eScore

discover.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

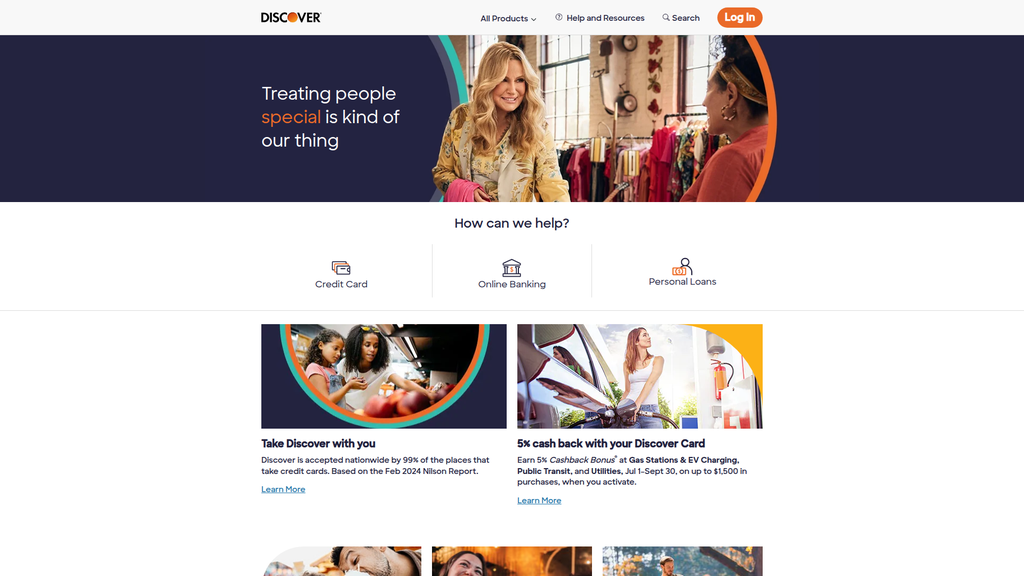

Discover.com demonstrates a strong and mature digital presence, particularly in its primary U.S. market. The site's content is well-aligned with the search intent of its target personas, such as credit builders and value maximizers, and its 'Card Smarts' blog serves as an effective top-of-funnel asset. The brand maintains a consistent multi-channel presence and possesses high domain authority, although it lacks the proprietary, data-driven thought leadership of larger competitors. Its global reach is a known limitation, with digital efforts correctly focused on deep domestic penetration.

Excellent search intent alignment for core customer segments like 'new to credit' and 'cashback rewards,' effectively capturing high-value traffic.

Launch a proprietary data insights program, similar to competitor economic reports, to generate high-quality backlinks and establish true thought leadership beyond foundational financial tips.

Brand communication is a significant strength, anchored by the clear, consistent, and approachable message of 'Treating people special is kind of our thing.' Messaging is effectively tailored to different audience segments, addressing specific pain points like credit score anxiety ('no impact to your credit to check') and fee aversion. The brand successfully differentiates itself on customer service and simplicity rather than prestige, creating a strong emotional connection with its target market.

The brand voice is exceptionally consistent and approachable, effectively differentiating Discover in a typically impersonal financial services market.

Incorporate more social proof, such as customer testimonials and success stories, on the homepage to substantiate brand claims and build immediate trust.

The website offers a highly optimized conversion experience with a low cognitive load, clear visual hierarchy, and intuitive navigation. Friction points are minimized through low-commitment CTAs like pre-approval checks, and the mobile experience is flawlessly executed. A public commitment to accessibility demonstrates an inclusive design philosophy, which positively impacts market reach and reduces legal risk.

The use of prominent, high-contrast, and action-oriented CTAs (e.g., 'Calculate Savings') is a best-in-class example of guiding user behavior towards key conversion actions.

A/B test the main hero headline to be more benefit-oriented (e.g., 'Cash Back Rewards Made Easy') instead of purely brand-focused to improve clarity for new visitors.

Discover excels in establishing credibility and mitigating perceived risks for its customers. The website features a robust hierarchy of trust signals, including a best-in-class Privacy Center and clear, compliant language that aligns with TILA and FCRA regulations. Third-party validation is consistently high, with numerous J.D. Power awards for customer satisfaction. Transparency is evident in its fee structures and product terms, fostering a high degree of trust.

A mature and sophisticated legal and compliance framework, especially in data privacy (GLBA, CCPA) and cookie consent, is used as a strategic asset to build customer trust.

While customer success is proven by awards, the website lacks qualitative evidence like case studies or detailed testimonials demonstrating how products have helped customers achieve financial goals.

Discover's competitive moat is built on two highly sustainable advantages: its award-winning, U.S.-based customer service culture and its vertically integrated closed-loop payment network. These are difficult for competitors to replicate and provide durable pricing and data advantages. While it cedes the premium market to Amex and lags in global acceptance, its brand identity of fairness and value creates high switching costs in the form of customer loyalty within its target market.

The combination of a top-ranked customer service reputation and a closed-loop network provides a defensible moat against both large bank issuers and nimble fintechs.

Develop a strategy to address the 'premium segment' gap, potentially through a new card tier, to avoid losing customers as their financial needs and spending power mature.

As a mature, digital-first bank, Discover's business model is highly scalable, with strong unit economics and operational leverage. The company shows clear signals for market expansion by targeting underserved segments like Gen Z and has a robust foundation for growth. The recent acquisition by Capital One dramatically increases its potential scale, although it also introduces significant integration challenges and risks.

The digital-first business model has high operational leverage, allowing for efficient customer acquisition and servicing at scale with low marginal costs.

Expand into the small business/freelancer segment, a significant whitespace opportunity where competitors' offerings are often overly complex for the target user.

Discover's business model is exceptionally coherent, with a clear value proposition that directly aligns with its revenue model and target market. Revenue streams from net interest income and transaction fees are well-established and support the rewards-centric product offerings. The company demonstrates strong strategic focus by exiting non-core businesses (home, student loans) to double down on its strengths in consumer credit and digital banking.

A clear and consistent strategic focus on the American middle-market consumer with a value proposition of rewards, service, and simplicity, which is reflected across all business activities.

Innovate the revenue model by integrating a native Buy Now, Pay Later (BNPL) feature to defend against fintech disruptors and meet evolving consumer payment preferences.

Discover is a significant but not dominant player, holding a stable market share behind the Visa/Mastercard duopoly and Amex. Its market power comes from its closed-loop network and strong brand loyalty, which grants it some pricing power in the form of lower interchange fees and customer retention. While it doesn't set broad market trends, it has significant influence within its value-focused segment and a strong negotiating position due to its network ownership, a position now massively amplified by the Capital One merger.

Ownership of its payment network gives it significant leverage and control over transaction data and economics, a key advantage over other major issuers like Chase and Capital One.

Address the persistent disadvantage of lower international merchant acceptance, which remains a key reason for customer attrition among frequent travelers.

Business Overview

Business Classification

Direct Banking & Payment Services

Financial Technology (FinTech)

Financial Services

Sub Verticals

- •

Credit Card Issuing

- •

Digital Banking

- •

Consumer Lending

- •

Payment Networks

Mature

Maturity Indicators

- •

Strong brand recognition and established market presence.

- •

Consistent profitability and robust financial performance.

- •

Diversified, well-defined product portfolio (credit cards, online banking, personal loans).

- •

Recent strategic acquisition by a major competitor (Capital One), indicating significant established value.

- •

Exiting non-core business lines like student and home loans to focus on core strengths.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Interest Income

Description:The primary source of revenue, generated from the interest charged on outstanding balances for credit cards and personal loans, minus the interest paid out on deposit accounts (savings, checking, CDs). This is the core of the lending business model.

Estimated Importance:Primary

Customer Segment:Credit Card Holders & Personal Loan Borrowers

Estimated Margin:High

- Stream Name:

Non-Interest Income

Description:Revenue generated from fees. This includes discount and interchange fees paid by merchants for transactions processed on the Discover Network, late payment fees, cash advance fees, and other service charges.

Estimated Importance:Secondary

Customer Segment:Merchants & Cardholders

Estimated Margin:Medium

- Stream Name:

Payment Network Fees

Description:Fees generated from the operation of the Discover Global Network, including PULSE (an ATM/debit network) and Diners Club International, providing transaction processing and settlement services for other financial institutions.

Estimated Importance:Tertiary

Customer Segment:Financial Institutions & Network Partners

Estimated Margin:Medium

Recurring Revenue Components

- •

Interest income from revolving credit card balances

- •

Interest income from fixed-term personal loans

- •

Merchant discount fees on recurring transactions

Pricing Strategy

Interest & Fee-Based

Mid-range

Semi-transparent

Pricing Psychology

- •

Zero-Fee Propositions (e.g., '$0 Annual Fee' on many cards, 'No monthly fees' for checking).

- •

Reward Incentives (e.g., '5% Cashback Bonus', 'Cashback Match').

- •

Introductory Offers (e.g., 0% intro APR on purchases and balance transfers)

Monetization Assessment

Strengths

- •

Diversified revenue from both lending (interest) and payments (fees).

- •

Closed-loop network model (issuer and network) allows for capturing a larger portion of transaction value.

- •

Strong customer loyalty driven by a successful cashback rewards program.

Weaknesses

- •

High exposure to credit risk and economic downturns, which can impact interest income.

- •

Revenue is sensitive to regulatory changes, especially regarding interest rates and late fees.

- •

Lower interchange fees charged to merchants compared to some competitors, potentially limiting fee income per transaction.

Opportunities

- •

Leverage the Capital One merger to expand the merchant network and cross-sell products.

- •

Grow the digital banking segment to increase low-cost deposits, reducing the cost of funds for lending.

- •

Introduce premium card offerings with annual fees to target higher-income segments and create a new revenue stream.

Threats

- •

Intense competition from other major issuers (Chase, Amex, Citi) and networks (Visa, Mastercard).

- •

Disruption from FinTechs in the Buy Now, Pay Later (BNPL) and digital payments space.

- •

Potential for increased regulatory scrutiny on credit card fees and interest rates.

Market Positioning

Customer-centric value and rewards-focused digital bank.

Significant player, often cited as the third or fourth largest credit card network in the U.S. by volume.

Target Segments

- Segment Name:

Credit Builders & Students

Description:Younger consumers, often students or recent graduates, who have limited or no credit history and are seeking their first credit card. They are attracted to accessible products like the Discover it Secured Card and student cards.

Demographic Factors

- •

Age 18-25

- •

Students or early in career

- •

Lower-to-moderate income

Psychographic Factors

- •

Value financial education

- •

Seek simple, easy-to-understand products

- •

Appreciate a pathway to unsecured credit

Behavioral Factors

- •

First-time credit card user

- •

Highly digitally engaged (mobile banking)

- •

Sensitive to fees and complex terms

Pain Points

- •

Difficulty getting approved for traditional credit cards

- •

Lack of understanding of how credit works

- •

Fear of high fees and debt

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Reward Maximizers

Description:Prime and super-prime credit consumers who are savvy about rewards and actively use credit cards to earn cash back on everyday spending. They are attracted to the 5% rotating categories and the first-year Cashback Match program.

Demographic Factors

- •

Age 25-55

- •

Middle-to-upper income

- •

Good to excellent credit score (670+)

Psychographic Factors

- •

Value-conscious and budget-oriented

- •

Enjoy 'gamifying' their spending to maximize returns

- •

Loyal to brands that provide tangible benefits

Behavioral Factors

- •

Regularly use credit cards for most purchases

- •

Actively manage and redeem rewards points

- •

Likely to have multiple credit cards

Pain Points

- •

Complex or low-value rewards programs from other issuers

- •

Poor customer service when issues arise

- •

Annual fees that diminish the value of rewards

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Debt Consolidators

Description:Individuals with existing high-interest debt (e.g., from other credit cards) who are looking for ways to manage and pay it down more effectively. They are targeted by Discover's balance transfer offers and personal loans.

Demographic Factors

- •

Age 30-60

- •

Moderate-to-high income

- •

Fair to excellent credit score

Psychographic Factors

- •

Seeking financial control and stability

- •

Stressed by managing multiple payments

- •

Goal-oriented towards becoming debt-free

Behavioral Factors

- •

Carry a revolving balance on other credit cards

- •

Actively search for financial solutions online

- •

Responsive to low-introductory APR offers

Pain Points

- •

High-interest rates eroding their payments

- •

Complexity of managing multiple debt accounts

- •

Lack of a clear plan to pay off debt

Fit Assessment:Good

Segment Potential:Medium

Market Differentiation

- Factor:

100% U.S.-Based Customer Service

Strength:Strong

Sustainability:Sustainable

- Factor:

Cashback Rewards Program (incl. 5% rotating categories and Cashback Match)

Strength:Strong

Sustainability:Sustainable

- Factor:

No Annual Fee on Most Products

Strength:Moderate

Sustainability:Sustainable

- Factor:

Closed-Loop Payment Network (Issuer & Network)

Strength:Strong

Sustainability:Sustainable

Value Proposition

Discover helps people spend smarter, manage debt better, and save more by providing accessible digital banking and credit products with great rewards and exceptional, U.S.-based customer service.

Excellent

Key Benefits

- Benefit:

Earn valuable cash back rewards on purchases.

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

5% Cashback Bonus in rotating categories

- •

Unlimited 1% cash back on all other purchases

- •

First-year Cashback Match program

- Benefit:

Avoid common bank and credit card fees.

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

No annual fee on any Discover card.

- •

No monthly fees on checking or savings accounts

- •

No fee for the first late payment.

- Benefit:

Receive high-quality, U.S.-based customer support.

Importance:Important

Differentiation:Unique

Proof Elements

Consistently high rankings in J.D. Power Customer Satisfaction surveys.

Prominently featured marketing claim.

- Benefit:

Free access to FICO® credit score and identity theft alerts.

Importance:Important

Differentiation:Common

Proof Elements

Free FICO score on monthly statements and online.

Social Security number alerts

Unique Selling Points

- Usp:

Cashback Match: Automatically matching all cash back earned at the end of the cardmember's first year.

Sustainability:Medium-term

Defensibility:Moderate

- Usp:

Guaranteed 100% U.S.-based customer service, providing a consistently positive support experience.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

Traditional credit cards and bank accounts have complex fee structures and penalties.

Severity:Major

Solution Effectiveness:Complete

- Problem:

Difficulty in getting help from knowledgeable customer service agents.

Severity:Major

Solution Effectiveness:Complete

- Problem:

New-to-credit consumers are often unable to access mainstream credit products.

Severity:Critical

Solution Effectiveness:Partial

- Problem:

Rewards programs are often complicated with limited redemption value.

Severity:Minor

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition strongly aligns with a large segment of the consumer market that is value-conscious, fee-averse, and desires straightforward rewards and excellent service.

High

The proposition is exceptionally well-aligned with the needs of credit builders and reward maximizers, offering clear benefits that directly address their primary pain points.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Merchants (retail, online, etc.)

- •

Strategic payment networks (e.g., UnionPay in China, Elo in Brazil) for global acceptance.

- •

Credit bureaus (TransUnion, Equifax, Experian)

- •

Technology providers (for mobile banking, security, etc.)

- •

Co-brand partners (historically)

Key Activities

- •

Credit risk management and underwriting

- •

Payment transaction processing and network operations

- •

Customer service and support

- •

Marketing and customer acquisition

- •

Digital product development and innovation

Key Resources

- •

Discover Global Payment Network (including PULSE and Diners Club).

- •

Strong brand reputation for customer satisfaction and value.

- •

Large, loyal cardmember base.

- •

Proprietary customer data and analytics capabilities

- •

Banking charter (Discover Bank)

Cost Structure

- •

Provision for credit losses

- •

Marketing and business development expenses.

- •

Employee compensation and benefits

- •

Rewards program expenses

- •

Information technology and communication costs

Swot Analysis

Strengths

- •

Integrated 'closed-loop' model as both card issuer and payment network operator.

- •

Award-winning customer service and high customer loyalty.

- •

Strong brand recognition and a clear value proposition centered on rewards and no annual fees.

- •

Diversified product portfolio spanning credit, debit, and consumer loans.

Weaknesses

- •

Lower merchant acceptance internationally compared to Visa and Mastercard.

- •

Perception by some as a less prestigious brand compared to American Express.

- •

Smaller cardholder base than the largest competitors like JPMorgan Chase and Citi.

Opportunities

- •

Leverage the completed acquisition by Capital One to create the largest US credit card issuer by balances, significantly increasing scale and cross-sell opportunities.

- •

Expand the Discover Network's acceptance and volume by migrating Capital One cards over time.

- •

Grow digital banking services (checking, savings) to attract more low-cost deposits and deepen customer relationships.

- •

Innovate in growing payment areas like digital wallets, contactless payments, and BNPL.

Threats

- •

Post-merger integration challenges with Capital One, including potential customer attrition and operational disruption.

- •

Intense and increasing competition from established banks, credit unions, and fintech startups.

- •

Increased regulatory oversight and potential for new rules limiting fees (e.g., late fees, interchange rates).

- •

Persistent cybersecurity threats targeting financial institutions.

Recommendations

Priority Improvements

- Area:

Post-Merger Strategy

Recommendation:Develop and clearly communicate a unified brand and product strategy with Capital One to retain customer loyalty and minimize confusion. Prioritize seamless integration of technology platforms and customer service channels.

Expected Impact:High

- Area:

Digital Banking Expansion

Recommendation:Enhance the feature set of Discover's online checking and savings accounts to better compete with leading neobanks, focusing on budgeting tools, automated savings, and higher APYs to attract sticky, low-cost deposits.

Expected Impact:Medium

- Area:

International Network Growth

Recommendation:Post-merger, leverage Capital One's existing relationships with Visa and Mastercard to strategically negotiate expanded acceptance for the Discover Network, particularly in travel and e-commerce corridors.

Expected Impact:High

Business Model Innovation

- •

Develop a 'Banking-as-a-Service' (BaaS) platform, leveraging the Discover Network and banking charter to enable fintechs to build and offer their own branded financial products.

- •

Create a subscription-based premium product tier that bundles benefits across credit cards, banking, and personal loans, such as higher rewards rates, dedicated financial advisors, and subscription service credits.

- •

Integrate BNPL (Buy Now, Pay Later) functionality directly into the Discover card at the point-of-sale, offering cardholders flexible payment options on larger purchases for a fixed fee.

Revenue Diversification

- •

Launch a small business credit card and banking division to tap into a new customer segment.

- •

Expand data and analytics services, offering anonymized transaction insights to merchant partners for a fee.

- •

Introduce wealth management or automated investing (robo-advisor) services to the existing digital banking platform to capture a greater share of the customer's financial life.

Discover Financial Services has successfully carved out a significant and defensible position in the highly competitive U.S. financial services market. Its business model is built on a robust, integrated foundation, functioning as both a direct digital bank and the operator of its own payment network. This closed-loop system is a core strategic asset, providing greater control over the customer experience and transaction economics, similar to American Express.

The company's value proposition is exceptionally clear and resonates strongly with its target segments of credit-builders and value-conscious consumers. By focusing on tangible benefits like cash back rewards, the absence of punitive fees (especially annual fees), and consistently excellent U.S.-based customer service, Discover has cultivated a loyal customer base. This strategy has allowed it to mature into a stable, profitable enterprise with steady growth.

However, the business faces significant strategic inflection points. The landscape is under threat from fintech disruptors and intense competition from larger, more diversified banking institutions. While historically challenged by a perception of lower prestige and limited international acceptance, Discover has effectively mitigated the domestic acceptance issue and built a powerful brand around trust and value.

The most transformative event is the recent completion of its acquisition by Capital One. This merger fundamentally reshapes the strategic outlook, presenting both immense opportunities and significant threats. The combination creates the largest U.S. credit card lender, providing unprecedented scale. The key opportunity lies in migrating Capital One's massive card portfolio to the Discover network, which would dramatically increase the network's volume and create a formidable competitor to Visa and Mastercard. However, the execution of this integration is fraught with risk, including potential brand dilution, cultural clashes, and technological hurdles. Future success will be entirely dependent on the effective strategic management of this post-merger integration, focusing on leveraging the combined scale while preserving the core tenets of customer service and value that made Discover successful in the first place.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

Regulatory Compliance & Licensing

Impact:High

- Barrier:

Payment Network Infrastructure

Impact:High

- Barrier:

Brand Trust & Customer Acquisition Cost

Impact:High

- Barrier:

Capital Requirements

Impact:High

- Barrier:

Economies of Scale

Impact:Medium

Industry Trends

- Trend:

Rise of Buy Now, Pay Later (BNPL) Services

Impact On Business:BNPL services are attracting younger demographics who are wary of traditional credit card debt, directly competing for point-of-sale transactions. This could erode credit card transaction volume.

Timeline:Immediate

- Trend:

Digital Wallet Integration (Apple Pay, Google Pay)

Impact On Business:Big tech firms control the user interface for payments, potentially disintermediating card issuers and commoditizing the underlying card.

Timeline:Immediate

- Trend:

Demand for Personalized Rewards & Hyper-Customization

Impact On Business:Customers increasingly expect tailored rewards and offers based on their spending habits, requiring significant investment in data analytics.

Timeline:Near-term

- Trend:

Fintech & Neobank Competition

Impact On Business:Digital-first banks are competing for the primary banking relationship, including loans and checking accounts, with lower overhead and often superior user experiences.

Timeline:Near-term

- Trend:

Increased Regulatory Scrutiny

Impact On Business:Heightened focus on fees (e.g., late fees), data privacy, and lending practices can impact revenue streams and increase compliance costs.

Timeline:Immediate

Direct Competitors

- →

American Express

Market Share Estimate:Third largest US card network by purchase volume.

Target Audience Overlap:Medium

Competitive Positioning:Premium/luxury brand focusing on high-spend consumers and business clients, emphasizing travel rewards, exclusive benefits, and superior service.

Strengths

- •

Strong brand prestige and reputation.

- •

Affluent and loyal customer base with high spending.

- •

Powerful Membership Rewards program.

- •

Vertically integrated 'closed-loop' network provides rich data insights.

- •

Consistently ranks highest in overall customer satisfaction.

Weaknesses

- •

Lower merchant acceptance globally compared to Visa/Mastercard.

- •

High annual fees on premium cards can be a barrier for some consumers.

- •

Perception of being exclusive can limit appeal to the mass market.

Differentiators

- •

Focus on charge cards over traditional credit cards.

- •

Exclusive access to events, airport lounges, and concierge services.

- •

High-end co-branded partnerships (e.g., Delta, Hilton).

- →

JPMorgan Chase (Chase)

Market Share Estimate:Largest US credit card issuer by purchase volume and outstanding balances.

Target Audience Overlap:High

Competitive Positioning:Mass-market leader leveraging its vast retail banking footprint to offer a wide range of cards with a powerful and flexible rewards ecosystem (Ultimate Rewards).

Strengths

- •

Massive existing customer base from its retail banking operations.

- •

Highly popular and valuable Ultimate Rewards program.

- •

Dominant co-branded card portfolio (e.g., Southwest, Marriott, Amazon).

- •

Significant marketing budget and brand recognition.

Weaknesses

- •

Customer service is not a primary brand differentiator compared to Discover or Amex.

- •

Less focused on the 'no annual fee' segment than Discover.

- •

Can be slower to innovate compared to more nimble fintech-focused competitors.

Differentiators

- •

The 'Chase Trifecta' strategy encourages customers to hold multiple Chase cards to maximize rewards.

- •

Seamless integration with Chase's retail banking and investment services.

- •

Broad appeal from entry-level to premium travel cards.

- →

Capital One

Market Share Estimate:A top-5 US credit card issuer, known for its significant market presence.

Target Audience Overlap:High

Competitive Positioning:A technology and data-driven bank that positions itself as modern and straightforward, appealing to a broad spectrum of consumers with a focus on analytics-based marketing.

Strengths

- •

Pioneer in using data analytics for customer targeting and risk management.

- •

Strong brand recognition built on heavy marketing and simple messaging.

- •

Diversified portfolio including auto loans and consumer banking.

- •

Early adopter of digital and mobile banking technologies.

Weaknesses

- •

Primarily an issuer on Visa/Mastercard networks, lacking its own payment network.

- •

Highly reliant on the competitive US consumer credit market.

- •

The pending merger with Discover could face significant regulatory hurdles and integration challenges.

Differentiators

- •

Emphasis on technology and user experience (e.g., Eno assistant).

- •

Acquisition-led growth strategy, including the proposed Discover merger.

- •

Strong presence across the credit spectrum, from subprime to super-prime.

Indirect Competitors

- →

BNPL Providers (Affirm, Klarna, Afterpay)

Description:Offer interest-free installment loans at the point of sale, allowing consumers to split purchases into smaller payments without a traditional credit card.

Threat Level:High

Potential For Direct Competition:Increasingly offering card-like products and apps that consolidate purchases, moving closer to direct competition. Many BNPL users state these services could replace their credit cards.

- →

Fintech/Neobanks (Chime, SoFi)

Description:Digital-first banking platforms that offer checking, savings, and lending products with low or no fees, competing for the primary financial relationship with customers. SoFi directly competes in personal loans.

Threat Level:Medium

Potential For Direct Competition:High. Many are expanding into credit products and are viewed more favorably by younger demographics, posing a long-term threat to incumbent card issuers.

- →

Big Tech (Apple Card / Apple Pay)

Description:Leverage massive user ecosystems to offer deeply integrated financial products. The Apple Card, issued by Goldman Sachs, offers a seamless digital experience within the iOS ecosystem.

Threat Level:High

Potential For Direct Competition:Already a direct competitor in the card space. The primary threat is the control over the digital wallet, which could reduce other cards to a secondary role.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Superior Customer Service Reputation

Sustainability Assessment:Highly sustainable. Consistently ranks at or near the top in J.D. Power satisfaction studies, which is deeply embedded in its brand identity and operational culture (e.g., 100% U.S.-based service).

Competitor Replication Difficulty:Hard

- Advantage:

Vertically Integrated 'Closed-Loop' Network

Sustainability Assessment:Highly sustainable. As both an issuer and a network (like Amex), Discover gains valuable transaction data, has greater control over fees, and can innovate on its platform directly.

Competitor Replication Difficulty:Hard

- Advantage:

Brand Identity of Fairness and Value (No Annual Fee)

Sustainability Assessment:Sustainable. The 'no annual fee' and transparent fee structure is a core tenet of the Discover brand since its inception, resonating strongly with its middle-market target audience.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': '5% Rotating Cashback Categories', 'estimated_duration': 'Quarterly. While the specific categories provide a short-term advantage, the model itself is replicable and has been adopted by competitors like Chase (Chase Freedom Flex).'}

{'advantage': 'Introductory 0% APR Offers', 'estimated_duration': 'Per campaign. These are standard market tools used by all major competitors to attract new customers for balance transfers and new purchases.'}

Disadvantages

- Disadvantage:

Lower International Merchant Acceptance

Impact:Major

Addressability:Difficult. Despite forming partnerships with regional networks, Discover still lags significantly behind Visa and Mastercard in global acceptance, making it a less reliable choice for frequent international travelers.

- Disadvantage:

Weaker Brand Perception in the Premium Segment

Impact:Major

Addressability:Difficult. The brand is strongly associated with value and the mass market, making it difficult to compete with Amex and Chase Sapphire for high-income customers who prioritize premium travel perks over no annual fee.

- Disadvantage:

Smaller Scale Compared to Visa/Mastercard

Impact:Minor

Addressability:Difficult. As the fourth-largest U.S. network, it has less volume and ubiquity than the two dominant players, which can impact co-branding opportunities and network effects.

Strategic Recommendations

Quick Wins

- Recommendation:

Launch Aggressive Marketing Campaigns Highlighting 'No Foreign Transaction Fees'.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Feature Customer Service Excellence in Top-of-Funnel Advertising.

Expected Impact:High

Implementation Difficulty:Easy

- Recommendation:

Promote Pre-Approval Tool to Mitigate Credit Score Anxiety.

Expected Impact:Medium

Implementation Difficulty:Easy

Medium Term Strategies

- Recommendation:

Develop a 'Discover Premium' Card with a Modest Annual Fee.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Expand Strategic Alliances with International Payment Networks.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Integrate with Popular Budgeting and Personal Finance Management (PFM) Apps.

Expected Impact:Medium

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Invest in or Acquire a BNPL Provider to Integrate the Service Natively.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Build out a Small Business Product Suite.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Leverage Closed-Loop Data to Create a Predictive Personal Finance Platform.

Expected Impact:High

Implementation Difficulty:Difficult

Double down on the position as the most customer-centric and transparent financial partner for the American middle class. Frame the brand as the 'smarter' choice, contrasting its simplicity and award-winning service against the complexity and high fees of premium competitors and the risks of unregulated fintech disruptors.

Focus on 'Human-Centered Finance'. This involves leading with the award-winning, US-based customer service as the primary differentiator. Further differentiate by creating products and tools specifically for life moments like building credit, managing student debt, and consolidating loans, reinforcing the mission to 'help people achieve a brighter financial future'.

Whitespace Opportunities

- Opportunity:

Targeted Financial Products for the Gig Economy/Freelancers

Competitive Gap:Most competitors offer generic small business cards that don't address the unique needs of freelancers, such as fluctuating income and expense tracking for tax purposes.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Subscription Management & Optimization Service

Competitive Gap:While some competitors offer basic subscription identification, a proactive tool that helps customers identify redundant services or find better deals would be a strong value-add.

Feasibility:Medium

Potential Impact:Medium

- Opportunity:

Enhanced 'New to Credit' Ecosystem

Competitive Gap:Beyond a secured card, create a comprehensive program with educational content, credit simulation tools, and a clear graduation path to unsecured products, fostering long-term loyalty from young consumers.

Feasibility:High

Potential Impact:High

- Opportunity:

Family-Oriented Financial Tools

Competitive Gap:There is a lack of integrated tools for family financial management, such as linked cards for teens with smart controls and shared savings goals within the Discover banking ecosystem.

Feasibility:Medium

Potential Impact:Medium

Discover Financial Services operates in the mature, oligopolistic U.S. financial services market. Its primary strength and most sustainable competitive advantage is a deeply ingrained culture of customer service, consistently validated by third-party awards. This, combined with its brand positioning around value, fairness, and transparency (e.g., no annual fees on core products), has allowed it to carve out a loyal customer base primarily within the American middle market. As a closed-loop network, similar to American Express, Discover possesses a significant structural advantage over issuers like Chase and Capital One, enabling greater control over data, fees, and product innovation.

The competitive landscape is defined by several key pressures. Direct competitors like American Express dominate the premium segment with a powerful brand and rewards, while mass-market leader Chase leverages its enormous banking footprint to create a sticky rewards ecosystem. Capital One competes fiercely on technology and data analytics. However, the more pressing threats are asymmetrical. The rise of Buy Now, Pay Later (BNPL) services directly attacks the core use case of credit cards for point-of-sale financing, especially with younger consumers. Simultaneously, Big Tech players like Apple are disintermediating the payment process through digital wallets, threatening to commoditize the underlying card issuers.

Discover's most significant disadvantage remains its limited international acceptance compared to Visa and Mastercard, which restricts its appeal to frequent travelers. Strategically, Discover's proposed merger with Capital One aims to address scale issues, but also presents significant integration risk. Key opportunities lie in leveraging its trusted brand to expand into underserved niches like the gig economy, enhancing its digital tools beyond basic banking, and deepening its relationship with customers new to credit. To win, Discover must double down on its identity as the most transparent, human-centric financial partner, using its superior service as a shield against both premium rivals and nascent fintech disruptors.

Messaging

Message Architecture

Key Messages

- Message:

Treating people special is kind of our thing.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Banner

- Message:

Earn 5% Cashback Bonus® at Gas Stations & EV Charging, Public Transit, and Utilities...

Prominence:Secondary

Clarity Score:High

Location:Homepage Tile

- Message:

Discover is accepted nationwide by 99% of the places that take credit cards.

Prominence:Secondary

Clarity Score:High

Location:Homepage Tile

- Message:

Free benefits that just make sense.

Prominence:Tertiary

Clarity Score:Medium

Location:Homepage Tile

- Message:

Making Your Finances Work Harder For You.

Prominence:Tertiary

Clarity Score:High

Location:Homepage Content Section

The messaging hierarchy is effective. It leads with a broad, emotionally resonant brand promise ('Treating people special') to establish a positive frame. It then immediately follows with tangible product benefits (cash back, acceptance) to substantiate the brand promise. Educational and product-specific content is placed further down, correctly assuming a user will seek details after being captured by the primary value propositions.

Messaging is highly consistent. The core themes of customer-centricity, value (rewards, low fees), and simplicity are woven throughout the homepage and the accessibility page. The friendly, approachable tone established in the hero banner is maintained across product descriptions and even in functional sections, creating a cohesive brand experience.

Brand Voice

Voice Attributes

- Attribute:

Approachable

Strength:Strong

Examples

- •

Treating people special is kind of our thing

- •

How can we help?

- •

Free benefits that just make sense

- Attribute:

Helpful

Strength:Strong

Examples

- •

Making Your Finances Work Harder For You

- •

We can help you get serious about saving

- •

Tips for how to recover from being scammed

- Attribute:

Simple

Strength:Moderate

Examples

- •

Fast and easy checkout

- •

Easy credit card preapproval check

- •

From clearly labeling pages, sections, and fields with straightforward language...

- Attribute:

Reassuring

Strength:Moderate

Examples

Discover is accepted nationwide by 99% of the places that take credit cards.

Find out if you're preapproved for a Discover® card with no impact to your credit to check.

Tone Analysis

Welcoming & Supportive

Secondary Tones

- •

Promotional

- •

Educational

- •

Empathetic

Tone Shifts

The tone shifts from broadly relational ('our thing') to transactional and benefit-driven in the rewards section ('Earn 5%').

It becomes more educational and advisory in the 'Making Your Finances Work Harder' section.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Discover provides a refreshingly human and rewarding banking experience with straightforward cashback rewards, excellent customer service, and fewer fees to help customers achieve a brighter financial future.

Value Proposition Components

- Component:

Generous Cashback Rewards

Clarity:Clear

Uniqueness:Somewhat Unique

Comment:The rotating 5% categories and Cashback Match for the first year are key differentiators.

- Component:

Customer-Centric Service

Clarity:Clear

Uniqueness:Unique

Comment:The 'Treating people special' message is a core brand pillar and a recognized strength.

- Component:

No/Low Fees

Clarity:Somewhat Clear

Uniqueness:Somewhat Unique

Comment:Mentioned for checking/savings but less explicitly for credit cards (e.g., no annual fee) on the homepage, though it's a known feature.

- Component:

Accessibility for Credit Builders

Clarity:Clear

Uniqueness:Somewhat Unique

Comment:The clear callout for 'New to Credit?' and secured cards effectively targets this segment.

- Component:

Financial Wellness Tools & Guidance

Clarity:Clear

Uniqueness:Common

Comment:Providing articles and calculators is common, but Discover integrates it well into their supportive narrative.

Discover effectively differentiates itself from competitors like Amex (premium lifestyle), Chase (travel rewards focus), and major banks (impersonal) by focusing on approachability, simplicity, and customer service. The brand personality is its strongest differentiator. While cashback is a common feature, Discover's program is perceived as straightforward and valuable, especially for everyday spend categories. The emphasis on treating customers well carves out a distinct market position centered on trust and positive experience over prestige.

Discover positions itself as the smart, friendly, and accessible alternative in the financial services market. It targets value-conscious consumers, including those new to credit or underserved by traditional banks. Messaging avoids jargon and focuses on tangible benefits and a supportive relationship, positioning the brand as a partner in financial progress rather than just a product provider. This contrasts with the more aspirational or corporate messaging of many competitors.

Audience Messaging

Target Personas

- Persona:

The Value Maximizer

Tailored Messages

- •

5% cash back with your Discover Card

- •

Find great cash back rewards

- •

Cashback Checking

Effectiveness:Effective

- Persona:

The Credit Builder / Student

Tailored Messages

- •

New to Credit?

- •

Discover it Secured Card might be a good card for you

- •

Getting your first credit card

Effectiveness:Effective

- Persona:

The Financially Cautious / Debt-Conscious

Tailored Messages

- •

Easy credit card preapproval check

- •

no impact to your credit to check

- •

Making a balance transfer is a great way to save money on higher interest debt

- •

Personal Loans

Effectiveness:Effective

Audience Pain Points Addressed

- •

Perception of limited acceptance ('accepted nationwide by 99%')

- •

High credit card fees (implied by 'no monthly fees' for banking)

- •

Fear of hurting credit score ('no impact to your credit to check')

- •

Complexity of financial products ('Free benefits that just make sense')

- •

Feeling like just a number to big banks ('Treating people special')

Audience Aspirations Addressed

- •

Achieving a brighter financial future

- •

Making smart money choices ('Making Your Finances Work Harder')

- •

Reaching savings goals ('get serious about saving')

- •

Being treated with respect by a financial institution

Persuasion Elements

Emotional Appeals

- Appeal Type:

Belonging & Care

Effectiveness:High

Examples

Treating people special is kind of our thing.

We've got your financial needs covered.

- Appeal Type:

Empowerment & Control

Effectiveness:Medium

Examples

- •

Making Your Finances Work Harder For You

- •

We can help you get serious about saving

- •

Take full advantage of your Discover Card and explore your benefits.

- Appeal Type:

Security & Reassurance

Effectiveness:Medium

Examples

Discover is accepted nationwide by 99%...

no impact to your credit to check

Social Proof Elements

- Proof Type:

Market Acceptance Data

Impact:Strong

Example:Discover is accepted nationwide by 99% of the places that take credit cards. Based on the Feb 2024 Nilson Report.

Trust Indicators

- •

Citing third-party data (Nilson Report)

- •

Transparency about discontinued products (Home Loans, Student Loans)

- •

Clear, accessible language, avoiding fine print in primary messaging

- •

Dedicated accessibility statement, signaling corporate responsibility

Scarcity Urgency Tactics

Time-limited offers for 5% cash back categories ('Jul 1–Sept 30')

Calls To Action

Primary Ctas

- Text:

See Credit Card Offers

Location:Homepage, below hero

Clarity:Clear

- Text:

Check if you're pre approved

Location:Homepage Tile

Clarity:Clear

- Text:

Calculate Savings

Location:Homepage Savings Section

Clarity:Clear

- Text:

Learn More

Location:Homepage Tiles

Clarity:Clear

The CTAs are highly effective. They are action-oriented, use simple language, and are contextually relevant to the surrounding content. The use of lower-commitment CTAs like 'Check if you're pre approved' and 'Calculate Savings' is a smart strategy to reduce friction and encourage engagement from users who are not yet ready to apply.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of customer testimonials or stories. The brand claims to treat people special but doesn't show it through the voice of the customer on the homepage.

- •

The well-known differentiator of '100% U.S.-based customer service' is not explicitly mentioned on the homepage, which is a significant missed opportunity to substantiate the 'treating people special' claim.

- •

The connection between the products and the overarching mission of a 'brighter financial future' is not explicitly drawn. The site presents the tools (cards, loans) but doesn't build a strong narrative around the outcome.

Contradiction Points

No itemsUnderdeveloped Areas

Storytelling. The brand could move beyond claiming its values to demonstrating them through narrative examples of customer success.

Community/Inclusion. While the Accessibility page is excellent, the broader theme of inclusion and community could be better integrated into the main brand narrative on the homepage.

Messaging Quality

Strengths

- •

Extraordinarily clear and consistent brand voice that is friendly and customer-centric.

- •

Strong opening with an emotional, memorable brand promise.

- •

Proactively addresses a key historical objection (merchant acceptance) with hard data.

- •

Excellent segmentation in messaging, with clear paths for credit builders, value seekers, and those needing loans.

Weaknesses

- •

Over-reliance on claims versus evidence (e.g., testimonials, awards).

- •

Key competitive advantages, like U.S.-based customer service, are not messaged prominently.

- •

The brand mission statement feels somewhat disconnected from the tactical, product-focused messaging on the homepage.

Opportunities

- •

Incorporate a 'Customer Stories' or 'Member Since' module to provide social proof and emotional connection.

- •

Develop a clearer narrative thread that connects using Discover's products (the 'how') to achieving a 'brighter financial future' (the 'why').

- •

Create more content around 'spending smarter' and 'managing debt better' to give more substance to the company's mission.

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition Communication

Recommendation:Add a prominent callout on the homepage explicitly stating '100% U.S.-Based Customer Service' to provide a concrete proof point for the 'Treating people special' message.

Expected Impact:High

- Area:

Social Proof & Trust

Recommendation:Integrate a module with brief, rotating customer testimonials (e.g., 'What our members are saying') that align with key value propositions like service, rewards, and simplicity.

Expected Impact:High

- Area:

Narrative Cohesion

Recommendation:Rewrite the 'Making Your Finances Work Harder' section to be 'Building Your Brighter Future' and frame the content to more directly connect product use with achieving financial goals.

Expected Impact:Medium

Quick Wins

- •

Add '100% U.S.-Based Customer Service' to the 'Free benefits' tile.

- •

A/B test CTA language, for example, 'Find Your Card' vs. 'See Credit Card Offers'.

- •

Explicitly mention 'No Annual Fee' on the main credit card section overview.

Long Term Recommendations

Invest in a content marketing strategy focused on customer success stories, creating short videos or articles that showcase how real people have used Discover products to improve their financial lives.

Develop a more robust 'Financial Wellness Hub' that integrates tools like the savings calculator with personalized content and advice, further cementing the brand's role as a helpful partner.

Discover's website messaging is a masterclass in establishing a clear, consistent, and approachable brand identity in the often-impersonal financial services industry. The central message, 'Treating people special is kind of our thing,' serves as a powerful and memorable anchor for the entire user experience. It effectively positions the brand as a customer-centric alternative and directly informs the supportive and simple brand voice.

The messaging architecture is strategically sound, moving the user from an emotional brand connection to tangible, high-value proofs like 5% cash back and 99% merchant acceptance. This addresses both the emotional ('How will you treat me?') and rational ('What's in it for me?') decision-making criteria of a prospective customer. The messaging effectively segments its audience, providing clear pathways for students, credit-builders, and value-seekers without cluttering the primary user journey.

However, the strategy has critical gaps. The most significant is the underutilization of proof. The brand tells you it treats people special but doesn't show you via customer testimonials or by highlighting its award-winning, U.S.-based customer service on the homepage—a powerful differentiator that is core to its brand identity. While trust is built through transparency and clear language, it could be substantially amplified with social proof.

To elevate its market position, Discover should focus on weaving a stronger narrative that connects its products to its mission. The messaging is excellent at communicating product features and benefits but could do more to tell the story of how these tools lead to the 'brighter financial future' it promises. By infusing the site with authentic customer voices and more explicitly linking its offerings to long-term financial wellness, Discover can evolve its message from being just a friendly and rewarding choice to being an indispensable partner in its customers' financial success.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Established brand with high recognition in the U.S. financial services market.

- •

Serves over 51 million cardholders worldwide, indicating a large and loyal customer base.

- •

Ranks consistently high in customer satisfaction studies, reinforcing its customer-centric value proposition.

- •

Offers a diversified product portfolio including credit cards, online banking (savings, checking), and personal loans, catering to a wide range of consumer financial needs.

- •

Successfully targets and acquires younger demographics and those new to credit, a key growth segment.

Improvement Areas

- •

Enhance the value proposition for affluent customers to better compete with premium cards from Amex and Chase.

- •

Accelerate digital feature development to match the agility of FinTech 'neobanks' in areas like budgeting tools and personalized financial advice.

- •

Address the market perception of being a 'basic' or 'starter' card to improve retention as customers' credit profiles mature.

Market Dynamics

Moderate. The overall US financial services industry is mature, but segments like digital banking and consumer credit are experiencing steady growth. Discover's revenue grew 9.4% year-over-year in 2025.

Mature

Market Trends

- Trend:

Digital Transformation and FinTech Adoption

Business Impact:Consumers increasingly expect seamless, mobile-first banking experiences. 31% of US households now have a digital-only bank account, creating pressure for Discover to innovate its digital platforms to retain and attract customers.

- Trend:

Demand for Personalization and Financial Wellness

Business Impact:There is a growing consumer desire for personalized financial advice and tools integrated into their banking apps. This is an opportunity for Discover to deepen customer relationships beyond transactional services.

- Trend:

Intensifying Competition

Business Impact:Competition is fierce from large traditional banks (Chase, Capital One), other networks (Visa, Amex), and agile FinTechs (Chime, SoFi) that are challenging traditional business models.

- Trend:

Evolving Consumer Loyalty

Business Impact:Younger demographics, particularly Gen Z, show a higher propensity to switch banks. Retaining these customers requires more than just good rewards; it demands a superior digital experience and brand alignment.

Favorable. While the market is mature, the ongoing shift to digital finance creates significant opportunities for established players with strong brands and large customer bases like Discover to capture further market share by innovating their offerings.

Business Model Scalability

High

The business model, centered on interest income and transaction fees, has a favorable cost structure with high upfront fixed costs in technology and marketing, but low marginal costs per customer.

High. Once technology platforms and regulatory frameworks are in place, adding new customers or processing more transactions can be done at a relatively low incremental cost, leading to margin expansion with scale.

Scalability Constraints

- •

Regulatory and Compliance Overhead: Scaling requires significant ongoing investment in compliance infrastructure to manage evolving financial regulations.

- •

Credit Risk Management: Rapid loan portfolio growth increases exposure to credit risk, requiring sophisticated underwriting and monitoring systems to scale safely.

- •

Customer Service Capacity: Maintaining a high level of customer service, a key brand differentiator, becomes more complex and costly at a larger scale.

Team Readiness

Strong. As an established public company, Discover has an experienced leadership team capable of managing large-scale operations and financial performance. Recent earnings beats demonstrate solid execution.

Functional. The structure is organized into Direct Banking and Payment Services segments, which is standard for the industry but may create silos that slow down cross-functional, agile growth initiatives.

Key Capability Gaps

- •

Agile Product Development: Need to enhance capabilities to rapidly develop and deploy new digital features to compete with FinTechs.

- •

Data Science and AI for Personalization: Requires deeper talent in data science to move from broad segmentation to hyper-personalized customer experiences and offers.

- •

Growth Marketing: Building a dedicated, cross-functional growth team focused on experimentation and rapid iteration across the customer lifecycle.

Growth Engine

Acquisition Channels

- Channel:

Direct Mail

Effectiveness:High

Optimization Potential:Medium

Recommendation:Leverage data analytics to improve targeting for pre-approved offers, focusing on segments with high lifetime value potential beyond just creditworthiness.

- Channel:

Digital Advertising (Paid Search & Social)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Increase investment in performance marketing on platforms favored by younger demographics (e.g., TikTok, YouTube). A/B test creative and messaging focused on financial wellness features, not just cashback rewards.

- Channel:

Affiliate Marketing (e.g., Credit Karma, NerdWallet)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Develop exclusive offers or co-branded content with top-tier affiliates to stand out in a crowded marketplace. Structure payouts to reward high-quality, engaged customers.

- Channel:

Content Marketing ('Card Smarts')

Effectiveness:Medium

Optimization Potential:High

Recommendation:Expand content from foundational financial literacy to more advanced topics. Develop interactive tools (calculators, simulators) and video content to increase engagement and capture leads earlier in the customer journey.

Customer Journey

The online journey is well-defined, with clear CTAs for pre-approval and application. The path from awareness of rewards to application is straightforward.

Friction Points

- •

Potential complexity in the full application process after pre-approval.

- •

Lack of immediate, fully digital account activation and virtual card issuance compared to leading neobanks.

- •

Transition from single-product user (credit card) to multi-product user (banking, loans) is not seamlessly integrated.

Journey Enhancement Priorities

{'area': 'Onboarding', 'recommendation': 'Implement an instant virtual card upon approval that can be provisioned to mobile wallets, bridging the gap between approval and physical card arrival.'}

{'area': 'Cross-selling', 'recommendation': "Create personalized, in-app offers for banking or personal loan products based on a customer's spending habits and financial health data."}

Retention Mechanisms

- Mechanism:

Cashback Rewards Program

Effectiveness:High

Improvement Opportunity:Introduce personalization to the 5% rotating categories based on individual spending habits, or offer flexible reward redemption options beyond cash back (e.g., fractional investing, crypto).

- Mechanism:

Customer Service

Effectiveness:High

Improvement Opportunity:Integrate AI-powered chatbots for instant resolution of common queries while retaining high-quality human support for complex issues, thereby improving efficiency without sacrificing quality.

- Mechanism:

Free Credit Score Monitoring & Security Alerts

Effectiveness:Medium

Improvement Opportunity:Evolve from a passive monitoring tool to an active financial wellness coach, providing proactive insights and recommendations on how to improve credit scores or manage debt.

Revenue Economics

Strong. The business model benefits from diversified revenue streams, including net interest income, interchange fees, and other non-interest income.

Favorable (Estimated). Industry averages suggest a CAC of ~$80-200 per credit card customer with an annual profit of ~$120, indicating a healthy ratio. Discover's strong brand may lead to a lower CAC.

High. The company demonstrates strong profitability and revenue growth, with recent reports showing a 30% YoY increase in net income and a 2% rise in revenue net of interest expense.

Optimization Recommendations

- •

Increase multi-product adoption: Drive higher LTV by effectively cross-selling online banking and personal loan products to the existing cardholder base.

- •

Optimize interchange revenue: Promote card usage in high-interchange categories and continue expanding merchant acceptance globally.

- •

Enhance risk-based pricing: Use advanced data analytics to refine pricing strategies for loans and credit lines to maximize net interest margin while managing risk.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Banking Systems

Impact:Medium

Solution Approach:Adopt a two-speed IT architecture, maintaining the stable legacy core while building a more agile, API-driven layer on top for rapid development of new customer-facing features and partner integrations.

Operational Bottlenecks

- Bottleneck:

Regulatory Compliance & Reporting

Growth Impact:Slows down new product launches and market entry due to extensive compliance review cycles.

Resolution Strategy:Invest in 'RegTech' solutions to automate compliance monitoring and reporting, reducing manual effort and accelerating time-to-market for new initiatives.

- Bottleneck:

Fraud Detection at Scale

Growth Impact:Increased transaction volume from growth elevates the risk and complexity of fraud, potentially leading to higher losses.

Resolution Strategy:Enhance fraud detection models with real-time machine learning to identify and prevent fraudulent activities more accurately without adding friction for legitimate customers.

Market Penetration Challenges

- Challenge:

Market Saturation and Intense Competition

Severity:Critical

Mitigation Strategy:Differentiate beyond price and rewards by building a superior digital ecosystem focused on financial wellness and personalization. Target underserved or growing niches, such as Gen Z and small businesses.

- Challenge:

Brand Perception vs. Premium Competitors

Severity:Major

Mitigation Strategy:Launch a targeted marketing campaign to highlight premium features and high customer satisfaction. Consider introducing a higher-tier card product with enhanced benefits to attract more affluent customers.

Resource Limitations

Talent Gaps

- •

AI/ML Engineers and Data Scientists

- •

UX/UI Designers with experience in financial services

- •

Agile Product Managers

Moderate. While profitable, aggressive growth initiatives such as major technology overhauls, acquisitions, or large-scale international expansion would require significant capital investment.

Infrastructure Needs

Cloud-native platform for hosting next-generation digital banking services.

Centralized customer data platform to enable a single, real-time view of the customer across all products.

Growth Opportunities

Market Expansion

- Expansion Vector:

Gen Z and Young Millennials

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Develop a targeted value proposition including features like small-dollar 'credit builder' loans, integration with budgeting apps, and marketing through authentic creator partnerships on relevant social platforms.

- Expansion Vector:

Small Business Segment

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Launch a suite of small business credit cards and a checking account with features tailored to entrepreneurs, such as expense management tools and integrations with accounting software.

Product Opportunities

- Opportunity:

Integrated Financial Wellness Platform

Market Demand Evidence:Consumers, especially millennials, are seeking advice on savings, budgeting, and credit management directly from their financial institutions.

Strategic Fit:Strong. Leverages existing customer trust and data to provide a value-added service that increases engagement and retention.

Development Recommendation:Develop an in-app hub that offers automated savings tools, spending analysis, debt management plans, and personalized financial insights.

- Opportunity:

Buy Now, Pay Later (BNPL) Features

Market Demand Evidence:Rapid consumer adoption of BNPL services from companies like Affirm and Klarna is challenging traditional credit card usage for point-of-sale financing.

Strategic Fit:Medium. Competes with a core function of credit cards but addresses a clear consumer trend.

Development Recommendation:Introduce a 'Discover Pay in 4' feature that allows cardholders to split larger purchases into short-term, interest-free installments directly within their existing credit line.

Channel Diversification

- Channel:

Financial Influencer Marketing

Fit Assessment:High

Implementation Strategy:Partner with credible financial influencers on platforms like YouTube, Instagram, and TikTok to create educational content that authentically integrates Discover's products as tools for achieving financial goals.

- Channel:

Embedded Finance / BaaS (Banking-as-a-Service)

Fit Assessment:Medium

Implementation Strategy:Explore partnerships with non-financial companies (e.g., large retailers, gig economy platforms) to provide white-label credit card or payment processing services, leveraging Discover's network and infrastructure.

Strategic Partnerships

- Partnership Type:

FinTech Integrations

Potential Partners

- •

YNAB (You Need A Budget)

- •

Mint

- •

Acorns

Expected Benefits:Enhance the value of Discover's products by allowing seamless data sharing and integration with popular personal finance apps, increasing daily utility and customer stickiness.

- Partnership Type:

Co-Branded Credit Cards

Potential Partners

- •

Major grocery chains

- •

Streaming services

- •

Travel aggregators

Expected Benefits:Acquire new customers at a lower cost by tapping into the partner's loyal customer base and offering tailored, high-value rewards.

Growth Strategy

North Star Metric

Weekly Multi-Product Active Customers

This metric shifts the focus from simply acquiring single-product customers to measuring deeper engagement and relationship-building. Growth in this metric indicates success in cross-selling and building a more defensible, higher LTV customer base.

Increase by 15% annually.

Growth Model

Hybrid: Content-led Acquisition + Product-led Expansion

Key Drivers

- •

High-quality financial literacy content attracting new-to-credit users.

- •

Seamless digital onboarding process.

- •

In-product discovery of additional services (banking, loans).

- •

Personalized offers that drive adoption of new products.

Use content and SEO to attract users seeking financial guidance. Once acquired, use in-app messaging, email, and personalized nudges based on user behavior to drive adoption of banking and loan products.

Prioritized Initiatives

- Initiative:

Launch 'Discover Financial Wellness Hub'

Expected Impact:High

Implementation Effort:Medium

Timeframe:6-9 months

First Steps:Conduct customer research to identify top financial wellness needs. Develop an MVP roadmap starting with spending analysis and savings goal tools.

- Initiative:

Develop a Gen Z Targeted Acquisition Campaign

Expected Impact:High

Implementation Effort:Medium

Timeframe:3-6 months

First Steps:Identify 5-10 authentic financial creators on TikTok and YouTube. Co-create a campaign focused on building credit responsibly and managing money in college.

- Initiative:

Pilot an 'Instant Virtual Card' Feature

Expected Impact:Medium

Implementation Effort:Low

Timeframe:3 months

First Steps:Develop a secure process for provisioning a virtual card to a mobile wallet immediately upon application approval. Launch as an A/B test to measure impact on initial card usage.

Experimentation Plan

High Leverage Tests

- Area:

Acquisition

Test:Test different welcome offers for student cards: higher upfront cashback vs. a subscription credit (e.g., Spotify, Netflix).

- Area:

Engagement

Test:A/B test personalized vs. standard 5% cashback categories for a cohort of users to measure impact on spend and satisfaction.

- Area:

Retention

Test:Experiment with proactive credit line increase offers for customers who demonstrate responsible usage patterns to see if it reduces attrition.

Use an A/B testing platform to track key metrics for each experiment, including conversion rates, activation rates, average spend, product adoption, and 30-day retention.

Run a bi-weekly 'Growth Sprint' to review experiment results, share learnings, and prioritize the next batch of tests.

Growth Team

Cross-functional 'Growth Pods' aligned to key metrics (e.g., New User Activation, Multi-Product Adoption). Each pod should be empowered with autonomy to ideate and execute experiments.

Key Roles

- •

Head of Growth

- •

Product Manager (Growth)

- •

Growth Marketing Manager

- •

Data Scientist

- •

Lead Software Engineer

Invest in training on experimentation, data analysis, and agile methodologies for all team members. Create a culture that celebrates learning from both successful and failed tests.

Discover Financial Services possesses a strong foundation for growth, built on a well-recognized brand, a large and loyal customer base, and a scalable, profitable business model. The company has successfully established a robust product-market fit, particularly within the mainstream consumer credit market and among those new to credit. However, the financial services landscape is undergoing a rapid digital transformation, presenting both a significant opportunity and a critical threat.

The primary barrier to accelerated growth is the intense competition from two fronts: large incumbent banks with massive resources and premium brand perception (Amex, Chase) and agile FinTech challengers who are setting new standards for digital customer experience (Chime, SoFi). While Discover's customer service and cashback rewards are key strengths, they are no longer sufficient differentiators in a market where digital convenience and personalized financial wellness tools are becoming paramount.

Key growth opportunities lie in deepening relationships with the existing 51 million+ customers and aggressively targeting new, younger demographics. The most promising vectors are: 1) Evolving from a suite of siloed products into an integrated Financial Wellness Platform, which would increase customer engagement, build a competitive moat, and improve retention. 2) Systematically pursuing the Small Business segment with tailored products. 3) Specifically targeting Gen Z with a value proposition that extends beyond cashback to include credit-building tools and authentic, educational content.

To capture this potential, Discover must adopt a more agile, experimental approach to growth. The recommended strategy is to implement a hybrid growth model: using Content-led Acquisition to attract users early in their financial journey and Product-led Expansion to drive them towards multi-product adoption. The North Star Metric should shift to Weekly Multi-Product Active Customers to align the organization around building deeper customer relationships. Prioritized initiatives should include launching a financial wellness hub, creating a targeted Gen Z acquisition campaign, and iterating on the digital onboarding experience. Building a dedicated, cross-functional growth team will be essential to drive the required velocity of experimentation and innovation needed to win in the next decade of financial services.

Legal Compliance

Discover maintains a comprehensive and well-structured 'Privacy Center' accessible from the website footer. This center provides distinct, detailed privacy notices for different products (credit cards, banking, loans) as required by the Gramm-Leach-Bliley Act (GLBA). The policies clearly outline the types of nonpublic personal information (NPI) collected, the reasons for sharing it, and whether consumers can limit this sharing, fulfilling GLBA's Financial Privacy Rule requirements. Specific sections for California residents address CCPA/CPRA rights, including a 'Notice at Collection' and a clear link to 'Make a Request to Opt out of Sharing,' demonstrating a robust mechanism for state-level compliance. The inclusion of a dedicated notice for EEA, UK, and Swiss data subjects indicates an awareness of GDPR obligations, although the primary focus is clearly on U.S. regulations.

The website provides a clear 'Terms of Use' link in the footer governing the use of the website itself. These terms are standard, covering intellectual property, disclaimers of liability, and user responsibilities. For its financial products, the legally binding document is the 'Cardmember Agreement,' which is provided to customers upon application and approval. The website offers a resource center to request a copy of this agreement, which is a good practice for transparency. This separation between general website use and specific product agreements is a standard and legally sound approach for a financial institution, ensuring that product-specific terms are clearly delineated and enforceable.

Upon visiting the site, a prominent cookie banner appears, notifying users about the use of cookies and tracking technologies. It provides an immediate 'OK' option for acceptance and a link to 'Cookie Preferences.' This preference center allows users to granularly control consent by toggling options for 'Functional Cookies,' 'Advertising Cookies,' and 'Analytics Cookies.' This mechanism is a best practice, aligning with the requirements of CCPA/CPRA and GDPR by obtaining user consent before deploying non-essential trackers and offering clear, specific choices rather than just a blanket acceptance.