eScore

berkley.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Berkley.com's digital presence reflects its business model, acting as a high-level corporate directory that funnels users to its nearly 60 specialized business units. This decentralized strategy dilutes the parent domain's content authority and visibility for high-intent insurance queries, ceding top-of-funnel awareness to competitors. The site is well-structured for users with existing brand awareness but is not optimized for digital discovery, lacking a centralized hub for thought leadership that would capture broader search intent.

The 'Berkley Locator' tool is an effective digital asset for users in the consideration stage, efficiently routing them to the correct specialized business unit.

Establish a centralized 'Risk & Insights' hub on berkley.com to aggregate expertise from all business units. This would capture significant top-of-funnel search traffic, build domain authority, and position the parent brand as a thought leader.

The brand messaging is exceptionally clear and consistent, effectively communicating its core value proposition of a decentralized, expert-led model backed by Fortune 500 financial strength. The website excels at immediate audience segmentation for 'Agents & Brokers' and 'Businesses & Individuals', creating clear user paths. While the messaging is highly effective at building trust and conveying expertise, it is underdeveloped for the high-net-worth individuals segment.

The core differentiator—a decentralized model combining specialist agility with large-company financial stability—is clearly and consistently articulated across the site.

Either create a dedicated, content-rich user journey for the 'High Net-Worth Individuals' audience to substantiate the homepage claim or remove this messaging to avoid an unsupported promise.

The site's conversion pathways are significantly hindered by critical design flaws, particularly the use of low-contrast 'ghost buttons' for primary calls-to-action. This undermines the site's main goal of funneling users to its locator tool and subsidiary businesses, creating unnecessary friction. While the initial segmentation is strong, content-heavy pages present a high cognitive load with long, unstructured lists, making it difficult for users to find solutions.

The homepage immediately and clearly segments users into 'Agents & Brokers' and 'Businesses & Individuals', which is a very strong foundation for the user journey.

Redesign all primary and secondary call-to-action buttons to use a consistent, high-contrast, solid-fill style. This single, low-effort change would have the most significant impact on guiding users and improving funnel effectiveness.

The company excels at establishing credibility through a strong hierarchy of trust signals, prominently featuring its A+ ratings from A.M. Best and S&P, its Fortune 500 status, and its long history. Its legal and compliance disclosures are mature and robust, particularly concerning the highly regulated US insurance industry. While the foundation is excellent, transparency could be slightly improved by making its GDPR compliance framework more explicit for its European operations.

Prominent and consistent display of top-tier financial strength ratings (A+ from A.M. Best and S&P), which is a critical trust signal for all target audiences in the insurance sector.

Update the Privacy Policy to explicitly name a Data Protection Officer (DPO) or an EU/UK Representative to enhance transparency and solidify its GDPR compliance posture for international partners and clients.

Berkley's competitive moat is exceptionally strong and sustainable, built on its unique decentralized operating model. This structure fosters deep niche expertise and an entrepreneurial culture that is extremely difficult for large, centralized competitors to replicate. This model allows them to expertly price complex risks in underserved markets, creating a significant and defensible advantage. The primary disadvantage is a fragmented brand identity, which is a direct trade-off of this successful model.

The decentralized structure of nearly 60 autonomous, specialist businesses is a deeply embedded and highly sustainable competitive advantage that drives market agility and deep underwriting expertise.

Launch a unified brand marketing campaign focused on the 'Strength of a Fortune 500, agility of a startup' message to help consolidate the brand identity without altering the successful operating model.

The business model is highly scalable due to its decentralized holding company structure, which allows for growth through acquisition or incubation of new units without a proportional increase in central overhead. The company has a proven track record of entering new markets and recently launched Berkley Edge to target underserved SMBs. The primary constraint on scalability is the challenge of implementing enterprise-wide technology and data strategies across dozens of autonomous entities.

The decentralized model is inherently built for expansion, allowing the company to incubate or acquire new, specialized business units to enter emerging markets with high agility.

Establish a centralized 'Data & Analytics Center of Excellence' to provide shared tools and AI-driven insights to all operating units, enhancing scalability by empowering specialists without removing their autonomy.

W. R. Berkley's business model is exceptionally coherent and strategically focused, aligning perfectly with the growing demand for specialty insurance. The dual revenue streams of underwriting profits and investment income provide financial stability, while the decentralized structure directly enables its value proposition of providing nimble, expert-led solutions. The company demonstrates strong resource allocation, focusing on high-margin specialty lines and consistently delivering strong returns on equity.

The entire business model is built around the core strategy of 'empowered decentralization,' where every component—from talent acquisition to revenue generation—is aligned to support and reinforce this unique market position.

Develop a clearer brand architecture that more explicitly connects the nearly 60 operating businesses to the parent Berkley brand, which could enhance cross-selling opportunities and overall market recognition.

Berkley demonstrates significant market power within its chosen specialty niches, evidenced by its ability to maintain underwriting discipline and achieve consistent rate increases. Its focus on complex risks where generic coverage is insufficient gives it substantial pricing power. However, its overall market share in the broader P&C industry is smaller than that of large, diversified competitors, and its brand is less recognized by the general public, reflecting its strategic focus on being a specialist for intermediaries rather than a mass-market brand.

The company has strong pricing power, derived from its deep expertise in underwriting complex, hard-to-place risks that are unattractive to larger, generalist carriers.

Systematically expand into new, high-growth international markets by replicating the successful decentralized model, acquiring local specialty insurers to build global market share in a targeted way.

Business Overview

Business Classification

Insurance Holding Company

Specialty & Commercial Property & Casualty Insurance Provider

Financial Services & Insurance

Sub Verticals

- •

Property & Casualty (P&C) Insurance

- •

Specialty Insurance

- •

Excess & Surplus (E&S) Lines

- •

Reinsurance

- •

Commercial Lines Insurance

Mature

Maturity Indicators

- •

Founded in 1967, demonstrating long-term operational history.

- •

Consistently ranked as a Fortune 500 company (since 2004).

- •

Inclusion in the S&P 500 index since 2019.

- •

Record profitability and revenue reported in recent fiscal years.

- •

Stable dividend history, including special dividends, indicating strong financial health.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Premiums Written

Description:The primary source of revenue, generated from underwriting a diverse portfolio of specialty and commercial property and casualty insurance policies across more than 55 decentralized operating units.

Estimated Importance:Primary

Customer Segment:Commercial Businesses (various niches), High Net-Worth Individuals

Estimated Margin:Medium

- Stream Name:

Net Investment Income

Description:A significant secondary revenue stream generated from investing the 'float' (premiums collected before claims are paid) into a portfolio of assets, primarily fixed-maturity securities. The company reported record net investment income of $1.1 billion in 2023.

Estimated Importance:Secondary

Customer Segment:N/A (Internal capital management)

Estimated Margin:High

- Stream Name:

Fee-Based Services

Description:Revenue generated from providing services such as claims administration, consulting, and risk management to clients, often in conjunction with insurance products.

Estimated Importance:Tertiary

Customer Segment:Commercial Businesses

Estimated Margin:Medium

Recurring Revenue Components

Policy renewals

Ongoing investment income from managed assets

Pricing Strategy

Underwriting-Based Pricing

Premium

Opaque

Pricing Psychology

Value-based pricing (based on specialized expertise and tailored coverage)

Risk-based pricing (actuarial analysis of specific niche risks)

Monetization Assessment

Strengths

- •

Diversified revenue from both underwriting and investment activities provides financial stability.

- •

Focus on niche specialty markets allows for premium pricing and potentially higher underwriting margins.

- •

Decentralized model enables pricing agility to respond to local market conditions and risk profiles.

Weaknesses

- •

Investment income is sensitive to interest rate fluctuations and market volatility.

- •

Underwriting profitability is exposed to catastrophic events and cyclical pricing pressures in the P&C market.

- •

Reliance on an indirect (broker-led) distribution model limits direct control over the end-customer relationship and pricing communication.

Opportunities

- •

Expanding into new, emerging high-growth specialty lines like cyber insurance, cannabis, and renewable energy.

- •

Leveraging data analytics and AI across operating units to refine underwriting, improve pricing accuracy, and enhance risk selection.

- •

Offering more comprehensive fee-based risk management services to deepen client relationships and create new revenue.

Threats

- •

Intense competition from other large, diversified insurers and specialized niche players.

- •

'Social inflation' and rising litigation costs increasing claims severity.

- •

Climate change increasing the frequency and severity of natural catastrophe-related claims.

- •

Regulatory changes impacting capital requirements, pricing, and coverage mandates.

Market Positioning

Niche Specialist with Enterprise Scale

Significant player in U.S. commercial lines, but a laggard in the overall P&C market due to its specialized focus.

Target Segments

- Segment Name:

Independent Agents & Brokers

Description:The primary distribution channel and key partners. These are independent insurance professionals who need access to specialized, reliable insurance products for their clients.

Demographic Factors

Licensed insurance agents/brokers

Varying in size from small independent agencies to large national brokerage firms

Psychographic Factors

- •

Value expertise and responsiveness

- •

Seek long-term, stable partnerships with carriers

- •

Motivated by commissions and ability to serve client needs effectively

Behavioral Factors

Select insurance carriers based on financial strength, product breadth, and ease of doing business

Manage relationships between end-customers and the insurance underwriter

Pain Points

- •

Finding coverage for unique or complex client risks

- •

Slow underwriting and claims processes from large, bureaucratic insurers

- •

Lack of direct access to decision-makers and underwriters

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Niche Commercial Businesses

Description:Small-to-large enterprises in specific industries (e.g., Construction, Agribusiness, Technology, Energy) that require tailored insurance solutions beyond standard 'off-the-shelf' policies.

Demographic Factors

Varies by industry (e.g., number of employees, annual revenue)

Often operate in higher-risk environments

Psychographic Factors

Risk-aware and value deep industry expertise

Prioritize comprehensive coverage and risk management over lowest price

Behavioral Factors

Rely on trusted brokers to find appropriate coverage

Purchase a suite of insurance products (e.g., General Liability, Workers' Comp, Cyber)

Pain Points

- •

Difficulty securing adequate coverage from generalist insurers

- •

Generic policies that don't cover industry-specific risks

- •

Lack of knowledgeable claims handling for their specific business type

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

High Net-Worth Individuals & Families

Description:Affluent individuals and families requiring specialized personal lines insurance for high-value homes, vehicles, collectibles, and liability protection.

Demographic Factors

High income and significant personal assets

Own multiple properties, luxury vehicles, or valuable collections

Psychographic Factors

Value asset protection and personalized service

Seek discretion and a high-touch service model

Behavioral Factors

Often work with private client brokers or financial advisors

Require customized policies and higher liability limits

Pain Points

- •

Standard personal insurance policies have insufficient coverage limits

- •

Lack of understanding from standard insurers about unique assets (e.g., art, classic cars)

- •

Desire for a single point of contact and seamless claims experience

Fit Assessment:Good

Segment Potential:Medium

Market Differentiation

- Factor:

Decentralized Operating Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Niche Market Expertise

Strength:Strong

Sustainability:Sustainable

- Factor:

Financial Strength & Stability

Strength:Strong

Sustainability:Sustainable

- Factor:

Entrepreneurial Culture

Strength:Moderate

Sustainability:Sustainable

Value Proposition

W. R. Berkley provides tailored, expert insurance solutions for niche commercial markets and high-value personal assets through a decentralized network of specialized businesses, combining the agility of a small firm with the financial strength of a Fortune 500 company.

Good

Key Benefits

- Benefit:

Specialized/Tailored Coverage

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Extensive list of specific industries and products served (e.g., Cannabis, Life Sciences, Cyber).

Operation of 55+ distinct insurance businesses, each focused on a niche.

- Benefit:

Financial Strength & Reliability

Importance:Critical

Differentiation:Common

Proof Elements

- •

A+ (Superior) A.M. Best rating.

- •

A+ (Strong) S&P rating.

- •

Fortune 500 and S&P 500 member.

- •

Over 50 years in business.

- Benefit:

Agility and Responsiveness

Importance:Important

Differentiation:Unique

Proof Elements

Emphasis on the 'Decentralized' model allowing local autonomy.

Tagline 'deal with decision makers' from Berkley Specialty London.

Unique Selling Points

- Usp:

A decentralized portfolio of nearly 60 autonomous, entrepreneurial insurance businesses.

Sustainability:Long-term

Defensibility:Strong

- Usp:

Deep, proven expertise in a wide array of underserved and complex niche markets.

Sustainability:Long-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Businesses with unique or complex risks cannot find adequate coverage from standard insurers.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Policyholders and brokers are frustrated by slow, bureaucratic processes at large, centralized insurance companies.

Severity:Major

Solution Effectiveness:Partial

- Problem:

Lack of deep industry knowledge from underwriters and claims adjusters leads to improper coverage and poor claims experience.

Severity:Major

Solution Effectiveness:Complete

Value Alignment Assessment

High

The specialty insurance market is growing faster than standard lines, driven by new and complex risks. Berkley's model is perfectly structured to capitalize on this trend.

High

The value proposition directly addresses the primary pain points of both brokers (finding specialized coverage) and end-customers (getting expert, tailored solutions).

Strategic Assessment

Business Model Canvas

Key Partners

- •

Independent Insurance Agents & Brokers

- •

Reinsurance Companies

- •

Third-Party Administrators (TPAs)

- •

Technology and Data Providers

Key Activities

- •

Underwriting & Risk Assessment

- •

Claims Management & Processing

- •

Investment Management

- •

Product Development for Niche Markets

- •

Broker & Agent Relationship Management

Key Resources

- •

Financial Capital & Reserves

- •

Specialized Underwriting Talent

- •

A.M. Best and S&P Financial Strength Ratings

- •

Brand Reputation & Trust

- •

Portfolio of 55+ Operating Units

Cost Structure

- •

Loss & Loss Adjustment Expenses (LAE)

- •

Acquisition Costs (Broker Commissions)

- •

Salaries & Employee Benefits (Underwriters, Claims Adjusters)

- •

Technology & Infrastructure

- •

Regulatory & Compliance Costs

Swot Analysis

Strengths

- •

Decentralized model fosters agility, specialization, and entrepreneurial drive.

- •

Highly diversified across numerous non-correlated specialty lines, reducing exposure to any single market downturn.

- •

Strong financial ratings and a robust balance sheet build trust and enable growth.

- •

Proven ability to incubate and grow new insurance businesses from the ground up.

Weaknesses

- •

Potential for operational inefficiencies and lack of economies of scale compared to centralized competitors.

- •

Fragmented brand identity due to the large number of distinct operating units.

- •

Heavy reliance on the broker channel makes the business vulnerable to shifts in distribution strategy.

- •

May be slow to implement enterprise-wide technology transformations due to the autonomous nature of its units.

Opportunities

- •

Rapidly growing demand for specialty insurance in areas like cyber, climate, and technology.

- •

Strategic acquisitions of smaller, specialized managing general agents (MGAs) or insurers.

- •

Leveraging AI and machine learning to create a centralized data analytics 'center of excellence' to support all operating units.

- •

Developing innovative insurance products for emerging risks associated with global supply chains, ESG, and the gig economy.

Threats

- •

Increasingly frequent and severe catastrophic weather events straining underwriting results.

- •

Disruption from Insurtech startups that use technology to streamline underwriting and distribution in niche markets.

- •

A prolonged low-interest-rate environment would negatively impact investment income.

- •

Intensifying competition from both large carriers expanding into specialty lines and smaller, highly-focused niche players.

Recommendations

Priority Improvements

- Area:

Technology & Data Integration

Recommendation:Establish a centralized 'Data & Analytics Center of Excellence' to provide shared tools, resources, and AI-driven insights to all operating units. This maintains decentralization in underwriting decisions but centralizes the power of data.

Expected Impact:High

- Area:

Brand Architecture & Cohesion

Recommendation:Develop a clearer brand architecture that connects the 55+ businesses to the parent Berkley brand more explicitly, enhancing cross-selling opportunities and overall market recognition.

Expected Impact:Medium

- Area:

Channel Strategy

Recommendation:Pilot a direct-to-consumer (DTC) or digitally-enabled broker channel for less complex specialty products to diversify distribution and capture data on emerging customer segments.

Expected Impact:Medium

Business Model Innovation

- •

Launch an 'Insurtech Venture Arm' to invest in and partner with startups that can provide technological enhancements (e.g., AI underwriting, drone-based claims assessment) to Berkley's operating units.

- •

Develop a 'Risk Management as a Service' (RMaaS) platform, offering their deep niche expertise on a subscription basis to clients who may not purchase a full insurance policy.

- •

Explore parametric insurance products for specific, measurable risks (e.g., weather events), which offer faster, automated payouts and can be scaled across various business units.

Revenue Diversification

- •

Expand fee-based claims and administrative services (TPA) to a broader market, leveraging the expertise within existing units.

- •

Monetize proprietary risk management data and analytics by offering anonymized, aggregated insights to specific industries.

- •

Increase focus on international markets where demand for specialty insurance is growing, particularly in Asia-Pacific and Latin America.

W. R. Berkley Corporation has built a formidable and highly defensible business model centered on a unique paradox: decentralized specialization at an enterprise scale. Its core strength lies in its portfolio of over 55 autonomous operating units, which act as nimble, expert-driven specialists in distinct niche markets. This structure allows the company to effectively identify, underwrite, and price complex risks that larger, more centralized competitors may overlook or misprice. The model fosters an entrepreneurial culture that attracts and retains top underwriting talent, a critical resource in the specialty insurance sector. Financially, the dual-engine revenue model—combining underwriting profits with substantial investment income—provides resilience and stability.

However, this decentralized model presents inherent strategic challenges. The very autonomy that drives its success can also create barriers to achieving enterprise-wide economies of scale, seamless data integration, and a cohesive brand identity. The primary strategic imperative for future evolution is not to abandon this successful model, but to overlay it with a digital and data-driven connective tissue. By creating centralized centers of excellence for data analytics, AI, and technology, Berkley can empower its specialized units with enhanced tools for risk selection and pricing without compromising their underwriting autonomy. This 'empowered decentralization' would enhance scalability and efficiency.

Looking forward, the market for specialty insurance is projected to grow robustly, outpacing standard P&C lines due to the proliferation of emerging risks like cyber threats and climate change. Berkley is exceptionally well-positioned to capture this growth. Strategic transformation should focus on three key areas: 1) Technological Enablement: Investing in AI and data platforms to augment, not replace, underwriter expertise. 2) Ecosystem Expansion: Moving beyond traditional broker partnerships to include strategic investments in Insurtech. 3) Brand Synergy: Creating clearer pathways for cross-selling and collaboration between its distinct operating units. By evolving its model to be more digitally integrated while preserving its core decentralized, expert-led culture, W. R. Berkley can sustain its competitive advantage and solidify its position as a leader in the evolving landscape of specialized risk.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

Regulatory Compliance & Capital Requirements

Impact:High

- Barrier:

Agent/Broker Distribution Networks

Impact:High

- Barrier:

Brand Recognition & Trust

Impact:High

- Barrier:

Specialized Underwriting Expertise & Data

Impact:High

Industry Trends

- Trend:

Digital Transformation and Insurtech Adoption

Impact On Business:Legacy systems and a decentralized model present challenges for rapid, unified adoption of AI in underwriting, digital claims processing, and providing a seamless customer experience.

Timeline:Immediate

- Trend:

Rising Importance of Cyber Insurance

Impact On Business:Represents a significant growth opportunity. As a specialty insurer, Berkley is well-positioned to capitalize on the increasing demand for sophisticated cyber risk products.

Timeline:Immediate

- Trend:

Climate Change and ESG Considerations

Impact On Business:Increases the frequency and severity of catastrophe losses, requiring more sophisticated underwriting models. There is also growing pressure on investment portfolios to align with ESG principles.

Timeline:Near-term

- Trend:

Social Inflation and 'Nuclear' Verdicts

Impact On Business:Drives up the cost of liability claims beyond standard economic inflation, pressuring underwriting profitability and requiring adjustments in pricing and reserving.

Timeline:Immediate

Direct Competitors

- →

Chubb Limited

Market Share Estimate:Approx. 3.1% of total US P&C market.

Target Audience Overlap:High

Competitive Positioning:Premium global insurer known for underwriting discipline, extensive product offerings, and serving high-net-worth individuals and complex commercial accounts.

Strengths

- •

Strong global brand recognition and reputation.

- •

Deep expertise in high-net-worth personal lines and specialty commercial insurance.

- •

Extensive global footprint and distribution network.

- •

Superior financial strength ratings.

Weaknesses

- •

Can be perceived as more expensive than competitors.

- •

Large size can lead to less agility compared to smaller, more specialized players.

- •

Potentially more bureaucratic and less entrepreneurial culture than Berkley's model.

Differentiators

- •

Masterpiece® home and auto policies for affluent clients.

- •

Broad multinational capabilities and servicing.

- •

Focus on superior claims service as a brand pillar.

- →

The Travelers Companies, Inc.

Market Share Estimate:Approx. 4.0% of total US P&C market.

Target Audience Overlap:High

Competitive Positioning:A leading provider of property and casualty insurance for business, home, and auto, with a strong focus on leveraging data and analytics for underwriting and risk management.

Strengths

- •

One of the largest writers of commercial insurance in the U.S.

- •

Strong agent and broker relationships.

- •

Advanced data and analytics capabilities (e.g., IntelliDrive®).

- •

Broad product portfolio across personal, business, and specialty lines.

Weaknesses

- •

Less focused on niche specialty markets compared to Berkley.

- •

Customer satisfaction ratings can be average in some segments.

- •

May not have the same level of prestige as Chubb in the high-net-worth segment.

Differentiators

- •

Strong position in workers' compensation.

- •

Risk control services and analytics for commercial clients.

- •

Recognizable brand with a long history (founded in 1864).

- →

The Hartford Financial Services Group, Inc.

Market Share Estimate:Among the top 10 for commercial lines.

Target Audience Overlap:High

Competitive Positioning:A major player in small business insurance, group benefits, and mutual funds, often marketing through an exclusive partnership with AARP.

Strengths

- •

Leading market position in small business insurance.

- •

Strong brand recognition, particularly among the AARP demographic.

- •

Expertise in group benefits and disability insurance, offering cross-selling opportunities.

- •

Well-established agent and broker network.

Weaknesses

- •

Less emphasis on the very large, complex, or highly specialized risks that Berkley targets.

- •

Older customer demographic may present long-term growth challenges.

- •

Can be slower to innovate in certain technology areas compared to Insurtechs.

Differentiators

- •

Exclusive partnership with AARP for personal lines.

- •

Strong focus and product suite for small businesses.

- •

Integrated offerings of group benefits and workers' compensation.

- →

CNA Financial Corporation

Market Share Estimate:Significant player in US commercial lines.

Target Audience Overlap:High

Competitive Positioning:One of the largest U.S. commercial property and casualty insurance companies, focusing on businesses of all sizes through a strong agent network.

Strengths

- •

Long-standing history and brand recognition in the commercial space.

- •

Broad appetite for various industries and business sizes.

- •

Strong relationships with an extensive network of independent agents.

- •

Expertise in specialty areas like professional liability and surety.

Weaknesses

- •

Has faced periods of underwriting volatility in the past.

- •

Not as prominent in high-net-worth personal lines.

- •

Perceived as a more traditional insurer, potentially lagging in digital innovation.

Differentiators

- •

Focus on specific industries such as construction, manufacturing, and healthcare.

- •

Risk control services tailored to their target industries.

- •

Offers a full suite of standard and specialty commercial products.

Indirect Competitors

- →

Insurtech MGAs (e.g., Coalition, Next Insurance)

Description:Tech-enabled managing general agents (MGAs) and full-stack carriers that use AI, data analytics, and digital platforms to offer specialized insurance products (like cyber or small business) directly or through brokers, with a focus on a streamlined user experience.

Threat Level:Medium

Potential For Direct Competition:High, as they expand their product offerings and target larger accounts.

- →

Professional Employer Organizations (PEOs) (e.g., TriNet, Insperity)

Description:PEOs bundle services like payroll, HR, and benefits, including workers' compensation insurance, for small to medium-sized businesses. They act as a co-employer, abstracting the insurance purchasing decision from the end-client.

Threat Level:Low

Potential For Direct Competition:Low, but they reduce the addressable market for standalone workers' compensation policies.

- →

Captive Insurance Companies

Description:Large corporations that create their own licensed insurance subsidiaries to insure their own risks, thereby bypassing the traditional commercial insurance market for certain coverages.

Threat Level:Medium

Potential For Direct Competition:Not applicable; they represent a loss of potential customers from the traditional market.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Decentralized Operating Model

Sustainability Assessment:Highly sustainable. This model fosters an entrepreneurial culture, market responsiveness, and specialized expertise that is deeply embedded in the company's DNA and difficult for large, centralized competitors to replicate.

Competitor Replication Difficulty:Hard

- Advantage:

Specialized Niche Expertise

Sustainability Assessment:Highly sustainable. Deep underwriting knowledge in over 55 distinct business units creates a significant competitive moat built on intellectual property and decades of experience.

Competitor Replication Difficulty:Hard

- Advantage:

Strong Financial Strength & Disciplined Underwriting

Sustainability Assessment:Sustainable. Consistent A+ ratings from A.M. Best and S&P provide a crucial foundation of trust and stability for agents and policyholders, which is a key consideration in insurance purchasing.

Competitor Replication Difficulty:Hard

Temporary Advantages

{'advantage': 'First-Mover in Emerging Risk Categories', 'estimated_duration': '1-3 years'}

Disadvantages

- Disadvantage:

Fragmented Brand Identity

Impact:Major

Addressability:Moderately

- Disadvantage:

Complexity of Enterprise-Wide Digital Transformation

Impact:Critical

Addressability:Difficult

- Disadvantage:

Potential for Inconsistent Agent/Customer Experience

Impact:Major

Addressability:Moderately

Strategic Recommendations

Quick Wins

- Recommendation:

Launch a unified brand marketing campaign focused on the "Strength of a Fortune 500, agility of a startup" message to consolidate brand identity.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Develop a centralized digital resource hub for agents and brokers that aggregates key information and tools from across all 55+ business units.

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Establish a shared services 'Center of Excellence' for digital tools (e.g., AI underwriting, claims processing) that individual operating units can adopt voluntarily.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Acquire a small, strategic Insurtech firm whose technology platform can be adapted and offered across the Berkley ecosystem to accelerate innovation.

Expected Impact:High

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Build a proprietary, enterprise-wide data platform that aggregates anonymized data from all operating units to identify systemic trends and develop next-generation predictive models, without compromising unit autonomy.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Systematically expand into international markets by replicating the decentralized model, acquiring local specialty insurers and empowering local leadership.

Expected Impact:High

Implementation Difficulty:Difficult

Position W. R. Berkley as 'The Specialist's Specialist'—the premier destination for agents and businesses with complex, unique, and emerging risks that require deep, entrepreneurial expertise.

Hyper-specialization. Double down on the decentralized model by continuing to identify and build new businesses in underserved, technically complex, or emerging niches where larger, more generalized competitors are slow to adapt.

Whitespace Opportunities

- Opportunity:

Insurance for the AI Value Chain

Competitive Gap:While cyber insurance is common, there is a lack of specific products covering risks for AI developers, data providers, and companies deploying AI, such as algorithmic bias liability, model degradation, or AI-induced business interruption.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Integrated Risk Management Platform for High-Growth Niches

Competitive Gap:Competitors sell insurance policies. Berkley can offer a bundled, tech-enabled service for industries like Life Sciences or Cannabis that combines specialized insurance coverage with compliance tools, risk management resources, and data analytics.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Parametric Insurance for Climate and Supply Chain Risks

Competitive Gap:Most traditional insurers are slow to adopt parametric (event-triggered) insurance. Berkley could develop specialized parametric products for non-damage business interruption risks like supply chain delays, heat stress for agriculture, or grid failures, offering faster, non-contentious payouts.

Feasibility:Medium

Potential Impact:High

W. R. Berkley Corporation has carved out a unique and defensible position within the mature and highly competitive property and casualty insurance industry. Its primary competitive advantage is its decentralized operating model, which cultivates deep expertise in over 55 niche markets. This structure allows it to act with the agility and entrepreneurial spirit of a small, specialized firm while being backed by the financial strength of a Fortune 500 company. This contrasts sharply with its larger, more centralized direct competitors like Chubb and Travelers, who compete on brand scale, broad product suites, and global reach. Berkley's key strength is its ability to underwrite complex and emerging risks that larger, more bureaucratic insurers may be slower to address.

The primary challenges and disadvantages stem from this same core strength. The decentralized model leads to a fragmented brand identity, making it harder to build the same level of market recognition as a monolithic brand like Chubb. Furthermore, driving enterprise-wide digital transformation is critically difficult across dozens of autonomous business units, posing a significant threat as the industry is increasingly disrupted by agile, tech-forward Insurtech competitors. These indirect competitors, while small, are setting new customer expectations for digital service and efficiency that Berkley must find a way to meet without dismantling its successful operating model.

Strategic opportunities lie in bridging this gap. Berkley can create significant value by developing a shared technology infrastructure and digital tools that its operating units can adopt to enhance efficiency and customer experience, creating a 'best of both worlds' scenario. The most promising whitespace opportunities are in hyper-specialized, tech-adjacent fields like insuring the AI value chain or developing parametric products for climate risk, areas where Berkley's specialized, entrepreneurial approach is perfectly suited to excel. The company's future success will depend on its ability to leverage its core strength of specialization while strategically overlaying a cohesive digital and brand strategy to effectively compete in an evolving marketplace.

Messaging

Message Architecture

Key Messages

- Message:

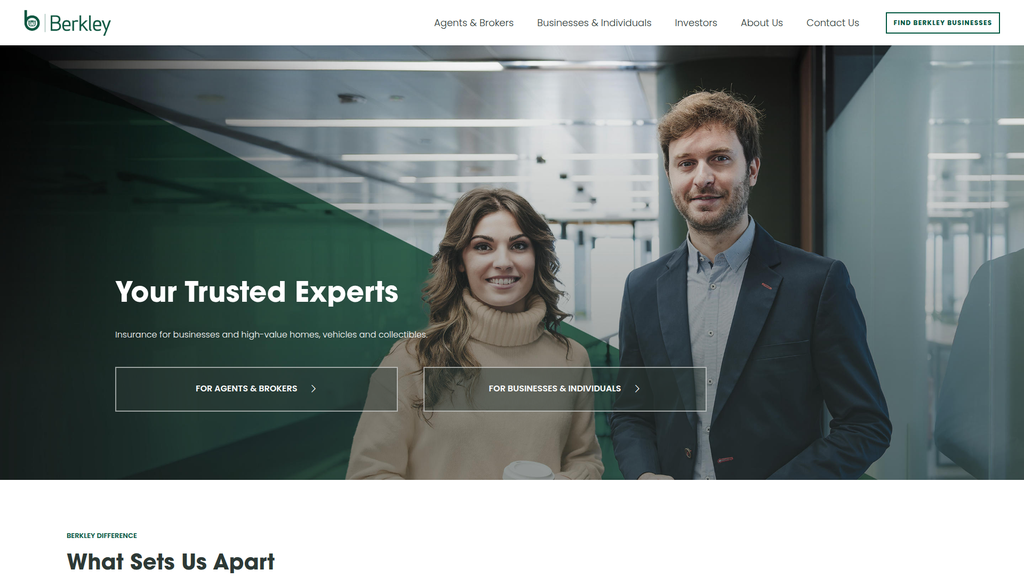

Your Trusted Experts

Prominence:Primary

Clarity Score:High

Location:Homepage - Main Headline

- Message:

Berkley's strength comes from its decentralized model of ~60 specialized insurance businesses, combining local agility with the resources of a Fortune 500 company.

Prominence:Secondary

Clarity Score:Medium

Location:Homepage - 'What Sets Us Apart' Section

- Message:

We forge lasting partnerships with our agents and brokers.

Prominence:Secondary

Clarity Score:High

Location:Homepage - 'FOR AGENTS & BROKERS' Section

- Message:

We have deep expertise across an array of businesses and occupations.

Prominence:Secondary

Clarity Score:High

Location:Construction Insurance Page

The message hierarchy is clear and logical. The homepage immediately establishes a primary theme of 'Expertise' and then bifurcates the user journey for its two main audiences: 'Agents & Brokers' and 'Businesses & Individuals'. Secondary messages effectively support the primary theme by explaining how Berkley achieves this expertise through its specialized, decentralized, and entrepreneurial model. The hierarchy successfully guides users toward the information most relevant to them.

Messaging is highly consistent across the analyzed pages. The core concepts of expertise, specialization, and a decentralized structure are reinforced on both the homepage and the specific industry page for Construction. This consistency builds a strong, coherent brand narrative.

Brand Voice

Voice Attributes

- Attribute:

Expert & Authoritative

Strength:Strong

Examples

- •

Your Trusted Experts

- •

deep expertise in various industries

- •

our underwriting teams are industry specialists

- •

Financially Strong

- Attribute:

Corporate & Professional

Strength:Strong

Examples

- •

manage their exposure and cost of risk

- •

decentralized structure

- •

Creating Value for Shareholders

- •

A Fortune 500 company

- Attribute:

Partner-Oriented

Strength:Moderate

Examples

- •

We forge lasting partnerships

- •

Berkley works collaboratively to tailor insurance

- •

Partners in Protecting Construction Businesses

- Attribute:

Entrepreneurial

Strength:Moderate

Examples

- •

Berkley builds insurance businesses from the ground up

- •

act with the agility of a small business

- •

Berkley seeks out and develops entrepreneurs

Tone Analysis

Formal and Confident

Secondary Tones

Reassuring

Informative

Tone Shifts

The tone becomes slightly more aspirational and employee-focused in the 'Careers' section with phrases like 'Everything Counts, Everyone Matters®'.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

W. R. Berkley provides highly specialized commercial and high net-worth insurance solutions by leveraging a unique decentralized model of nearly 60 expert, autonomous businesses, backed by the financial strength and resources of a Fortune 500 parent company.

Value Proposition Components

- Component:

Specialization & Deep Expertise

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Decentralized, Agile Service Model

Clarity:Clear

Uniqueness:Unique

- Component:

Financial Strength & Stability

Clarity:Clear

Uniqueness:Common

- Component:

Entrepreneurial Approach

Clarity:Somewhat Clear

Uniqueness:Somewhat Unique

The primary differentiator is the 'Decentralized' business model. While many large insurers claim specialization, Berkley's articulation of empowering nearly 60 autonomous businesses to act with 'the agility of a small business' is a compelling and unique narrative. This structure is positioned as the mechanism that delivers superior expertise and service, which effectively sets it apart from more monolithic competitors. The financial strength is a 'table stakes' claim for the industry, but powerful when combined with the agility message.

Berkley positions itself as a large, stable, and expert provider that avoids the bureaucratic slowness often associated with size. It competes by offering the 'best of both worlds': the deep, nimble expertise of a boutique specialty firm and the robust financial backing of a major corporation like AIG, Chubb, or Travelers. The messaging is aimed at sophisticated buyers and intermediaries who value expertise and tailored solutions over commoditized, price-driven products.

Audience Messaging

Target Personas

- Persona:

Insurance Agents & Brokers

Tailored Messages

- •

We forge lasting partnerships with our agents and brokers

- •

helping them connect customers to solutions using our expertise

- •

How to get appointed

Effectiveness:Effective

- Persona:

Commercial Business Owners/Risk Managers (e.g., in Construction)

Tailored Messages

- •

Insurance for businesses

- •

we focus on better outcomes and provide coverage for traditional and emerging risks

- •

Partners in Protecting Construction Businesses

- •

We understand that you want to focus on running your business with the reassurance that your insurance partner understands your industry

Effectiveness:Effective

- Persona:

High Net-Worth Individuals

Tailored Messages

Insurance for... high-value homes, vehicles and collectibles.

Effectiveness:Ineffective

Audience Pain Points Addressed

- •

Finding an insurer who understands my niche industry's risks.

- •

Dealing with slow, bureaucratic insurance companies.

- •

Completing projects on time within budget, protecting employees, equipment, and vehicles (Construction-specific).

- •

Managing the cost and exposure of risk.

Audience Aspirations Addressed

- •

Focusing on running my business with peace of mind.

- •

Partnering with a responsive and knowledgeable insurer.

- •

Securing the financial stability of my business or personal assets.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Trust & Security

Effectiveness:High

Examples

- •

Your Trusted Experts

- •

Financially Strong

- •

rated A+ (Superior)...by A.M. Best

- •

With over 50 years of experience

- Appeal Type:

Partnership & Collaboration

Effectiveness:Medium

Examples

- •

We forge lasting partnerships

- •

Berkley works collaboratively

- •

Partners in Protecting Construction Businesses

Social Proof Elements

- Proof Type:

Third-Party Ratings

Impact:Strong

Examples

rated A+ (Superior), Financial Size Category XV by A.M. Best Company

A+ (Strong) by Standard & Poor’s

- Proof Type:

Market Standing

Impact:Strong

Examples

A Fortune 500 company since 2004

Joined the S&P 500 in 2019

- Proof Type:

Customer Testimonials

Impact:Moderate

Examples

Quotes from customers like Frank V. and Amy G. on the Construction page.

Trust Indicators

- •

Financial ratings (A.M. Best, S&P)

- •

50+ years of experience

- •

Fortune 500 / S&P 500 status

- •

Global presence (55+ businesses, 190+ office locations)

- •

Publicly traded status (NYSE: WRB)

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

LEARN MORE

Location:Homepage, Berkley Specialty London spotlight

Clarity:Clear

- Text:

Berkley Locator (Industry/Product Search)

Location:Homepage, Construction Insurance Page

Clarity:Clear

- Text:

HOW TO GET APPOINTED

Location:Homepage - For Agents & Brokers

Clarity:Clear

- Text:

FIND BERKLEY BUSINESSES

Location:Bottom of product/industry lists on Construction Page

Clarity:Clear

The CTAs are clear, logical, and well-placed. The primary user tool, the 'Berkley Locator,' is an excellent interactive CTA that operationalizes the company's value proposition of specialization by allowing users to find the exact business unit for their specific needs. CTAs are appropriately segmented for different audiences ('GET APPOINTED' for brokers vs. 'LEARN MORE' for businesses). The overall effectiveness is high for guiding users to relevant information.

Messaging Gaps Analysis

Critical Gaps

The message to 'High Net-Worth Individuals' is present in the headline but receives almost no subsequent support, content, or clear user journey on the homepage, making it an unsupported claim.

Lack of tangible case studies or success stories. While testimonials exist, detailed narratives demonstrating how the decentralized, expert model led to a better outcome for a client are missing.

Contradiction Points

The message of being 'nimble' and 'agile' is a core differentiator but could be perceived as contradictory to the simultaneous messaging of being a large, established Fortune 500 company. The content successfully mitigates this by explaining the decentralized model, but it's a tension point that requires careful and consistent explanation.

Underdeveloped Areas

The 'Entrepreneurial' aspect of the value proposition is mentioned but not fully developed or proven with content. Stories of how Berkley builds and grows its businesses could strengthen this message.

The messaging is very focused on the 'how' (our model, our expertise) and could be enhanced by more explicitly stating the ultimate benefit to the end customer (e.g., reduced risk, cost savings, business continuity).

Messaging Quality

Strengths

- •

Excellent clarity and consistency around the core value proposition of a decentralized expert model.

- •

Strong audience segmentation on the homepage, creating clear paths for key user groups (brokers vs. businesses).

- •

Effective use of trust indicators like financial ratings and market standing to build credibility.

- •

The 'Berkley Locator' tool is a powerful piece of interactive content that makes the brand's complex structure accessible and useful.

Weaknesses

- •

The language can be dense and corporate, lacking emotional resonance beyond feelings of trust and security.

- •

Over-reliance on features (our model, our structure) rather than translating them into tangible client benefits and outcomes.

- •

The message for the 'High Net-Worth Personal Lines' audience is critically underdeveloped and feels like an afterthought on the homepage.

- •

Customer proof points are limited to short testimonials rather than more persuasive, in-depth case studies.

Opportunities

- •

Develop rich content (articles, case studies, videos) that tells the story of how a specific Berkley business solved a complex problem for a client, directly proving the value of the decentralized model.

- •

Create a dedicated, fleshed-out section or microsite for the 'High Net-Worth Individuals' audience to substantiate the homepage claim.

- •

Humanize the brand by spotlighting the 'entrepreneurs' and 'experts' who lead the individual businesses, connecting faces and stories to the expertise claim.

- •

Translate the 'Risk Management Services' listed on the Construction page into benefit-oriented language (e.g., 'Helping you maintain a safer job site' instead of just 'Jobsite Safety and Hazard Analysis').

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition Communication

Recommendation:Develop and feature at least three detailed case studies on the homepage that showcase specific client challenges and how Berkley's unique 'Specialized + Decentralized' model led to a superior outcome. Frame them as 'The Berkley Difference in Action'.

Expected Impact:High

- Area:

Audience Messaging

Recommendation:Either remove the 'high-value homes...' messaging from the main headline or create a dedicated content path and landing page for this audience segment to make it a credible offering.

Expected Impact:High

- Area:

Persuasion Elements

Recommendation:Incorporate more benefit-driven headlines and sub-headlines. For example, change 'What Sets Us Apart' to 'Get the Agility of a Specialist with the Strength of a Leader'.

Expected Impact:Medium

Quick Wins

- •

Add logos of the individual operating companies (e.g., Berkley Southwest, Admiral) to the homepage to visually represent the '55+ businesses' concept.

- •

In the testimonials section, add the specific Berkley business the client worked with to reinforce the decentralized model.

- •

Rewrite the 'Risk Management Services' bullet points on industry pages to start with a verb and focus on the client benefit (e.g., 'Reduce risk transfer conflicts with...' instead of 'Contractual Risk Transfer Guidelines').

Long Term Recommendations

- •

Implement a thought leadership content strategy where experts from the various specialty businesses publish articles and insights on emerging risks in their niche industries, cementing the 'Trusted Experts' position.

- •

Develop a more robust 'For Businesses & Individuals' section that goes beyond just a link, perhaps featuring success stories or tools to help them identify their primary risks.

- •

Create video content featuring the leaders of the decentralized businesses to humanize the brand and add a personal voice to the 'entrepreneurial' and 'expert' claims.

W. R. Berkley Corporation's website messaging is highly effective at communicating its core strategic differentiator: a decentralized model that combines specialist expertise with financial strength. The message architecture is clear, logical, and consistent, effectively segmenting its primary audiences—agents/brokers and commercial businesses—and guiding them to relevant information. The brand voice is authoritative, professional, and trustworthy, heavily reinforced by strong social proof elements like A+ financial ratings and its Fortune 500 status.

The central value proposition is unique and well-articulated, positioning Berkley as a solution to the common pain point of dealing with large, slow, impersonal insurers. However, the communication relies heavily on explaining the features of its business model rather than consistently translating them into tangible, quantified client benefits. The primary weakness lies in its underdeveloped messaging for the high net-worth individual segment, which is mentioned prominently but lacks any substantive support, creating a messaging gap. Furthermore, persuasion could be strengthened by moving beyond simple testimonials to in-depth case studies that narrate the success of their model in practice.

To optimize, Berkley should focus on proving, not just stating, its value. Developing compelling case studies, elevating thought leadership from its in-house experts, and better articulating client outcomes will transition the message from being about 'who we are' to 'what we can achieve for you.' This will enhance its market positioning and more effectively drive acquisition for its key business segments.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Over 50 years of operation as a Fortune 500 and S&P 500 company, indicating long-term market acceptance and stability.

- •

Successful operation of over 55 distinct, specialized insurance businesses, demonstrating deep expertise and fit across numerous niche markets.

- •

Consistently strong financial performance, including record net income and a 23.6% return on equity in 2024, signals robust demand and effective underwriting.

- •

Positive customer testimonials on the website from various operating units (Berkley One, Midwest Employers Casualty, etc.) suggest strong customer satisfaction and claims handling.

- •

High financial strength ratings (A+ from A.M. Best and S&P) reinforce trust and credibility in the marketplace.

Improvement Areas

- •

Develop a more unified digital experience for brokers and agents across the 55+ businesses to reduce friction and improve ease of doing business.

- •

Enhance data analytics capabilities at the holding company level to identify cross-selling opportunities between the decentralized business units.

- •

Invest in a consistent brand message that highlights the combined strength and expertise of the Berkley network, beyond the individual operating companies.

Market Dynamics

Approximately 9-11% CAGR for the specialty insurance market.

Mature

Market Trends

- Trend:

Increased demand for specialty insurance for emerging risks (e.g., cyber, climate change, cannabis, AI liability).

Business Impact:High. This is a primary growth driver for Berkley's specialized business model, creating new markets for their expertise-led underwriting.

- Trend:

Digital transformation and the rise of Insurtech are automating processes, improving underwriting, and enhancing customer experience.

Business Impact:High. Creates both an opportunity to improve efficiency and a threat from more agile, tech-native competitors. Berkley must invest in technology to empower its brokers and underwriters.

- Trend:

Increased frequency and severity of catastrophic events (natural disasters) driving demand and hardening the property insurance market.

Business Impact:Medium-High. Creates demand for coverage but also increases underwriting risk and potential for large-scale losses, requiring sophisticated risk modeling.

- Trend:

A shift towards customer-centricity and personalized insurance products, facilitated by data analytics.

Business Impact:Medium. While Berkley's model is primarily B2B (via brokers), the end-customer's expectations for personalization will influence the products brokers seek.

Excellent. The market is increasingly valuing the specialized expertise that is core to Berkley's business model, particularly with the proliferation of complex and emerging risks.

Business Model Scalability

High

The decentralized holding company model allows for a highly variable cost structure. New business units can be launched or acquired, scaling operations and revenue without a proportional increase in central overhead.

High. The model allows local, autonomous businesses to act with agility while leveraging the parent company's capital, financial strength, and shared services (where applicable).

Scalability Constraints

- •

Talent acquisition for leadership and specialized underwriting expertise for new niche business units.

- •

Potential for cultural clashes or integration challenges when acquiring existing businesses.

- •

Maintaining underwriting discipline and quality control across a growing number of autonomous entities.

Team Readiness

Strong. The company's long-term success, consistent financial performance, and successful operation of dozens of businesses indicate a highly capable and experienced leadership team.

Highly suitable for growth. The decentralized structure is a core strategic advantage, allowing for parallel processing of growth initiatives and rapid entry into new markets.

Key Capability Gaps

- •

Centralized Digital & Innovation Leadership: A team to drive technology adoption and share best practices across all 55+ operating units.

- •

Data Science & Analytics: A central resource to leverage the vast, siloed data across the organization for improved underwriting, pricing, and identifying new market opportunities.

- •

Head of Insurtech Partnerships: A dedicated role to scout, vet, and integrate technologies from the booming Insurtech sector.

Growth Engine

Acquisition Channels

- Channel:

Independent Agents & Brokers

Effectiveness:High

Optimization Potential:High

Recommendation:Develop a best-in-class, unified digital broker portal with streamlined quoting, binding, and policy management capabilities across all relevant Berkley businesses to become the 'carrier of choice' for complex risks.

- Channel:

Wholesale Brokers (for E&S lines)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Further strengthen relationships by providing dedicated underwriting expertise and rapid response times for complex risks, as demonstrated by the Berkley Edge launch.

- Channel:

Direct-to-Business (Digital)

Effectiveness:Low

Optimization Potential:Low

Recommendation:Not a primary focus. Berkley's value proposition is built on expertise for complex risks, which is best delivered through knowledgeable intermediaries. This channel is not a strategic fit.

Customer Journey

The primary path is Business -> Agent/Broker -> Berkley Operating Company. The corporate website serves as a directory ('Berkley Locator') to guide brokers to the appropriate specialized unit.

Friction Points

- •

Navigating between the main Berkley corporate site and the 55+ individual business unit websites, which may have inconsistent branding and user experiences.

- •

Lack of a single sign-on or unified dashboard for brokers who work with multiple Berkley companies.

- •

Manual or semi-manual processes for submitting and tracking complex applications that could be digitized.

Journey Enhancement Priorities

{'area': 'Broker Digital Experience', 'recommendation': 'Create a unified digital platform for brokers that provides a single point of entry for quoting, policy management, and claims across all Berkley entities they are appointed with.'}

{'area': 'Berkley Locator Tool', 'recommendation': 'Enhance the locator with more advanced filtering, AI-powered recommendations, and direct contact information for key underwriters to speed up the connection process.'}

Retention Mechanisms

- Mechanism:

Broker Relationships

Effectiveness:High

Improvement Opportunity:Invest in co-marketing initiatives, exclusive educational content, and advisory councils to deepen partnerships with key brokers.

- Mechanism:

Claims Service Quality

Effectiveness:High

Improvement Opportunity:Leverage AI and automation to further expedite claims processing and provide real-time status updates to both brokers and policyholders.

- Mechanism:

Underwriting Expertise & Responsiveness

Effectiveness:High

Improvement Opportunity:Empower underwriters with better data analytics and AI tools to enhance risk assessment and accelerate decision-making on complex submissions.

Revenue Economics

Healthy. As a consistently profitable public company with a strong ROE, their underwriting discipline ensures positive unit economics.

Undeterminable from public data, but likely very high for a B2B insurer focused on specialty lines where relationships and policy renewals span many years.

High. The company has demonstrated strong revenue growth (9.6% GWP growth in 2024) and profitability, indicating an efficient revenue engine.

Optimization Recommendations

- •

Develop a formal process for identifying and acting on cross-sell opportunities between the 55+ business units.

- •

Utilize predictive analytics to optimize pricing and risk selection, improving margins on new and renewal business.

- •

Invest in automation for policy administration and claims to reduce operational costs and improve the combined ratio.

Scale Barriers

Technical Limitations

- Limitation:

Siloed Data & Legacy Systems

Impact:High

Solution Approach:Implement a central data lake or data fabric to aggregate key underwriting and claims data from all subsidiaries. Develop APIs to allow modern front-end tools to interact with legacy core systems.

- Limitation:

Inconsistent Technology Stacks

Impact:Medium

Solution Approach:Establish a centralized 'Center of Excellence' to define technology standards and best practices for all operating units, promoting interoperability without mandating a single monolithic system.

Operational Bottlenecks

- Bottleneck:

Onboarding and Integrating New Acquisitions

Growth Impact:Slows down M&A-led growth.

Resolution Strategy:Develop a standardized integration playbook that covers key areas like finance, HR, technology, and compliance, while preserving the operational autonomy of the acquired entity.

- Bottleneck:

Sharing of Best Practices

Growth Impact:Inhibits organic growth and efficiency gains.

Resolution Strategy:Establish formal knowledge-sharing forums, such as an annual innovation summit for business unit leaders, and an internal digital platform for sharing successful strategies and tools.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Major

Mitigation Strategy:Continue to double down on the specialized expertise model, focusing on niche markets where deep knowledge creates a defensible moat against larger, more generalized competitors like Chubb, AIG, and Travelers.

- Challenge:

Disruption from Insurtech Startups

Severity:Minor

Mitigation Strategy:Adopt a 'partner/acquire' strategy. Create a corporate venture arm or strategic partnership program to invest in and leverage promising Insurtechs that can enhance Berkley's existing operations rather than trying to build all technology in-house.

Resource Limitations

Talent Gaps

- •

Data Scientists and AI/ML Engineers with insurance domain expertise.

- •

Digital Product Managers to lead the development of broker-facing technologies.

- •

Specialized Underwriters for new and emerging risk categories (e.g., carbon credits, AI ethics liability).

Low. The company generates strong operating cash flow ($3.7 billion in 2024), which is sufficient to fund organic growth initiatives and strategic acquisitions.

Infrastructure Needs

- •

Cloud-based data and analytics platform.

- •

Modern API gateway to enable secure data exchange with partners and brokers.

- •

A unified digital workplace/intranet to foster collaboration across the decentralized businesses.

Growth Opportunities

Market Expansion

- Expansion Vector:

Geographic Expansion into Asia-Pacific

Potential Impact:High

Implementation Complexity:High

Recommended Approach:The Asia-Pacific region is projected to be the fastest-growing specialty insurance market. Replicate the Berkley Specialty London model by establishing a regional hub in a key market like Singapore to underwrite specialty risks for the broader region.

- Expansion Vector:

Launch New Niche-Specific Operating Units

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Systematically identify and incubate new businesses focused on high-growth, underserved niches, such as insurance for the circular economy, renewable energy projects, or digital assets, similar to the recent launch of Berkley Edge.

Product Opportunities

- Opportunity:

Parametric Insurance Products

Market Demand Evidence:Growing need for faster, more transparent claims payouts for risks like weather events, where payouts are triggered by predefined data points (e.g., wind speed, rainfall level) rather than lengthy damage assessments.

Strategic Fit:High. Fits the specialty model and leverages data analytics.

Development Recommendation:Launch a pilot program within an existing subsidiary (e.g., Berkley Agribusiness) focused on a specific, data-rich peril like drought or hurricane.

- Opportunity:

Cyber Insurance for Operational Technology (OT)

Market Demand Evidence:Increasing connectivity of industrial control systems in manufacturing, energy, and transportation creates significant, specialized cyber risks that are distinct from traditional IT risks.

Strategic Fit:High. Aligns perfectly with existing expertise in manufacturing, energy, and construction.

Development Recommendation:Create a dedicated underwriting team that combines cyber expertise with deep industrial sector knowledge to develop tailored OT cyber policies.

Channel Diversification

- Channel:

Embedded Insurance via APIs

Fit Assessment:High

Implementation Strategy:Develop a set of robust APIs that allow technology platforms (e.g., construction management software, logistics platforms) to embed Berkley's specialized insurance products directly into their user workflow. This opens a new, scalable distribution channel.

- Channel:

Managing General Agents (MGAs)

Fit Assessment:High

Implementation Strategy:Expand partnerships with specialized MGAs who have deep expertise and distribution in niche markets that Berkley wants to enter, providing them with underwriting capacity and paper.

Strategic Partnerships

- Partnership Type:

Insurtech Data & Analytics Providers

Potential Partners

- •

Hyperscience (for intelligent document processing)

- •

Verisk (for advanced risk modeling)

- •

Tensorflight (for AI-based property assessment)

Expected Benefits:Enhance underwriting accuracy, automate manual processes, and reduce claims processing time, leading to improved profitability and broker satisfaction.

- Partnership Type:

Industry-Specific Technology Platforms

Potential Partners

- •

Procore (Construction)

- •

ServiceTitan (Home Services)

- •

Major Logistics and Supply Chain Platforms

Expected Benefits:Create exclusive embedded insurance offerings, gaining access to a large pool of qualified customers at the point of need and creating a new revenue stream.

Growth Strategy

North Star Metric

Gross Written Premium from New Ventures & Emerging Risks

This metric aligns with Berkley's core strategy of decentralized, entrepreneurial growth. It focuses the organization on high-margin, future-facing opportunities rather than just incremental growth in mature markets, and directly measures the success of their innovation and expansion efforts.

Increase the percentage of total GWP from businesses launched in the last 5 years and from new product lines (e.g., climate, advanced cyber) by 15% annually.

Growth Model

Hybrid: Expertise-Led & Acquisition-Driven

Key Drivers

- •

Reputation for deep underwriting expertise in niche markets.

- •

Strong relationships with the independent and wholesale broker communities.

- •

Strategic acquisition and incubation of new, specialized insurance businesses.

- •

Disciplined capital allocation to support profitable growth.

Continue the core model while layering on a 'Technology-Enablement' strategy. Invest centrally in platforms and data capabilities that empower the decentralized businesses to compete more effectively and scale faster.

Prioritized Initiatives

- Initiative:

Project Unify: Develop a Unified Broker Platform

Expected Impact:High

Implementation Effort:High

Timeframe:18-24 months

First Steps:Form a cross-functional team with representatives from key operating units and broker partners. Conduct extensive user research to define core requirements and map the ideal broker journey. Start with a pilot for 2-3 of the most complementary business units.

- Initiative:

Berkley Innovation Labs

Expected Impact:High

Implementation Effort:Medium

Timeframe:6 months to launch

First Steps:Appoint a Head of Innovation. Allocate a dedicated seed fund for incubating new business ideas. Launch an internal competition to source ideas for the first one or two ventures focused on emerging risks like AI liability or climate adaptation.

- Initiative:

API-as-a-Product Program

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:9-12 months

First Steps:Identify the top 3 insurance products best suited for embedded distribution. Develop a standardized API and documentation. Partner with one or two design partners from a key industry (e.g., construction tech) to co-develop the first integration.

Experimentation Plan

High Leverage Tests

{'test': 'Dynamic Pricing Pilot', 'hypothesis': 'Using real-time, third-party data sources (e.g., telematics, weather, satellite imagery) in our underwriting models for specific product lines will improve risk selection and allow for more competitive pricing.'}

{'test': 'AI-Assisted Underwriting Workbench', 'hypothesis': 'Providing underwriters with a tool that automates data extraction from submissions and flags key risk indicators will reduce response times by 30% and improve underwriting consistency.'}

Use an A/B testing framework where possible. Track metrics such as quote-to-bind ratio, submission response time, loss ratio of the experimental cohort vs. control group, and broker satisfaction (NPS).

Run quarterly innovation sprints focused on specific business problems or opportunities, with clear go/no-go decisions at the end of each sprint.

Growth Team

A centralized 'Growth & Technology Enablement' team that acts as an internal consulting group and service provider to the autonomous business units. This team would not own a P&L but would be measured on the adoption of its platforms and the success of the businesses it supports.

Key Roles

- •

Chief Growth Officer

- •

Head of Digital Platforms (Broker Experience)

- •

Head of Data & Analytics

- •

Director of Strategic Partnerships & Insurtech Ventures

Recruit top talent from outside the traditional insurance industry (e.g., from tech, consulting). Create a rotational program for high-potential individuals from the operating units to spend 12-18 months in the central growth team to foster cross-pollination of ideas and skills.

W. R. Berkley Corporation possesses an exceptionally strong foundation for growth, built upon a highly scalable, decentralized business model and deep expertise in profitable specialty insurance niches. Its product-market fit is validated by decades of strong financial performance and a dominant position in complex commercial and high-net-worth lines. The primary growth engine, driven by strong broker relationships, is effective but has significant potential for optimization through digital transformation.

The most critical challenge and greatest opportunity lies in overcoming the technical and operational silos inherent in its decentralized structure. While this autonomy is a key strength, it creates barriers to leveraging scale, cross-selling, and data analytics across the enterprise. A strategic investment in a unified digital platform for brokers and a central data analytics capability would unlock immense value, making it easier for brokers to do business with Berkley and providing invaluable insights for underwriting and new product development.

The key growth vectors are clear: continued expansion into new, underserved specialty markets (both organically and via acquisition), geographic expansion into high-growth regions like Asia-Pacific, and diversification into technology-enabled distribution channels like embedded insurance. To execute this, Berkley should evolve its structure to include a central 'Growth & Technology Enablement' team. This team would not dilute the autonomy of the business units but would provide the tools, platforms, and strategic capabilities necessary to accelerate their growth and ensure the corporation as a whole remains competitive in an increasingly digital marketplace. The strategy should be to weaponize their specialized knowledge with best-in-class technology, creating an insurmountable competitive advantage.

Legal Compliance

A 'Privacy' link is present in the website footer. The policy is comprehensive, addressing the collection and use of personal information. Crucially for an insurer, it acknowledges its obligations under the Gramm-Leach-Bliley Act (GLBA), detailing how it handles nonpublic personal information (NPI). It also includes a specific 'California CCPA Notice' link, demonstrating awareness of CCPA/CPRA obligations. The policy outlines the types of data collected, the purposes for processing, and circumstances of data sharing. For its European operations, like 'Berkley Specialty London', compliance with GDPR is critical. The policy addresses data subject rights, which aligns with GDPR principles, but could be more explicit about naming a Data Protection Officer (DPO) or an EU representative for GDPR purposes, if applicable.

A 'Legal & Licensing' link, effectively serving as the terms of use, is accessible from the footer. The terms are robust, containing necessary disclaimers of warranties, limitations of liability, and intellectual property notices. They explicitly state that website content does not constitute an offer to sell insurance and that all coverage is subject to the terms of the actual policy issued. This is a critical disclaimer for an insurance provider. It also includes a choice of law and jurisdiction clause. The language is legally sound but could be presented in a more user-friendly format to improve clarity for the average user.