eScore

erieinsurance.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Erie Insurance demonstrates strong brand authority and content alignment for users already considering their products, effectively leveraging trust signals like J.D. Power awards. However, its digital presence is significantly constrained by its regional focus, causing it to be outranked by national competitors on broader search terms. The website serves more as a validation tool and agent locator rather than a primary, top-of-funnel customer acquisition engine, with underdeveloped SEO and voice search optimization for non-branded, informational queries.

Excellent use of the website to reinforce brand authority and trust for users in the consideration and decision stages within their operating regions.

Implement a hyper-local SEO strategy, creating content hubs and tools specifically for each state and major metropolitan area they serve to capture high-intent, geographically specific search queries.

The brand's messaging is exceptionally clear, consistent, and differentiated, focusing on the core value proposition of superior service via independent agents. This is powerfully supported by quantitative proof points like the '90%+ customer retention' statistic. However, the communication is overly reliant on data and lacks emotional resonance, missing a major opportunity to use customer storytelling to illustrate *why* their service is superior.

A clear, consistent, and defensible messaging strategy that effectively differentiates the brand from price-focused national competitors by emphasizing the human-centric agent model.

Develop a content series featuring authentic video testimonials from customers and agents detailing positive claims experiences to bring the 'superior service' promise to life.

The website provides a clean, professional, and trustworthy user experience with a light cognitive load and clear navigation. However, the primary conversion path for 'Get a Quote' introduces significant friction by requiring multiple data inputs upfront in the hero section and ultimately funnels users into an offline process with an agent. This online-to-offline handoff is a major barrier compared to the seamless digital funnels of direct-to-consumer competitors, and the mobile experience has been rated poorly by users.

A well-structured and uncluttered information architecture that effectively communicates trustworthiness and makes it easy for users to find product information.

Redesign the primary 'Get a Quote' call-to-action to be a single button that leads to a dedicated, streamlined, multi-step form, reducing initial friction and improving lead capture rates.

Erie excels in establishing credibility through a powerful hierarchy of trust signals, including its A+ A.M. Best rating, Fortune 500 status, and consistently high J.D. Power rankings for customer satisfaction. The company maintains a strong compliance posture with industry-specific regulations like GLBA and has a comprehensive Accessibility Statement. A recent network outage and subsequent lawsuits, alongside a compliance gap concerning CCPA/CPRA, present moderate risks that slightly temper an otherwise outstanding score.

Leveraging elite third-party validation (A.M. Best A+ rating, multiple J.D. Power awards) prominently across the site to build immediate and powerful trust.

Update the privacy policy to explicitly address CCPA/CPRA rights for non-GLBA covered data (e.g., website marketing data) to close a key compliance gap and mitigate regulatory risk.

Erie's competitive moat is deep and sustainable, built on a human-centric, independent agent model that fosters industry-leading customer retention (90%+) and satisfaction. This service-oriented culture is extremely difficult for digital-first competitors to replicate. However, this advantage is geographically constrained to 12 states, and the agent-based model creates higher switching costs for customers but also slows down digital innovation and market expansion.

The synergistic combination of an independent agent network and a culture of superior service creates an exceptionally high customer retention rate, which acts as a powerful and sustainable economic moat.

Invest in 'Agent-Tech'—a modern digital toolkit for agents—to blend the human-touch advantage with the digital convenience customers now expect, thus strengthening the moat against tech-savvy competitors.

The company's growth potential is severely constrained by its business model, which relies on the slow and capital-intensive process of building out agent networks in new states. The agent-centric cost structure offers limited operational leverage compared to tech-driven, direct-to-consumer models. While unit economics are likely healthy due to high LTV, the model is not built for rapid, exponential scaling, and its geographic limitation caps the total addressable market.

Strong and stable unit economics, evidenced by a very high customer lifetime value (LTV) driven by exceptional retention rates, providing a profitable foundation for any expansion.

Develop a playbook for a 'digital-first' market entry into a new state, using a direct-to-consumer model to establish a customer base efficiently before making the larger investment in a physical agent network.

Erie's business model demonstrates exceptional coherence, with a clear alignment between its value proposition (service and trust), target audience (relationship-seekers), and distribution channel (independent agents). The revenue model, based on recurring premiums and investment income, is stable and proven over a century of operation. The model's primary challenge is its market timing, as it is slow to adapt to the digital-first preferences of emerging consumer segments.

An almost perfect alignment between the company's service-centric value proposition, its agent-based distribution model, and the needs of its target customer segment, creating a highly effective and self-reinforcing system.

Pilot a hybrid service model where customers can choose their interaction method (agent, app, web) for different tasks, improving alignment with modern, omni-channel consumer expectations.

Within its 12-state operational footprint, Erie is a major player with significant market power, evidenced by its high customer retention and ability to compete on value rather than price alone. The company consistently earns top satisfaction rankings, giving it pricing power and insulating it from purely price-based competition. However, its influence is regional, not national, and it lacks the scale and brand awareness to shape broader market trends compared to giants like State Farm or Progressive.

Extremely high customer loyalty and top-tier satisfaction ratings provide significant pricing power and a strong defensive position against competitors within its established markets.

Launch targeted digital marketing campaigns in existing states that explicitly highlight J.D. Power rankings and the 90%+ retention rate to reinforce its premium service position and defend market share.

Business Overview

Business Classification

Insurance Provider

Property & Casualty (P&C) and Life Insurance Carrier

Financial Services

Sub Verticals

- •

Personal Lines (Auto, Home, Umbrella)

- •

Commercial Lines (Business)

- •

Life & Retirement Products

Mature

Maturity Indicators

- •

Founded in 1925, demonstrating a century of operational history.

- •

Consistently ranked as a Fortune 500 company.

- •

Maintains a strong financial strength rating of A+ (Superior) from A.M. Best.

- •

Established distribution network of over 13,000 independent agents across 12 states and D.C.

- •

High customer retention, with over 90% of customers staying year after year, as stated on their website.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Insurance Premiums

Description:The primary source of revenue, generated from underwriting and selling a diversified portfolio of insurance policies, including auto, home, business, and life insurance. This is recurring revenue from policy renewals.

Estimated Importance:Primary

Customer Segment:Individuals, Families, Small to Medium-sized Businesses

Estimated Margin:Medium

- Stream Name:

Investment Income

Description:Income generated from investing the 'float' – premiums collected before claims are paid out. These funds are invested in a portfolio of bonds, stocks, and other securities.

Estimated Importance:Secondary

Customer Segment:N/A (Internal Operation)

Estimated Margin:High

- Stream Name:

Management Fees (Erie Indemnity Co.)

Description:Erie Indemnity Company (NASDAQ: ERIE) acts as the attorney-in-fact for the Erie Insurance Exchange, earning management fees calculated as a percentage of the premiums written by the Exchange. This is a core part of the unique reciprocal exchange structure.

Estimated Importance:Primary (for the publicly traded entity)

Customer Segment:Erie Insurance Exchange

Estimated Margin:High

Recurring Revenue Components

Policy Renewals for Personal and Commercial Lines

Recurring Premiums for Life Insurance Policies

Pricing Strategy

Risk-Based Underwriting

Value-Oriented / Mid-Range

Opaque

Pricing Psychology

- •

Bundling Discounts (e.g., auto and home)

- •

Loyalty Discounts (implied by high retention rates)

- •

Value-Based Pricing (emphasizing service over lowest cost)

Monetization Assessment

Strengths

- •

High customer retention provides a stable and predictable premium base.

- •

Diversified product mix across P&C and Life reduces dependency on any single line of business.

- •

The reciprocal exchange model aligns the interests of the company with its policyholders (members).

Weaknesses

- •

Pricing may be less competitive against direct-to-consumer models that have lower overhead.

- •

The agent-based model incurs significant commission costs, which can impact margins.

- •

Slower to implement dynamic, usage-based pricing models compared to insurtech-native competitors.

Opportunities

- •

Leverage data analytics and AI for more sophisticated underwriting and personalized pricing.

- •

Develop and promote usage-based insurance (UBI) or telematics products for auto insurance.

- •

Introduce value-added services bundled with policies (e.g., smart home sensor kits for homeowners insurance).

Threats

- •

Increased price sensitivity among consumers, driven by digital comparison tools.

- •

Rising claims costs due to inflation, supply chain issues, and social inflation.

- •

Intense competition from direct-to-consumer insurers like Geico and Progressive and agile insurtech startups.

Market Positioning

Service-Centric, Agent-Driven Relationship Model

Major Regional Player

Target Segments

- Segment Name:

Relationship-Seeking Families

Description:Individuals and families who value personalized service and guidance from a local agent for their comprehensive insurance needs (auto, home, life, umbrella).

Demographic Factors

- •

Age 30-65

- •

Homeowners

- •

Multiple vehicles

- •

Presence of dependents

Psychographic Factors

- •

Value security and peace of mind

- •

Prefer human interaction over digital-only experiences

- •

Seek long-term relationships and trust

- •

Risk-averse

Behavioral Factors

- •

Likely to bundle multiple policies

- •

Low price sensitivity, high service sensitivity

- •

High loyalty and retention

Pain Points

- •

Feeling overwhelmed by complex insurance options

- •

Distrust of large, impersonal corporations

- •

Fear of being underinsured during a major life event or claim

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Main Street Small Businesses

Description:Small to medium-sized business owners who need tailored commercial insurance policies and prefer working with a local agent who understands their community and business risks.

Demographic Factors

Local service businesses, retailers, contractors, professional offices

Fewer than 100 employees

Psychographic Factors

- •

Community-oriented

- •

Value expert advice and risk management support

- •

Time-constrained and appreciate a single point of contact

Behavioral Factors

Seek comprehensive coverage (BOP, commercial auto, workers' comp)

Relationship-driven purchasing decisions

Pain Points

- •

Difficulty navigating the complexities of commercial insurance

- •

Lack of in-house risk management expertise

- •

Needing a responsive agent for certificates of insurance and policy changes

Fit Assessment:Excellent

Segment Potential:Medium

Market Differentiation

- Factor:

Independent Agent Distribution Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Customer Service and High Retention

Strength:Strong

Sustainability:Sustainable

- Factor:

Financial Strength and Stability

Strength:Strong

Sustainability:Sustainable

- Factor:

Brand Legacy and Trust (Since 1925)

Strength:Moderate

Sustainability:Sustainable

Value Proposition

To provide near-perfect protection and service through a dedicated network of local, independent agents, ensuring peace of mind at a fair price.

Excellent

Key Benefits

- Benefit:

Personalized Guidance from a Local Agent

Importance:Critical

Differentiation:Unique

Proof Elements

- •

Network of over 13,000 independent agents.

- •

Website features an agent finder prominently.

- •

Long-standing commitment to the agent model since founding.

- Benefit:

Superior Customer Service and Claims Handling

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Claim of over 90% customer retention year-over-year.

- •

Numerous customer service awards and recognitions.

- •

Historical emphasis on service, with founders taking calls directly.

- Benefit:

Financial Stability and Reliability

Importance:Important

Differentiation:Common

Proof Elements

- •

A+ (Superior) rating from A.M. Best.

- •

Fortune 500 company status.

- •

Long operating history since 1925.

Unique Selling Points

- Usp:

The combination of a human-centric, agent-based service model with the scale and financial strength of a Fortune 500 insurer.

Sustainability:Long-term

Defensibility:Strong

- Usp:

A corporate culture deeply rooted in service ('The ERIE is above all in sERvIcE'), which translates to demonstrably high customer loyalty.

Sustainability:Long-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

The complexity and confusion of choosing the right insurance coverage.

Severity:Major

Solution Effectiveness:Complete

- Problem:

Lack of personal support and advocacy during a stressful claims process.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

The impersonal and transactional nature of dealing with large, digital-first insurers.

Severity:Major

Solution Effectiveness:Complete

Value Alignment Assessment

High

Erie's model is perfectly aligned with the segment of the market that prioritizes service, trust, and relationships over obtaining the absolute lowest price.

High

The value proposition directly addresses the primary pain points of its target segments, who actively seek the guidance and personalized support that an independent agent provides.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Independent Insurance Agents (over 13,000)

- •

Reinsurance Companies

- •

Auto Repair Shops and Contractors (claims fulfillment)

- •

Technology Partners (for core systems and digital tools)

Key Activities

- •

Underwriting & Risk Assessment

- •

Claims Processing & Management

- •

Agent Network Management & Support

- •

Investment Management

- •

Product Development

- •

Regulatory Compliance

Key Resources

- •

Brand Reputation & Trust

- •

Extensive Independent Agent Network

- •

Financial Capital & Policyholder Surplus

- •

Underwriting Data & Actuarial Expertise

- •

A.M. Best A+ Rating

Cost Structure

- •

Claims Payouts (Loss & Loss Adjustment Expenses)

- •

Agent Commissions & Incentives

- •

Employee Salaries & Benefits

- •

Technology & Infrastructure Costs

- •

Marketing & Advertising

Swot Analysis

Strengths

- •

Extremely high customer retention and brand loyalty.

- •

Strong, well-established, and loyal independent agent distribution network.

- •

Superior financial strength rating (A+ from A.M. Best).

- •

Conservative and stable business model refined over nearly a century.

- •

Diversified portfolio across personal, commercial, and life insurance.

Weaknesses

- •

Heavy reliance on the independent agent model can slow digital adoption and create a higher expense structure.

- •

Slower to innovate and bring new tech-driven products (like telematics) to market compared to competitors.

- •

Geographically concentrated in 12 states and D.C., making it vulnerable to regional catastrophic events.

- •

The 12-month policy term can slow the realization of benefits from necessary rate increases.

Opportunities

- •

Invest in 'Agent-Tech' to empower agents with better digital tools for quoting, sales, and service.

- •

Leverage its new corporate venture arm, Erie Strategic Ventures, to partner with and invest in insurtech startups.

- •

Expand geographically into adjacent states where its brand and service model could be well-received.

- •

Develop more personalized insurance products using AI and big data analytics.

Threats

- •

Intense competition from tech-savvy, direct-to-consumer insurers with massive advertising budgets (e.g., Progressive, Geico).

- •

Increasing frequency and severity of catastrophic weather events driving up claims costs and underwriting volatility.

- •

Shifting consumer preferences, particularly among younger demographics, towards digital-first and self-service insurance purchasing.

- •

Cybersecurity risks, as evidenced by a recent network security event.

Recommendations

Priority Improvements

- Area:

Digital Transformation & Agent Enablement

Recommendation:Accelerate investment in a unified digital platform that provides agents with state-of-the-art quoting, CRM, and analytics tools to enhance efficiency and improve the end-customer experience.

Expected Impact:High

- Area:

Customer Self-Service Capabilities

Recommendation:Enhance the mobile app and customer portal to provide more robust self-service options (e.g., complex policy changes, full claims FNOL with AI assistance) while always maintaining a clear path to agent contact.

Expected Impact:Medium

- Area:

Advanced Data Analytics in Underwriting

Recommendation:Integrate more third-party data sources and leverage AI/ML to refine risk segmentation and pricing accuracy, particularly for commercial lines and complex personal risks.

Expected Impact:High

Business Model Innovation

- •

Develop a 'Hybrid' customer service model where clients can choose their preferred interaction method (agent, app, web) for different tasks, seamlessly.

- •

Pilot and scale Usage-Based Insurance (UBI) programs, leveraging the agent relationship to explain the benefits and privacy considerations to customers.

- •

Form strategic partnerships with IoT providers (e.g., smart home, water leak detectors, telematics) to offer proactive risk mitigation services, moving from 'repair and replace' to 'predict and prevent'.

Revenue Diversification

- •

Expand the portfolio of value-added services offered through agents, such as identity theft protection, digital estate planning, or home maintenance subscription services.

- •

Explore opportunities in niche or specialty commercial lines that align with the agent expertise model.

- •

Further develop retirement and annuity products to capture more of the existing customer base's financial lifecycle needs.

Erie Insurance operates a classic, highly successful, and mature insurance business model, built on the bedrock of a strong, symbiotic relationship with its network of independent agents. Its core competitive advantages—superior customer service, trust, and exceptionally high retention rates—are direct results of this agent-centric strategy. This model has proven remarkably durable and profitable for nearly a century, creating a loyal customer base that values personalized guidance over rock-bottom prices.

However, the primary strategic challenge facing Erie is the evolution required to thrive in the digital age. The very agent model that is its greatest strength also introduces potential weaknesses, such as a higher cost structure and slower adoption of digital technologies compared to direct-to-consumer competitors. The key to its future success does not lie in abandoning this model, but in digitally supercharging it. The strategic imperative is to transform from a traditional insurer with digital tools to a digitally-enabled company that empowers its core asset: the independent agent. By investing heavily in 'Agent-Tech,' enhancing data analytics for underwriting, and building seamless omni-channel experiences, Erie can fortify its value proposition, protect its market share against digital disruption, and position itself for another century of steady, service-driven growth.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

Regulatory Compliance and Licensing

Impact:High

- Barrier:

Capital and Financial Solvency Requirements

Impact:High

- Barrier:

Brand Recognition and Trust

Impact:High

- Barrier:

Distribution Network (Agent Relationships)

Impact:Medium

- Barrier:

Technological Infrastructure and Data Analytics Capabilities

Impact:Medium

Industry Trends

- Trend:

Digital Transformation and AI Integration

Impact On Business:Requires investment in modernizing agent tools, underwriting, and claims processing to meet customer expectations and improve efficiency.

Timeline:Immediate

- Trend:

Increased Competition from Insurtechs

Impact On Business:Pressure to enhance digital customer experience and offer more personalized, usage-based insurance (UBI) products to retain tech-savvy customers.

Timeline:Immediate

- Trend:

Personalization and Hyper-customization

Impact On Business:Opportunity to leverage agent relationships for deep customer insights, but pressure to translate that into tailored products and pricing.

Timeline:Near-term

- Trend:

Climate Change and Increased Catastrophe Risk

Impact On Business:Affects underwriting risk, pricing models, and reinsurance costs, particularly for property insurance lines.

Timeline:Long-term

Direct Competitors

- →

State Farm

Market Share Estimate:Largest P&C insurer in the U.S. with ~10.4% market share.

Target Audience Overlap:High

Competitive Positioning:Positions as a reliable, neighborhood-focused insurer with a vast 'captive' agent network, emphasizing personal relationships and bundled services.

Strengths

- •

Massive brand recognition and marketing budget.

- •

Largest agent network in the U.S., providing broad distribution.

- •

Leading market share provides economies of scale.

- •

Often competitive on pricing for bundled home and auto policies.

Weaknesses

- •

Can be slower to innovate due to its size and legacy systems.

- •

Customer service experience can be highly dependent on the quality of the individual agent.

- •

May not be the cheapest option for non-bundling customers or those with imperfect driving records.

Differentiators

"Like a good neighbor" branding focused on trust and presence.

Extensive 'captive' agent network (agents exclusively sell State Farm products).

- →

Progressive

Market Share Estimate:Second largest P&C insurer in the U.S. with ~7.3% market share.

Target Audience Overlap:High

Competitive Positioning:Positions as a tech-forward, direct-to-consumer insurer focused on price comparison, transparency, and usage-based insurance.

Strengths

- •

Dominant direct-to-consumer online and mobile experience.

- •

Strong brand identity and memorable, high-spend advertising campaigns.

- •

Pioneer and leader in telematics/usage-based insurance with 'Snapshot'.

- •

Offers a wide range of products and caters well to high-risk drivers.

Weaknesses

- •

Customer service can be less personalized compared to agent-based models.

- •

Can have lower customer satisfaction ratings for claims handling.

- •

Brand is heavily associated with auto insurance, potentially weaker for home and life.

Differentiators

- •

Name Your Price® tool and direct comparison rates.

- •

Heavy focus on technology and data analytics for pricing.

- •

Strong direct-to-consumer channel, bypassing traditional agents.

- →

Allstate

Market Share Estimate:Top 5 P&C insurer with a significant national presence.

Target Audience Overlap:High

Competitive Positioning:Positions as a provider of premium protection, with the tagline "You're in good hands," leveraging a large network of local agents combined with strong digital tools.

Strengths

- •

Strong brand recognition and reputation for reliability.

- •

Large network of agents providing local service.

- •

Offers a wide array of discounts and bundling options.

- •

Advanced telematics programs like Drivewise.

Weaknesses

Premiums can be higher than competitors, particularly for younger drivers.

Customer satisfaction scores can be average compared to top performers like Erie.

Differentiators

"Good Hands" branding emphasizing protection and support.

Feature-rich policies with options like accident forgiveness and new car replacement.

- →

Auto-Owners Insurance

Market Share Estimate:Major regional/super-regional competitor operating in 26 states.

Target Audience Overlap:Medium

Competitive Positioning:Positions as a service-focused, independent agent-based insurer with high customer satisfaction.

Strengths

- •

Exclusively sells through independent agents, similar to Erie's model.

- •

Consistently high rankings for customer and claims satisfaction.

- •

Offers a full suite of personal and commercial products.

Weaknesses

- •

Limited geographic availability (26 states).

- •

Lower brand recognition compared to national giants.

- •

Digital tools and online quoting capabilities lag behind direct-to-consumer leaders.

Differentiators

100% commitment to the independent agent model.

Often praised for its claims handling process.

Indirect Competitors

- →

Lemonade

Description:An insurtech company that uses AI and a mobile-first platform to offer renters, homeowners, pet, and term life insurance. It targets a younger, tech-savvy demographic.

Threat Level:Medium

Potential For Direct Competition:High, as they expand their product offerings (like auto insurance) and gain trust, they could appeal to a broader segment of Erie's customer base.

- →

The Zebra / Policygenius

Description:Insurance comparison aggregators that allow consumers to compare quotes from multiple carriers side-by-side. They commoditize the insurance product, focusing heavily on price.

Threat Level:Medium

Potential For Direct Competition:Low, as their model is based on partnership, but they threaten Erie's model by disintermediating the agent and making price the primary decision factor, reducing customer loyalty.

- →

Embedded Insurance (e.g., Tesla Insurance)

Description:Insurance offered at the point of sale by a non-insurance company. For example, Tesla leveraging vehicle data to offer its own auto insurance.

Threat Level:Low

Potential For Direct Competition:Low in the short-term, but represents a long-term systemic threat to the traditional distribution model as more large-ticket purchases (cars, homes) come with bundled insurance offers.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Independent Agent Network and Service Model

Sustainability Assessment:Highly sustainable. This human-centric model builds deep customer relationships and loyalty that is difficult for direct-to-consumer or AI-driven models to replicate.

Competitor Replication Difficulty:Hard

- Advantage:

Extremely High Customer Retention

Sustainability Assessment:Highly sustainable. A reported 90%+ retention rate is a powerful economic moat, reducing acquisition costs and indicating superior customer satisfaction.

Competitor Replication Difficulty:Hard

- Advantage:

Consistently High Customer Satisfaction and Claims Service Ratings

Sustainability Assessment:Sustainable with continued focus. Erie consistently ranks at the top of J.D. Power studies for auto and home insurance, which is a powerful differentiator.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Price Competitiveness in Specific Segments/Regions', 'estimated_duration': '1-3 years. While currently very competitive on price for many drivers, this can change quickly due to market dynamics and competitor actions. '}

{'advantage': "Unique Policy Features like 'Rate Lock'", 'estimated_duration': '3-5 years. Innovative policy features provide a current advantage but can be replicated by competitors over time. '}

Disadvantages

- Disadvantage:

Limited Geographic Footprint

Impact:Major

Addressability:Difficult. Expanding into new states is a capital-intensive and complex regulatory process. This inherently limits their total addressable market.

- Disadvantage:

Lower National Brand Awareness

Impact:Major

Addressability:Moderately. Overcoming the massive advertising spend of national competitors is challenging, requiring highly efficient and targeted marketing.

- Disadvantage:

Reliance on Traditional Agent Model Can Slow Digital Adoption

Impact:Minor

Addressability:Easily. While the agent model is a strength, the customer-facing and agent-enabling technology has been cited as an area for improvement.

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted digital marketing campaigns in existing states, highlighting J.D. Power rankings and the 90%+ retention rate.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Develop enhanced content marketing (blog, videos) explaining the value of an independent agent vs. a call center or app.

Expected Impact:Low

Implementation Difficulty:Easy

Medium Term Strategies

- Recommendation:

Invest heavily in digital tools for agents to streamline quoting, policy management, and client communication, blending human touch with digital convenience.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Expand telematics/UBI offerings to be more competitive with Progressive's Snapshot, using it as a tool for agents to offer personalized discounts.

Expected Impact:Medium

Implementation Difficulty:Moderate

- Recommendation:

Establish partnerships with regional banks or credit unions within the 12-state footprint to offer insurance products to their members.

Expected Impact:Medium

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Execute a phased, strategic geographic expansion into adjacent states where the brand and operational model can be effectively extended.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Explore creating a venture arm to invest in insurtech startups that can enhance the agent model, not replace it (e.g., AI for underwriting, automated claims processing).

Expected Impact:High

Implementation Difficulty:Difficult

Position Erie as the 'High-Tech, High-Touch' regional champion. Emphasize the unbeatable combination of a local, expert agent dedicated to your needs, empowered by best-in-class technology for convenience and efficiency.

Double down on the 'service and trust' axis. Differentiate not on price alone, but on the total value of superior service, stable rates, and the peace of mind that comes from a highly-rated insurer with exceptional customer loyalty. Use the 90%+ retention rate as the ultimate proof point of this value.

Whitespace Opportunities

- Opportunity:

Proactive Risk Mitigation Services

Competitive Gap:Most competitors are reactive (paying claims after an event). A proactive model (e.g., partnering to provide smart water sensors, discounted security systems) deepens relationships and reduces claims.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Specialized Insurance Packages for Niche Regional Markets

Competitive Gap:National giants often use a one-size-fits-all approach. Erie can leverage its regional focus to create tailored business or personal bundles for dominant local industries (e.g., wineries in NY, tech startups in NC).

Feasibility:Medium

Potential Impact:Medium

- Opportunity:

Financial Wellness and Insurance Planning Hub

Competitive Gap:Competitors sell policies. Erie can position its agents as holistic financial wellness advisors, using content and tools to help customers understand how life, auto, and home insurance fit into their broader financial picture.

Feasibility:High

Potential Impact:Medium

Erie Insurance operates within the mature and highly competitive U.S. Property and Casualty insurance industry. The market is moderately concentrated, with behemoths like State Farm, Progressive, and Allstate commanding significant market share through massive advertising budgets and national presence.

Erie's core competitive advantage is its powerful, sustainable combination of a dedicated independent agent network and a culture of superior customer service. This strategy has resulted in exceptionally high customer satisfaction ratings from J.D. Power and a remarkable 90%+ customer retention rate, which serves as a significant economic moat. Unlike national direct-to-consumer players who compete primarily on price and digital convenience, Erie competes on trust, personalized advice, and long-term relationships.

However, Erie's primary strategic challenges are its limited geographic footprint—operating in only 12 states and D.C.—and a corresponding lack of national brand awareness. This regional focus, while a source of strength, inherently caps its market potential and makes it vulnerable to the marketing scale of its national rivals. Furthermore, while its agent model is a key differentiator, it must be supported by modern digital tools to meet evolving customer expectations and prevent being outmaneuvered by nimble insurtechs like Lemonade, which appeal to a younger, digital-native demographic.

Strategic whitespace for Erie lies in leveraging its regional density and agent relationships in ways national competitors cannot. This includes creating hyper-localized insurance products, offering proactive risk management services that go beyond traditional policies, and positioning agents as holistic financial advisors. The key to future success will be to successfully blend its traditional, high-touch service model with a high-tech digital backbone that empowers both agents and customers. This 'high-tech, high-touch' approach will allow Erie to defend its loyal customer base while attracting a new generation that values both expert guidance and digital convenience.

Messaging

Message Architecture

Key Messages

- Message:

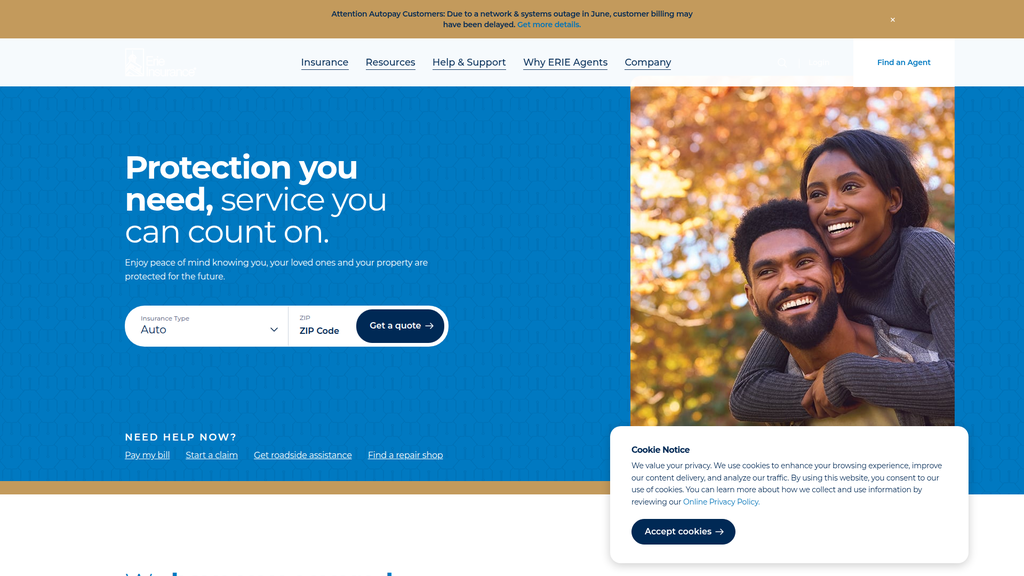

Protection you need, service you can count on.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero

- Message:

Our agents are our difference.

Prominence:Secondary

Clarity Score:High

Location:Homepage Mid-section

- Message:

Over 90% of our customers stay with ERIE year after year.

Prominence:Tertiary

Clarity Score:High

Location:Homepage Social Proof Section

- Message:

Access ERIE anytime, anywhere.

Prominence:Tertiary

Clarity Score:High

Location:Homepage Mobile App Section

The message hierarchy is logical and effective. It begins with a broad, benefit-oriented promise (protection and service), funnels into specific product categories, highlights the key brand differentiator (agents), and substantiates claims with powerful proof points (retention rate, A.M. Best rating). This structure successfully guides the user from a general need to Erie's specific solution.

Messaging is highly consistent across the homepage. Every section reinforces the central theme of dependable, human-centric service combined with comprehensive protection. The emphasis on agents, high retention rates, and financial stability all support the primary headline.

Brand Voice

Voice Attributes

- Attribute:

Dependable

Strength:Strong

Examples

- •

service you can count on.

- •

Our rating by A.M. Best-the largest company devoted to rating insurers' financial strength.

- •

Over 90% of our customers stay with ERIE year after year

- Attribute:

Human

Strength:Strong

Examples

- •

Our agents are our difference.

- •

The number of independent ERIE agents ready to help

- •

Protect your loved ones from potentially devastating financial loss.

- Attribute:

Straightforward

Strength:Moderate

Examples

- •

We have you covered.

- •

Explore our variety of policies

- •

Pair two or more insurance policies to save up to 25%

- Attribute:

Reassuring

Strength:Strong

Examples

- •

Enjoy peace of mind

- •

Protect yourself and your car

- •

Safeguard your business

Tone Analysis

Reassuring

Secondary Tones

- •

Trustworthy

- •

Professional

- •

Helpful

Tone Shifts

The tone is remarkably consistent. There are no jarring shifts; the voice remains reassuring and professional from the hero section to the product descriptions and proof points.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Erie Insurance provides comprehensive, fairly-priced protection delivered with superior, personalized service through a network of trusted local agents.

Value Proposition Components

- Component:

Personalized service via local agents

Clarity:Clear

Uniqueness:Unique

- Component:

High customer satisfaction and retention

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Comprehensive and customizable policies

Clarity:Clear

Uniqueness:Common

- Component:

Financial stability and trustworthiness

Clarity:Clear

Uniqueness:Common

Erie's messaging strategy successfully differentiates the brand by elevating the role of the independent agent as the primary value driver. While competitors often focus on speed, technology, or price, Erie centers its identity on the human element: 'Our agents are our difference.' This is powerfully substantiated by the 90% customer retention statistic, which serves as tangible proof of their service quality. This positioning effectively carves out a niche for consumers who prioritize guidance and relationships over a purely digital, self-service experience.

The messaging positions Erie as a premium service provider that competes on value and trust, not just price. It stands in direct contrast to direct-to-consumer models like GEICO or Progressive, which emphasize digital convenience and cost savings. By highlighting its consistently high J.D. Power rankings for customer and claims satisfaction, Erie frames itself as a reliable, high-touch alternative in a crowded and often commoditized market.

Audience Messaging

Target Personas

- Persona:

Relationship Seekers

Tailored Messages

- •

Our agents are our difference.

- •

service you can count on.

- •

13K+ The number of independent ERIE agents ready to help

Effectiveness:Effective

- Persona:

Value-Conscious Bundlers

Tailored Messages

Pair two or more insurance policies to save up to 25%

Explore our variety of policies - plus bundles and packages

Effectiveness:Effective

- Persona:

Risk-Averse Planners

Tailored Messages

- •

Enjoy peace of mind knowing you, your loved ones and your property are protected for the future.

- •

Our rating by A.M. Best

- •

Protect your loved ones from potentially devastating financial loss.

Effectiveness:Effective

Audience Pain Points Addressed

- •

The complexity and confusion of choosing the right insurance.

- •

Dealing with impersonal call centers during a stressful claim.

- •

The fear of being underinsured or having a claim denied.

- •

Worry about the financial stability of an insurer.

Audience Aspirations Addressed

- •

Achieving 'peace of mind' and financial security.

- •

Feeling supported by a real person who knows them.

- •

Protecting their family, home, and assets for the future.

- •

Making a smart, informed decision about insurance.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Peace of Mind / Security

Effectiveness:High

Examples

Enjoy peace of mind knowing you, your loved ones and your property are protected for the future.

Safeguard your business with a variety of policy types

- Appeal Type:

Trust / Reliability

Effectiveness:High

Examples

service you can count on.

Over 90% of our customers stay with ERIE year after year

Social Proof Elements

- Proof Type:

Customer Loyalty Stat

Impact:Strong

Example:Over 90% of our customers stay with ERIE year after year

- Proof Type:

Expert Endorsement

Impact:Moderate

Example:A+ Our rating by A.M. Best

- Proof Type:

Scale/Network Size

Impact:Moderate

Example:13K+ The number of independent ERIE agents ready to help

Trust Indicators

- •

A.M. Best A+ rating prominently displayed.

- •

High customer retention statistic (90%+).

- •

Explicitly mentioning the number of agents available.

- •

Company history since 1925 (from mission statement).

- •

Numerous J.D. Power awards for customer satisfaction.

Scarcity Urgency Tactics

None present, which is appropriate for the brand and industry. The messaging focuses on long-term stability and trust, not high-pressure sales tactics.

Calls To Action

Primary Ctas

- Text:

Get a quote

Location:Homepage Hero

Clarity:Clear

- Text:

Find an agency

Location:Agent Section

Clarity:Clear

The CTAs are effective and strategically placed. The dual primary CTAs ('Get a quote' and 'Find an agency') cater to two distinct user journeys: the user who is ready for a price comparison and the user who is sold on the agent-based model and wants to connect with a person. This dual approach aligns perfectly with their overall messaging strategy.

Messaging Gaps Analysis

Critical Gaps

Lack of customer storytelling. The 90% retention stat is powerful, but there are no testimonials, case studies, or stories that illustrate why customers are so loyal. Humanizing the 'service you can count on' promise with real examples is a major missed opportunity.

Limited explanation of the agent's value during claims. The site states agents are the difference but doesn't explicitly connect that to the most critical customer moment: a claim. Messaging could be stronger by explaining how an agent advocates for you during a stressful event.

Contradiction Points

No itemsUnderdeveloped Areas

The 'Why Erie?' narrative. While individual proof points are strong, they are presented as data points. A more cohesive narrative that weaves together the history, agent focus, and customer loyalty into a compelling 'Why Erie?' story is underdeveloped.

Competitive comparison. The messaging implies superiority over digital-first insurers but never explicitly states the benefits of their model versus competitors. Content that educates consumers on the pros and cons of different insurance models could be very effective.

Messaging Quality

Strengths

- •

Exceptional clarity and focus on the core value proposition of agent-led service.

- •

Powerful and credible use of data (90% retention, A+ rating) to build trust.

- •

Strong brand voice that is consistently reassuring, dependable, and human.

- •

Clear differentiation in a competitive market by leaning into a human-centric model.

Weaknesses

- •

Over-reliance on statistics at the expense of emotional storytelling.

- •

The message, while strong, can feel very traditional and may not fully capture the attention of younger, digitally-native audiences without more dynamic content.

- •

The value of the agent is stated but not vividly demonstrated through examples or scenarios.

Opportunities

- •

Develop a video content series featuring real agents and their clients to bring the 'agents are our difference' message to life.

- •

Create a dedicated section on the site for customer success stories, particularly focusing on complex claims handled with exceptional service.

- •

Launch a campaign educating consumers on the value of an independent agent, positioning Erie as a thought leader in the 'human-touch' insurance space.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Agent Section

Recommendation:Incorporate short, authentic video testimonials from both agents and customers. Replace the static '13K+ agents' number with a rotating feature of a real agent with a quote about their service philosophy.

Expected Impact:High

- Area:

Content Strategy

Recommendation:Create a blog/video series titled 'The Erie Difference' or 'When It Matters Most,' detailing real-life claim stories where a local agent's involvement was critical. Promote these stories across all channels.

Expected Impact:High

- Area:

Value Proposition Copy

Recommendation:Sharpen the copy to more directly connect the benefits of an agent to customer pain points. For example: 'When you have a claim, you call a person, not a call center. That's the Erie difference.'

Expected Impact:Medium

Quick Wins

- •

Add a compelling customer quote directly below the main 'Protection you need, service you can count on' headline to add immediate human proof.

- •

Change the sub-heading for the agent section to something more benefit-driven, like 'A Real Person on Your Side.'

- •

Prominently feature the J.D. Power #1 ranking for customer satisfaction near the other proof points.

Long Term Recommendations

Invest in building out agent micro-sites or profiles that tell their individual stories and showcase their community involvement, reinforcing the 'local' aspect of the brand promise.

Develop an educational content hub comparing different insurance models (e.g., agent vs. direct-to-consumer) to attract and inform shoppers early in their buying journey, positioning Erie as a trusted advisor.

Erie Insurance's strategic messaging is exceptionally clear, consistent, and well-differentiated. The brand has successfully built its entire communication strategy around a core, defensible value proposition: superior, human-powered service delivered by local, independent agents. This is a powerful position in an industry increasingly dominated by low-cost, digital-first competitors. The messaging architecture is logical, guiding users from a high-level promise of 'protection and service' to a tangible differentiator in 'our agents,' all backed by compelling quantitative proof points like the 90% retention rate and A+ A.M. Best rating.

The brand voice is consistently reassuring and dependable, effectively building trust with a target audience that values security and personal relationships. However, the primary weakness in Erie's messaging is its over-reliance on data and statements at the expense of storytelling. While the statistics are impressive, they lack the emotional resonance that comes from real human stories. The 'why' behind the 90% retention rate is the most powerful marketing asset Erie possesses, yet it remains untold on the site. The key to elevating their messaging from effective to truly compelling lies in bringing the 'service you can count on' promise to life through authentic agent and customer narratives. By showcasing—not just stating—the value of a human expert during life's most stressful moments, Erie can fortify its market position and create a deeper, more memorable brand connection.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Extraordinarily high customer retention rate, with over 90% of customers staying with ERIE year after year, as stated on their website.

- •

A+ (Superior) financial strength rating from A.M. Best, indicating a strong ability to meet policy obligations, which builds significant customer trust.

- •

Long-standing market presence since 1925, demonstrating a century of stability and successful operation.

- •

Consistently high rankings in J.D. Power customer satisfaction studies for auto and home insurance.

- •

Operates with a large network of over 13,000 independent agents, suggesting a robust and loyal distribution channel.

Improvement Areas

- •

Develop and market products tailored to younger, digitally-native demographics who may prefer self-service and have different coverage needs.

- •

Enhance the digital product experience to match the high-quality, high-touch service provided by agents.

- •

Introduce more flexible and usage-based insurance (UBI) products to compete with insurtech offerings.

Market Dynamics

Mid-single-digit growth (Approx. 6.8% projected for 2025 in the US P&C market).

Mature

Market Trends

- Trend:

Digital Transformation and Insurtech Adoption

Business Impact:Traditional agent-based models are being challenged by direct-to-consumer (D2C) competitors. Customers increasingly expect seamless digital experiences for quotes, policy management, and claims.

- Trend:

Use of AI and Advanced Analytics

Business Impact:Competitors are leveraging AI for dynamic pricing, personalized marketing, underwriting automation, and fraud detection, creating pressure to modernize core systems.

- Trend:

Changing Customer Expectations

Business Impact:Demand for personalization, transparency, and 24/7 self-service options is growing, potentially making the traditional agent model a point of friction for some segments.

- Trend:

Climate Change and Catastrophe Risk

Business Impact:Increased frequency and severity of weather-related events are impacting underwriting profitability and driving up premiums, especially in homeowners insurance.

Challenging but opportune. The mature market is highly competitive, but the slow pace of digital adoption by traditional players creates a significant opportunity for a well-trusted brand like Erie to innovate and capture new market segments by blending its service reputation with modern technology.

Business Model Scalability

Medium

The model has a significant variable cost component tied to agent commissions and support. While core back-office functions have scale, the primary distribution channel (independent agents) scales linearly with human capital, not exponentially like a digital D2C model.

Moderate. There is leverage in centralized underwriting, claims processing, and technology infrastructure. However, this is constrained by the high-touch, decentralized agent network which is costly to expand into new territories.

Scalability Constraints

- •

Dependence on recruiting, training, and managing a large independent agent network.

- •

Geographic expansion is slow and capital-intensive, requiring the establishment of new agent relationships in each new state.

- •

The business model is less effective at capturing the digitally-native customer segment that prefers self-service over intermediated sales.

Team Readiness

Likely strong in traditional insurance operations, risk management, and agent network management given the company's long history and financial stability. Potential gaps may exist in digital transformation, product-led growth, and agile methodologies.

Assumed to be a traditional, hierarchical structure common in incumbent insurers. This can slow down innovation and cross-functional collaboration required for rapid growth experiments.

Key Capability Gaps

- •

Digital Marketing and Customer Acquisition (especially performance marketing and SEO).

- •

Data Science and AI/ML for underwriting, pricing, and personalization.

- •

User Experience (UX) and Digital Product Management.

- •

Agile Development and DevOps for faster technology deployment.

Growth Engine

Acquisition Channels

- Channel:

Independent Agent Network

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip agents with better digital tools for lead management, quoting, and customer communication to enhance their efficiency and effectiveness in a digital-first world.

- Channel:

Referrals / Word-of-Mouth

Effectiveness:High

Optimization Potential:High

Recommendation:Formalize a digital referral program that rewards both agents and customers for successful referrals, amplifying the effects of the company's strong reputation.

- Channel:

Website / Organic Search

Effectiveness:Medium

Optimization Potential:High

Recommendation:Invest heavily in SEO, focusing on non-branded keywords for specific insurance products (e.g., 'best homeowners insurance in Pennsylvania'). The site currently functions as a validator and agent-finder, not a primary lead generation engine.

- Channel:

Content Marketing (Blog)

Effectiveness:Low

Optimization Potential:High

Recommendation:Develop a content strategy that targets specific customer personas and stages of the buying journey. Integrate clear calls-to-action (CTAs) within content to drive users to online quote tools or agent locators.

Customer Journey

The primary digital journey funnels users to 'Find an Agent', creating an online-to-offline process. The website lacks a fully-developed, direct-to-consumer (D2C) quoting and binding engine for most products.

Friction Points

- •

Lack of immediate, online bindable quotes for many insurance types, forcing a high-friction handoff to an agent.

- •

The 'Get a Quote' process requires users to leave the digital environment and wait for an agent to contact them, leading to potential drop-off.

- •

Mobile app is focused on existing customers (policy management, claims), not on acquisition.

Journey Enhancement Priorities

{'area': 'Online Quoting Funnel', 'recommendation': 'Develop and pilot a seamless, mobile-first D2C quote-and-bind experience for a simple product like renters insurance to test and optimize the digital journey.'}

{'area': 'Agent Handoff', 'recommendation': 'Implement a system for online appointment booking with agents directly from the website, reducing the friction of phone tag and email exchanges.'}

Retention Mechanisms

- Mechanism:

Agent Relationship

Effectiveness:High

Improvement Opportunity:Empower agents with CRM tools and data insights to proactively engage clients with personalized advice and coverage reviews, further strengthening the relationship.

- Mechanism:

Product Bundling

Effectiveness:High

Improvement Opportunity:Use data analytics to proactively identify and market bundling opportunities to existing single-policy customers, increasing policy density and customer lifetime value.

- Mechanism:

Brand Trust and Financial Stability

Effectiveness:High

Improvement Opportunity:More prominently feature customer testimonials and stories in digital marketing to translate the abstract concept of trust into tangible social proof.

Revenue Economics

Likely strong. The exceptionally high retention rate (>90%) suggests a very high Customer Lifetime Value (LTV). Customer Acquisition Cost (CAC) is likely tied to agent commissions, which is a predictable, though not highly scalable, model.

Undeterminable from public data, but presumed to be very healthy given the high retention. The key question is whether CAC can be lowered through more efficient digital channels.

High (in the traditional model). The company has demonstrated sustained profitability. The challenge is improving efficiency in emerging digital channels.

Optimization Recommendations

Invest in digital acquisition channels (SEO, PPC) to acquire customers at a potentially lower CAC than the agent model for simpler products.

Increase cross-selling and up-selling to the existing loyal customer base to maximize LTV without incurring additional acquisition costs.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Systems

Impact:High

Solution Approach:Adopt an API-first modernization strategy. Encapsulate legacy systems with modern APIs to enable faster development of digital front-end experiences and partnerships without a full rip-and-replace.

- Limitation:

Limited D2C E-commerce Capability

Impact:High

Solution Approach:Build or partner with an insurtech to launch a modern, cloud-native policy administration and sales platform, initially for a single product line or state.

Operational Bottlenecks

- Bottleneck:

Agent-Centric Processes

Growth Impact:Manual processes for quoting, binding, and servicing that rely on agent intervention slow down the customer experience and limit scalability.

Resolution Strategy:Automate routine tasks for both customers (self-service) and agents (digital toolkits) to free up human capacity for high-value advisory work.

- Bottleneck:

Geographic Expansion Process

Growth Impact:Entering new states is a slow process of regulatory approval and building an agent network from scratch.

Resolution Strategy:Pilot a D2C-first market entry strategy in a new state to establish a beachhead before making the larger investment in a physical agent network.

Market Penetration Challenges

- Challenge:

Intense Competition from D2C Insurers

Severity:Critical

Mitigation Strategy:Differentiate on service and trust ('The ERIE Difference') while achieving parity on digital convenience. Develop a hybrid model that offers the best of both worlds: digital ease and human advice.

- Challenge:

Limited Brand Awareness in Expansion Markets

Severity:Major

Mitigation Strategy:Launch targeted brand marketing and performance advertising campaigns in new geographies before and during agent network build-out to generate awareness and inbound leads.

- Challenge:

Appealing to Younger Demographics

Severity:Major

Mitigation Strategy:Create a sub-brand or a distinct product experience tailored to the needs and communication preferences of millennials and Gen Z, focusing on mobile-first interaction and transparent pricing.

Resource Limitations

Talent Gaps

- •

Growth Marketers

- •

Data Scientists / AI Engineers

- •

Digital Product Managers

- •

UX/UI Designers

Significant investment will be needed for technology modernization (core systems, data platforms) and marketing spend to build brand awareness in new channels and markets.

Infrastructure Needs

- •

Modern cloud-based data warehouse and analytics platform.

- •

Customer Data Platform (CDP) to create a unified view of the customer across agent and digital interactions.

- •

Marketing automation and CRM platform that serves both D2C and agent-led funnels.

Growth Opportunities

Market Expansion

- Expansion Vector:

Geographic Expansion

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Prioritize expansion into adjacent states to leverage existing brand recognition. Use a digital-first entry model to test the market before committing to a full agent network rollout. Erie currently operates in only 12 states and DC.

- Expansion Vector:

Demographic Expansion (Millennials & Gen Z)

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Launch a simplified, mobile-first product (e.g., renters insurance) with a fully digital journey. Use targeted social media and influencer marketing to reach this audience where they are.

Product Opportunities

- Opportunity:

Usage-Based Auto Insurance (Telematics)

Market Demand Evidence:Strong adoption and promotion by major competitors like Progressive (Snapshot) and State Farm (Drive Safe & Save).

Strategic Fit:Aligns with the brand promise of fair pricing and protection by rewarding safe driving behavior.

Development Recommendation:Partner with a proven telematics technology provider rather than building the hardware/software from scratch to accelerate time-to-market.

- Opportunity:

Embedded Insurance

Market Demand Evidence:Growing trend of offering insurance at the point of sale in other transactions (e.g., auto purchase, home mortgage application).

Strategic Fit:Creates a new, highly efficient distribution channel that leverages the trust of a partner brand.

Development Recommendation:Develop APIs to allow partners (e.g., auto dealerships, real estate platforms, mortgage lenders) to easily integrate Erie insurance quotes into their digital workflows.

- Opportunity:

Modern Small Business Insurance (BOP)

Market Demand Evidence:Explosion of small businesses and freelancers who need simple, digitally-purchasable business owner policies (BOP).

Strategic Fit:Leverages existing business insurance expertise but packages it for a modern, underserved digital audience.

Development Recommendation:Create a streamlined online application for specific small business niches (e.g., photographers, consultants) that can be completed in minutes.

Channel Diversification

- Channel:

Direct-to-Consumer (D2C) Digital Channel

Fit Assessment:Crucial for long-term growth and reaching new customer segments, but must be managed carefully to avoid alienating the existing agent network.

Implementation Strategy:Position the D2C channel as a 'front door' that handles simple risks, while referring complex needs to agents. Create a 'hybrid' model where customers can start online and finish with an agent, with attribution for both.

- Channel:

Comparison Websites / Aggregators

Fit Assessment:Good for volume, but can lead to price-shopping behavior that de-emphasizes Erie's service-based value proposition.

Implementation Strategy:Selectively partner with aggregators that allow for brand and feature differentiation, not just price. Use it as a targeted strategy for specific products or states.

Strategic Partnerships

- Partnership Type:

Insurtech Collaboration

Potential Partners

- •

Lemonade (for D2C platform tech)

- •

Hippo (for smart home integration)

- •

Cambridge Mobile Telematics (for UBI)

Expected Benefits:Accelerate technology development, acquire new capabilities, and learn from digitally-native innovators.

- Partnership Type:

Affinity Groups

Potential Partners

- •

University Alumni Associations

- •

Professional Organizations (e.g., for small business insurance)

- •

AARP

Expected Benefits:Access to large, targeted customer bases with a trusted endorsement, lowering customer acquisition costs.

Growth Strategy

North Star Metric

Number of Multi-Policy Households

This metric aligns with the core business model of building long-term, high-LTV relationships. It inherently measures both acquisition (new households) and retention/expansion (adding policies). Growth in this metric demonstrates success in both the agent and potential D2C channels.

Increase the percentage of new customers who bundle by 15% year-over-year.

Growth Model

Hybrid: Agent-Led, Digitally-Enabled

Key Drivers

- •

Agent Productivity (empowered by digital tools).

- •

Digital Lead Generation (fueling both agent and D2C funnels).

- •

Cross-Sell Rate (driven by data-driven recommendations).

- •

Customer Retention (maintaining the existing core strength).

Gradually shift from a purely agent-centric model to one where digital channels generate and nurture leads, handling simple transactions directly and seamlessly routing complex needs to the best-suited agent.

Prioritized Initiatives

- Initiative:

Launch a D2C Renters Insurance Pilot

Expected Impact:High

Implementation Effort:High

Timeframe:9-12 Months

First Steps:Assemble a cross-functional 'tiger team'. Select a single state for the pilot. Choose a technology partner for the policy administration system.

- Initiative:

Develop an 'Agent Digital Toolkit'

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:6-9 Months

First Steps:Survey agents to identify their biggest pain points and tool gaps. Develop a roadmap for a unified CRM, digital marketing assets, and communication platform for agents.

- Initiative:

Implement a Proactive Bundling Program

Expected Impact:High

Implementation Effort:Medium

Timeframe:4-6 Months

First Steps:Use data analytics to identify mono-line customers who are prime candidates for bundling. Launch an automated email and agent-led outreach campaign with personalized offers.

Experimentation Plan

High Leverage Tests

{'test': "A/B test website CTAs: 'Find an Agent' vs. 'Get an Instant Online Quote'.", 'hypothesis': "An instant quote CTA will generate more total leads, even if some don't complete the online journey."}

{'test': 'Test different landing page value propositions for younger vs. older demographics.', 'hypothesis': 'Younger audiences will respond better to messages of speed and convenience, while older audiences will prefer messages of trust and agent support.'}

Utilize a standard framework like AARRR (Acquisition, Activation, Retention, Referral, Revenue) but adapt it for both the agent and D2C funnels. Track metrics like Cost Per Quote, Quote-to-Bind Ratio, and Policies Per Household.

Establish a bi-weekly 'Growth Sprint' where new experiments are launched and results from previous tests are analyzed.

Growth Team

A centralized 'Digital Growth' team that works cross-functionally with IT, Marketing, and the agent-facing business units. The team should have a dedicated leader with P&L responsibility for the digital channel.

Key Roles

- •

Head of Digital Growth

- •

Digital Product Manager (for online quote/bind experience)

- •

Performance Marketing Manager (PPC/SEO)

- •

Data Analyst

Invest in training for existing marketing staff on digital analytics and growth marketing principles. Hire external talent with experience in scaling D2C brands (not necessarily from insurance) to bring in fresh perspectives.

Erie Insurance possesses an exceptionally strong growth foundation built on nearly a century of trust, financial stability (A+ rating), and an incredibly loyal customer base with a retention rate exceeding 90%. This high-touch, agent-centric model has created a powerful brand and a deep competitive moat based on service. However, this same model is also the primary barrier to scalable growth in the modern era. The reliance on a physical agent network makes expansion slow and costly, and the lack of a robust direct-to-consumer (D2C) channel leaves the company vulnerable to digitally-native competitors, especially among younger demographics who prioritize convenience and self-service.

The most significant growth opportunity lies in evolving the business model from being 'agent-centric' to 'customer-centric, agent-empowered.' This involves a strategic and deliberate investment in digital channels, not as a replacement for agents, but as a complementary and powerful engine for acquisition and efficiency. The immediate priority should be to develop and pilot a seamless D2C experience for a simple product like renters insurance. This will serve as a low-risk laboratory to build digital capabilities, understand online customer behavior, and optimize the digital journey.

Simultaneously, Erie must double down on its key differentiator: its agents. Equipping them with modern digital tools for lead management, marketing automation, and customer communication will enhance their productivity and allow them to focus on high-value advisory services where they excel. By creating a hybrid model—where simple transactions can be handled digitally, while complex needs are seamlessly routed to an empowered agent—Erie can leverage its core strength of service while meeting modern expectations for convenience. This strategy will unlock new markets, attract new demographics, and create a sustainable growth engine for the next century.

Legal Compliance

Erie Insurance provides a comprehensive 'Privacy Notice' accessible via the website footer. The policy is structured as an FAQ, addressing key questions about data collection, sharing, and protection. It clearly identifies the Erie Insurance Group companies covered by the notice and specifies the types of non-public personal information (NPI) collected, such as Social Security numbers, credit history, and claim history. The notice is designed to comply with the federal Gramm-Leach-Bliley Act (GLBA), detailing reasons for sharing data (e.g., everyday business, marketing, affiliates) and explaining whether customers can limit this sharing. An explicit 'opt-out' procedure is provided for limiting certain data sharing with affiliates and non-affiliates, with a dedicated webpage for submission. The policy lacks specific language addressing the California Consumer Privacy Act (CCPA)/California Privacy Rights Act (CPRA), which is a notable gap given the evolving application of these laws to insurance data not covered by GLBA. It also does not explicitly mention GDPR, which is appropriate as their business is focused within the United States.

A 'Terms of Use' document is accessible in the website footer. The terms are straightforward and primarily govern the use of the website and its content. It includes standard clauses on intellectual property, disclaimers of warranties, and limitations of liability. The language is clear and legally standard for a corporate website. It defines the user's responsibilities and the company's rights regarding the site's content and services. The enforceability appears standard, but like any online agreement, it is contingent on proper user notification and acceptance, which is implicitly handled by website usage. A specific 'eSignature Consent' is also mentioned, likely applicable when customers purchase policies online, indicating a process for creating legally binding digital agreements.

Upon visiting the website, a cookie consent banner appears at the bottom of the screen. The banner provides a brief notice about the use of cookies and links to the Privacy Notice. It offers two options: 'Accept All' and 'Reject All'. This binary choice is good for simplicity but lacks the granular control (e.g., managing preferences for different cookie categories like analytics or marketing) recommended by modern privacy frameworks. A more robust mechanism would allow users to selectively opt-in to non-essential cookie categories. The current implementation is a good first step but could be improved to offer greater user control and transparency.

Erie Insurance's data protection posture is heavily influenced by its obligations as a financial institution under the GLBA. The Privacy Notice explicitly states that the company uses security measures that comply with federal law, including 'computer safeguards and secured files and buildings,' to protect personal information from unauthorized access. This aligns with the requirements of the GLBA Safeguards Rule, which mandates a written information security plan. The use of reCAPTCHA on forms is another visible technical safeguard to prevent automated abuse. The company's commitment to protecting NPI is a central theme of its privacy communications, which is crucial for maintaining customer trust in the insurance sector.

The website footer contains a dedicated 'Accessibility' link leading to a comprehensive Accessibility Statement. The statement affirms Erie's commitment to digital accessibility and its efforts to conform to the Web Content Accessibility Guidelines (WCAG) 2.1 Level AA. This is the recognized standard for ADA compliance in digital spaces. The statement provides a contact phone number and email address for users who encounter accessibility barriers, which is a best practice. A quick manual check shows the use of some accessibility features, such as descriptive link text. The public commitment and provision of contact information represent a strong and legally sound position on accessibility, mitigating risk from ADA-related lawsuits which are common in the financial services industry.

As an insurer operating in 12 states and the District of Columbia, Erie Insurance is subject to a complex web of state and federal regulations.

1. State Insurance Regulations: The primary regulatory framework is at the state level, governed by each state's Department of Insurance. This includes rules on advertising, agent licensing, policy forms, and unfair trade practices. All website content, especially marketing claims and quote processes, must comply with the specific laws of each state they operate in. Disclaimers about product availability by state (e.g., 'Erie Family Life insurance products are not available in New York') are present and necessary for compliance.

2. Gramm-Leach-Bliley Act (GLBA): This is the cornerstone of their data privacy compliance. The GLBA requires financial institutions, including insurers, to provide clear notices on information-sharing policies and to safeguard customer data. Their Privacy Notice is clearly structured to meet GLBA's Financial Privacy Rule requirements.

3. NAIC Model Laws: The National Association of Insurance Commissioners (NAIC) creates model regulations that many states adopt, covering advertising, data security, and more. Adherence to NAIC models helps ensure multistate compliance. Website advertising must be truthful, not misleading, and clearly identify the insurer.

Compliance Gaps

- •

The Privacy Notice does not contain a specific section addressing the rights of California residents under the CCPA/CPRA, such as the right to know, delete, and correct personal information not covered by the GLBA exemption.

- •

The cookie consent mechanism lacks granular controls, only offering 'Accept All' or 'Reject All', which is less compliant with user-choice expectations under laws like the CCPA/CPRA.

- •

Lack of a centralized 'Licensing Information' page that clearly lists the states where specific Erie entities are licensed to do business and their corresponding license numbers. This information is critical for regulatory transparency.

Compliance Strengths

- •

Strong compliance with the Gramm-Leach-Bliley Act (GLBA), with a detailed and accessible Privacy Notice tailored to its requirements.

- •