eScore

citizensbank.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Citizens Bank demonstrates a strong and mature digital presence, effectively aligning its content with the customer journey from awareness to decision. The bank has high authority in its regional markets, supported by a comprehensive content hub that positions it as a helpful financial advisor. However, its national visibility is moderate compared to giants like Chase, and it shows an underdeveloped strategy for voice search optimization, which is a growing channel.

Excellent content marketing strategy through its 'Learning' hub, which effectively targets top-of-funnel prospects with educational content and aligns with user search intent for key financial life stages.

Develop a formal voice search optimization strategy by creating conversational content (FAQs, Q&A pages) to capture featured snippets and answer queries on smart speakers and digital assistants.

The brand's messaging is highly consistent, with an empowering and helpful voice that resonates across product pages and educational content. It effectively tailors messages to key audience segments like students and homeowners, addressing specific pain points with unique product features like 'Multi-Year Approval'. The primary weakness is an over-reliance on abstract brand slogans in high-visibility placements and an underutilization of social proof like customer testimonials.

Clear and compelling value propositions for specific products (e.g., 'Citizens FastLine®' HELOC), which effectively differentiate them in a crowded market by solving tangible customer problems.

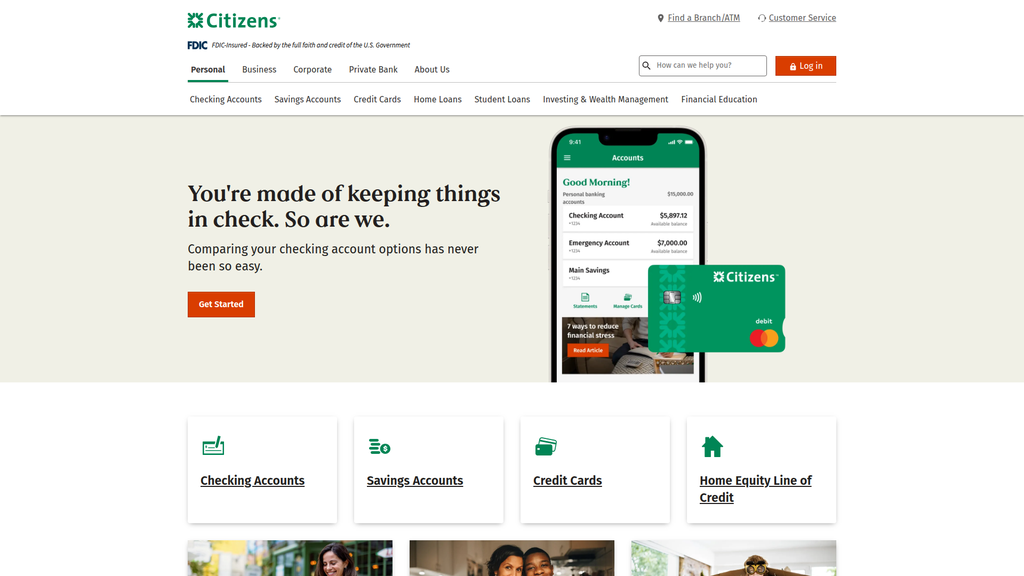

A/B test the main homepage headline, comparing the current abstract slogan ('You're made of keeping things in check. So are we.') with a more direct, benefit-oriented message to potentially improve immediate user comprehension and conversion.

The website offers a visually clean, mobile-responsive, and intuitive user experience with a light cognitive load on primary pages. Primary CTAs are effective, and the bank has a stated commitment to WCAG AA accessibility standards, which is a significant strength. However, the analysis notes inconsistent styling for secondary CTAs and content-dense pages that can increase friction, along with a need to further streamline digital onboarding processes to match fintech competitors.

Excellent mobile responsiveness and a logical information architecture ensure a seamless and intuitive user journey across devices for core tasks.

Unify the design of all secondary and tertiary CTAs, converting plain text links into a consistent secondary button style (e.g., ghost buttons) to improve visibility and guide users more effectively through non-primary conversion paths.

As a large, FDIC-insured financial institution, credibility is a core strength. The bank showcases a best-in-class approach to legal and regulatory compliance, with multi-layered privacy policies (GLBA, CCPA) and a proactive, public stance on digital accessibility. The strategic placement of trust signals like 'Member FDIC' and 'Equal Housing Lender' is effective, though the site could benefit from more third-party validation like awards and customer success stories.

A proactive and transparent commitment to digital accessibility (WCAG 2.1 AA), which significantly mitigates legal risk and strengthens the brand's reputation for inclusivity.

Prominently feature customer testimonials, case studies, and any industry awards on the homepage and key product pages to add powerful social proof and third-party validation.

Citizens Bank's competitive moat is built on sustainable, traditional advantages: brand trust established since 1828, a large physical branch network for omnichannel service, and deep regulatory expertise. However, its advantages in digital innovation are often temporary, as it struggles to match the pace of fintech disruptors. The high switching costs associated with being a primary bank for multiple products (checking, mortgage, etc.) remain a significant, albeit passive, advantage.

The combination of an extensive physical branch network with a robust digital platform provides a key omnichannel advantage that digital-only competitors cannot replicate, catering to a wider range of customer preferences.

Instead of building all technology in-house, establish a more aggressive fintech partnership strategy to rapidly integrate innovative features, increasing the pace of digital innovation and closing the gap with nimbler competitors.

The bank demonstrates strong scalability potential, driven by strategic acquisitions to expand its geographic footprint and a clear focus on digital transformation to improve efficiency. As a large, well-capitalized institution, funding for growth is not a constraint. The primary limitations are operational bottlenecks from legacy technology and a high fixed-cost structure tied to its branch network, which the leadership is actively addressing through modernization programs.

A proven strategy of growth through strategic acquisitions (e.g., HSBC East Coast branches, Investors Bancorp) that successfully expands market presence and customer base in key metropolitan areas.

Accelerate the modernization of the core banking platform to a more agile, cloud-native, API-driven architecture to reduce technical debt and speed up the development of new, scalable digital products.

Citizens operates a highly coherent and mature business model, with a diversified revenue mix of net interest income and a growing base of fee-based income. The strategic focus is clear: blend digital convenience with human advice, targeting key consumer and business segments. Recent strategic moves, like expanding the private bank and making targeted acquisitions, are well-aligned with the goal of growing higher-margin revenue streams and solidifying its regional market leadership.

Strong alignment between its market positioning as a full-service regional leader and its operational execution, which combines digital investment with leveraging its physical branch network for high-value advisory services.

Further diversify revenue streams by aggressively expanding wealth management and other fee-based services to reduce sensitivity to net interest margin compression from interest rate fluctuations.

As a top-15 US bank, Citizens is a major regional power but lacks the market-shaping influence of national giants like JPMorgan Chase. Its market share trajectory is stable to growing within its footprint, bolstered by acquisitions. However, it has limited pricing power in a competitive market and is more of a market follower than a trendsetter in digital innovation, often reacting to moves made by larger banks and fintechs.

Significant market share and brand recognition within its core geographic footprint (Northeast, Mid-Atlantic, Midwest), creating a defensible position against competitors in those regions.

Invest in creating proprietary, data-driven research reports on regional economic trends to establish thought leadership, generate high-quality media mentions, and increase its influence within its key markets.

Business Overview

Business Classification

Diversified Financial Services

Retail & Commercial Banking

Financial Services

Sub Verticals

- •

Consumer Banking

- •

Commercial Banking

- •

Wealth Management

- •

Student Lending

- •

Mortgage Lending

Mature

Maturity Indicators

- •

Established brand with a history dating back to 1828.

- •

Operates approximately 1,000 branches and 3,100 ATMs.

- •

Significant total assets ($218.3 billion as of June 2025).

- •

Consistent dividend payments for 12 consecutive years.

- •

Growth strategy focused on strategic acquisitions (e.g., Investors Bancorp, HSBC East Coast branches) and digital transformation.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Interest Income (NII)

Description:The primary driver of revenue, representing the difference between interest earned on assets (loans such as mortgages, student loans, commercial loans) and interest paid on liabilities (customer deposits, debt). This is the core revenue stream for the banking operation.

Estimated Importance:Primary

Customer Segment:All Segments (Consumer & Commercial)

Estimated Margin:Medium

- Stream Name:

Non-interest Income (Fee-Based)

Description:Revenue generated from fees for services, including account maintenance fees, credit card interchange and annual fees, wealth management advisory fees, capital markets advisory fees, and mortgage servicing rights.

Estimated Importance:Secondary

Customer Segment:All Segments (Consumer & Commercial)

Estimated Margin:High

Recurring Revenue Components

- •

Interest income from loan portfolios

- •

Account maintenance fees

- •

Wealth management and advisory fees

- •

Credit card annual fees

Pricing Strategy

Relationship-based & Tiered Pricing

Mid-range

Opaque

Pricing Psychology

- •

Bundling (e.g., checking with savings)

- •

Tiered offerings (e.g., different checking account levels with varying benefits)

- •

Relationship discounts (e.g., lower rates for wealth management clients)

Monetization Assessment

Strengths

- •

Diversified revenue across consumer and commercial banking, reducing reliance on a single segment.

- •

Large, stable base of low-cost deposits provides a funding advantage.

- •

Growing fee-based income from wealth management and capital markets provides higher-margin revenue.

Weaknesses

- •

High dependence on Net Interest Income, making the business vulnerable to interest rate fluctuations.

- •

Pressure on fee income remains a potential risk.

- •

Intense price competition on loan and deposit rates from larger national banks and fintechs.

Opportunities

- •

Expand wealth management services (Citizens Private Bank) to capture more fee income from high-net-worth clients.

- •

Increase cross-selling of products (e.g., mortgages, investments) to existing deposit customers using data analytics.

- •

Develop more digital-native, fee-based financial wellness and planning tools.

Threats

- •

Prolonged low-interest-rate environments can compress net interest margins.

- •

Economic downturns can increase loan defaults and reduce demand for banking services.

- •

Competition from fintech companies and neobanks offering low-fee or no-fee banking products.

Market Positioning

Full-service regional banking leader with a focus on building deep customer relationships and expanding nationally through digital channels and strategic acquisitions.

Leading regional bank, primarily concentrated in the Northeastern, Mid-Atlantic, and Midwestern United States.

Target Segments

- Segment Name:

Mass Market & Mass Affluent Consumers

Description:Individuals and households requiring day-to-day banking services, planning for life events, and seeking financial advice. This includes a spectrum from basic checking account holders to emerging affluent clients needing wealth management.

Demographic Factors

Middle-to-high income households

All age ranges, with specific products for students and seniors

Psychographic Factors

- •

Value convenience and a mix of digital and in-person banking

- •

Seek a trusted, established financial partner

- •

Goal-oriented (saving for a home, retirement, college)

Behavioral Factors

- •

Use mobile and online banking for transactions

- •

Visit branches for complex needs or advice ('Citizens Checkup')

- •

Hold multiple products with a single institution (checking, savings, credit card, mortgage)

Pain Points

- •

Feeling overwhelmed by financial planning

- •

Difficulty saving consistently

- •

Complex and slow application processes for loans (e.g., HELOC)

- •

Lack of personalized financial advice

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Students & Young Adults

Description:College students and recent graduates who are beginning their financial journey, often with student loan needs and a desire to build credit.

Demographic Factors

Ages 18-29

Currently enrolled in or recently graduated from higher education

Psychographic Factors

- •

Digitally native and expect seamless mobile experiences

- •

Price-sensitive and wary of fees

- •

Seeking financial education and simple tools

Behavioral Factors

- •

Heavy mobile banking users

- •

Early adopters of new financial technology

- •

Highly influenced by peer reviews and online presence

Pain Points

- •

Managing student loan debt

- •

Establishing a credit history

- •

Learning how to budget and save effectively

- •

High fees on basic banking accounts

Fit Assessment:Good

Segment Potential:High

- Segment Name:

Small to Mid-Sized Enterprises (SMEs) & Middle-Market Companies

Description:Businesses requiring a suite of services including lending, treasury and payment services, and capital markets solutions.

Demographic Factors

Varies by industry, but concentrated in the bank's geographic footprint

Psychographic Factors

- •

Value relationships with their bankers

- •

Seek a bank that understands their industry and local market

- •

Need efficient and scalable cash management solutions

Behavioral Factors

Utilize a mix of digital treasury tools and in-person relationship management

Complex borrowing and cash management needs

Pain Points

- •

Access to capital for growth

- •

Inefficient payment and receivables processing

- •

Managing cash flow effectively

- •

Lack of strategic financial advice from banking partners

Fit Assessment:Excellent

Segment Potential:High

Market Differentiation

- Factor:

Strong Regional Branch Network

Strength:Strong

Sustainability:Sustainable

- Factor:

Specialized Product Offerings (e.g., Multi-Year Student Loan Approval, Citizens FastLine HELOC)

Strength:Moderate

Sustainability:Temporary

- Factor:

Integrated Digital and Human Service Model ('Citizens Checkup')

Strength:Moderate

Sustainability:Sustainable

- Factor:

Content Marketing and Financial Education Hub

Strength:Moderate

Sustainability:Sustainable

Value Proposition

Citizens provides a comprehensive and convenient range of financial products and personalized guidance, helping individuals and businesses manage their finances today and plan for their future.

Good

Key Benefits

- Benefit:

Convenience through Integrated Channels

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Extensive branch and ATM network

- •

Full-featured mobile and online banking platform

- •

Ability to schedule appointments online ('Citizens Checkup')

- Benefit:

Tailored Products for Key Life Stages

Importance:Important

Differentiation:Somewhat unique

Proof Elements

- •

Student loans with multi-year approval

- •

FastLine HELOC for homeowners

- •

Variety of checking and credit card options

- Benefit:

Proactive Financial Guidance and Education

Importance:Important

Differentiation:Common

Proof Elements

- •

Online 'Learning' center with articles and calculators

- •

Personalized planning with bankers via 'Citizens Checkup'

- •

Budgeting and saving tools integrated into digital banking (e.g., 'Round Ups')

Unique Selling Points

- Usp:

Citizens FastLine® HELOC offers an accelerated, simplified application and funding process.

Sustainability:Medium-term

Defensibility:Moderate

- Usp:

Multi-Year Approval for student loans simplifies funding for a student's entire college career.

Sustainability:Medium-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Need for simple, accessible day-to-day banking services.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Navigating complex financial decisions for major life goals (homeownership, education).

Severity:Major

Solution Effectiveness:Partial

- Problem:

Difficulty in consistently saving money and building wealth.

Severity:Major

Solution Effectiveness:Partial

Value Alignment Assessment

High

The value proposition of being a stable, full-service bank aligns well with the needs of the mainstream banking market, which values trust, convenience, and a breadth of services.

High

The focus on convenience, digital tools, and products for key life stages (student loans, mortgages) directly addresses the primary pain points of its core consumer segments.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Payment Networks (Mastercard, Visa).

- •

Core Banking Technology Providers (Fiserv, Jack Henry & Associates).

- •

Credit Bureaus (Experian, TransUnion, Equifax)

- •

Small Business Administration (SBA).

- •

Fintech partners for specific capabilities

Key Activities

- •

Retail and Commercial Lending

- •

Deposit Gathering

- •

Payment Processing

- •

Wealth Management & Financial Advisory

- •

Risk Management and Regulatory Compliance

- •

Digital Platform Development and Maintenance

Key Resources

- •

Brand Reputation and Trust

- •

Extensive Branch and ATM Network

- •

Large Customer Deposit Base (Capital)

- •

Digital Banking Platform

- •

Relationship Managers and Financial Advisors

Cost Structure

- •

Interest Expense (paid on deposits)

- •

Salaries and Employee Benefits

- •

Technology and Infrastructure Costs

- •

Marketing and Customer Acquisition Costs

- •

Provision for Credit Losses

- •

Real Estate and Branch Operations

Swot Analysis

Strengths

- •

Strong brand recognition and long history.

- •

Diversified portfolio of consumer and commercial products.

- •

Significant market presence in core geographic regions.

- •

Robust digital platforms and ongoing investment in technology.

Weaknesses

- •

Geographic concentration in the Northeastern US, despite digital expansion efforts.

- •

Higher operating costs associated with maintaining a large physical branch network.

- •

Perception as a traditional bank, which may be less appealing to digitally-native younger generations compared to fintechs.

Opportunities

- •

Accelerate digital transformation to create a best-in-class customer experience and improve operational efficiency.

- •

Expand national presence through digital-first products like Citizens Access.

- •

Grow the high-margin wealth management and private banking businesses.

- •

Leverage data and analytics for deeper customer personalization and cross-selling.

Threats

- •

Intense competition from national banking giants (JPMorgan Chase, Bank of America) and agile fintech companies.

- •

Economic downturns leading to increased loan defaults.

- •

Evolving regulatory landscape and increased compliance costs.

- •

Cybersecurity threats targeting customer data and financial assets.

Recommendations

Priority Improvements

- Area:

Digital Onboarding & User Experience

Recommendation:Further streamline digital application processes for all products to match the speed and simplicity of the 'FastLine HELOC'. Invest in UX/UI enhancements to create a more personalized and intuitive mobile/online banking experience.

Expected Impact:High

- Area:

Data Analytics & Personalization

Recommendation:Develop a more sophisticated data analytics engine to proactively identify customer needs and deliver hyper-personalized product recommendations and financial advice through digital channels, moving beyond content marketing to contextual offers.

Expected Impact:High

- Area:

Operational Efficiency

Recommendation:Continue the Transformation of Operational Performance (TOP) program to automate back-office processes and optimize the branch network based on changing customer behavior, potentially reformatting some branches into smaller, digitally-focused advisory centers.

Expected Impact:Medium

Business Model Innovation

- •

Launch a subscription-based financial wellness service that bundles premium digital tools, dedicated financial coaching (human or AI-driven), and preferential rates, moving beyond a purely transactional model.

- •

Develop a Banking-as-a-Service (BaaS) platform, allowing non-financial companies to embed Citizens' banking products (e.g., loans, accounts) into their own ecosystems, opening a new B2B2C channel.

- •

Create a 'Life Moments' platform that integrates banking services with third-party partners around key events like buying a home (realtors, movers), attending college (student services), or starting a business (legal, accounting).

Revenue Diversification

- •

Aggressively expand the Citizens Private Bank and wealth management offerings to capture a larger share of the high-net-worth market and increase fee-based revenue.

- •

Enhance the SME/Commercial banking suite with more sophisticated, fee-generating treasury management and international trade finance solutions.

- •

Explore opportunities in insurance or point-of-sale financing through strategic partnerships or acquisitions to capture more of the customer's financial wallet.

Citizens Financial Group operates a mature, well-diversified business model characteristic of a leading super-regional bank. Its core strength lies in its established brand, extensive branch network in key regions, and a comprehensive product suite serving both consumers and businesses. The primary revenue driver is traditional Net Interest Income, supported by a growing contribution from non-interest (fee) income sources.

The bank's strategic evolution is clearly focused on navigating the transition from a traditional, branch-centric model to an integrated, digitally-enabled institution. Strategic acquisitions of Investors Bancorp and HSBC's East Coast branches have solidified its market position in the attractive Northeast corridor, while investments in its digital platform, including the national online-only bank Citizens Access, signal a clear intent to compete beyond its physical footprint.

The primary challenge and opportunity for Citizens is to balance the costs and culture of its legacy operations with the speed, efficiency, and customer experience demanded by the digital age. Competitors range from national behemoths with larger technology budgets to nimble fintechs unencumbered by physical infrastructure. Citizens' key differentiators—specialized products like the FastLine HELOC and a service model that blends human advice with digital convenience ('Citizens Checkup')—are vital assets. However, to achieve sustainable competitive advantage, the bank must accelerate its digital transformation, focusing on creating a seamless, personalized customer journey powered by data analytics. Future growth will be contingent on its ability to enhance operational efficiency, successfully expand its higher-margin wealth management business, and innovate its business model to capture new, recurring revenue streams beyond traditional banking.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

Regulatory Compliance and Licensing

Impact:High

- Barrier:

High Capital Requirements

Impact:High

- Barrier:

Brand Trust and Reputation

Impact:High

- Barrier:

Legacy Technology Integration

Impact:Medium

- Barrier:

Economies of Scale

Impact:High

Industry Trends

- Trend:

Digital Transformation and AI Integration

Impact On Business:Requires significant investment in technology to meet customer expectations for seamless, personalized digital experiences. AI is being used for everything from fraud detection to customer service chatbots.

Timeline:Immediate

- Trend:

Competition from Neobanks and Fintechs

Impact On Business:Erosion of customer base, particularly among younger demographics, due to fintechs' superior user experience, lower fees, and niche product offerings.

Timeline:Immediate

- Trend:

Hyper-Personalization

Impact On Business:Customers expect banks to use their data to provide tailored advice, product recommendations, and customized experiences, moving beyond a one-size-fits-all approach.

Timeline:Near-term

- Trend:

Embedded Finance (Banking-as-a-Service)

Impact On Business:Financial services are increasingly integrated into non-financial platforms, creating both partnership opportunities and competitive threats as the traditional bank-customer relationship is disintermediated.

Timeline:Near-term

- Trend:

Focus on Financial Wellness and Education

Impact On Business:Banks are moving beyond transactional services to become trusted advisors, offering tools and content (like Citizens' 'Learning' section) to help customers manage their financial health.

Timeline:Immediate

Direct Competitors

- →

JPMorgan Chase & Co.

Market Share Estimate:Largest US bank by assets

Target Audience Overlap:High

Competitive Positioning:Positions itself as a global, technology-first financial powerhouse offering a comprehensive suite of services for every customer segment, emphasizing scale, security, and digital convenience.

Strengths

- •

Massive scale and economies of scale, leading to higher profitability.

- •

Industry-leading mobile app and digital platform with high adoption rates.

- •

Strong brand recognition and reputation for stability.

- •

Vast physical branch and ATM network.

- •

Highly diversified revenue streams across retail, investment, and wealth management.

Weaknesses

- •

Less agile and slower to innovate on niche products compared to fintechs.

- •

Can be perceived as impersonal or bureaucratic due to its large size.

- •

Higher potential for regulatory scrutiny due to its systemic importance.

Differentiators

- •

Unmatched breadth of integrated financial products under one roof.

- •

Significant and continuous investment in technology and digital innovation.

- •

Dominant position in credit cards and investment banking.

- →

PNC Financial Services Group

Market Share Estimate:Top 10 US bank by assets, significant super-regional player

Target Audience Overlap:High

Competitive Positioning:A 'Main Street Bank' approach that combines the capabilities of a large national bank with a focus on community-level service and relationships.

Strengths

- •

Strong presence in many of Citizens' core markets (Mid-Atlantic, Midwest).

- •

Well-regarded for its Virtual Wallet product, integrating checking, savings, and budgeting tools.

- •

Strong corporate and institutional banking division.

- •

Acquisition of BBVA USA expanded its national footprint.

Weaknesses

- •

Digital offerings, while solid, are not typically seen as cutting-edge as Chase or fintechs.

- •

Brand recognition is lower outside of its primary geographic footprint.

- •

Still integrating a major acquisition, which can lead to operational challenges.

Differentiators

- •

Virtual Wallet product is a key differentiator in the digital checking space.

- •

Emphasis on financial wellness and education for consumers.

- •

Significant focus on corporate social responsibility and community investment.

- →

KeyBank

Market Share Estimate:Significant US regional bank

Target Audience Overlap:High

Competitive Positioning:Focuses on targeted client segments and relationship banking, leveraging fintech partnerships to enhance capabilities rather than building everything in-house.

Strengths

- •

Strong focus on specific commercial niches (e.g., healthcare, real estate).

- •

Agile in forming partnerships with fintechs to accelerate innovation.

- •

Emphasis on providing financial wellness tools and personalized guidance.

- •

Growing its commercial banking presence in new markets.

Weaknesses

- •

Smaller marketing budget and brand recognition compared to national players.

- •

Physical branch network is less dense than larger competitors.

- •

Reliance on partners could create integration complexities.

Differentiators

- •

Strategic focus on specific industries for its commercial business.

- •

Openness to fintech partnerships as a core strategy.

- •

HelloWallet tool and a stated focus on financial confidence for clients.

Indirect Competitors

- →

Chime

Description:A leading US neobank offering fee-free mobile banking services, including checking and savings accounts, early direct deposit, and a credit-builder card.

Threat Level:High

Potential For Direct Competition:High - Already competes for primary checking account relationships, especially with Millennial and Gen Z customers.

- →

SoFi

Description:A digital personal finance company that started with student loan refinancing and has expanded into a comprehensive suite of products including personal loans, mortgages, credit cards, investing, and banking.

Threat Level:High

Potential For Direct Competition:High - Directly competes with Citizens' key lending products (student loans, personal loans) and is building a full digital banking ecosystem.

- →

PayPal / Venmo

Description:Dominant digital payment platforms that are expanding into adjacent financial services like credit products, savings accounts, and cryptocurrency, disintermediating the bank's role in daily transactions.

Threat Level:Medium

Potential For Direct Competition:Medium - While not a full-service bank, it erodes the bank's relationship with the customer and share of their financial life, particularly in payments.

- →

Rocket Mortgage

Description:A digital-first mortgage lender that has streamlined the mortgage application process, competing directly with traditional bank offerings like home equity lines of credit and mortgages.

Threat Level:High (in the mortgage sector)

Potential For Direct Competition:Low (outside of lending) - Focused primarily on mortgage and home-related lending, but sets a high bar for digital user experience that customers expect elsewhere.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Established Brand Trust and History

Sustainability Assessment:Highly sustainable, as trust is built over decades and is a primary consideration for consumers in banking.

Competitor Replication Difficulty:Hard

- Advantage:

Physical Branch Network

Sustainability Assessment:Moderately sustainable. While less important for daily transactions, branches remain key for complex advice, sales, and serving certain demographics, providing an omnichannel advantage over digital-only players.

Competitor Replication Difficulty:Hard

- Advantage:

Regulatory Expertise and FDIC Insurance

Sustainability Assessment:Highly sustainable. Provides a fundamental layer of security and trust that newer, less-regulated fintechs often partner with banks to achieve.

Competitor Replication Difficulty:Hard

- Advantage:

Diversified Product Portfolio

Sustainability Assessment:Highly sustainable. The ability to serve a customer's full lifecycle (student loans, first credit card, mortgage, wealth management) creates high switching costs and deepens relationships.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Innovative Product Features (e.g., Multi-Year Student Loan Approval)', 'estimated_duration': '12-24 months before competitors replicate the concept if successful.'}

{'advantage': 'Promotional Interest Rates (e.g., for HELOCs or Savings)', 'estimated_duration': 'Short-term, highly dependent on market conditions and competitive responses.'}

Disadvantages

- Disadvantage:

Legacy Technology Infrastructure

Impact:Major

Addressability:Difficult

- Disadvantage:

Pace of Digital Innovation vs. Fintechs

Impact:Major

Addressability:Moderate

- Disadvantage:

Brand Perception Among Younger Demographics

Impact:Major

Addressability:Moderate

- Disadvantage:

Smaller National Marketing Budget vs. 'Big Four' Banks

Impact:Minor

Addressability:Difficult

Strategic Recommendations

Quick Wins

- Recommendation:

Prominently feature and integrate financial wellness tools and calculators from the 'Learning' hub into the main dashboard of the mobile and online banking experience.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Launch targeted digital marketing campaigns highlighting the 'Citizens FastLine' HELOC, emphasizing speed and convenience to directly counter fintech lenders.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Simplify the digital account opening process by reducing the number of steps and required fields to be more competitive with neobanks.

Expected Impact:High

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Develop a hyper-personalization engine that uses customer data to provide proactive, tailored financial advice and product suggestions within the digital banking platform.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Form strategic partnerships with fintechs to integrate innovative features (e.g., advanced budgeting, subscription management) rather than building all capabilities in-house.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Invest in a unified 'phygital' (physical + digital) customer experience, where digital appointments scheduled online lead to seamless, data-informed conversations in-branch.

Expected Impact:Medium

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Continue modernizing the core banking platform to a more agile, API-driven architecture to accelerate future product development and reduce technical debt.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Explore niche digital banking propositions for underserved professional segments (e.g., traveling nurses, freelance creatives) that leverage the bank's core strengths but with a fintech-like user experience.

Expected Impact:Medium

Implementation Difficulty:Difficult

Position Citizens as 'The People-First Digital Bank,' blending the trust and comprehensive services of a traditional bank with a simple, empathetic, and forward-looking digital experience.

Differentiate on pragmatic and accessible financial guidance. While national banks compete on scale and fintechs on niche features, Citizens can win by being the most trusted and practical financial partner, delivering seamless advice across digital and physical channels.

Whitespace Opportunities

- Opportunity:

Integrated Financial Wellness Platform

Competitive Gap:Many banks offer educational content, but few integrate it with actionable, personalized tools within the core banking experience. This bridges the gap between their content and their products.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Voice Banking for Everyday Transactions

Competitive Gap:The use of voice assistants for banking is an emerging field. Developing secure, convenient voice commands for checking balances, transferring funds, or getting spending summaries could capture a first-mover advantage.

Feasibility:Medium

Potential Impact:Medium

- Opportunity:

Small Business Digital Onboarding and Support

Competitive Gap:While many fintechs serve consumers, the digital onboarding and support experience for small businesses at traditional banks often lags. A streamlined, fully-digital process could attract significant business deposits.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Family-Oriented Banking Features

Competitive Gap:Few traditional banks offer integrated tools for families, such as linked teen debit cards with parental controls, shared savings goals, and financial literacy modules for kids, a space where fintechs are innovating.

Feasibility:Medium

Potential Impact:Medium

Comprehensive Competitive Landscape Analysis: Citizens Bank

Citizens Financial Group operates as a large, established super-regional bank in a mature and highly concentrated US banking industry. The market is an oligopoly, dominated by a handful of money-center banks (JPMorgan Chase, Bank of America, etc.) that set the pace for digital innovation and marketing spend. Citizens' primary competitive set includes these national players as well as other super-regional banks like PNC and KeyBank, which often share the same geographic footprint and target customer base.

Key Competitive Dynamics

The primary competitive axis has shifted decisively from physical branches to the digital customer experience. While a branch network remains a sustainable advantage for trust-building and complex advisory services, the battle for customer acquisition and daily engagement is now fought on mobile apps and websites. This presents Citizens' core challenge: balancing the strengths of a traditional institution with the need for fintech-like agility and innovation.

Direct Competitors:

* JPMorgan Chase represents the top tier of competition, leveraging immense scale and a massive technology budget to offer a best-in-class digital platform that creates high customer expectations.

* PNC and KeyBank are more direct peers. PNC competes effectively with its integrated 'Virtual Wallet' product, while KeyBank differentiates through a focused strategy on specific commercial niches and a greater willingness to partner with fintechs to accelerate innovation.

Indirect Competitors & Disruptors:

The most significant threat comes from a bifurcated group of indirect competitors:

1. Neobanks (e.g., Chime): These digital-only players excel at customer acquisition, especially among younger, less affluent demographics, by offering a superior mobile experience, low-to-no fees, and features like early direct deposit. They are successfully unbundling the traditional checking account relationship.

2. Specialized Fintechs (e.g., SoFi, Rocket Mortgage): These competitors attack specific, profitable product lines of traditional banks (student loans, mortgages, personal loans) with streamlined digital processes, transparent pricing, and a strong brand identity within their niche. SoFi, in particular, poses a major long-term threat as it reconstructs a full-service bank on a modern, digital-native platform.

Citizens' Competitive Position

Citizens is positioned as a full-service, relationship-oriented bank. Its website content reinforces this by highlighting a complete product suite—from basic checking to student loans and HELOCs—and a strong emphasis on financial education through its 'Learning' hub. This strategy aims to capture customers for their entire financial lifecycle.

Strengths:

* Trust and Brand Equity: As an FDIC-insured bank with a long history, it holds a significant trust advantage over new entrants.

* Omnichannel Presence: The combination of a physical branch network and digital platforms accommodates a wider range of customer preferences than digital-only competitors.

* Diversified Product Set: Ability to cross-sell and bundle products increases customer stickiness and lifetime value.

Weaknesses:

* Pace of Innovation: Like most traditional banks, Citizens is hampered by legacy technology, making it slower to launch new digital features compared to fintechs built on modern architecture.

* Digital User Experience: While functional, the user experience may not match the seamless, intuitive design that younger customers have come to expect from leading consumer tech apps and neobanks.

* Brand Perception: May be perceived as a 'traditional' or 'older' bank, posing a challenge in attracting the next generation of customers.

Strategic Opportunities & Recommendations

The most significant whitespace opportunity for Citizens lies in bridging the gap between its traditional strengths and modern customer expectations. This involves leveraging its educational content and reputation for trustworthy advice and delivering it through a hyper-personalized, proactive digital experience.

Strategic Imperatives:

1. Double Down on Financial Guidance: Transform the 'Learning' content from a static resource into an integrated, interactive financial wellness platform within the core banking app. This can become a key differentiator against both product-focused fintechs and impersonal national banks.

2. Embrace 'Smart' Partnerships: Instead of trying to build everything, Citizens should strategically partner with best-in-class fintechs to quickly integrate sought-after features (e.g., subscription management, advanced budgeting) into its own platform, enhancing its value proposition.

3. Modernize the Onboarding Experience: The new account opening process is a critical first impression. Radically simplifying this digital journey is essential to reduce abandonment and compete effectively with the near-instant onboarding offered by neobanks.

Messaging

Message Architecture

Key Messages

- Message:

You're made of keeping things in check. So are we.

Prominence:Primary

Clarity Score:Medium

Location:Homepage Hero

- Message:

Comparing your checking account options has never been so easy.

Prominence:Secondary

Clarity Score:High

Location:Homepage Hero

- Message:

A card for where you are and where you're going.

Prominence:Secondary

Clarity Score:High

Location:Homepage - Credit Cards Section

- Message:

Pay for college with Multi-Year Approval.

Prominence:Secondary

Clarity Score:High

Location:Homepage - Student Loans Section

- Message:

Money in as little as two weeks. Meet Citizens FastLine®, the simpler, faster way to get a Home Equity Line of Credit.

Prominence:Secondary

Clarity Score:High

Location:Homepage - HELOC Section

- Message:

Turn your spare change into savings with Round Ups.

Prominence:Tertiary

Clarity Score:High

Location:Homepage - Savings Section

- Message:

Knowing how to save money wisely can make you ready for anything that lies ahead.

Prominence:Primary

Clarity Score:High

Location:Learning Center - Saving and Budgeting Page

The homepage effectively prioritizes key consumer banking products (Checking, Credit Cards, HELOC, Student Loans) which are likely primary drivers of customer acquisition. The main brand message is given top prominence, followed immediately by a clear, benefit-oriented message about checking accounts. The hierarchy is logical, guiding users from a broad brand concept to specific, solution-oriented product messages.

Messaging is highly consistent. The theme of empowerment and readiness ('made of keeping things in check', 'made you ready for anything') is present on both the homepage and the educational content. The product-focused messaging on the homepage is complemented by the advice-driven, educational content in the 'Learning' section, creating a cohesive user journey from product discovery to financial education.

Brand Voice

Voice Attributes

- Attribute:

Empowering

Strength:Strong

Examples

- •

You're made of keeping things in check. So are we.

- •

Ready to take control of your finances?

- •

Whatever your goals are, we can help you find ways in the moment and still save for tomorrow.

- Attribute:

Helpful

Strength:Strong

Examples

- •

We made savings easier...

- •

Learn how to budget and be prepared.

- •

With a Citizens Checkup®, our bankers can help you focus on what's important...

- Attribute:

Straightforward

Strength:Moderate

Examples

- •

Comparing your checking account options has never been so easy.

- •

Meet Citizens FastLine®, the simpler, faster way to get a Home Equity Line of Credit.

- •

With the 50/30/20 budget method, you divide your income into three simple categories.

- Attribute:

Approachable

Strength:Moderate

Examples

College prep is a lot, but the right college funding can be a lot off your back.

Turn your spare change into savings...

Tone Analysis

Reassuring and Competent

Secondary Tones

Educational

Aspirational

Tone Shifts

The tone shifts from promotional and product-focused on the homepage to advisory and educational in the 'Learning' section. This shift is appropriate for the context and serves the user's intent in each section.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Citizens Bank is a financial partner that understands your responsible nature and provides simple, accessible tools and expert guidance to help you manage your financial journey and prepare for the future.

Value Proposition Components

- Component:

Simplicity & Speed (HELOC)

Clarity:Clear

Uniqueness:Somewhat Unique

Details:The 'Citizens FastLine®' with its promise of 'simpler, faster' and 'money in as little as two weeks' is a strong, tangible value proposition. While speed is a common competitive angle, branding it creates distinctiveness.

- Component:

Long-Term Planning (Student Loans)

Clarity:Clear

Uniqueness:Unique

Details:'Multi-Year Approval' for student loans directly addresses a major pain point for students and families: the need to re-apply for funding each year. This is a significant differentiator.

- Component:

Effortless Saving (Savings Accounts)

Clarity:Clear

Uniqueness:Common

Details:The 'Round Ups' feature is clearly explained and appeals to a desire for easy, automated savings. However, this feature is now common among both traditional banks and fintech competitors.

- Component:

Personalized Guidance (Overall)

Clarity:Somewhat Clear

Uniqueness:Common

Details:The 'Citizens Checkup®' and 'Meet with a banker' offerings communicate personalized advice. While this is a standard offering for full-service banks, the branded 'Checkup' adds a tangible, proactive feel.

Citizens' differentiation strategy appears to hinge on specific, branded product features that address acute customer pain points ('Multi-Year Approval', 'Citizens FastLine®'). This is more effective than competing on generic claims of 'good service'. While some features like 'Round Ups' are not unique, the overall message of being a partner for the responsible, forward-planning customer ('You're made of keeping things in check') provides a solid, if subtle, brand identity. The brand platform seems to be an evolution of their 'Made Ready' campaign, which was designed to appeal to customers on their unique, non-linear life journeys.

The messaging positions Citizens as a large, capable regional bank that offers the product breadth of a national player (like Truist or KeyBank) but with a more approachable, customer-centric focus. It avoids the overtly 'local' feel of a small community bank, instead projecting an image of a sophisticated, digitally-savvy institution that makes banking easier and aligns with customers' life stages.

Audience Messaging

Target Personas

- Persona:

Students and Parents

Tailored Messages

- •

Pay for college with Multi-Year Approval.

- •

College prep is a lot, but the right college funding can be a lot off your back.

- •

How to save money in college

Effectiveness:Effective

- Persona:

Homeowners

Tailored Messages

- •

Money in as little as two weeks

- •

Meet Citizens FastLine®, the simpler, faster way to get a Home Equity Line of Credit.

- •

Use your home equity

Effectiveness:Effective

- Persona:

Aspiring Savers / Budgeters

Tailored Messages

- •

Turn your spare change into savings with Round Ups‡

- •

Knowing how to save money wisely can make you ready for anything that lies ahead.

- •

4 budgeting strategies

Effectiveness:Effective

- Persona:

Credit Builders/Users

Tailored Messages

A card for where you are and where you're going

Looking to establish credit, earn cash back, or access exclusive events?

Effectiveness:Somewhat Effective

Audience Pain Points Addressed

- •

The complexity and hassle of comparing bank accounts.

- •

The stress and repetitive nature of applying for student loans annually.

- •

The slow, cumbersome process of getting a home equity line of credit.

- •

The difficulty of actively saving money.

- •

Feeling overwhelmed by budgeting and financial planning.

Audience Aspirations Addressed

- •

Gaining control over personal finances.

- •

Being prepared for the future.

- •

Achieving major life goals (college, homeownership).

- •

Building a strong credit history.

- •

Making financial management feel simple and effortless.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Empowerment/Control

Effectiveness:High

Examples

You're made of keeping things in check.

Ready to take control of your finances?

- Appeal Type:

Peace of Mind/Security

Effectiveness:Medium

Examples

...the right college funding can be a lot off your back.

Knowing how to save money wisely can make you ready for anything that lies ahead.

- Appeal Type:

Aspiration

Effectiveness:Medium

Examples

A card for where you are and where you're going.

map out a plan for your future.

Social Proof Elements

- Proof Type:

Statistic

Impact:Strong

Details:The student loan disclaimer includes a powerful data point: 'Multi-Year Approval borrowers have a 99% approval rate on future requests for additional funds.' This is a highly persuasive statistic for the target audience.

Trust Indicators

- •

Member FDIC logo

- •

Equal Housing Lender logo

- •

Clear contact information (Phone, Chat, In-person)

- •

Branch and ATM locator

- •

Explicit mention of bankers and appointments ('Meet with a banker')

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

Get Started

Location:Homepage Hero (Checking)

Clarity:Clear

- Text:

Explore credit cards

Location:Homepage (Credit Cards)

Clarity:Clear

- Text:

Learn about multi-year approval

Location:Homepage (Student Loans)

Clarity:Clear

- Text:

Use your home equity

Location:Homepage (HELOC)

Clarity:Clear

- Text:

Start Saving

Location:Homepage (Savings)

Clarity:Clear

- Text:

Schedule an appointment

Location:Homepage (Meet with a banker)

Clarity:Clear

The CTAs are consistently clear, concise, and use action-oriented language. They are logically placed after a value proposition, telling the user exactly what the next step is. The variety of CTAs ('Get Started', 'Explore', 'Learn', 'Use') is well-matched to the user's likely stage of consideration for each product.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of prominent messaging for business banking or wealth management clients on the consumer-facing homepage. This suggests a clear segmentation in their digital strategy, but could miss cross-sell opportunities.

- •

The corporate mission ('To help our customers, colleagues, and communities reach their potential') is not explicitly communicated. While the 'customer' part is implied, the 'community' aspect is a missed opportunity for brand building and emotional connection.

- •

There are no customer testimonials or stories on the homepage, which are powerful persuasion tools used to build trust and connection.

Contradiction Points

No itemsUnderdeveloped Areas

The core brand concept ('You're made of...') is evocative but abstract. It could be strengthened by connecting it more directly to tangible customer outcomes or stories.

Messaging around digital banking tools is focused on basic features ('mobile check deposit'). There is an opportunity to highlight more advanced features like budgeting tools, alerts, or security measures that reinforce the 'keeping things in check' theme.

Messaging Quality

Strengths

- •

Excellent clarity on product-level value propositions.

- •

Strong alignment between brand voice (empowering, helpful) and content.

- •

Effective audience segmentation with tailored messaging for key life stages (college, homeownership).

- •

The 'Learning' section successfully positions the bank as an expert advisor, building trust beyond transactions.

Weaknesses

- •

The main headline is creative but lacks a direct, compelling benefit. Its abstract nature may be less effective than a more straightforward value statement.

- •

Differentiation from major competitors is reliant on specific product features rather than an overarching, unique brand promise that is immediately obvious.

- •

Underutilization of social proof elements like customer stories or awards.

Opportunities

- •

Integrate storytelling, especially around the 'community' aspect of the corporate mission, to build a stronger emotional brand.

- •

Elevate the 'Citizens Checkup®' from a simple service offering to a core part of the brand promise, framing the bank as a proactive financial wellness partner.

- •

Develop more content around the 'where you're going' aspirational theme, showcasing how Citizens helps customers achieve long-term goals.

- •

A/B test the homepage hero message to compare the current brand-centric slogan with a more benefit-driven headline to optimize customer acquisition.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Hero Messaging

Recommendation:Test an alternative primary headline that is more direct and benefit-oriented, such as 'Banking that's ready for your journey' or 'The partner for your financial plan.'

Expected Impact:High

- Area:

Social Proof

Recommendation:Incorporate a 'Customer Stories' or 'Member Spotlight' section on the homepage, featuring short, compelling testimonials with photos or videos.

Expected Impact:Medium

- Area:

Brand Narrative

Recommendation:Create a dedicated 'Our Commitment' or 'Community Impact' page and link to it from the homepage, showcasing stories and data about how Citizens helps communities reach their potential.

Expected Impact:Medium

Quick Wins

- •

Make the '99% approval rate' statistic for Multi-Year Approval a more prominent visual element in the student loan section, rather than just in the disclaimer.

- •

Add a sub-headline to the 'Meet with a banker' section that clarifies the benefit, e.g., 'Get a complimentary financial plan for your future.'

- •

Add logos of publications or organizations that have recognized the bank, if available, as trust seals.

Long Term Recommendations

Develop a comprehensive content strategy that maps educational articles directly to product funnels, guiding users from learning about a topic (e.g., 'how to save for a house') directly to a relevant solution (e.g., mortgage options or high-yield savings).

Invest in video storytelling to bring the 'Made Ready' brand platform to life, showing real customer journeys and how the bank provided support at critical moments.

Citizens Bank's website messaging is highly effective at the product level, communicating clear, tangible value propositions for its core consumer offerings. The message architecture is logical, guiding users from a central brand idea to specific solutions for key life stages like paying for college and managing home equity. The brand voice is consistently helpful and empowering, successfully positioning the bank as an approachable partner.

The primary strength lies in its differentiated product features, such as 'Multi-Year Approval' for student loans, which serves as a powerful and unique selling proposition. However, the overarching brand message, 'You're made of keeping things in check. So are we,' while creative, is abstract and may not be as compelling as a more direct benefit statement. This represents the central tension in their strategy: a desire for an emotional, identity-based brand connection versus the need for clear, benefit-driven communication to drive acquisition in a competitive market.

The messaging successfully addresses the pain points of its target personas—students, homeowners, and savers—and positions the bank as a provider of simple, smart solutions. The educational content in the 'Learning' section is a significant asset, building trust and authority.

Key opportunities for optimization include strengthening the top-of-funnel brand message, incorporating more social proof like customer testimonials to build emotional resonance, and making the bank's community commitment more visible. By better connecting its strong product-level messaging to a more tangible and emotionally resonant brand narrative, Citizens can enhance its market position and drive stronger business outcomes.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Comprehensive product suite covering core consumer and business needs: checking, savings, credit cards, student loans, and home equity lines ofcredit.

- •

Established brand as one of the nation's oldest and largest financial institutions, indicating a large, stable customer base.

- •

Targeted offerings for specific life stages and needs, such as multi-year student loan approvals and financial literacy content for various demographics.

- •

Recent strategic focus on high-net-worth individuals with the launch of Citizens Private Bank, which has shown rapid growth.

Improvement Areas

- •

Enhance the user experience of digital products to match the seamlessness of fintech competitors and neobanks.

- •

Develop more deeply integrated financial wellness and automated savings tools within the mobile app, beyond the current 'Round Ups' feature.

- •

Increase personalization of product recommendations and financial advice using data and AI.

Market Dynamics

Moderate. The U.S. regional banking industry is mature, with growth expected to be in the low-to-mid single digits, driven by loan activity and potential M&A.

Mature

Market Trends

- Trend:

Accelerated Digital Adoption

Business Impact:Mobile is surpassing desktop as the primary banking channel. A superior digital experience is critical for customer acquisition and retention, as nearly 1 in 5 consumers are likely to switch institutions.

- Trend:

Intensifying Competition from Fintechs

Business Impact:Over 40% of Americans now use a non-traditional digital banking provider, increasing pressure on traditional banks to innovate on product offerings, user experience, and speed.

- Trend:

Data-Driven Personalization

Business Impact:Leveraging AI and data analytics to offer personalized advice, products, and experiences is becoming a key differentiator.

- Trend:

Rise of Open Banking and Embedded Finance

Business Impact:The ability to integrate with third-party apps and services is becoming a consumer expectation, creating opportunities for partnerships but also competitive threats.

Crucial. The market is at an inflection point. While the core business is stable, the accelerated shift to digital means that failure to innovate and adapt now will result in significant market share loss to more agile competitors.

Business Model Scalability

Medium

High fixed costs associated with a physical branch network, legacy technology infrastructure, and regulatory compliance. Digital offerings have lower variable costs and higher scalability.

Moderate. Citizens is pursuing operational leverage through digital transformation, AI adoption, and efficiency programs ('TOP' programs) to reduce its efficiency ratio from the mid-60s to the mid-50s long-term.

Scalability Constraints

- •

Dependency on physical branches for certain services and customer segments.

- •

Regulatory overhead and compliance costs that increase with scale.

- •

Legacy core banking systems that can slow down the development and launch of new digital products.

Team Readiness

Strong. The leadership team has a clear vision for digital transformation and is actively investing in technology and talent. The recent promotion of a tech-focused executive to President signals a commitment to this strategy.

Transitioning. The bank is moving towards a more agile, DevSecOps model but likely still retains traditional, siloed structures that can impede rapid, cross-functional execution.

Key Capability Gaps

- •

Data Science & AI Talent: Deep expertise is needed to build and deploy hyper-personalized customer experiences.

- •

Agile Product Management: Requires a shift in mindset from traditional project management to iterative, customer-centric product development.

- •

Digital Marketing & Growth Experts: Specialized skills in performance marketing and funnel optimization are needed to compete with digital-native firms.

Growth Engine

Acquisition Channels

- Channel:

Digital Marketing (SEO/Content)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Expand the financial 'Learning' hub with more interactive tools, video content, and personalized content journeys to capture top-of-funnel traffic and nurture leads.

- Channel:

Branch Network

Effectiveness:Medium

Optimization Potential:Medium

Recommendation:Transform branches from transactional centers to advisory hubs ('Citizens Checkup®') focusing on complex financial planning, while driving simple transactions to digital channels.

- Channel:

Paid Digital Advertising

Effectiveness:Medium

Optimization Potential:High

Recommendation:Implement highly targeted PPC and social media campaigns focused on specific products (e.g., 'FastLine®' HELOC) and demographics (e.g., students), with clear conversion tracking.

- Channel:

Strategic Partnerships

Effectiveness:High

Optimization Potential:High

Recommendation:Aggressively expand point-of-sale financing partnerships beyond existing ones (e.g., with Apple) into new high-growth retail and service ecosystems.

Customer Journey

The digital conversion path appears functional but standard. It relies on users navigating to specific product pages and completing traditional application forms.

Friction Points

- •

Potentially lengthy and complex online application processes for accounts and loans, a common issue for traditional banks.

- •

Lack of a fully seamless, mobile-first onboarding experience that can be completed in minutes.

- •

Siloed experiences between different products (e.g., opening a checking account vs. applying for a credit card).

Journey Enhancement Priorities

{'area': 'Digital Onboarding', 'recommendation': 'Develop a 5-minute, mobile-first, fully digital account opening process leveraging identity verification technology to minimize manual data entry and friction.'}

{'area': 'Product Discovery', 'recommendation': 'Implement a guided needs-assessment tool on the homepage that recommends a tailored bundle of products (e.g., checking, savings, card) based on user input.'}

Retention Mechanisms

- Mechanism:

Product Bundling & Relationship Banking

Effectiveness:High

Improvement Opportunity:Proactively offer relationship-based pricing and benefits through digital channels, rather than relying solely on in-person 'Checkups'.

- Mechanism:

Digital Engagement Tools (e.g., Round Ups)

Effectiveness:Medium

Improvement Opportunity:Expand beyond simple round-ups to offer a full suite of AI-driven financial wellness tools, including spending analysis, budgeting, and automated goal-based savings.

- Mechanism:

Credit Card Rewards Programs

Effectiveness:Medium

Improvement Opportunity:Introduce personalized and flexible reward options that can be redeemed for a wider variety of benefits, potentially including fractional investing or crypto.

Revenue Economics

Moderate. As a traditional bank, Citizens likely has a high Lifetime Value (LTV) per customer but also a high Customer Acquisition Cost (CAC), particularly for customers acquired through its branch network.

Likely healthy (Est. >5:1) due to the long-term nature of banking relationships, but could be improved by shifting acquisition to lower-cost digital channels.

Moderate. The focus on improving the efficiency ratio indicates a need to enhance revenue efficiency. Recent earnings have beaten expectations, showing positive momentum.

Optimization Recommendations

- •

Focus digital acquisition efforts on attracting customers who are likely to adopt multiple products, increasing LTV.

- •

Automate underwriting and onboarding for simple products to reduce the cost-to-serve.

- •

Utilize data analytics to identify and convert high-potential customers for wealth management and private banking services.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Banking Infrastructure

Impact:High

Solution Approach:Continue the stated 'next-generation technology' (NGT) strategy, focusing on a cloud-first, API-driven architecture. This enables faster product development and easier integration with fintech partners.

- Limitation:

Data Silos

Impact:Medium

Solution Approach:Accelerate the development of the enterprise data lake and 'Citizens Customer Master' to create a unified customer view, enabling true personalization and AI-powered insights.

Operational Bottlenecks

- Bottleneck:

Manual/Paper-Based Processes

Growth Impact:Slows down customer onboarding and loan processing, increasing operational costs and harming the customer experience.

Resolution Strategy:Aggressively digitize and automate back-office processes, from account opening to compliance checks, leveraging AI and machine learning.

- Bottleneck:

Branch-Centric Service Model

Growth Impact:Limits geographic scalability and does not meet the expectations of digitally-native customers.

Resolution Strategy:Implement a robust remote advisory model and enhance self-service capabilities in the mobile app, while repurposing branches for high-value consultations.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Critical

Mitigation Strategy:Differentiate through a superior, personalized digital experience and by focusing on specific growth segments like wealth management and strategic partnerships where Citizens can build a competitive moat.

- Challenge:

Customer Inertia

Severity:Major

Mitigation Strategy:Reduce switching friction with a seamless digital onboarding process and offer compelling, personalized incentives for new customers to switch their primary banking relationship.

Resource Limitations

Talent Gaps

- •

AI/ML Engineers

- •

Cloud Architects

- •

Digital Product Managers

- •

Growth Marketers

Low. As a large, profitable bank, capital is not a primary constraint. The key is prioritizing capital allocation towards technology and growth initiatives over legacy systems. The board has authorized a $1.5 billion stock buyback, indicating strong capital position.

Infrastructure Needs

- •

Modern cloud-native core banking platform.

- •

Enterprise-wide API gateway for internal and external innovation.

- •

Advanced data analytics and AI modeling platform.

Growth Opportunities

Market Expansion

- Expansion Vector:

Targeting Affluent/High-Net-Worth Customers

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Continue the aggressive build-out of the Citizens Private Bank, expanding wealth management teams into high-growth markets like California and Florida.

- Expansion Vector:

Digital-First National Expansion

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Develop a distinct digital-only banking brand or offering to attract customers outside the current physical branch footprint, competing directly with neobanks.

Product Opportunities

- Opportunity:

Integrated Financial Wellness Platform

Market Demand Evidence:Increasing consumer demand for tools that help manage finances, save automatically, and provide personalized advice.

Strategic Fit:Strong. Aligns with the 'Learning' content and positions the bank as a trusted advisor.

Development Recommendation:Partner with a leading financial wellness fintech to integrate their solution into the Citizens mobile app, accelerating time-to-market.

- Opportunity:

Banking as a Service (BaaS)

Market Demand Evidence:Growing number of non-financial companies looking to embed financial products (payments, lending) into their customer experience.

Strategic Fit:Medium. Requires significant technology and business model evolution.

Development Recommendation:Launch a pilot program offering specific API-based services (e.g., account verification, payment processing) to a select group of corporate clients or tech startups.

Channel Diversification

- Channel:

Fintech App Marketplaces

Fit Assessment:High. Leverages open banking trends.

Implementation Strategy:Develop APIs that allow fintech apps (e.g., budgeting, investing) to securely connect to Citizens accounts, positioning the bank as a central financial hub for customers.

- Channel:

Embedded Finance in E-commerce

Fit Assessment:High. Extends the successful point-of-sale financing model.

Implementation Strategy:Create partnerships with major e-commerce platforms and software providers to offer embedded lending and payment solutions at the point of need.

Strategic Partnerships

- Partnership Type:

Technology/Capability Partnership

Potential Partners

- •

Plaid

- •

Finicity

- •

Leading AI/ML Platform providers (e.g., Databricks, Snowflake)

Expected Benefits:Accelerate development of open banking capabilities, enhance data analytics, and improve digital onboarding processes.

- Partnership Type:

Product/Service Partnership

Potential Partners

Robo-advisors (e.g., Betterment, Wealthfront)

Specialty lending fintechs

Expected Benefits:Quickly expand the digital product shelf to serve new customer segments (e.g., mass-affluent investors) without building capabilities from scratch.

Growth Strategy

North Star Metric

Digitally Engaged Primary Customers

This metric shifts focus from simply opening accounts to building valuable, long-term relationships through digital channels. It measures both adoption (primary bank status) and engagement (digital activity), which are leading indicators of LTV and retention.

Increase the percentage of new customers who become digitally active within 30 days by 25% year-over-year.

Growth Model

Hybrid: Content-led Acquisition + Product-led Engagement + Sales-led High-Value Services

Key Drivers

- •

Valuable financial literacy content attracting organic traffic.

- •

A seamless, low-friction digital onboarding experience.

- •

In-app features that encourage habitual use and cross-product adoption.

- •

Skilled bankers and advisors for complex needs (wealth, business).

Create distinct funnels for different customer segments, using content and digital ads for initial attraction, a world-class app for self-service and engagement, and clear pathways to connect with human experts when needed.

Prioritized Initiatives

- Initiative:

Launch 'Digital Express Onboarding'

Expected Impact:High

Implementation Effort:High

Timeframe:9-12 months

First Steps:Assemble a cross-functional team (product, engineering, legal, marketing). Select a technology partner for identity verification. Map the end-to-end customer journey and define MVP features.

- Initiative:

Develop 'Citizens Financial Wellness Hub' in-app

Expected Impact:High

Implementation Effort:Medium

Timeframe:6-9 months

First Steps:Evaluate build vs. partner options for core features (spending analysis, goal setting). Conduct customer research to identify the most desired wellness tools. Launch an MVP to a segment of mobile app users.

- Initiative:

Expand Point-of-Sale (POS) Lending Partnerships

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:Ongoing

First Steps:Identify and target key growth verticals (e.g., home improvement, elective medical). Develop a scalable partnership onboarding process. Dedicate a business development team to this channel.

Experimentation Plan

High Leverage Tests

{'test_name': 'Homepage Value Proposition A/B Test', 'hypothesis': "Testing different headline messages (e.g., 'Simpler, Faster Banking' vs. 'Your Partner for Financial Goals') will impact click-through rates to product pages."}

{'test_name': 'Onboarding Friction Test', 'hypothesis': 'Reducing the number of fields in the initial application form will increase completion rates.'}

Utilize an A/B testing platform (e.g., Optimizely, Google Optimize) integrated with core analytics to track conversion rates, drop-off points, and engagement metrics for each experiment.

Run at least two concurrent high-impact experiments per month, with a weekly review of results and a monthly planning session to prioritize the next batch of tests.

Growth Team

Cross-functional, mission-oriented teams. Establish a dedicated 'Digital Growth' team with representatives from Product, Marketing, Engineering, and Data, focused exclusively on the North Star Metric. This team should operate with a high degree of autonomy.

Key Roles

- •

Head of Digital Growth

- •

Product Manager (Onboarding & Engagement)

- •

Performance Marketing Specialist

- •

Data Analyst

Invest in continuous training on agile methodologies, growth marketing frameworks, and data analytics tools. Empower the team to make decisions based on experiment results.

Citizens Bank is a well-established regional bank with a strong foundation and a clear recognition of the need for digital transformation. Its product-market fit is solid within the traditional banking landscape, and leadership has initiated key strategic programs, such as the 'One Citizens' initiative, the build-out of a private bank, and a next-generation technology strategy, to adapt to the changing market. The bank's recent financial performance has been strong, exceeding expectations and demonstrating resilience.

The primary challenge and greatest opportunity for Citizens lies in the velocity of its transformation. The US consumer banking market is being fundamentally reshaped by digital-native fintechs and evolving customer expectations for seamless, personalized, and mobile-first experiences. While Citizens has the right strategic priorities—enhancing data analytics, focusing on digital channels, and improving efficiency—its success will depend on its ability to execute with the speed and agility of a technology company, not a traditional bank.