed in the provided content, which is appropriate for the industry and brand positioning.

Calls To Action

Primary Ctas

- Text:

GET IN TOUCH

Location:Homepage Hero

Clarity:Clear

- Text:

Request a Quote

Location:UK Service Page Hero

Clarity:Clear

- Text:

CONTACT US

Location:Homepage Footer Section, UK Service Page Body

Clarity:Clear

The CTAs are clear, well-placed, and contextually appropriate. The UK page uses a more direct, high-intent CTA ('Request a Quote') which is fitting for a specific service page. The US homepage uses a softer, lower-commitment CTA ('GET IN TOUCH') which is suitable for a broader audience at an earlier stage of consideration. The effectiveness could be improved by adding value propositions to the CTAs, e.g., 'Get a Custom Quote' or 'Talk to a Growth Specialist'.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of Tangible Proof: The site is missing customer testimonials, case studies, or specific success metrics that would substantiate the 'growth journey' promise.

- •

Process Obscurity: The messaging explains what Brown & Brown does (finds solutions) but not how they do it. There's no clear articulation of their consultative process or methodology.

- •

Human Element: Despite mentioning a 'trusted team,' the website lacks photos, bios, or stories about the actual people who deliver the service, making the brand feel more corporate than personal.

Contradiction Points

No direct contradictions were found. However, there is a potential disconnect between the high-level, aspirational messaging about 'growth' and the inherently risk-averse nature of the insurance products being sold.

Underdeveloped Areas

Brand Storytelling: The history and values of the company are not communicated. Why should a customer choose Brown & Brown beyond its stated capabilities?

Competitive Differentiation: While the 'growth' angle is a good start, the messaging does not explicitly state what makes their approach or solutions superior to those of other major brokerages.

Messaging Quality

Strengths

- •

Strong, aspirational core theme ('Growth Journey') that attempts to elevate the brand beyond a commodity service.

- •

Effective message segmentation between broad audiences (US homepage) and niche audiences (UK service page).

- •

Clear and consistent focus on partnership and support.

- •

Clean, professional language that inspires confidence.

Weaknesses

- •

Over-reliance on abstract corporate language ('solutions', 'capabilities') without concrete examples.

- •

Lack of social proof (testimonials, case studies) to build trust and credibility.

- •

The value proposition feels more asserted than demonstrated.

- •

Missed opportunities to humanize the brand and showcase their expert team.

Opportunities

- •

Develop customer success stories that explicitly link Brown & Brown's services to a client's growth.

- •

Create content that demystifies the insurance process, reinforcing their role as a helpful partner.

- •

Introduce a 'Meet Our Team' section to showcase the expertise and personality of their brokers.

- •

Quantify their impact where possible (e.g., 'We've helped X businesses navigate complex M&A insurance needs').

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition Substantiation

Recommendation:Create a 'Client Stories' or 'Case Studies' section featuring short, impactful narratives of how Brown & Brown helped specific types of clients overcome challenges and achieve growth. Use direct quotes and, if possible, client logos.

Expected Impact:High

- Area:

Homepage Clarity

Recommendation:Refine the homepage sub-headline to more directly connect 'growth' with 'protection'. For example: 'Growth Has No Finish Line. We protect your journey, every step of the way.'

Expected Impact:Medium

- Area:

Humanize the Brand

Recommendation:Add high-quality photos and short bios of key team members or regional leaders to relevant pages to build a personal connection and reinforce the 'trusted team' message.

Expected Impact:Medium

Quick Wins

- •

Incorporate client testimonials directly onto the homepage and key service pages.

- •

Rewrite generic phrases like 'Discover Our Capabilities' to be more benefit-oriented, such as 'Insurance Solutions Built For Your Business'.

- •

Add a short sentence to the 'Get in Touch' CTA section that sets expectations, e.g., 'Contact us for a no-obligation review of your current coverage.'

Long Term Recommendations

- •

Develop a comprehensive content marketing strategy around the 'growth journey' theme, creating targeted content (webinars, articles, checklists) for businesses at different stages (startup, expansion, M&A, maturity).

- •

Build out dedicated industry-specific landing pages that speak directly to the unique risks and growth challenges of key sectors.

- •

Invest in video content, including client testimonials and 'meet the expert' interviews, to make the brand more dynamic and personable.

Brown & Brown's strategic messaging successfully positions the company as more than an insurance broker; it aspires to be a strategic partner for growth. The core message, 'Growth Has No Finish Line,' is a powerful, aspirational concept that differentiates it from competitors who may focus solely on risk mitigation or price. The message architecture effectively adapts from this high-level vision on the US homepage to a practical, solution-focused approach on specific service pages, demonstrating an understanding of audience segmentation.

The primary weakness in the current strategy is the gap between the promise and the proof. The website asserts its value through phrases like 'trusted team' and 'experienced teams' but fails to provide the tangible evidence—such as case studies, client testimonials, or detailed process descriptions—that would make these claims fully credible. This reliance on abstract corporate language ('solutions,' 'capabilities') makes the messaging feel professional but impersonal and less compelling than it could be.

To elevate its market position and improve customer acquisition, Brown & Brown should focus on substantiating its core value proposition. The immediate priority is to inject social proof and human elements across the site. By showcasing real-world examples of how they've guided clients through their 'growth journey' and by introducing the experts behind the advice, Brown & Brown can transform its aspirational message into a believable and compelling reason to choose them over the competition.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

A publicly traded company (NYSE: BRO) with a market capitalization of over $30 billion, indicating significant market validation.

- •

Consistent revenue growth, reporting $4.8 billion in GAAP revenues for the full year 2024, a 12.9% increase from 2023.

- •

Long-standing history, founded in 1939, demonstrating decades of sustained operations and adaptation to market needs.

- •

Comprehensive service offerings covering Property & Casualty, Employee Benefits, Personal Insurance, and various specialized markets, catering to a wide range of clients from individuals to multinational enterprises.

Improvement Areas

- •

Enhancing digital client-facing tools for the SME and personal lines segments to compete with Insurtech disruptors.

- •

Developing a more unified customer experience across its decentralized and acquired entities.

- •

Strengthening data analytics capabilities to provide more advanced risk management advisory services beyond traditional brokerage.

Market Dynamics

Approx. 8-9% annually. The global insurance brokerage market is projected to grow at a CAGR of 8.2% to 9.2% between 2024 and 2030.

Mature

Market Trends

- Trend:

Industry Consolidation via M&A

Business Impact:Continued M&A activity is a primary growth driver but also increases competition for acquiring quality firms. Effective post-merger integration is critical for realizing value.

- Trend:

Digital Transformation & Insurtech

Business Impact:Clients increasingly expect digital-first experiences. Investment in AI, data analytics, and automation is necessary to improve efficiency, enhance client service, and remain competitive.

- Trend:

Demand for Specialization

Business Impact:Clients require deep expertise in niche areas like cyber risk, climate change, and complex liability. This creates opportunities for specialty divisions and targeted acquisitions.

- Trend:

Evolving Regulatory Landscape

Business Impact:Increasingly complex compliance requirements (e.g., data privacy, ESG) necessitate sophisticated advisory services, representing both a risk and a revenue opportunity.

- Trend:

Talent Shortage

Business Impact:An aging workforce and a shortage of new talent in the insurance industry can constrain growth and increase operational costs.

Favorable. The market is robust with steady growth. Brown & Brown's scale and aggressive M&A strategy position it well to capitalize on consolidation and specialization trends.

Business Model Scalability

High

Scalable, with a significant portion of costs being variable (e.g., broker commissions). M&A allows for rapid, albeit complex, scaling of revenue and market presence.

High. Brown & Brown's decentralized model empowers local teams, fostering an ownership culture that drives sales. National resources support local operations, creating leverage. Recent reorganization to a new 'Specialty Distribution' segment aims to further enhance synergies.

Scalability Constraints

- •

Cultural and systems integration challenges following numerous acquisitions.

- •

Dependence on acquiring and retaining high-performing brokers and specialized talent.

- •

Maintaining consistent service quality and brand identity across a globally decentralized network.

Team Readiness

Strong and experienced executive team with a clear, articulated growth strategy centered on disciplined M&A and organic growth.

A historically effective decentralized structure that promotes local autonomy. Recent reorganization into two core segments (Retail and Specialty Distribution) is a proactive move to streamline operations and integrate large acquisitions like Accession Risk Management Group.

Key Capability Gaps

- •

Advanced Data Science & Predictive Analytics: Need to build deeper capabilities to translate data into proactive risk advisory products.

- •

Digital Product Management: Requires talent to build and manage digital platforms for direct-to-client or self-service models.

- •

Cybersecurity Expertise: Growing in-house capabilities to address the escalating threat landscape for both the company and its clients.

Growth Engine

Acquisition Channels

- Channel:

Mergers & Acquisitions (M&A)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Develop a Center of Excellence for post-merger integration to accelerate synergy realization and standardize best practices across acquired firms. The recent $9.8B acquisition of Accession is a prime example of this strategy's scale.

- Channel:

Direct Sales & Broker Relationships

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip sales teams with advanced analytics and CRM tools to identify cross-selling opportunities and better predict client needs.

- Channel:

Digital Marketing & Content

Effectiveness:Low

Optimization Potential:High

Recommendation:Invest in a robust content strategy (insights, webinars, podcasts) targeted at specific industry verticals to generate qualified inbound leads for high-margin specialty lines. The current website serves as a brochure, not a lead-generation engine.

- Channel:

Referral Partnerships

Effectiveness:Medium

Optimization Potential:High

Recommendation:Formalize strategic partnerships with professional services firms (e.g., law firms, accounting firms, wealth managers) to create a systematic referral pipeline.

Customer Journey

High-touch, relationship-driven sales process. The website acts as a digital storefront for initial discovery, leading to offline engagement with a broker.

Friction Points

- •

Transition from online inquiry ('Get in Touch') to the appropriate local broker can be slow or inconsistent.

- •

Lack of self-service options for smaller commercial or personal lines clients who expect a more digital-native experience.

- •

Onboarding process for new clients, particularly post-acquisition, may vary in quality and efficiency.

Journey Enhancement Priorities

{'area': 'Digital Onboarding', 'recommendation': 'Implement a digital onboarding platform for SME clients to streamline data collection, initial quoting, and policy binding, reducing manual effort and improving client experience.'}

{'area': 'Client Portal', 'recommendation': 'Develop a unified client portal that provides access to policy documents, risk management resources, and claims information, regardless of which Brown & Brown entity services the account.'}

Retention Mechanisms

- Mechanism:

Dedicated Broker Relationship

Effectiveness:High

Improvement Opportunity:Augment broker expertise with AI-powered tools that provide proactive alerts on emerging risks or coverage gaps for their clients.

- Mechanism:

Cross-Selling Services

Effectiveness:Medium

Improvement Opportunity:Systematically analyze client portfolios to identify and incentivize cross-selling of additional lines (e.g., P&C clients who lack cyber or D&O coverage). This is a key synergy driver for M&A.

- Mechanism:

Value-Added Services (e.g., Risk Management)

Effectiveness:Medium

Improvement Opportunity:Productize risk management and consulting services. Offer tiered service levels that can be upsold to clients seeking more than just transactional brokerage.

Revenue Economics

Strong. The business model is characterized by high client retention rates and recurring commission-based revenue, leading to a high Lifetime Value (LTV).

Likely Highly Favorable. While precise figures are unavailable, the high client retention inherent in the insurance brokerage industry combined with significant cross-sell and upsell potential suggests a strong LTV relative to client acquisition costs.

High. Demonstrated by consistent organic revenue growth (10.4% for 2024) and strong adjusted EBITDAC margins (35.2% for 2024), indicating efficient conversion of resources into revenue.

Optimization Recommendations

- •

Increase revenue per client by systematically bundling risk advisory services with brokerage.

- •

Reduce cost-to-serve for smaller clients through automation and digital self-service tools.

- •

Improve client acquisition efficiency by investing in lower-cost digital channels to supplement the traditional sales-led approach.

Scale Barriers

Technical Limitations

- Limitation:

Fragmented Technology Stack

Impact:High

Solution Approach:Develop a multi-year technology roadmap focused on creating a unified data platform and standardizing core systems (CRM, Broker Management System) across the organization to enable a single view of the customer.

- Limitation:

Legacy Core Systems

Impact:Medium

Solution Approach:Prioritize modernization of legacy systems that inhibit the rapid launch of new digital products or create data silos. Adopt an API-first architecture to facilitate integration with Insurtech partners.

Operational Bottlenecks

- Bottleneck:

Post-Acquisition Integration

Growth Impact:Slows down the realization of synergies and can lead to inconsistent client experiences.

Resolution Strategy:Establish a dedicated M&A integration team responsible for creating and executing a standardized 100-day plan covering technology, culture, and process alignment for all new acquisitions.

- Bottleneck:

Manual Processes and Workflows

Growth Impact:Limits broker productivity and increases operational costs, especially for smaller, more transactional accounts.

Resolution Strategy:Invest in Robotic Process Automation (RPA) and AI to automate routine tasks such as data entry, compliance checks, and basic quoting.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Critical

Mitigation Strategy:Double down on specialization in high-growth, complex niches where deep expertise is a significant differentiator. Key competitors include Marsh McLennan, Aon, Gallagher, and Willis Towers Watson.

- Challenge:

Disruption from Insurtech Startups

Severity:Major

Mitigation Strategy:Develop a 'build, partner, or buy' strategy for technology. Actively partner with or acquire Insurtechs that offer complementary capabilities, particularly in data analytics and digital distribution.

Resource Limitations

Talent Gaps

- •

Data Scientists and AI/ML Engineers

- •

Digital Customer Experience (CX) Designers

- •

Integration Architects for M&A

Significant and ongoing capital required to fund the aggressive M&A strategy. Access to debt and equity markets is crucial. The recent $8.5B capital raise for the Accession acquisition demonstrates this need.

Infrastructure Needs

A modern, cloud-based data warehouse and analytics platform.

A scalable and secure IT infrastructure capable of seamlessly integrating acquired companies.

Growth Opportunities

Market Expansion

- Expansion Vector:

Deeper Penetration in Specialty Lines

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Leverage the newly formed 'Specialty Distribution' segment to build out centers of excellence for high-growth areas like renewable energy, cyber, and transactional liability, using recent acquisitions as the foundation.

- Expansion Vector:

International Market Growth

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Continue strategic 'tuck-in' acquisitions in key international markets (e.g., UK, Canada) to expand global footprint and service multinational clients more effectively.

- Expansion Vector:

Digital-First SME Segment

Potential Impact:Medium

Implementation Complexity:High

Recommended Approach:Launch a separate brand or digital platform targeted at Small and Medium-sized Enterprises (SMEs), offering a streamlined, automated quoting and binding process.

Product Opportunities

- Opportunity:

Proprietary Risk Analytics Platform

Market Demand Evidence:Increasing client demand for data-driven risk management and loss prevention insights beyond simple insurance placement.

Strategic Fit:Moves Brown & Brown up the value chain from broker to strategic risk advisor, creating stickier client relationships.

Development Recommendation:Acquire a specialized risk analytics firm or partner with an Insurtech to co-develop a platform that can be offered to large commercial clients on a subscription basis.

- Opportunity:

Parametric Insurance Products

Market Demand Evidence:Growing interest in parametric coverage for risks like climate events and supply chain disruption, where traditional policies are inadequate.

Strategic Fit:Positions the company as an innovator in risk transfer solutions.

Development Recommendation:Build an in-house team within the 'Specialty Distribution' segment to design and place parametric solutions, partnering with specialized carriers and data providers.

Channel Diversification

- Channel:

Embedded Insurance

Fit Assessment:Good for specific personal and small commercial lines.

Implementation Strategy:Develop APIs to partner with software platforms (e.g., vertical SaaS for contractors, property management software) to offer embedded insurance products at the point of need.

- Channel:

Digital Lead Generation Funnels

Fit Assessment:Excellent for niche specialty areas.

Implementation Strategy:Create targeted digital campaigns with high-value content (e.g., 'The State of Cyber Risk in Healthcare') to capture leads that can be nurtured and passed to specialized broker teams.

Strategic Partnerships

- Partnership Type:

Insurtech Alliances

Potential Partners

- •

Data Analytics Startups (e.g., for predictive risk modeling)

- •

AI-powered Underwriting Platforms

- •

Digital Claims Processing Companies

Expected Benefits:Accelerate digital transformation, gain access to cutting-edge technology without building it from scratch, and enhance service offerings.

- Partnership Type:

Private Equity & Venture Capital Firms

Potential Partners

Mid-market and large-cap PE firms

Expected Benefits:Become the preferred insurance brokerage and risk management partner for their portfolio companies, creating a significant and scalable new business pipeline.

Growth Strategy

North Star Metric

Organic Revenue Growth Rate

While total revenue is heavily influenced by M&A, focusing on organic growth ensures the core business is healthy, client relationships are deepening, and value is being created beyond acquisitions. It is a key metric highlighted by leadership.

Maintain a sustainable organic growth rate that consistently outpaces the industry average (e.g., target 8-10% annually).

Growth Model

Acquisition-Led Compounding Growth

Key Drivers

- •

Disciplined M&A pipeline and execution

- •

Successful post-merger integration and synergy realization

- •

Cross-selling services into acquired client bases

- •

Sustained organic growth in core and specialty segments

Continue the highly successful M&A strategy while simultaneously investing in a centralized integration and digital transformation function to accelerate value creation from acquired assets.

Prioritized Initiatives

- Initiative:

Accelerate Integration of Accession Risk Management Group

Expected Impact:High

Implementation Effort:High

Timeframe:12-18 Months

First Steps:Finalize the leadership structure of the new 'Specialty Distribution' segment and establish cross-functional teams to manage the integration of systems, data, and client relationships.

- Initiative:

Launch a Pilot Digital Brokerage Platform for a Specific SME Niche

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:6-9 Months

First Steps:Identify a target niche (e.g., UK-based professional contractors). Partner with an Insurtech vendor to white-label a digital platform for quoting and binding. Market through targeted digital channels.

- Initiative:

Develop a Proprietary 'Risk Score' for Cyber Insurance Clients

Expected Impact:High

Implementation Effort:High

Timeframe:12 Months

First Steps:Assemble a team of cyber experts, data scientists, and underwriters. Aggregate internal and third-party data to create a predictive model that helps clients understand their cyber posture and allows brokers to negotiate better terms.

Experimentation Plan

High Leverage Tests

{'test': 'A/B test different value propositions on targeted landing pages for specialty lines to measure lead conversion rates.', 'hypothesis': "Focusing on 'risk advisory' rather than 'insurance quotes' will generate higher-quality leads."}

{'test': 'Pilot a subscription-based risk advisory service for 20 mid-market clients.', 'hypothesis': 'Clients are willing to pay a recurring fee for proactive risk management insights, creating a new revenue stream.'}

Use a combination of leading indicators (e.g., qualified leads, pipeline velocity) and lagging indicators (e.g., client retention, revenue per client, organic growth rate).

Quarterly review of key growth experiments and initiatives by a dedicated Growth Council composed of leaders from across the business segments.

Growth Team

A centralized 'Growth & Innovation Office' that works cross-functionally with the Retail and Specialty Distribution segments. This office should include M&A strategy, digital transformation, and corporate marketing.

Key Roles

- •

Head of M&A Integration

- •

Director of Digital Strategy

- •

Head of Data Analytics & Insights

- •

Corporate Development Manager

A combination of hiring external talent for key digital and data roles and upskilling existing brokers through a 'Digital Academy' focused on leveraging new tools and consultative selling techniques.

Brown & Brown, Inc. is in a formidable position for continued growth, built upon a strong foundation as a leading, publicly-traded insurance brokerage. Its primary growth engine—a highly disciplined and aggressive M&A strategy—is proven and effective, as evidenced by consistent revenue growth and the landmark acquisition of Accession Risk Management Group. The company's decentralized operational model fosters an entrepreneurial culture that drives strong organic growth, a critical indicator of core business health.

The market dynamics are favorable, with industry consolidation and a growing demand for specialized risk advisory services playing directly to Brown & Brown's strengths. However, the company faces significant challenges that must be addressed to sustain its trajectory. The primary barrier to scale is not capital, but the operational complexity of integrating dozens of acquisitions. A fragmented technology stack and inconsistent processes can erode margins and dilute the client experience. Furthermore, the threat from nimble, digital-first Insurtech competitors is growing, particularly in less complex market segments.

The key strategic imperative is to evolve from a holding company of acquired brokerages into a truly integrated, tech-enabled risk advisory firm. The growth opportunities lie in leveraging its scale to build proprietary data and analytics capabilities, creating digital channels to efficiently serve the SME market, and productizing its deep expertise into high-margin consulting services.

Recommendations:

1. Prioritize Integration Excellence: Establish a permanent, well-resourced M&A integration function to accelerate synergy realization from the Accession acquisition and future deals.

2. Invest in a Unified Digital Platform: Commit significant resources to building a common technology backbone, including a unified CRM and a client-facing data portal, to create a consistent experience and unlock cross-selling opportunities.

3. Incubate Digital-First Models: Launch targeted digital initiatives, potentially under a separate brand, to capture market share in the SME segment and learn how to compete with Insurtechs.

By successfully merging its M&A prowess with a strategic investment in technology and operational integration, Brown & Brown can solidify its competitive advantage and continue to deliver superior growth and shareholder value.

Legal Compliance

The website demonstrates a mature approach to privacy by providing multiple, region-specific privacy statements accessible from the footer: a general 'Privacy Statement', a 'UK & EU Privacy Statement', and a 'CA Privacy Statement'. This granular approach is a significant strength. The policies are comprehensive, detailing the types of personal information collected (e.g., from website visitors, clients, employees), the purposes for collection (e.g., providing insurance quotes, marketing, analytics), and the legal bases for processing. The presence of distinct policies for the UK/EU and California shows a clear understanding of the need to comply with GDPR and CCPA/CPRA respectively. The policies are reasonably accessible and written in clear language, which is crucial for transparency.

A 'Terms of Use' document is present and easily accessible in the website footer. The terms are clearly written and cover standard, necessary clauses for a corporate website, including intellectual property rights, acceptable use of the site, disclaimers of warranties, and limitations of liability. It also specifies the governing law and jurisdiction for disputes. The enforceability is standard for such click-wrap agreements, providing a solid legal baseline for governing the use of the website.

Upon visiting the site, a prominent cookie consent banner appears. It offers 'Accept All Cookies', 'Reject All Optional Cookies', and 'Manage Cookies' options. This multi-option approach is a best practice under GDPR, as it does not force acceptance and allows for granular user control. The 'Manage Cookies' interface allows users to toggle consent for different categories (Functional, Targeting, Performance), with 'Strictly Necessary Cookies' correctly set to 'Always Active'. A 'Cookies Policy' link is also available, providing detailed information about the types of cookies used. Crucially, the site appears to respect user choice by not loading non-essential trackers before consent is given. An important positive feature is the text 'Your Opt Out Preference Signal is Honored', indicating proactive compliance with Global Privacy Control (GPC) signals mandated by CPRA.