eScore

cinfin.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Cincinnati Financial's digital presence is strategically focused on supporting its independent agent channel rather than direct customer acquisition. Content is heavily skewed towards the decision stage of the buyer's journey, primarily serving to validate the brand and funnel prospects to an agent. This leads to low visibility for high-volume, top-of-funnel consumer search queries, but strong authority within its core agent audience. The website lacks broader educational or thought leadership content, creating a significant competitive gap and missed opportunity to capture users in earlier research phases.

The website's content and messaging are exceptionally consistent in reinforcing the core value proposition of the agent-centric model and financial stability.

Develop a 'Business Risk Resource Center' with in-depth articles and guides for target industries to capture high-intent B2B search traffic and establish thought leadership.

The company excels at communicating its core message with remarkable consistency, focusing on the value of independent agents, financial strength, and personal relationships. This messaging clearly targets its primary audiences (agents, businesses, and families) and effectively builds trust through a professional and reassuring brand voice. However, the communication relies heavily on assertions rather than quantifiable proof, such as specific claims satisfaction scores or case studies, and misses opportunities to articulate why a Cincinnati agent is superior to another independent agent.

Exceptional message clarity and consistency, which strongly reinforces the brand's core identity as a stable, agent-focused carrier.

Substantiate claims of 'unparalleled service' by creating a dedicated section with diverse testimonials, case studies, and key performance indicators (e.g., claims satisfaction scores, speed of payment).

The website's primary conversion goal—connecting users with an agent—is clear, but the experience has notable friction. The 'Find an Agent' journey is the only path, with no options for direct digital interaction or quoting, which creates a high cognitive load for users expecting modern, self-service options. While the information architecture is logical, the reliance on text-heavy pages and inconsistent CTA design (e.g., ghost buttons in the hero section) weakens the path to conversion.

The website is clearly and logically oriented around a single, primary conversion goal: driving prospective clients to its network of independent agents.

A/B test the homepage hero's 'ghost button' CTA against a solid-fill, high-contrast version to increase the visibility and click-through rate of the primary user action.

Credibility is a major strength, built on a foundation of exceptional financial ratings (A.M. Best A+) that are prominently displayed as third-party validation. The company demonstrates high transparency through detailed corporate governance documents, a clear Code of Conduct, and specific, layered privacy policies. Trust is further enhanced by customer testimonials and a 70+ year history, mitigating perceived risk for both agents and policyholders. The analysis points out only minor gaps, like a non-prominent 'Do Not Sell' link, but the overall posture is excellent.

Prominent and repeated use of its A+ (Superior) A.M. Best rating serves as a powerful, easily understood trust signal for all audiences.

Immediately add a direct 'Do Not Sell or Share My Personal Information' link to the website footer to fully comply with CCPA/CPRA and eliminate a high-severity compliance risk.

The company's primary competitive advantage—its loyal, exclusive independent agent network—is a highly sustainable and defensible moat that is difficult for D2C competitors to replicate. This is fortified by a stellar reputation for financial strength and excellent claims service, creating high switching costs for agents and their clients. However, the analysis reveals a weakness in innovation indicators, showing slow adoption of digital technologies, which could erode the moat's sustainability over the long term if not addressed.

The loyal, deeply-entrenched independent agent network provides a formidable distribution channel and a defensible barrier against D2C competitors.

Invest in or partner with an insurtech firm specializing in agent-facing technology to accelerate digital tool development and 'supercharge' the existing agent network.

The business model has demonstrated steady, profitable growth but faces inherent scalability constraints due to its reliance on a human-led agent network, which is less scalable than a technology-driven D2C model. While unit economics are healthy, operational leverage is only moderate, as growth is tied to the time-intensive process of recruiting and enabling new agencies. Significant potential exists to increase scalability by investing in automation and digital tools to enhance the productivity of each agent.

Strong product-market fit and a healthy LTV-to-CAC ratio, driven by high retention rates within the agent-centric model.

Implement an AI-powered underwriting workbench to automate data ingestion and analysis, reducing manual processes and speeding up quote-to-bind times for agents.

Cincinnati Financial exhibits exceptional business model coherence, with every component aligned around its core strategy of serving independent agents. Revenue streams are diversified across multiple insurance lines, resource allocation (as implied by messaging and structure) is focused on agent support, and the strategic focus is unwavering. The value proposition, key activities, and cost structure are all internally consistent and reinforce the agent-centric approach that has proven successful for decades.

An unwavering and strategically aligned focus on the independent agent channel, ensuring all business activities support this core principle.

Develop a 'Carrier-as-a-Service' pilot to provide back-end underwriting and claims services to select tech-enabled agencies, creating a new, aligned B2B revenue stream.

As a top 25 P&C insurer, the company holds a stable, albeit moderate, market share (around 1-1.5%). Its market power stems from its strong relationships with its agent partners, giving it significant leverage within its chosen distribution channel. Its reputation for service and stability allows for a degree of pricing power, positioning it as a premium offering rather than competing on price. However, its influence on broader market trends is limited compared to D2C giants who are driving digital innovation.

Significant leverage and influence within its premier independent agent network, making it a 'carrier of choice' for high-performing agencies.

Leverage proprietary claims data to publish an annual, data-driven 'State of Business Risk' report to generate media buzz and increase its influence on market conversations.

Business Overview

Business Classification

Insurance Carrier

Financial Services

Insurance

Sub Verticals

- •

Property & Casualty (P&C) Insurance

- •

Life Insurance

- •

Excess & Surplus (E&S) Lines

- •

Commercial Leasing & Financing

Mature

Maturity Indicators

- •

Founded in 1950, operating for over 70 years.

- •

Consistently high financial strength ratings (A+ from A.M. Best).

- •

Publicly traded company (NASDAQ: CINF) with a significant market capitalization.

- •

Ranked among the top 25 P&C insurers in the U.S. by net written premiums.

- •

Long history of paying and increasing dividends.

- •

Established and extensive network of independent agents across 46 states.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Written Premiums

Description:The primary source of revenue is the collection of premiums from policyholders for property, casualty, and life insurance policies, net of reinsurance costs. This is diversified across commercial lines, personal lines, E&S, and life insurance.

Estimated Importance:Primary

Customer Segment:All Segments (Individuals, Families, Businesses)

Estimated Margin:Medium

- Stream Name:

Investment Income

Description:Income generated from investing the 'float' – premiums collected before claims are paid out. The portfolio includes fixed-maturity investments and a significant allocation to dividend-paying equity securities.

Estimated Importance:Secondary

Customer Segment:Internal Operations

Estimated Margin:High

- Stream Name:

Leasing and Financing Fees

Description:Revenue from CFC Investment Company, which offers commercial leasing and financing services to agents and their clients.

Estimated Importance:Tertiary

Customer Segment:Independent Agents and their Commercial Clients

Estimated Margin:Medium

Recurring Revenue Components

- •

Policy Renewals (P&C)

- •

Term Life Insurance Premiums

- •

Fixed Annuity Payments

Pricing Strategy

Underwriting-Based Pricing

Mid-range to Premium

Opaque

Pricing Psychology

Value-Based Pricing (emphasizing service and claims handling over cost)

Relationship Pricing (pricing may be influenced by the long-term relationship and total business with a client via the agent)

Monetization Assessment

Strengths

- •

Highly diversified revenue from multiple insurance lines (Commercial, Personal, E&S, Life).

- •

Stable and significant secondary income stream from investments.

- •

Independent agent model provides a broad and loyal distribution network, driving consistent premium flow.

- •

Strong financial ratings allow for competitive and stable pricing.

Weaknesses

- •

Revenue is sensitive to catastrophic loss events, which can impact underwriting profitability.

- •

Investment income is exposed to equity market volatility and interest rate fluctuations.

- •

The agent-based model may have higher acquisition costs compared to direct-to-consumer models.

Opportunities

- •

Further expansion of high-margin Excess & Surplus (E&S) lines through their specialist subsidiaries.

- •

Leverage data analytics and AI to refine underwriting and pricing models for improved profitability.

- •

Develop and offer new products tailored to emerging risks like cyber liability and climate-related events.

Threats

- •

Intense competition from both direct-to-consumer insurers (e.g., Progressive, Geico) and other agent-based carriers (e.g., Chubb, Travelers).

- •

Insurtech startups disrupting the value chain with technology-first solutions.

- •

Increasing frequency and severity of natural disasters driving up claims costs.

- •

A protracted low-interest-rate environment could suppress investment income growth.

Market Positioning

Relationship-driven service and financial stability, delivered exclusively through a premier network of independent agents.

Top 25 P&C Insurer in the U.S. with approximately 1% of the domestic P&C market.

Target Segments

- Segment Name:

Independent Insurance Agencies

Description:The primary 'customer' and distribution channel. These are established, professional agencies that value strong carrier relationships, local decision-making, and superior claims service to serve their own clients effectively.

Demographic Factors

- •

Established P&C and/or Life insurance agencies

- •

Located in one of 46 states of operation

- •

Varying in size from small local agencies to large regional brokers

Psychographic Factors

- •

Value long-term, stable carrier partnerships

- •

Prioritize service and claims handling over lowest price

- •

Seek empowered, local underwriting and claims contacts

Behavioral Factors

- •

Act as trusted advisors to their clients

- •

Seek to consolidate business with a few key carriers

- •

Desire efficient technology and tools from carriers to streamline operations

Pain Points

- •

Inconsistent service from carriers

- •

Lack of direct access to underwriters

- •

Slow claims processing for their clients

- •

Complex or inefficient carrier technology platforms

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Small & Mid-Sized Businesses

Description:Commercial clients who rely on independent agents for advice on comprehensive coverage for property, liability, auto, and workers' compensation.

Demographic Factors

- •

Various industries

- •

Typically privately owned or family-run

- •

Seeking standard to moderately complex commercial policies

Psychographic Factors

- •

Risk-averse

- •

Value expert advice and personalized service

- •

Loyal to their agent relationship

Behavioral Factors

Prefer to bundle policies with one carrier

Rely on agent recommendations for carrier selection

Pain Points

- •

Navigating complex insurance needs

- •

Finding affordable, comprehensive coverage

- •

Experiencing business disruption during a claim

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

High-Net-Worth Individuals (Private Client)

Description:Affluent individuals and families with complex personal insurance needs, such as high-value homes, luxury vehicles, collections, and umbrella liability.

Demographic Factors

High income and asset levels

Own multiple properties or high-value assets

Psychographic Factors

- •

Value discretion and white-glove service

- •

Seek comprehensive asset protection

- •

Brand conscious

Behavioral Factors

Work with specialized financial advisors or agents

Demand exceptional and fast claims service

Pain Points

- •

Standard insurance policies have coverage gaps

- •

Difficulty insuring unique assets

- •

Lack of personalized risk management advice

Fit Assessment:Good

Segment Potential:Medium

- Segment Name:

Individuals & Families (Personal Lines)

Description:General consumers seeking standard home and auto insurance who prefer the guidance of an agent over a direct-to-consumer model.

Demographic Factors

- •

Homeowners

- •

Multi-car households

- •

Families seeking life insurance

Psychographic Factors

- •

Value security and peace of mind

- •

Prefer human interaction and advice for major financial decisions

- •

May be less price-sensitive than direct-to-consumer shoppers

Behavioral Factors

Likely to have a long-term relationship with their agent

Often purchase bundled policies

Pain Points

- •

Understanding policy details and coverages

- •

Frustration with automated or impersonal service

- •

Navigating the claims process alone

Fit Assessment:Good

Segment Potential:Medium

Market Differentiation

- Factor:

Exclusive Independent Agent Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Superior Financial Strength (A+ Rating)

Strength:Strong

Sustainability:Sustainable

- Factor:

Reputation for Claims Service

Strength:Strong

Sustainability:Sustainable

- Factor:

Local, Empowered Field Operations

Strength:Moderate

Sustainability:Sustainable

Value Proposition

For individuals and businesses who value expert guidance and superior service, Cincinnati Financial provides comprehensive insurance solutions and financial stability through an exclusive network of premier independent agents, ensuring peace of mind and prompt, personal support when it's needed most.

Good

Key Benefits

- Benefit:

Expert guidance and personalized advice from a local professional.

Importance:Critical

Differentiation:Unique

Proof Elements

- •

Exclusive distribution through independent agents.

- •

Emphasis on agent relationships on the website.

- •

Agent locator tool prominently featured.

- Benefit:

Financial strength and ability to pay claims.

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

A+ (Superior) rating from A.M. Best prominently displayed.

- •

Strong ratings from Fitch, Moody's, and S&P.

- •

Decades of financial stability and market presence.

- Benefit:

Unparalleled, empathetic claims service.

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Customer testimonials highlighting positive claims experiences.

Emphasis on 'putting people first' and 'local associates'.

Unique Selling Points

- Usp:

An unwavering, exclusive commitment to the independent agent channel as the sole method of distribution.

Sustainability:Long-term

Defensibility:Strong

- Usp:

A business model built on local, empowered field representatives for underwriting and claims, enabling faster, more responsive decisions.

Sustainability:Medium-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

The complexity and confusion of choosing the right insurance coverage.

Severity:Major

Solution Effectiveness:Complete

- Problem:

The impersonal and frustrating experience of dealing with call centers or automated systems during a claim.

Severity:Major

Solution Effectiveness:Complete

- Problem:

Worrying if an insurance company has the financial stability to pay a large claim.

Severity:Critical

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition is well-aligned with a significant market segment that prioritizes service, advice, and stability over the lowest possible price, a segment often underserved by direct-to-consumer models.

High

The proposition aligns perfectly with the needs of their primary customer: the independent agent, who requires a reliable, service-oriented, and financially strong carrier partner to serve their end clients effectively.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Independent Insurance Agencies (Core Channel)

- •

Reinsurance Companies

- •

Technology and Data Providers

- •

Financial Institutions

Key Activities

- •

Underwriting and Risk Assessment

- •

Claims Processing and Management

- •

Investment Management

- •

Agent Relationship Management and Support

- •

Product Development

Key Resources

- •

Capital Reserves and Investment Portfolio

- •

A+ Financial Strength Rating

- •

Network of ~1,900 Independent Agencies.

- •

Brand Reputation and Trust

- •

Experienced Underwriters and Claims Professionals

Cost Structure

- •

Loss and Loss Adjustment Expenses (LAE)

- •

Agent Commissions and Profit Sharing

- •

Employee Salaries and Benefits

- •

Technology and Infrastructure Costs

- •

Marketing and Corporate Overhead

Swot Analysis

Strengths

- •

Loyal and extensive independent agent distribution network provides a deep market reach and strong customer relationships.

- •

Exceptional financial strength and 'Strongest' balance sheet assessment by A.M. Best.

- •

Diversified portfolio across personal, commercial, life, and specialty lines reduces risk.

- •

Strong brand reputation built over 70+ years, centered on service and claims excellence.

Weaknesses

- •

Potential for slower adaptation to technological change compared to agile insurtech competitors.

- •

Indirect control over the end-customer relationship, which is owned by the agent.

- •

Growth is dependent on the ability to recruit and retain high-performing independent agencies.

- •

Higher expense ratio inherent in the agent-based model compared to direct insurers.

Opportunities

- •

Invest in and deploy advanced digital tools to empower agents, improving their efficiency and binding more business.

- •

Leverage AI and big data for more sophisticated underwriting, risk selection, and pricing.

- •

Expand presence in high-growth, high-margin segments like E&S and the high-net-worth market.

- •

Form strategic partnerships with insurtechs to enhance specific capabilities (e.g., claims automation, risk modeling) without disrupting the core agent model.

Threats

- •

Persistent competition from national direct-to-consumer carriers with massive advertising budgets.

- •

Climate change leading to increased frequency and severity of catastrophic events, pressuring underwriting profitability.

- •

Economic downturns that could reduce demand for insurance or impact the investment portfolio.

- •

Regulatory changes affecting capital requirements, data privacy, or product approvals.

Recommendations

Priority Improvements

- Area:

Agent Digital Experience

Recommendation:Accelerate investment in a next-generation agent portal, focusing on API integrations, streamlined quoting and binding, and real-time data analytics to make Cincinnati Financial the easiest carrier for agents to work with.

Expected Impact:High

- Area:

Data Analytics & AI

Recommendation:Develop a centralized data analytics unit to leverage AI for enhanced risk modeling, claims fraud detection, and identifying cross-sell opportunities within the existing book of business to be passed as leads to agents.

Expected Impact:High

- Area:

Product Innovation for High-Net-Worth Segment

Recommendation:Expand the 'Private Client' product suite with tailored coverages for emerging HNW risks (e.g., cyber, reputation management, collections) to capture more market share in this profitable segment.

Expected Impact:Medium

Business Model Innovation

- •

Develop a 'Carrier-as-a-Service' platform, providing back-end underwriting, claims, and policy management services to select large, tech-enabled agencies or even some insurtechs, creating a new B2B revenue stream.

- •

Launch a venture capital arm to invest in early-stage insurtechs that are building technologies complementary to the independent agent channel, gaining early access to innovation.

- •

Create value-added risk management services using IoT devices (e.g., water leak detectors, security sensors) offered to policyholders at a discount, shifting from pure risk transfer to proactive risk mitigation.

Revenue Diversification

- •

Aggressively expand the Cincinnati Global and Cincinnati Re platforms to increase geographic and risk diversification outside the U.S. domestic market.

- •

Further build out the fee-based services from subsidiaries like CFC Investment Company.

- •

Explore offering standalone risk management consulting services to large commercial clients for a fee.

Cincinnati Financial Corporation operates a classic, highly successful, and mature insurance business model centered on an exclusive partnership with independent agents. Its strategic foundation is built on three unshakeable pillars: the primacy of the agent relationship, superior financial strength, and a reputation for excellent claims service. This model has proven remarkably durable, fostering deep loyalty within its distribution channel and allowing the company to consistently rank among the nation's top P&C insurers. The primary competitive advantage is defensible and sustainable; by positioning itself as the premier partner for high-performing agents, it insulates itself from the purely price-driven competition in the direct-to-consumer market.

The key strategic challenge and opportunity for evolution lie in navigating the digital transformation of the insurance industry. While its agent-centric model is a core strength, it also creates a risk of technological lag and distance from the end policyholder. The future market will not eliminate the need for expert advice, but it will demand that this advice be delivered through seamless, data-driven, and highly efficient digital platforms.

Therefore, the most critical path for strategic evolution is not to abandon its core model but to aggressively augment it with technology. The focus must be on 'empowering the agent'—providing them with superior digital tools, AI-powered insights, and streamlined processes that make Cincinnati Financial the most profitable and efficient carrier partner. Evolving the business model means transforming from an insurer that uses agents to a technology and service platform that powers the most successful independent agents in the market. Continued expansion into specialized, high-margin lines like E&S and a deeper penetration of the high-net-worth segment represent clear pathways for profitable growth, leveraging the existing strengths of the model.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

High Capital & Reserve Requirements

Impact:High

- Barrier:

Complex Regulatory & Licensing Hurdles

Impact:High

- Barrier:

Establishing a Competitive Distribution Network (e.g., agent relationships)

Impact:High

- Barrier:

Brand Recognition & Trust

Impact:Medium

- Barrier:

Data & Actuarial Expertise

Impact:Medium

Industry Trends

- Trend:

Digital Transformation & Insurtech Adoption

Impact On Business:Requires investment in technology to improve customer experience, agent tools, and operational efficiency to keep pace with digitally native competitors.

Timeline:Immediate

- Trend:

AI and Advanced Analytics

Impact On Business:AI is being used for underwriting, claims processing, and personalized pricing. Lagging in this area could lead to less competitive pricing and slower service.

Timeline:Immediate

- Trend:

Changing Customer Expectations

Impact On Business:Customers, especially younger demographics, expect seamless, digital, self-service options, which challenges the traditional agent-centric model.

Timeline:Immediate

- Trend:

Increased Frequency of Catastrophic Events

Impact On Business:Climate-related events increase claim costs and volatility, requiring sophisticated risk modeling and potentially higher premiums to maintain profitability.

Timeline:Near-term

- Trend:

Usage-Based Insurance (UBI)

Impact On Business:Telematics and IoT devices allow for more personalized risk assessment, a model pioneered by direct-to-consumer competitors that traditional models must adapt to.

Timeline:Near-term

Direct Competitors

- →

Travelers Companies, Inc.

Market Share Estimate:Approx. 4.5% of US P&C market.

Target Audience Overlap:High

Competitive Positioning:A leading provider of property and casualty insurance for business, personal, and specialty lines, leveraging a strong independent agent network and a reputation for claims management.

Strengths

- •

Strong brand recognition and long-standing history (founded 1853).

- •

Diverse product portfolio across personal, business, and specialty lines.

- •

Extensive network of independent agents and brokers.

- •

Robust financial stability and strong ratings.

Weaknesses

- •

High dependency on US markets.

- •

Exposure to significant catastrophe losses can impact profitability.

- •

Perceived as less innovative than insurtech competitors.

- •

Potential for deceleration in business insurance rates due to market competition.

Differentiators

- •

One of the largest and most established P&C carriers in the U.S.

- •

Strong focus on risk management and prevention services for commercial clients.

- •

Well-regarded for its claims handling process.

- →

The Hartford Financial Services Group, Inc.

Market Share Estimate:Top 15 P&C insurer in the U.S.

Target Audience Overlap:High

Competitive Positioning:A leader in property and casualty insurance, group benefits, and mutual funds, with a strong focus on the small business commercial market, often distributed through independent agents.

Strengths

- •

Market leader in small business insurance.

- •

Strong, established brand with over 200 years of history.

- •

Well-established relationships with independent agents and brokers.

- •

Diversified business including group benefits and mutual funds.

Weaknesses

- •

Can be perceived as a more traditional, slower-moving incumbent.

- •

Faces intense competition in the highly attractive small business segment.

- •

Digital experience may lag behind more modern competitors.

Differentiators

- •

Deep expertise and tailored products for the small business segment.

- •

Cross-selling opportunities between P&C and group benefits.

- •

Strong brand equity associated with stability and trust.

- →

Chubb Limited

Market Share Estimate:Approx. 3.5% of US P&C market.

Target Audience Overlap:Medium

Competitive Positioning:The world's largest publicly traded P&C insurance company, focusing on premium segments including high-net-worth personal lines and complex commercial risks, distributed through top-tier independent agents.

Strengths

- •

Global presence and operational scale.

- •

Leader in the high-net-worth personal insurance market.

- •

Renowned for superior underwriting discipline and claims service.

- •

Strong relationships with elite agents and brokers.

Weaknesses

- •

Less focused on the standard/mass-market personal and small business lines where Cincinnati competes heavily.

- •

Premium pricing may not be competitive for all segments.

- •

Large, complex organization can sometimes lead to slower decision-making.

Differentiators

- •

Specialization in affluent and high-net-worth clients.

- •

Exceptional reputation for handling large, complex claims ('white-glove' service).

- •

Broad, specialized commercial product offerings globally.

Indirect Competitors

- →

Progressive Corporation

Description:A leading direct-to-consumer (D2C) insurer, primarily for auto insurance, that also utilizes independent agents. Known for its heavy investment in technology, data analytics, and brand marketing.

Threat Level:High

Potential For Direct Competition:Already competes, but through a different primary business model (D2C). The threat is their model eroding the value proposition of the traditional agent-only model.

- →

Lemonade Inc.

Description:A digital-native insurtech company that uses AI, chatbots, and a mobile-first approach to offer renters, homeowners, car, and pet insurance with a focus on a younger demographic.

Threat Level:Medium

Potential For Direct Competition:Represents a disruptive business model that challenges the fundamental assumptions of the traditional insurance industry. While currently focused on simpler risks, their technological advantage and customer experience focus could allow them to move into more complex lines over time.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Loyal Independent Agent Network

Sustainability Assessment:Highly sustainable, but requires continuous investment. This network provides deep market penetration and trusted, personal relationships that are difficult for D2C models to replicate, especially for complex commercial or high-value personal lines.

Competitor Replication Difficulty:Hard

- Advantage:

Strong Financial Strength & Stability (A+ A.M. Best Rating)

Sustainability Assessment:Highly sustainable. This is a critical factor for both agents and policyholders, signifying the company's ability to pay claims, especially after major catastrophes.

Competitor Replication Difficulty:Hard

- Advantage:

Reputation for Excellent Claims Service

Sustainability Assessment:Sustainable with consistent operational focus. Positive claims experiences are a powerful retention tool and a key reason agents recommend Cincinnati Insurance.

Competitor Replication Difficulty:Medium

Temporary Advantages

No itemsDisadvantages

- Disadvantage:

Dependency on the Independent Agent Model

Impact:Major

Addressability:Moderately

- Disadvantage:

Slower Adoption of Digital & D2C Technologies

Impact:Major

Addressability:Moderately

- Disadvantage:

Lower Brand Recognition vs. Top D2C Competitors

Impact:Minor

Addressability:Difficult

Strategic Recommendations

Quick Wins

- Recommendation:

Launch an 'Agent Digital Toolkit' campaign

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Optimize 'Find an Agent' tool with better UX and agent bios

Expected Impact:Medium

Implementation Difficulty:Easy

Medium Term Strategies

- Recommendation:

Invest in a unified agent portal with real-time data analytics and quoting tools

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Develop API integrations for agents' management systems

Expected Impact:Medium

Implementation Difficulty:Moderate

- Recommendation:

Pilot a hybrid 'Agent + Digital' service model for specific segments like small business

Expected Impact:High

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Invest in or partner with an insurtech firm specializing in agent-facing technology

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Leverage AI and machine learning to provide agents with predictive insights for underwriting and client retention

Expected Impact:High

Implementation Difficulty:Difficult

Reinforce positioning as the premier insurance partner for top-tier independent agents, emphasizing that Cincinnati provides the best combination of financial strength, product breadth, and digital tools to help agents thrive.

Differentiate not by competing directly with D2C models, but by 'supercharging' the independent agent. The strategy should be to become the most technologically-enabled and responsive carrier for agents to work with, combining human touch with digital efficiency.

Whitespace Opportunities

- Opportunity:

Become the 'Carrier of Choice' for digitally-savvy independent agents

Competitive Gap:Many traditional carriers provide agents with clunky, outdated digital tools. Insurtechs ignore agents. There is a gap for a carrier that fully embraces and digitally empowers the agent channel.

Feasibility:High

Potential Impact:High

- Opportunity:

Target complex small-to-medium business (SMB) risks

Competitive Gap:D2C and insurtech models are often focused on simpler, high-volume personal lines or very small businesses. Complex SMBs still require the expertise of an agent, which aligns perfectly with Cincinnati's model.

Feasibility:High

Potential Impact:High

- Opportunity:

Develop specialized insurance products for emerging industries

Competitive Gap:New industries (e.g., renewable energy, gig economy services) have unique risks that off-the-shelf policies from D2C providers don't cover well. This requires specialized underwriting, a strength of the agent-based model.

Feasibility:Medium

Potential Impact:Medium

Cincinnati Financial Corporation operates in the mature and moderately concentrated U.S. Property & Casualty insurance market. Its core, sustainable competitive advantage is a deeply entrenched distribution model that relies exclusively on a network of high-quality independent agents. This model is fortified by a stellar reputation for financial strength (A+ A.M. Best rating) and superior claims service, creating a powerful value proposition for both agents and end-customers, particularly in complex commercial and high-value personal lines where expert advice is paramount.

Direct competitors like Travelers and The Hartford operate with a similar independent agent focus, competing on the quality of agent relationships, product offerings, and service levels. Chubb represents a more specialized threat, focusing on the high-net-worth segment where Cincinnati's 'Private Client' services also compete. The primary competitive threat, however, is not from these direct peers but from a fundamental shift in the market driven by indirect competitors. Large-scale direct-to-consumer (D2C) players like Progressive and digitally native insurtechs like Lemonade are reshaping customer expectations towards speed, transparency, and digital self-service. This places Cincinnati's agent-only model at a strategic crossroads.

The key challenge and opportunity for Cincinnati is not to abandon its core strength but to augment it with technology. The company's future success hinges on its ability to digitally empower its agent network. While competitors are focused on disintermediating the agent, Cincinnati has a significant whitespace opportunity to become the carrier that provides the best digital tools, data analytics, and responsive systems for agents. This strategy would transform their primary dependency from a potential weakness into a tech-enabled, defensible advantage. By focusing on complex risks that D2C models struggle to automate and by making their agents the most efficient and insightful in the industry, Cincinnati can solidify its market position and continue to thrive.

Messaging

Message Architecture

Key Messages

- Message:

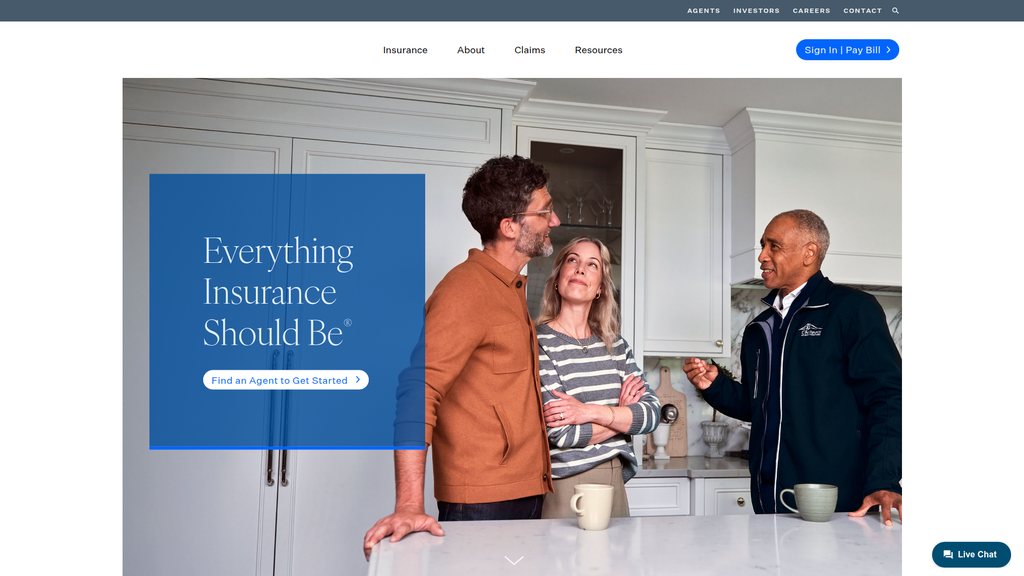

Everything Insurance Should Be®

Prominence:Primary

Clarity Score:Medium

Location:Homepage Hero, About Us Hero

- Message:

We operate exclusively through local, independent agents who provide personal service and professional advice.

Prominence:Primary

Clarity Score:High

Location:Homepage ('Why Independent Agents'), About Us ('Relationships'), 'The Cincinnati Difference' sections

- Message:

We possess superior financial strength to keep our promises and pay claims.

Prominence:Secondary

Clarity Score:High

Location:About Us ('Financial Strength'), 'The Cincinnati Difference' section

- Message:

We offer tailored, comprehensive personal and business insurance solutions.

Prominence:Secondary

Clarity Score:High

Location:Homepage product sections (Individuals & Families, Business Insurance)

- Message:

Insurance is a relationship business.

Prominence:Tertiary

Clarity Score:High

Location:About Us, 'The Cincinnati Difference'

The message hierarchy is logical and well-structured. The primary focus on the independent agent model as the core delivery mechanism is immediately clear. The homepage effectively splits the audience into 'Individuals & Families' and 'Business,' then immediately reinforces the agent-centric model as the universal value proposition. The tagline 'Everything Insurance Should Be®' acts as a consistent, high-level brand promise that frames all other messaging.

Messaging is exceptionally consistent across the analyzed pages. The core themes of agent partnership, personal relationships, financial strength, and superior service are repeated verbatim or in concept in every major section, creating a cohesive and unified brand narrative. There are no notable contradictions.

Brand Voice

Voice Attributes

- Attribute:

Professional

Strength:Strong

Examples

- •

Complex risks deserve personal service.

- •

Receive exceptional insurance solutions backed by a company with superior financial strength.

- •

Our A+ (Superior) financial strength rating from A.M. Best Co. demonstrates our ability to keep our promises...

- Attribute:

Reassuring

Strength:Strong

Examples

- •

Find the peace of mind you deserve.

- •

Enjoy the open road with confidence.

- •

Protect your family's financial future.

- Attribute:

Traditional

Strength:Moderate

Examples

- •

Since 1950, we’ve operated exclusively through independent agents...

- •

Our Ethic identifies the values we demonstrate in our daily work.

- •

Community bonds them to you in ways that less personal, automated insurance programs cannot.

- Attribute:

Caring

Strength:Moderate

Examples

- •

I have never experienced such caring and professionalism from an insurance company.

- •

Your life is full of treasured memories and cherished belongings. Let us help protect them...

- •

Experience more than a policy; experience a company that believes in putting people first.

Tone Analysis

Formal and Assured

Secondary Tones

Empathetic

Trustworthy

Tone Shifts

The tone shifts from professional and product-focused in the main site copy to more personal and empathetic in the customer testimonial section.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Cincinnati Insurance delivers superior, tailored insurance products and unparalleled claims service through a dedicated, exclusive network of local independent agents, ensuring a personal, professional relationship backed by exceptional financial stability.

Value Proposition Components

- Component:

Exclusive Independent Agent Model

Clarity:Clear

Uniqueness:Unique

- Component:

Personal Service & Relationships

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Superior Financial Strength (A+ Rating)

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Unparalleled Claims Service

Clarity:Somewhat Clear

Uniqueness:Common

The primary differentiator is the exclusive reliance on the independent agent model. While many carriers use independent agents, Cincinnati's messaging frames it as a foundational, non-negotiable part of their identity, positioning them against direct-to-consumer carriers (like Geico) and carriers with captive agents (like State Farm). The combination of this distribution model with a strong emphasis on financial stability creates a compelling niche. However, the claim of 'unparalleled claims service' is a common industry platitude and is not sufficiently substantiated with unique evidence beyond a single testimonial.

The messaging positions Cincinnati Insurance as a premium, relationship-focused carrier for consumers and businesses who value expert guidance, personal service, and long-term stability over transactional convenience or the lowest possible price. They compete not on price, but on the value of the agent's counsel and the promise of reliable claims handling.

Audience Messaging

Target Personas

- Persona:

Individuals & Families

Tailored Messages

- •

Your life is full of treasured memories and cherished belongings. Let us help protect them with tailored personal insurance.

- •

Find the peace of mind you deserve.

- •

Protect your family's financial future.

Effectiveness:Effective

- Persona:

Small Businesses

Tailored Messages

Big solutions for small businesses.

Insurance programs that offer comprehensive coverage and the flexibility to grow with your tomorrows.

Effectiveness:Somewhat Effective

- Persona:

Large/Complex Businesses

Tailored Messages

Complex risks deserve personal service.

Receive exceptional insurance solutions backed by a company with superior financial strength.

Effectiveness:Effective

- Persona:

Independent Agents (Implied)

Tailored Messages

- •

We do business exclusively through them.

- •

Unparalleled claims service, convenient technology solutions, competitive products and empowered, local associates are just some of the reasons independent agents choose Cincinnati...

- •

Our vision is to be the best company serving independent agents.

Effectiveness:Effective

Audience Pain Points Addressed

- •

The complexity and confusion of choosing the right insurance ('guessing isn’t enough').

- •

The impersonal nature of automated or direct insurance providers.

- •

The fear of an insurer not being able to pay a claim.

- •

The risk of having inadequate coverage for one's specific needs.

Audience Aspirations Addressed

- •

Achieving 'peace of mind' and confidence.

- •

Protecting treasured belongings and memories.

- •

Securing the financial future of one's family or business.

- •

Preserving a distinctive lifestyle (for Private Client).

- •

Building a long-term, trusted relationship with a professional advisor.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Security & Safety

Effectiveness:High

Examples

- •

Let us help protect them with tailored personal insurance.

- •

Protect your family's financial future.

- •

Our business is protecting businesses like yours.

- Appeal Type:

Peace of Mind

Effectiveness:High

Examples

Find the peace of mind you deserve.

Enjoy the open road with confidence.

- Appeal Type:

Trust & Reliability

Effectiveness:High

Examples

- •

Since 1950...

- •

Our A+ (Superior) financial strength rating...

- •

I have never experienced such caring and professionalism...

Social Proof Elements

- Proof Type:

Customer Testimonial

Impact:Strong

- Proof Type:

Longevity (Since 1950)

Impact:Moderate

- Proof Type:

Expert Validation (A.M. Best A+ Rating)

Impact:Strong

Trust Indicators

- •

Explicitly stated A+ (Superior) financial strength rating from A.M. Best.

- •

Mention of being founded in 1950, implying stability and longevity.

- •

Clear explanation of their values ('Our Ethic').

- •

Detailed 'About Us' section with information on subsidiaries and company structure.

- •

Professional website design and clear, error-free copy.

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

Find an Agent

Location:Homepage Hero, Why Independent Agents section, The Cincinnati Difference section, About Us Hero

Clarity:Clear

- Text:

Learn More

Location:Individuals & Families section, Business Insurance section, About Us section

Clarity:Clear

- Text:

Explore

Location:Product cards for Home, Auto, Life, Private Client, and Business segments

Clarity:Clear

The CTAs are clear and logically aligned with the business model, consistently funneling users towards their distribution channel—the independent agents. However, they lack strong persuasive language. The primary CTA, 'Find an Agent,' is functional but could be more benefit-oriented (e.g., 'Connect with a Local Expert'). The secondary CTAs ('Learn More', 'Explore') are generic and could be made more specific and compelling to increase click-through rates.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of quantifiable proof for claims like 'unparalleled claims service'. More statistics, case studies, or a variety of testimonials would add significant weight.

- •

Insufficiently developed messaging for the 'Private Client' segment. The promise to 'Preserve your distinctive lifestyle' is vague and doesn't communicate the specific, elevated services this clientele expects.

- •

The value proposition for the end-customer choosing a Cincinnati-affiliated agent over another independent agent (who may represent multiple carriers) is not articulated. The messaging sells the agent model, but not why a Cincinnati agent is superior.

Contradiction Points

No itemsUnderdeveloped Areas

- •

The 'convenient technology solutions' mentioned in 'The Cincinnati Difference' are not detailed, representing a missed opportunity to appeal to audiences who value digital convenience alongside personal service.

- •

Messaging for specific industries under the 'Business Insurance' section is generic. Tailored content addressing the unique risks of different professions would be more effective.

- •

The narrative of 'putting people first' could be brought to life with stories about their agents or employees, moving from a statement to a demonstrated value.

Messaging Quality

Strengths

- •

Exceptional clarity and consistency in its core strategic message: the value of the independent agent.

- •

Effectively builds trust through repeated emphasis on financial strength and longevity.

- •

Clean, professional, and reassuring brand voice that aligns perfectly with the conservative nature of the insurance industry.

- •

Clear audience segmentation on the homepage guides users to relevant information quickly.

Weaknesses

- •

Over-reliance on industry jargon and abstract concepts like 'peace of mind' and 'protecting what matters most' without sufficient tangible examples.

- •

The overall tone is conservative and safe, lacking a distinct personality that could make the brand more memorable.

- •

Missed opportunities to quantify value. For example, 'What is the average claim satisfaction score?' or 'How quickly are claims typically processed?'

- •

The messaging is more company-centric ('what we do') than customer-centric ('what you get').

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition Substantiation

Recommendation:Create a dedicated 'Claims Excellence' section featuring a variety of testimonials, case studies (anonymized), and key performance indicators (e.g., claim satisfaction scores, speed of payment) to transform 'unparalleled service' from a claim into a fact.

Expected Impact:High

- Area:

Audience-Specific Messaging

Recommendation:Develop detailed landing pages for each 'Industry' under Business Insurance, using language and scenarios specific to those professions to demonstrate deep expertise.

Expected Impact:High

- Area:

Call-to-Action Language

Recommendation:A/B test more benefit-driven CTA copy. Change 'Find an Agent' to 'Get a Personal Consultation' or 'Partner with a Local Expert'. Change 'Explore' to 'See Your Coverage Options'.

Expected Impact:Medium

Quick Wins

- •

Revise the 'Private Client' headline to be more specific and exclusive, such as 'Specialized Protection for High-Value Assets and Lifestyles.'

- •

Add a short sub-headline under the main testimonial to highlight the key outcome (e.g., '...allowing my mother to quickly return to her home.').

- •

In the 'Why Independent Agents' section, add a bulleted list of direct benefits for the customer (e.g., 'Objective advice from multiple carriers', 'Personalized risk assessment', 'A local advocate during a claim').

Long Term Recommendations

- •

Develop a content marketing strategy focused on storytelling. Feature blog posts or videos that spotlight individual agents and their positive impact on clients' lives, humanizing the brand and making the 'relationship' promise tangible.

- •

Invest in creating interactive tools or resources that help potential customers understand their risks, providing upfront value and reinforcing the brand's role as a knowledgeable advisor.

- •

Refine the overall brand narrative to more clearly articulate why an agent who partners with Cincinnati can offer a superior experience for the end-customer compared to an agent who partners with other A-rated carriers.

Cincinnati Financial's strategic messaging is a masterclass in consistency and clarity of purpose. The brand's core identity is inextricably linked to its exclusive independent agent distribution model, and this message is executed with disciplined precision across the website. The primary value propositions—the expertise of a local agent, the personal relationship, and the backing of a financially sound company—are communicated effectively, creating a strong position against direct-to-consumer competitors. The brand voice is professional, reassuring, and trustworthy, which is perfectly suited to the insurance industry and its target audience of individuals and businesses who prioritize stability and expert counsel over low cost.

However, the messaging, while consistent, is also conservative and relies heavily on industry platitudes. Claims of 'unparalleled service' and 'putting people first' are asserted but not sufficiently proven with tangible, multi-faceted evidence. This creates a messaging gap where the brand tells you it's different but doesn't always show you how in a memorable way. The primary weakness lies in the lack of specific, quantifiable proof points and compelling storytelling that could elevate the message from simply credible to truly differentiating.

The key business opportunity is to inject more vitality and tangible proof into the existing strong framework. By substantiating its claims with diverse testimonials, case studies, and performance data, Cincinnati can add a powerful layer of rational persuasion to its strong emotional appeals. Furthermore, by developing more specific messaging for its distinct business segments (like Private Client and various industries) and humanizing its agent network through storytelling, the company can deepen engagement and more effectively demonstrate why it is 'Everything Insurance Should Be®'.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Established in 1950, demonstrating long-term market presence and stability.

- •

Consistently high financial strength rating (A+ from A.M. Best), indicating reliability and trustworthiness to agents and policyholders.

- •

Exclusive focus on the independent agent channel has built deep, defensible relationships and expertise within that specific market.

- •

Recent reports indicate double-digit premium growth, suggesting strong demand for their products through their chosen channel.

- •

Personal lines net written premiums have nearly tripled over the last decade, showing significant growth in a key segment.

Improvement Areas

- •

Enhancing digital tools and platforms for independent agents to improve their efficiency and sales effectiveness.

- •

Developing a direct-to-insured digital service portal (for claims, policy documents, etc.) to augment the agent relationship and meet modern customer expectations.

- •

Creating more flexible and personalized insurance products to compete with insurtech offerings, such as usage-based or on-demand insurance.

Market Dynamics

Moderate (~5-7% Net Written Premium Growth Forecast for 2025)

Mature

Market Trends

- Trend:

Digital Transformation and Insurtech Adoption

Business Impact:Pressure to modernize legacy systems and provide digital tools for agents and policyholders to remain competitive with direct-to-consumer writers and tech-enabled carriers.

- Trend:

Evolving Customer Expectations

Business Impact:Customers increasingly expect seamless, self-service digital experiences, even when buying through an agent, creating a need for omnichannel service models.

- Trend:

Increased Use of AI and Data Analytics

Business Impact:Opportunity to leverage AI for more sophisticated underwriting, pricing, claims processing, and fraud detection, but requires significant investment in technology and talent.

- Trend:

Rising Catastrophe Losses and Climate Risk

Business Impact:Increased volatility in underwriting results and higher reinsurance costs, necessitating advanced risk modeling and disciplined underwriting.

Crucial inflection point. The market is rapidly digitizing. While their traditional model is strong, the window to adapt and digitally empower their agent channel is now. Delaying could lead to significant market share erosion to more agile competitors.

Business Model Scalability

Medium

Balanced structure with significant fixed costs (underwriting, claims infrastructure, corporate overhead) and variable costs tied to growth (agent commissions, claims payouts).

Moderate. Growth is contingent on recruiting and enabling a finite number of independent agents, which is less scalable than a pure technology-driven D2C model. However, technology can increase the productivity of each agent, creating leverage.

Scalability Constraints

- •

Dependence on a human-led sales force (independent agents) limits the speed of customer acquisition.

- •

Onboarding and training new agencies is a time-intensive process.

- •

Potential for legacy IT systems to hinder the rollout of new products and digital services at scale.

Team Readiness

Experienced leadership with deep industry knowledge, as evidenced by long-term profitable growth and recent strategic restructuring to focus on distinct market segments.

Traditional, relationship-focused structure. Recently reorganized to separate commercial/life and personal/specialty operations, which should improve focus and accountability for growth in those segments.

Key Capability Gaps

- •

Digital Product Management: Need for experts who can translate agent and customer needs into effective digital tools and experiences.

- •

Data Science & AI: Requires talent to build and implement advanced analytical models for underwriting, pricing, and claims.

- •

User Experience (UX) Design: Critical for developing intuitive and efficient agent portals and customer-facing applications.

Growth Engine

Acquisition Channels

- Channel:

Independent Agent Network

Effectiveness:High

Optimization Potential:High

Recommendation:Develop a best-in-class digital agent portal with features like instant quoting, automated marketing tools, and data analytics on their book of business to make them more productive and loyal to Cincinnati.

Customer Journey

Primarily offline and agent-driven. The website's main function is to validate the brand and connect prospects with a local agent. The actual sales process is handled entirely by the agent.

Friction Points

- •

Lack of online quoting capability for digitally-native customers.

- •

Multiple steps required to get from the website to a conversation with an agent.

- •

Inconsistent customer experience that varies by agent.

- •

Absence of self-service options for simple inquiries or policy management.

Journey Enhancement Priorities

{'area': 'Agent Handoff', 'recommendation': "Implement a 'smart' agent finder that not only locates nearby agents but also allows for immediate digital contact or appointment scheduling directly from the website."}

{'area': 'Policyholder Servicing', 'recommendation': 'Launch a secure customer portal and mobile app where policyholders can view documents, make payments, and initiate a claim, reducing reliance on agents for basic administrative tasks.'}

Retention Mechanisms

- Mechanism:

Agent Relationship

Effectiveness:High

Improvement Opportunity:Strengthen the direct brand relationship with the end-customer through digital communication and servicing tools, creating stickiness beyond the agent.

- Mechanism:

Claims Service

Effectiveness:High

Improvement Opportunity:Incorporate digital claims processing (e.g., photo-based estimates, virtual assistants for status updates) to increase speed and transparency, augmenting the human touch.

- Mechanism:

Multi-Policy Bundling

Effectiveness:Medium

Improvement Opportunity:Use data analytics to proactively identify cross-sell and bundling opportunities for agents, providing them with targeted campaigns to deepen client relationships.

Revenue Economics

As a large, established insurer, unit economics (driven by the combined ratio) are likely well-understood and managed for profitability. Recent reports show strong underwriting results, despite catastrophe losses, indicating disciplined pricing.

Likely healthy (industry ideal is >3:1). CAC is primarily agent commissions, a variable cost. LTV is high due to the recurring nature of premiums and high retention driven by agent relationships.

High within their model, but potentially lower than tech-first competitors due to higher operational costs associated with a human-centric, multi-layered distribution system.

Optimization Recommendations

- •

Invest in technology to increase agent productivity (premium written per agent).

- •

Use predictive analytics to refine underwriting and pricing, improving the loss ratio component of the combined ratio.

- •

Automate routine administrative and claims tasks to lower the expense ratio.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Systems

Impact:High

Solution Approach:Adopt a two-speed IT architecture. Maintain legacy systems for core policy administration while using modern, API-driven platforms for new digital agent and customer experiences.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting Processes

Growth Impact:Slows down quote-to-bind times, particularly for complex commercial or private client risks, potentially losing business to faster competitors.

Resolution Strategy:Implement an AI-powered underwriting workbench that automates data ingestion and analysis, freeing up underwriters to focus on high-judgment decisions.

- Bottleneck:

Agent Onboarding and Enablement

Growth Impact:Limits the pace at which new agents can be brought into the network and become productive.

Resolution Strategy:Develop a digital onboarding and continuous training platform for agents, providing on-demand resources and certifications.

Market Penetration Challenges

- Challenge:

Intense Competition from Direct-to-Consumer (D2C) Insurers

Severity:Critical

Mitigation Strategy:Double down on the value proposition of the independent agent as an expert advisor, and equip them with digital tools that provide a comparable level of convenience to D2C platforms.

- Challenge:

Perception of Independent Agent Model as Outdated

Severity:Major

Mitigation Strategy:Launch co-branded marketing campaigns with agents that highlight the 'best of both worlds': expert human advice powered by modern technology.

Resource Limitations

Talent Gaps

- •

Insurtech product managers

- •

AI/Machine learning engineers

- •

Cybersecurity specialists

- •

Digital marketing experts focused on channel enablement

Significant capital investment required for a multi-year digital transformation initiative, including core system modernization and development of new digital platforms.

Infrastructure Needs

Cloud-based infrastructure to support new applications and data analytics workloads.

Modern API gateway to enable seamless integration with third-party and agent systems.

Growth Opportunities

Market Expansion

- Expansion Vector:

Deeper Penetration in High-Growth States

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Use data analytics to identify states/regions with high premium potential but low market share. Launch targeted agent recruitment campaigns in these areas.

- Expansion Vector:

Targeting Niche Commercial Segments

Potential Impact:Medium

Implementation Complexity:Medium

Recommended Approach:Develop specialized insurance products and risk management services for specific industries (e.g., tech startups, renewable energy) and train select agents to become experts in these niches.

Product Opportunities

- Opportunity:

Embedded Insurance Offerings

Market Demand Evidence:Growing trend for insurance to be offered at the point of sale for other products/services (e.g., buying a car, securing a loan).

Strategic Fit:High, if agent-fulfilled. This creates a new lead source for agents.

Development Recommendation:Develop APIs that allow partners (e.g., auto dealers, mortgage lenders) to offer a Cincinnati quote, with the lead being routed to a local agent to finalize the policy.

- Opportunity:

Cyber Insurance for Small Businesses

Market Demand Evidence:Rising threat of cyber attacks creates a significant and growing need for specialized coverage among small and mid-sized businesses.

Strategic Fit:High

Development Recommendation:Partner with a leading cybersecurity firm to bundle risk mitigation services (e.g., employee training, vulnerability scanning) with the insurance policy, creating a differentiated offering.

Channel Diversification

- Channel:

Digital Self-Service Portal (Agent-Centric)

Fit Assessment:High

Implementation Strategy:Develop a white-label portal that agents can brand and offer to their clients. This enhances the agent's value proposition rather than competing with them.

- Channel:

Strategic Partnerships with B2B Software Platforms

Fit Assessment:High

Implementation Strategy:Integrate with platforms like payroll providers or accounting software to generate qualified leads that are then passed to independent agents to close.

Strategic Partnerships

- Partnership Type:

Insurtech Technology Providers

Potential Partners

AI claims processing platforms (e.g., Tractable, CCC Intelligent Solutions)

Data analytics and risk modeling firms

Expected Benefits:Accelerate digital transformation without building all capabilities in-house; improve underwriting accuracy and operational efficiency.

- Partnership Type:

Affinity Groups & Associations

Potential Partners

Trade associations for small businesses

Alumni associations

Expected Benefits:Provide a source of high-quality, targeted leads for agents specializing in those affinity groups.

Growth Strategy

North Star Metric

Agent-Driven Premium Growth

This metric directly aligns with their core business model. It measures not just overall growth, but the health and productivity of their sole acquisition channel—the independent agents. It combines new agent acquisition with existing agent productivity.

Achieve and sustain 10-12% year-over-year growth in net written premiums originating from the independent agent channel.

Growth Model

Channel-Led Growth (B2B2C)

Key Drivers

- •

Agent Recruitment (Expanding the network)

- •

Agent Enablement (Increasing productivity of existing agents with technology)

- •

Agent Retention (Ensuring loyalty and preventing churn to competitors)

Focus all growth investments on making independent agents more successful. This means prioritizing the development of tools, resources, and support systems that help agents win more business and serve clients more efficiently.

Prioritized Initiatives

- Initiative:

Next-Generation Agent Portal

Expected Impact:High

Implementation Effort:High

Timeframe:18-24 months

First Steps:Form a dedicated product team with agent representation to define the MVP feature set, focusing on a streamlined quote-and-bind process for a key product line.

- Initiative:

Co-Branded Digital Marketing Toolkit for Agents

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:6-9 months

First Steps:Develop a pilot program with a small group of tech-savvy agents to create templates for social media, email newsletters, and local SEO that they can easily customize and deploy.

- Initiative:

Policyholder Self-Service App (Phase 1)

Expected Impact:High

Implementation Effort:High

Timeframe:12-18 months

First Steps:Launch a foundational app focused on non-licensed activities: viewing policy documents, checking claim status, and making payments. Promote it as a tool provided by the agent.

Experimentation Plan

High Leverage Tests

{'test': 'A/B test different commission incentives or bonuses for agents selling new, strategic products (e.g., cyber insurance).'}

{'test': "Pilot a 'digital lead generation' program for a select group of agents, funded by corporate marketing, to measure the ROI of direct lead support."}

Use an Objectives and Key Results (OKR) framework. For each experiment, define a clear objective (e.g., Increase cyber policy sales) and measurable key results (e.g., 20% lift in quote-to-bind ratio, 15% increase in agent participation).

Quarterly review of ongoing pilots and launch of 1-2 new strategic experiments.

Growth Team

A dedicated 'Agent Success' or 'Channel Growth' team that sits at the intersection of marketing, technology, and sales. This team's sole mission is to improve agent productivity and growth.

Key Roles

- •

Head of Agent Digital Experience (Product Owner for agent-facing tech)

- •

Channel Marketing Manager (Develops tools and programs for agents)

- •

Agent Training & Onboarding Specialist

- •

Data Analyst (Focus on agent performance and market opportunity)

Recruit talent from outside the traditional insurance industry, particularly from SaaS companies with strong channel sales models, to bring in fresh perspectives on partner enablement.

Cincinnati Insurance Companies possesses a powerful and enduring growth foundation built on deep, trust-based relationships with its exclusive network of independent agents. This model has proven resilient and profitable, establishing a strong brand reputation for service and financial stability. However, the company is at a critical strategic crossroads. The insurance industry's rapid digital transformation, driven by insurtech innovation and shifting consumer expectations, poses a direct threat to traditional, relationship-only models.

The primary barrier to future growth is not the agent-centric model itself, but the current lack of digital enablement surrounding it. The customer journey is fragmented and offline, creating friction for modern buyers and operational inefficiencies for agents. Legacy technology is likely a significant inhibitor to the rapid deployment of necessary digital tools.

The most significant growth opportunity lies not in abandoning its core strategy, but in supercharging it. By transforming from a product provider to a true 'platform' for its agents, Cincinnati can create a powerful hybrid model. The strategic imperative is to invest heavily in a best-in-class technology stack—including a next-generation agent portal, co-branded marketing automation, and a customer self-service platform—that empowers agents to compete and win against digital-first competitors.

Recommendations are prioritized around this central theme: empower the agent. The 'North Star Metric' should be Agent-Driven Premium Growth, focusing the entire organization on making their channel partners more successful. By launching initiatives like a modernized agent portal and a digital marketing toolkit, Cincinnati can enhance agent productivity, strengthen loyalty, and create a defensible competitive advantage that combines the best of expert human advice with the convenience of modern technology. This channel-led growth model is the key to sustainable, scalable growth in the evolving insurance landscape.

Legal Compliance

The website provides a centralized 'Privacy Policies' page, which is a strong practice. It links to several distinct notices: an 'Electronic Privacy Policy' for website users, a GLBA-mandated 'Notice of Privacy Practices' for insurance customers, and a specific 'California Privacy Notice'. This layered approach is appropriate for a financial institution. The GLBA notice details the types of nonpublic personal information (NPI) collected and disclosed, as required by law. The California notice outlines rights under the CCPA/CPRA, including the right to know, delete, and correct information. However, the path to finding a 'Do Not Sell or Share My Personal Information' link is not immediately obvious from the homepage footer, which is a common and expected practice under CCPA/CPRA.

A comprehensive 'Terms & Conditions' document is accessible via the website footer. It covers key areas such as the informational purpose of the site, disclaimers of liability, limitations on use, and procedures for DMCA notices. The document explicitly states that the website content does not constitute legal or financial advice and that an attorney-client relationship is not formed, which is a crucial disclaimer for a company in a highly regulated industry. It also includes sections on internet communication security and user-posted content, demonstrating a good understanding of potential liabilities associated with an interactive web presence.

Upon visiting the website, a cookie consent banner appears at the bottom of the screen. It provides 'Accept All Cookies' and 'Cookie Settings' options. This granular control is a best practice under GDPR and CCPA. The banner links to the 'Electronic Privacy Policy' which explains the types of cookies used (essential, performance, functional, targeting). This mechanism provides users with clear information and choice regarding tracking technologies, which is a significant strength in their compliance posture.

Cincinnati Financial, as an insurance and financial services company, is primarily regulated by the Gramm-Leach-Bliley Act (GLBA), which governs the protection of Nonpublic Personal Information (NPI). Their privacy notices reflect GLBA requirements by explaining how customer data is collected, used, shared, and protected. For California residents, the company provides a specific CCPA notice, addressing the broader definition of 'personal information' beyond NPI. This demonstrates a clear understanding that while GLBA exempts certain data, other data collected (e.g., from general website visitors or prospective employees) falls under CCPA jurisdiction. The company also has a London-based subsidiary, Cincinnati Global, which implies GDPR applicability. While a specific GDPR notice is not prominent on the main cinfin.com site, their global entity likely maintains separate, compliant policies.

The website footer includes a dedicated 'Accessibility' link, which leads to an Accessibility Statement. The statement affirms commitment to digital accessibility for people with disabilities and references the Web Content Accessibility Guidelines (WCAG). This public commitment is a critical first step in mitigating legal risk under the Americans with Disabilities Act (ADA). The site appears to use standard HTML elements and has a logical structure, but a full technical audit would be required to determine the exact level of WCAG 2.1 AA conformance. The presence of the statement and clear navigation are positive indicators.

As a multi-state licensed insurer, the company is subject to a complex web of state-level insurance regulations and oversight from bodies like the National Association of Insurance Commissioners (NAIC). The website demonstrates compliance by providing clear information about its subsidiaries, their roles, and financial strength ratings (A.M. Best), which builds trust and meets regulatory expectations for transparency. They also provide specific notices as required by certain states, such as the 'New York Domestic Violence Notice,' indicating an active process for monitoring and adhering to state-specific mandates. The core of their compliance is centered on GLBA, which dictates privacy and data security standards for financial institutions, and their policies are structured accordingly.

Compliance Gaps

- •

The 'Do Not Sell or Share My Personal Information' link, a key requirement of the CCPA/CPRA, is not directly visible or easily accessible from the homepage footer. It is nested within the 'California Privacy Notice'.

- •

While the company has a UK subsidiary, the applicability of GDPR to data collected through the primary US-facing website (cinfin.com) is not explicitly addressed for potential EU/UK visitors.

- •

The website's Terms & Conditions includes a general disclaimer about the Internet being an unsecure medium, but it could be strengthened by providing more detail on the specific security measures (e.g., encryption) used to protect data in transit and at rest.

Compliance Strengths

- •