eScore

everestglobal.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Everest Global's digital presence is strong for branded searches but weak in capturing non-branded, high-intent queries, indicating poor search intent alignment for new customer acquisition. Its content authority is underdeveloped due to a significant gap in thought leadership compared to competitors, functioning more as a digital brochure than a strategic asset. While the company has a strong global footprint, its digital content is not deeply localized to maximize geographic reach.

The website effectively serves its existing client and partner base with a clear, professional presentation of its products and global structure.

Launch a 'Global Risk Insights' hub with proprietary research and analysis on emerging risks to build content authority and attract new, high-value B2B relationships early in their research phase.

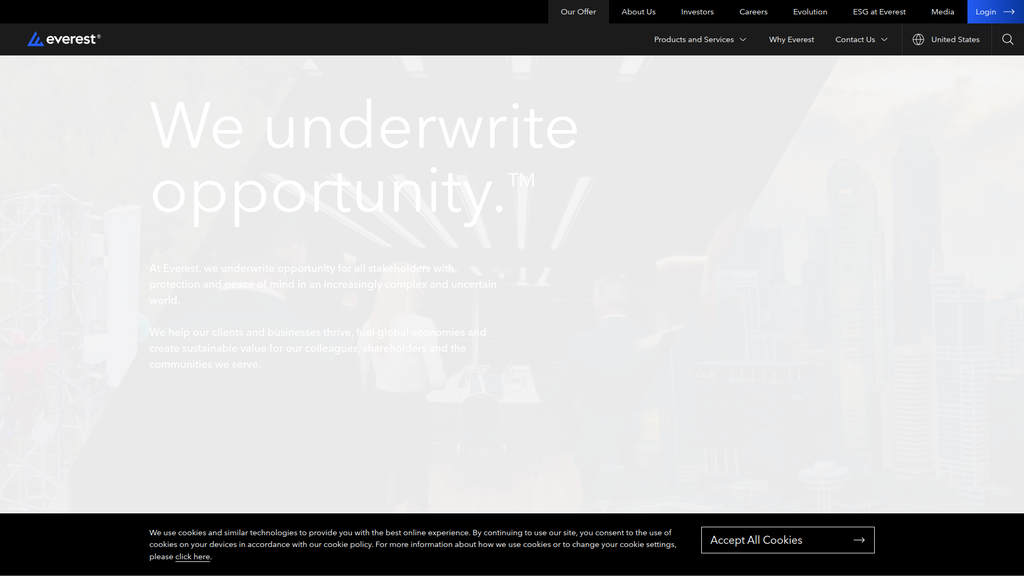

The brand messaging is highly consistent and professional, with a clear hierarchy that communicates stability and scale. However, the core value proposition, 'We underwrite opportunity.TM', remains abstract and is not substantiated with customer evidence or case studies. While messaging is tailored for key personas like brokers, weak calls-to-action (text links instead of buttons) reduce conversion effectiveness.

The brand voice is consistently authoritative and professional, effectively reinforcing its position as a stable, global leader in the financial industry.

Develop a library of client case studies (even if anonymized) that bring the 'underwrite opportunity' tagline to life by demonstrating tangible client outcomes and successes.

The website provides a clean user experience with logical information architecture and good mobile responsiveness. However, it suffers from significant friction points at critical conversion moments, using understated text links for key actions like 'Contact Us' instead of prominent buttons. The absence of a formal Accessibility Statement indicates a compliance and user experience gap that could limit market reach and create legal risk.

The information architecture is logical and intuitive, allowing sophisticated B2B users to efficiently navigate complex product offerings.

Implement a clear visual hierarchy for Calls-to-Action (CTAs), converting primary conversion points like 'Contact via email' into prominent, solid-colored buttons to increase visibility and drive leads.

Everest's underlying credibility is exceptionally strong, built on a 50-year history and A+ financial ratings. However, the website does a poor job of showcasing these trust signals, failing to prominently display ratings or provide easy access to state licensing information. A critical weakness is the complete lack of customer success evidence, such as testimonials or case studies, which forces reliance on asserted claims rather than demonstrated proof.

The company's A+ financial strength ratings from A.M. Best and S&P are a powerful, objective indicator of credibility and stability in the risk-averse insurance market.

Create a dedicated 'Regulatory & Licensing' page and prominently display financial rating agency logos in the website footer or an 'About Us' section to immediately build trust and transparency.

The company's competitive moat is highly sustainable, anchored in its disciplined underwriting culture and deep, long-standing broker relationships, which are difficult for competitors to replicate. This is reinforced by a diversified business model spanning both insurance and reinsurance. However, the advantage is weakened by a lag in innovation, with a noted need to invest in data analytics and technology to keep pace with market leaders and agile insurtechs.

The deeply embedded culture of disciplined underwriting, honed over 50 years, provides a highly sustainable advantage that leads to long-term profitability and stability.

Establish a formal program for partnering with or investing in insurtech firms to accelerate the adoption of new technologies for underwriting, claims, and distribution.

The business model has high operational leverage, allowing it to absorb significant premium volume with marginal cost increases. Strong unit economics are driven by a focus on profitable underwriting rather than growth at any cost. However, scalability is constrained by operational bottlenecks, including a reliance on manual underwriting for complex risks and legacy technology systems that hinder agility.

The dual-engine business model (Insurance and Reinsurance) provides diversified and scalable revenue streams, supported by a strong capital base.

Invest in developing an AI-augmented underwriting workbench to increase the speed and accuracy of processing complex risks, thereby breaking a key operational bottleneck to growth.

Everest's business model is exceptionally coherent and robust, centered on the clear, strategic focus of disciplined underwriting. The revenue model is well-diversified across insurance, reinsurance, and investment income, creating resilience. The value proposition of stability and expertise is perfectly aligned with the needs of its risk-averse B2B target market, particularly in a volatile economic environment.

The strategic focus on disciplined underwriting and capital management is a clear, guiding principle that ensures long-term stability and profitability, aligning the interests of clients, partners, and shareholders.

Accelerate resource allocation toward digital transformation and data analytics to ensure the traditional, stability-focused model evolves to compete in a future defined by AI and emerging risks.

As a top-10 global player with strong financial ratings, Everest commands significant market presence and pricing power, particularly in a 'flight-to-quality' market. However, its market influence is severely limited by its weakness in thought leadership, where it lags far behind competitors who shape industry conversations. Furthermore, a high dependency on the broker channel for distribution creates a concentration risk and reduces partner leverage.

The company's strong reputation for financial stability and disciplined underwriting gives it significant pricing power and makes it a preferred partner in hardening markets.

Mitigate broker dependency by developing digital-direct channels for specific, standardized SME products and investing in thought leadership to build a brand that pulls clients in directly.

Business Overview

Business Classification

B2B Financial Services

B2B2C (via brokers and other intermediaries)

Financial Services

Sub Verticals

- •

Reinsurance

- •

Property & Casualty Insurance

- •

Specialty Insurance

- •

Accident & Health Insurance

Mature

Maturity Indicators

- •

Approximately 50-year operating history, founded in 1973.

- •

Established global presence with subsidiaries in the U.S., Europe, Bermuda, and Asia.

- •

Highly diversified and comprehensive product portfolio across both reinsurance and insurance segments.

- •

Strong financial strength ratings from major agencies (A+ from A.M. Best and S&P).

- •

Consistent focus on disciplined underwriting and capital management as a core tenet of its strategy.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Reinsurance Premiums

Description:Premiums collected from other insurance companies (cedents) in exchange for assuming a portion of their risk portfolio. This includes property, casualty, and specialty lines. This is the larger of the two primary business segments.

Estimated Importance:Primary

Customer Segment:Primary Insurance Carriers

Estimated Margin:Medium

- Stream Name:

Insurance Premiums

Description:Premiums collected directly from businesses and other entities for a wide range of property, casualty, and specialty insurance products, such as Accident & Health coverage.

Estimated Importance:Primary

Customer Segment:Large Corporations, SMEs (via partners)

Estimated Margin:Medium

- Stream Name:

Net Investment Income

Description:Income generated by investing the 'float,' which consists of premiums collected that have not yet been paid out as claims. This is a critical source of profitability for the company.

Estimated Importance:Secondary

Customer Segment:N/A

Estimated Margin:High

Recurring Revenue Components

Policy renewals for insurance contracts

Treaty renewals for reinsurance contracts

Pricing Strategy

Actuarial-Based Underwriting

Premium

Opaque

Pricing Psychology

- •

Authority (leveraging 50-year history and strong financial ratings)

- •

Value-Based Pricing (solutions for complex, high-stakes risks)

- •

Social Proof (highlighting status as a 'preferred partner' in the market)

Monetization Assessment

Strengths

- •

Highly diversified revenue from two core segments (Insurance and Reinsurance) and investment income.

- •

Strong brand reputation and financial stability support premium pricing and a 'flight to quality' in uncertain markets.

- •

Recurring revenue from a high percentage of policy and treaty renewals.

Weaknesses

- •

Profitability is highly susceptible to high-severity, low-frequency catastrophic events, which are increasing due to climate change.

- •

Investment income is sensitive to interest rate fluctuations and financial market volatility.

- •

Exposure to 'social inflation' in casualty lines, which drives up claim costs unexpectedly.

Opportunities

- •

Develop and scale new products for emerging risks like cybersecurity, climate liability, and parametric insurance.

- •

Leverage data analytics and AI for more sophisticated underwriting, risk modeling, and operational efficiency.

- •

Expand presence in high-growth emerging markets.

Threats

- •

Increasing frequency and severity of natural catastrophes straining capital and impacting underwriting results.

- •

Intense competition from other global reinsurers like Munich Re and Swiss Re, and insurance giants like Chubb and AIG.

- •

Disruption from Insurtech startups that leverage technology to create more efficient underwriting or distribution models.

Market Positioning

Quality, Stability, and Expertise Leadership

Significant Global Player

Target Segments

- Segment Name:

Primary Insurance Carriers

Description:Global, national, and regional insurance companies seeking to cede risk to manage their own capital, reduce volatility, and protect against catastrophic losses.

Demographic Factors

Varying sizes, from large multinational carriers to smaller regional insurers.

Psychographic Factors

- •

Risk-averse

- •

Value financial strength and long-term stability in partners

- •

Seek underwriting expertise and claims-paying reliability

Behavioral Factors

Engage in long-term relationships and treaty-based agreements

Procure services through specialized reinsurance brokers

Pain Points

- •

Managing exposure to catastrophic events

- •

Optimizing capital allocation under regulatory frameworks (e.g., Solvency II)

- •

Controlling earnings volatility

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Large Corporations & Major Accounts

Description:Multinational corporations and large domestic companies with complex, large-scale risks requiring sophisticated, customized insurance solutions.

Demographic Factors

- •

Fortune 1000 or equivalent size

- •

Operations in multiple geographies

- •

High-risk industries (e.g., energy, aviation, marine)

Psychographic Factors

Sophisticated buyers with in-house risk management teams

Value global service capabilities and financial strength of the insurer

Behavioral Factors

Purchase insurance through major global brokers (e.g., Marsh, Aon)

Require high liability limits and specialized coverage

Pain Points

- •

Managing emerging risks like cyber threats and supply chain disruption

- •

Ensuring consistent global coverage and compliance

- •

Securing sufficient capacity for large or unique risks

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

SMEs (via Intermediaries)

Description:Small-to-medium enterprises that access Everest's products through a network of brokers, Managing General Agents (MGAs), and other strategic partners.

Demographic Factors

Wide range of industries and revenue sizes

Psychographic Factors

Often lack dedicated risk management resources

Value ease of doing business and responsive service

Behavioral Factors

Rely heavily on the advice of their broker or agent

Purchase standardized 'program' business or specialty products

Pain Points

- •

Finding affordable, comprehensive coverage for their specific risks

- •

Navigating a complex claims process

- •

Accessing specialized expertise

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Financial Strength and Stability

Strength:Strong

Sustainability:Sustainable

- Factor:

Disciplined Underwriting Expertise

Strength:Strong

Sustainability:Sustainable

- Factor:

Diversified Global Platform (Insurance & Reinsurance)

Strength:Moderate

Sustainability:Sustainable

Value Proposition

Everest is a global underwriting leader providing best-in-class property, casualty, and specialty reinsurance and insurance solutions, backed by a 50-year track record of disciplined underwriting and superior financial strength to deliver protection and peace of mind in a complex world.

Excellent

Key Benefits

- Benefit:

Superior Financial Strength & Capitalization

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

A+ ratings from S&P and A.M. Best.

Large capital base ($13.9B shareholders' equity as of year-end 2024).

- Benefit:

Deep Underwriting and Risk Management Expertise

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

50-year track record of disciplined underwriting.

Broad portfolio of complex and specialty risk products.

- Benefit:

Global Reach with Local Market Knowledge

Importance:Important

Differentiation:Somewhat unique

Proof Elements

Operations in key markets across North America, Europe, and Asia.

Ability to serve clients in over 115 countries.

- Benefit:

Responsive and Efficient Claims Handling

Importance:Critical

Differentiation:Common

Proof Elements

Dedicated claims section on the website promising speed and efficiency.

Unique Selling Points

- Usp:

A dual-engine business model combining a top-tier global reinsurance franchise with a growing, diversified specialty insurance platform.

Sustainability:Long-term

Defensibility:Strong

- Usp:

A long-standing reputation for financial prudence and disciplined risk-taking, which attracts clients seeking stability in a volatile market.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

Volatility of Financial Results

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Exposure to Catastrophic or Complex Risks

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Need for a Financially Secure Counterparty

Severity:Major

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition of financial strength, stability, and expertise is perfectly aligned with the primary needs of the insurance and reinsurance markets, particularly in a landscape of increasing risk complexity and economic uncertainty.

High

Target clients (other insurers and large corporations) are sophisticated buyers who prioritize financial ratings, long-term reliability, and deep expertise over price, making Everest's value proposition highly resonant.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Reinsurance Brokers (e.g., Aon, Guy Carpenter)

- •

Retail & Wholesale Insurance Brokers (e.g., Marsh)

- •

Managing General Agents (MGAs)

- •

Strategic partners (banks, technology providers)

Key Activities

- •

Risk Assessment & Underwriting

- •

Claims Adjudication & Management

- •

Investment Portfolio Management

- •

Capital Management & Allocation

- •

Broker & Client Relationship Management

Key Resources

- •

Substantial Capital Base (Balance Sheet)

- •

Expert Underwriting & Actuarial Talent

- •

Global Operating Licenses & Regulatory Compliance

- •

Brand Reputation & Strong Financial Ratings

Cost Structure

- •

Payment of Claims (Loss and Loss Adjustment Expenses)

- •

Commissions to Brokers & Agents (Acquisition Costs)

- •

Salaries & Employee Benefits

- •

Technology & Data Infrastructure

- •

Regulatory & Compliance Costs

Swot Analysis

Strengths

- •

Strong brand recognition and reputation built over 50 years.

- •

Diversified business across reinsurance and insurance segments and multiple geographic regions.

- •

Superior financial strength and a robust balance sheet.

- •

Deep, specialized expertise in underwriting complex risks.

Weaknesses

- •

High dependency on intermediaries (brokers) for distribution, with the largest broker accounting for a significant portion of premiums.

- •

Potential for legacy systems and processes to hinder agility compared to newer Insurtech competitors.

- •

Profitability can be highly volatile due to catastrophic events.

Opportunities

- •

Capitalize on the 'flight to quality' as clients seek more stable partners in a volatile market.

- •

Invest in data analytics, AI, and machine learning to create a competitive advantage in risk selection and pricing.

- •

Expand product offerings for emerging risks such as climate change and cyber threats.

- •

Strategic acquisitions or partnerships with Insurtech firms to accelerate digital transformation.

Threats

- •

Increased frequency and severity of natural catastrophes due to climate change.

- •

Sustained economic and social inflation driving up claims costs.

- •

Intense competition from a concentrated number of large, well-capitalized global players.

- •

Potential for capital market volatility to negatively impact the investment portfolio.

Recommendations

Priority Improvements

- Area:

Digital and Analytical Transformation

Recommendation:Accelerate investment in a unified data platform and advanced analytics (AI/ML) to enhance underwriting precision, automate claims processing, and provide predictive risk insights. This will improve risk selection and operational efficiency.

Expected Impact:High

- Area:

Distribution Channel Optimization

Recommendation:Develop a digital portal and API capabilities for brokers and MGAs to streamline the submission, quoting, and binding process. This enhances ease of doing business and strengthens partnerships.

Expected Impact:Medium

- Area:

Talent Development for Emerging Risks

Recommendation:Invest in training and hiring talent with expertise in non-traditional areas like data science, cybersecurity, and climate modeling to build underwriting capabilities for the next generation of risks.

Expected Impact:Medium

Business Model Innovation

- •

Develop a 'Risk-as-a-Service' (RaaS) offering, providing access to Everest's proprietary risk models, data, and underwriting expertise to smaller insurers or MGAs on a subscription or fee basis.

- •

Launch a corporate venture arm to invest in and partner with promising Insurtech startups, creating an ecosystem of innovation and gaining early access to disruptive technologies.

- •

Expand the use of alternative risk transfer solutions, such as parametric insurance products, which offer faster payouts based on predefined event triggers (e.g., hurricane wind speed) rather than lengthy loss adjustments.

Revenue Diversification

- •

Grow fee-based income by offering unbundled risk management and advisory services to large corporate clients.

- •

Further expand into less catastrophe-exposed specialty lines to reduce earnings volatility.

- •

Partner with technology companies to embed insurance products into their platforms and ecosystems, creating new distribution channels.

Everest Global operates a robust and mature business model, firmly positioned as a leader in the global insurance and reinsurance industry. Its core strengths—a formidable balance sheet, disciplined underwriting culture, and a diversified portfolio—create a sustainable competitive advantage and a powerful value proposition centered on stability and expertise. The business model is well-aligned with current market demands, particularly the 'flight to quality' in an increasingly risky world. However, the primary strategic challenge lies in evolving this traditional, stability-focused model for a future defined by rapid technological change and escalating climate-related risk. Future success will be determined by the company's ability to augment its traditional strengths with digital agility and analytical prowess. Strategic transformation should focus on leveraging technology to create a more dynamic, data-driven underwriting and claims process, innovating with new products for emerging risks, and optimizing distribution partnerships. By embracing this evolution, Everest can enhance its operational efficiency, defend against both traditional and Insurtech competitors, and solidify its position as a forward-looking leader in risk management for the next fifty years.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

Extreme Capital Requirements

Impact:High

- Barrier:

Regulatory Compliance and Licensing

Impact:High

- Barrier:

Underwriting Expertise and Data

Impact:High

- Barrier:

Broker and Client Relationships

Impact:High

- Barrier:

Brand Reputation and Financial Strength Ratings

Impact:High

Industry Trends

- Trend:

Climate Change and Increased Catastrophe (CAT) Losses

Impact On Business:Increases demand for reinsurance but also elevates risk, volatility, and the need for sophisticated modeling. This pressures underwriting profitability.

Timeline:Immediate

- Trend:

Growth of Alternative Capital (Insurance-Linked Securities - ILS)

Impact On Business:ILS, especially catastrophe bonds, represent a major competitive force for property-catastrophe reinsurance, potentially compressing margins. This creates both a competitive threat and an opportunity to sponsor ILS or manage third-party capital.

Timeline:Immediate

- Trend:

Digitalization and AI in Underwriting and Claims

Impact On Business:Leveraging AI and big data can create a competitive advantage through more accurate pricing, better risk selection, and operational efficiency. Lagging in this area is a significant threat.

Timeline:Near-term

- Trend:

Rising Social and Economic Inflation

Impact On Business:Increases claims costs, particularly in long-tail casualty lines, making reserving and pricing more challenging and potentially eroding profitability.

Timeline:Immediate

- Trend:

Focus on Specialty Lines

Impact On Business:There is a strategic shift toward highly specialized, technical, and profitable niches (e.g., cyber, sports disability, energy) where deep expertise can command higher margins.

Timeline:Near-term

Direct Competitors

- →

Munich Re

Market Share Estimate:Top 2 Global Reinsurer

Target Audience Overlap:High

Competitive Positioning:Global market leader known for its vast balance sheet, immense data and research capabilities (NatCatSERVICE), and innovative solutions in specialty and emerging risks like cyber.

Strengths

- •

Unmatched financial strength and excellent credit ratings.

- •

Superior data analytics, risk modeling, and R&D capabilities.

- •

Highly diversified across geographies and lines of business (reinsurance, primary insurance via ERGO, and services).

- •

Strong brand reputation and long-standing client relationships.

Weaknesses

- •

Massive scale can lead to slower decision-making compared to smaller rivals.

- •

Exposure to large, complex, and volatile global catastrophe events.

- •

Primary insurance arm (ERGO) can be capital-intensive and has historically diluted overall returns.

Differentiators

- •

Proprietary risk assessment tools and knowledge leadership.

- •

Ability to underwrite the largest and most complex risks in the market.

- •

Integrated model of primary and reinsurance.

- →

Swiss Re

Market Share Estimate:Top 2 Global Reinsurer

Target Audience Overlap:High

Competitive Positioning:A premier global reinsurer positioning itself as a knowledge and risk transfer leader, with a strong focus on research (Swiss Re Institute) and making the world more resilient.

Strengths

- •

Leading market position and powerful global brand.

- •

Strong focus on thought leadership and data-driven insights.

- •

Diversified portfolio including P&C and Life & Health reinsurance, and corporate solutions (Corso).

- •

Excellent financial strength and capitalization.

Weaknesses

- •

Significant exposure to natural catastrophe volatility.

- •

Like other giants, can be perceived as less agile than smaller competitors.

- •

Subject to complex global regulatory environments.

Differentiators

- •

Swiss Re Institute provides market-leading research and analysis.

- •

Strong focus on sustainability and climate risk solutions.

- •

Innovative risk transfer solutions and long-term partnerships.

- →

Chubb Limited

Market Share Estimate:Top-tier Global P&C Insurer

Target Audience Overlap:Medium

Competitive Positioning:A global leader in property & casualty insurance, particularly in commercial and specialty lines, known for its underwriting discipline, exceptional claims service, and focus on high-net-worth personal lines.

Strengths

- •

World-class underwriting expertise and discipline.

- •

Strong brand reputation for quality, service, and claims handling.

- •

Highly diversified product portfolio, including significant specialty and A&H lines that overlap with Everest.

- •

Vast global presence and distribution network.

Weaknesses

- •

Less focused on reinsurance than pure-play reinsurers.

- •

Can be more expensive (premium pricing) due to its focus on quality and service.

- •

Faces intense competition from both large global insurers and nimble insurtechs.

Differentiators

- •

Superior claims service is a core tenet of their brand promise.

- •

Deep expertise in specialty commercial lines (e.g., cyber, financial lines).

- •

Strong position in the high-net-worth personal insurance market.

- →

AXA XL

Market Share Estimate:Major Global P&C and Specialty Insurer/Reinsurer

Target Audience Overlap:High

Competitive Positioning:The P&C and specialty risk division of AXA, focusing on large and complex risks for mid-sized to multinational corporations and reinsurance.

Strengths

- •

Backed by the financial strength of the global AXA Group.

- •

Strong position in specialty lines like professional liability, cyber, and fine art.

- •

Global network and ability to service multinational clients.

- •

Offers both insurance and reinsurance solutions.

Weaknesses

- •

Has undergone significant integration and restructuring post-acquisition of XL Catlin, which can create internal challenges.

- •

Profitability has been volatile in the past, particularly due to catastrophe losses.

- •

May face channel conflicts between its insurance and reinsurance operations.

Differentiators

- •

Focus on complex, multinational risk solutions.

- •

Strong data and analytics capabilities, including risk consulting services.

- •

Broad appetite across a wide range of specialty products.

Indirect Competitors

- →

Insurance-Linked Securities (ILS) Funds

Description:Investment funds that allow institutional investors (pension funds, hedge funds) to invest in insurance-related risks, primarily through catastrophe bonds and collateralized reinsurance. They provide alternative capital to the reinsurance market.

Threat Level:High

Potential For Direct Competition:They are already direct competitors in the property catastrophe reinsurance space, offering capacity that directly competes with traditional reinsurers' balance sheets.

- →

Insurtech MGAs and Platforms

Description:Technology-first companies that use AI, data analytics, and digital platforms to underwrite and distribute insurance products with greater efficiency. While many focus on personal lines, the model is being applied to specialty commercial lines, disrupting traditional distribution.

Threat Level:Medium

Potential For Direct Competition:High. While many partner with reinsurers today for capital, successful tech-driven underwriters could eventually retain more risk or build their own capital structures, reducing their reliance on traditional reinsurers.

- →

Berkshire Hathaway (General Re & National Indemnity)

Description:While a direct competitor, its unique structure as a capital-rich conglomerate allows it to underwrite massive, unique risks (e.g., retroactive reinsurance) that others cannot. It competes indirectly by absorbing market risks in ways that fall outside the typical treaty reinsurance cycle.

Threat Level:High

Potential For Direct Competition:Is already a major direct competitor, but its indirect threat comes from its ability to deploy massive capital opportunistically, fundamentally altering market pricing and capacity dynamics after major events.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Disciplined Underwriting Culture

Sustainability Assessment:Highly sustainable. A strong underwriting culture is deeply embedded and difficult to replicate, leading to consistently better-than-average loss ratios and long-term profitability.

Competitor Replication Difficulty:Hard

- Advantage:

Strong Broker and Ceding Company Relationships

Sustainability Assessment:Sustainable with continued investment. Deep, trust-based relationships are a significant moat in the intermediated reinsurance market.

Competitor Replication Difficulty:Medium

- Advantage:

Diversified Portfolio (Insurance & Reinsurance)

Sustainability Assessment:Highly sustainable. A balanced book across different lines and types of business (insurance vs. reinsurance) provides resilience against market cycles in any single segment.

Competitor Replication Difficulty:Medium

- Advantage:

Strong Financial Strength Ratings (A+)

Sustainability Assessment:Sustainable, but requires constant strong performance. High ratings are essential for credibility and are a prerequisite to compete for top-tier business.

Competitor Replication Difficulty:Hard

Temporary Advantages

{'advantage': 'Favorable Pricing in Specific Hardening Market Segments', 'estimated_duration': '12-24 months. Market pricing is cyclical; advantages gained during a hard market tend to erode as new capacity enters and softens rates. '}

Disadvantages

- Disadvantage:

Scale and Capital Base Relative to Giants

Impact:Major

Addressability:Difficult

- Disadvantage:

Brand Recognition Outside the Industry

Impact:Minor

Addressability:Moderately

- Disadvantage:

Concentration in Broker Distribution Channel

Impact:Major

Addressability:Moderately

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted digital marketing campaigns highlighting underwriting expertise in high-growth specialty niches (e.g., pro sports, A&H).

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Host broker-exclusive webinars on emerging risks (e.g., AI liability, parametric triggers for climate events) to reinforce thought leadership.

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Invest significantly in a proprietary data analytics platform to enhance risk selection and pricing models, aiming to close the gap with larger competitors.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Form strategic partnerships with select insurtech firms to gain access to new distribution channels and underwriting technologies.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Expand the global footprint in targeted emerging markets where competition is less saturated and growth potential is high.

Expected Impact:High

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Develop an in-house or partnered alternative capital management platform to offer ILS products, directly competing with ILS funds and capturing management fees.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Consider a strategic acquisition of a specialty insurer or a technology firm to gain market share in a key growth area or acquire critical tech capabilities.

Expected Impact:High

Implementation Difficulty:Difficult

Position Everest as the 'Premier Specialist Underwriter': more agile and responsive than the giants (Munich Re, Swiss Re) but with deeper expertise and a stronger balance sheet than smaller niche players. Emphasize empowerment, autonomy, and direct access to decision-makers as a key differentiator for brokers.

Differentiate through 'Underwriting Excellence and Broker Centricity'. Focus on superior risk selection in complex specialty lines, faster quote-to-bind times, and providing unparalleled service and support to the broker channel. This contrasts with the massive, potentially slower giants and the tech-focused but less experienced insurtechs.

Whitespace Opportunities

- Opportunity:

Develop Parametric Insurance/Reinsurance for Non-CAT Climate Risks

Competitive Gap:Many competitors focus on traditional indemnity coverage for named perils (hurricanes, earthquakes). There is a growing demand for parametric products covering secondary perils like drought, extreme heat, or excessive rainfall, which are underserved.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Reinsurance for Emerging Technology Risks

Competitive Gap:Provide reinsurance capacity and expertise for risks associated with AI liability, quantum computing failures, and biotech. While larger players are in this space, deep specialization can create a defensible niche.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Offer a 'Digital-First' Broker Platform

Competitive Gap:Many legacy reinsurers have clunky, outdated systems for brokers. A modern, API-driven platform for submissions, quoting, and claims could significantly improve the broker experience and create stickiness.

Feasibility:Medium

Potential Impact:Medium

Comprehensive Competitive Landscape Analysis: Everest Global

Everest Global operates within the mature and highly competitive global insurance and reinsurance industry. The market is moderately concentrated at the top, with giants like Munich Re and Swiss Re commanding significant market share and influence. Barriers to entry are exceptionally high, predicated on immense capital reserves, stringent regulatory hurdles, deep underwriting expertise, and long-standing broker relationships, which protects established players like Everest from new startup threats.

Direct Competition:

Everest is a formidable player but is out-scaled by the top-tier global reinsurers, Munich Re and Swiss Re. These competitors differentiate through massive balance sheets and extensive investment in proprietary data, analytics, and thought leadership. On the specialty insurance side, Everest competes with underwriting-focused powerhouses like Chubb and AXA XL, which are known for their deep expertise in complex commercial risks and superior claims handling. Everest's core competitive advantage lies in its disciplined underwriting culture, a 50-year track record of profitability, and strong, responsive relationships within the broker community. It positions itself as a more agile and accessible partner than the market behemoths.

Indirect Competition and Disruptors:

The most significant indirect threat comes from the alternative capital market, specifically Insurance-Linked Securities (ILS) funds. These funds provide collateralized reinsurance capacity, primarily for property catastrophe risk, which directly competes with Everest's traditional offerings and can suppress pricing. A secondary, yet growing, threat is from insurtechs. While many currently partner with reinsurers for capital, their technology-driven underwriting and distribution models threaten to disintermediate traditional players over the long term, especially in less complex specialty lines.

Market Position and Opportunities:

Everest is solidly positioned in the global top 10 reinsurers but lacks the scale to compete with the top two on every front. Its key disadvantage is a smaller capital base and R&D budget compared to these giants. However, this can be turned into a strength by focusing on agility and specialization.

Strategic whitespace exists in several areas:

1. Emerging & Complex Risks: There is an opportunity to become the market leader for underwriting emerging technological risks (e.g., AI, quantum computing) and developing innovative products like parametric insurance for secondary climate perils (drought, flood) that are not well-served by the current market.

2. Digital Broker Experience: A significant gap exists between the digital-native experience offered by insurtechs and the often-clunky processes of legacy insurers. Investing in a best-in-class digital platform for brokers could create a powerful competitive moat.

3. Alternative Capital Management: Instead of only competing with ILS, Everest could launch its own platform to manage third-party capital, creating a new, fee-based revenue stream and allowing it to offer clients a broader range of risk transfer solutions.

Conclusion & Strategic Imperative:

Everest Global's path forward requires a dual strategy: fortifying its core and innovating at the edges. It must continue to leverage its foundational strength in disciplined specialty underwriting and broker relationships. Simultaneously, it must strategically invest in technology and data analytics to close the gap with larger rivals and embrace new risk transfer mechanisms like ILS. The key to winning is not to out-scale the giants, but to be the most nimble, expert, and responsive underwriter in its chosen specialty markets.

Messaging

Message Architecture

Key Messages

- Message:

We underwrite opportunity.TM

Prominence:Primary

Clarity Score:Medium

Location:Homepage Hero

- Message:

Everest is a global underwriting leader providing best-in-class property, casualty and specialty reinsurance and insurance solutions.

Prominence:Secondary

Clarity Score:High

Location:Homepage

- Message:

Known for its 50-year track record of disciplined underwriting, capital, and risk management.

Prominence:Secondary

Clarity Score:High

Location:Homepage

- Message:

Our professionals are dedicated to reducing your cost of risk while handling claims quickly and efficiently.

Prominence:Tertiary

Clarity Score:High

Location:Homepage, Product Pages

The message hierarchy is logical and well-structured. It begins with the high-level, aspirational brand promise ('underwrite opportunity') and quickly provides more concrete supporting messages about leadership, experience, and specific solutions. This effectively guides the user from the 'why' to the 'what'.

Messaging is highly consistent across the analyzed pages. Core themes of global leadership, financial strength ('disciplined underwriting'), comprehensive solutions, and efficient claims are repeated, reinforcing the brand's key attributes effectively.

Brand Voice

Voice Attributes

- Attribute:

Authoritative

Strength:Strong

Examples

- •

Everest is a global underwriting leader...

- •

Learn why Everest is one of the world's largest reinsurers...

- •

We are a leader in the Accident and Health marketplace.

- Attribute:

Corporate

Strength:Strong

Examples

- •

We underwrite opportunity for all stakeholders...

- •

...create sustainable value for our colleagues, shareholders and the communities we serve.

- •

Empowerment of our people through authority and autonomy is a key tenet of our business philosophy.

- Attribute:

Reassuring

Strength:Moderate

Examples

...with protection and peace of mind...

...navigate their most complex challenges.

Tone Analysis

Formal and professional

Secondary Tones

Confident

Reassuring

Tone Shifts

The language on the 'Accident and Health' product page is slightly more direct and sales-oriented ('We will consider opportunities...') than the high-level corporate tone of the homepage.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Everest is a large-scale, financially disciplined global (re)insurer with a 50-year history of providing comprehensive, best-in-class solutions for complex risks, enabling clients to operate with security and pursue opportunities.

Value Proposition Components

- Component:

Global Scale and Leadership

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Financial Strength & Disciplined Underwriting

Clarity:Clear

Uniqueness:Common

- Component:

Breadth of Solutions (Insurance & Reinsurance)

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Longevity and Experience (50-year track record)

Clarity:Clear

Uniqueness:Unique

- Component:

Efficient Claims Handling

Clarity:Clear

Uniqueness:Common

The messaging effectively differentiates Everest through its combination of immense scale ('one of the world's largest reinsurers'), a long and specific history ('50-year track record'), and the dual capability in both insurance and reinsurance. While competitors like Swiss Re and Munich Re also claim scale, the '50-year' proof point is a tangible and powerful asset. The tagline 'We underwrite opportunity' is a unique framing, but it requires more substantiation to be a core differentiator.

The messaging positions Everest as a top-tier, established, and reliable leader in the global market, competing with other major players like Swiss Re, Munich Re, and Berkshire Hathaway. The emphasis on disciplined underwriting and capital management squarely addresses the core concerns of B2B clients and partners in a risk-averse industry.

Audience Messaging

Target Personas

- Persona:

Risk Managers & Corporate Buyers

Tailored Messages

- •

...address customers’ most pressing challenges.

- •

...navigate their most complex challenges.

- •

Our professionals are dedicated to reducing your cost of risk...

Effectiveness:Effective

- Persona:

Brokers, MGAs, and Distribution Partners

Tailored Messages

We will consider opportunities either retail or wholesale, via MGA’s, Brokers and strategic distribution partners...

Learn why Everest is... the preferred partner in every market we serve.

Effectiveness:Effective

- Persona:

Cedents (Insurance companies seeking reinsurance)

Tailored Messages

Learn why Everest is one of the world's largest reinsurers...

Reliable capacity and trusted partnerships remain paramount

Effectiveness:Somewhat Effective

Audience Pain Points Addressed

- •

Navigating complex and uncertain risk environments

- •

Financial loss from unforeseen events

- •

High cost of risk

- •

Inefficient or slow claims processing

Audience Aspirations Addressed

- •

Business growth and thriving

- •

Stability and peace of mind

- •

Seizing new opportunities

- •

Partnering with a reliable and financially strong entity

Persuasion Elements

Emotional Appeals

- Appeal Type:

Security & Safety

Effectiveness:High

Examples

...with protection and peace of mind...

...navigate their most complex challenges.

- Appeal Type:

Success & Opportunity

Effectiveness:Medium

Examples

We underwrite opportunity.TM

We help our clients and businesses thrive, fuel global economies...

Social Proof Elements

- Proof Type:

Claim of Leadership/Scale

Impact:Strong

Examples

Everest is a global underwriting leader...

...one of the world's largest reinsurers...

- Proof Type:

Longevity/History

Impact:Strong

Examples

Known for its 50-year track record...

- Proof Type:

Media Mentions

Impact:Moderate

Examples

In the news - The Insurer

Trust Indicators

- •

Specific claim of '50-year track record'

- •

Mention of 'disciplined underwriting, capital, and risk management'

- •

Clear identification of key personnel with direct contact information

- •

Prominent 'Claims and Support' sections

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

Read more

Location:Homepage, under Insurance/Reinsurance sections

Clarity:Clear

- Text:

Claims and support

Location:Homepage and Product Pages

Clarity:Clear

- Text:

Contact via email

Location:Product Page Key Contacts section

Clarity:Clear

The CTAs are clear and functional but lack persuasive power. They are directive ('Read more') rather than benefit-oriented ('See our solutions'). For a sophisticated B2B audience, the direct contact CTAs on the product page are highly effective as they connect prospects directly with decision-makers.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of customer evidence: There are no client testimonials, case studies, or success stories to substantiate the claims of leadership and 'underwriting opportunity'.

- •

Absence of quantifiable metrics: Besides the '50-year' track record, the messaging lacks hard data (e.g., financial strength ratings from A.M. Best, capital surplus figures, number of clients served) that are crucial for building credibility in the financial services sector.

- •

Underdeveloped 'Why Everest' narrative: The core brand promise 'We underwrite opportunity' remains abstract and is not connected to tangible client outcomes through storytelling or examples.

Contradiction Points

No itemsUnderdeveloped Areas

Thought Leadership: The site asserts expertise but doesn't demonstrate it with insights, white papers, or analysis on the 'increasingly complex and uncertain world' it mentions.

Humanization: The brand feels institutional. Apart from headshots in the 'Key contacts' section, there is little to showcase the human expertise driving the company's success.

Messaging Quality

Strengths

- •

Strong, consistent, and professional brand voice.

- •

Clear articulation of core services (Insurance, Reinsurance, Claims).

- •

Effective use of authority by claiming leadership and citing its long history.

- •

Logical message hierarchy that guides users from brand to product.

Weaknesses

- •

Over-reliance on assertion rather than demonstration (lack of proof points).

- •

Messaging is overly abstract and corporate, lacking emotional connection.

- •

Value proposition feels generic at times ('best-in-class solutions') without specific examples.

- •

CTAs are passive and could be more action-oriented.

Opportunities

- •

Develop case studies that bring the 'underwrite opportunity' tagline to life.

- •

Create a 'Why Everest' page that includes key financial metrics, ratings, and client testimonials to build a stronger trust narrative.

- •

Launch a thought leadership section with articles and insights from Everest's experts to prove their expertise in navigating complex risks.

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition Substantiation

Recommendation:Create a 'Client Success' or 'Case Studies' section featuring short, impactful stories that demonstrate how Everest's solutions enabled a client's success or solved a complex challenge. Frame these stories around the 'underwriting opportunity' concept.

Expected Impact:High

- Area:

Trust & Credibility

Recommendation:Incorporate a 'By the Numbers' or 'Our Financial Strength' module on the 'Why Everest' page and homepage, prominently displaying key metrics like financial strength ratings (e.g., A+ from A.M. Best), capital levels, and global presence.

Expected Impact:High

- Area:

Thought Leadership

Recommendation:Develop a content strategy that produces articles, reports, or webinars featuring Everest's experts. This will demonstrate their expertise on emerging risks and industry trends, supporting the claim of being a leader in a 'complex and uncertain world'.

Expected Impact:Medium

Quick Wins

- •

Revise generic 'Read more' CTAs to be more specific and benefit-driven, such as 'Explore our Reinsurance Capabilities' or 'See our Insurance Solutions'.

- •

Feature the '50-year track record' more prominently on the homepage, possibly as a sub-headline, to immediately establish credibility.

- •

Add logos of financial rating agencies (e.g., A.M. Best, S&P) in the website footer or on the 'Why Everest' page.

Long Term Recommendations

- •

Evolve the brand narrative from being company-centric ('We are leaders') to being more client-centric ('How we empower our clients').

- •

Invest in creating more human-centric content, such as video interviews with key underwriters or claims professionals, to put a face to the expertise.

- •

Develop persona-specific content hubs that aggregate the most relevant products, insights, and case studies for key audiences like brokers or risk managers.

Everest's strategic messaging establishes a strong foundation, positioning the company as a major, credible, and experienced player in the global insurance and reinsurance market. The brand voice is authoritative and consistent, and the message architecture logically guides stakeholders from a high-level brand promise to specific service offerings. The core value proposition—built on scale, experience, and disciplined underwriting—is clearly communicated and aligns with the decision-making criteria of its B2B audience.

However, the messaging strategy has a significant gap between assertion and substantiation. While Everest claims it is a leader that 'underwrites opportunity,' it fails to show this through tangible proof points. The website lacks the case studies, client testimonials, and quantifiable data (beyond its 50-year history) that are critical for converting interest into trust in the high-stakes B2B insurance space. The powerful tagline 'We underwrite opportunity' remains an abstract concept rather than a demonstrated reality.

The primary opportunity for optimization lies in building a richer narrative supported by evidence. By weaving in client success stories, showcasing financial strength metrics, and demonstrating expertise through thought leadership, Everest can transform its messaging from a confident statement into a compelling and differentiated argument, moving beyond industry-standard corporate language to create a more persuasive and memorable brand.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Established global leader with a 50-year track record in property, casualty, and specialty reinsurance and insurance.

- •

Recent financial results show consistent revenue growth (6.2% YoY in Q2 2025) and beating analyst expectations, indicating strong market demand.

- •

Diversified portfolio across numerous business lines (e.g., Accident & Health, Pro Sports Disability) and geographies, reducing dependency on any single market segment.

- •

Strong financial strength ratings are essential for customer trust and are a key indicator of product-market fit in the insurance sector.

Improvement Areas

Enhance digital product offerings and self-service capabilities for brokers and direct clients to match Insurtech competitors.

Increase speed-to-market for new, specialized insurance products that address emerging risks like advanced cyber threats and climate-related impacts.

Market Dynamics

Reinsurance market CAGR estimated at 4.5% to 8.04%; P&C insurance market CAGR between 4.3% and 8.3%.

Mature

Market Trends

- Trend:

Digital Transformation & Insurtech Integration

Business Impact:Pressure to innovate core processes (underwriting, claims) with AI/ML and improve digital channels for brokers and clients to remain competitive.

- Trend:

Climate Change & Catastrophe Modeling

Business Impact:Increased demand for sophisticated risk modeling and new products (e.g., parametric insurance). Heightened risk exposure requires disciplined underwriting and capital management.

- Trend:

Growth in Cyber Insurance

Business Impact:Significant opportunity for premium growth in the expanding cyber insurance market, but also poses challenges in risk assessment and modeling.

- Trend:

Focus on Underwriting Discipline

Business Impact:A market-wide shift towards profitability over pure growth, favoring companies like Everest with a history of disciplined underwriting, especially in hardening markets.

Favorable. The current market conditions, characterized by heightened risk awareness (climate, cyber) and a flight to quality, favor established, well-capitalized players. There is a clear window of opportunity to capture market share in high-growth specialty lines.

Business Model Scalability

High

Scalable model with significant fixed costs in technology and talent, but these can support substantial increases in gross written premiums with marginal cost increases.

High. Once underwriting expertise and systems are in place, the model can absorb significantly more premium volume. Profitability is highly sensitive to underwriting performance (combined ratio) and investment income.

Scalability Constraints

- •

Capital Adequacy: Growth is fundamentally limited by the amount of capital held to underwrite new risks and satisfy regulators.

- •

Talent Availability: Scarcity of specialized underwriting talent for emerging and complex risks (e.g., advanced cyber, climate science).

- •

Legacy Technology: Older IT systems can hinder the rapid launch of new products and digital integrations.

Team Readiness

Experienced. Recent executive appointments in key roles like CEO of Reinsurance and Chief Commercial Officer for International Insurance demonstrate a focus on strategic leadership for growth.

Traditional. The structure appears to be segmented by business line (Insurance, Reinsurance) and geography. While efficient for core operations, this may slow cross-functional innovation.

Key Capability Gaps

- •

Agile Product Development: Need for faster, more iterative product development cycles to compete with Insurtechs.

- •

Data Science & AI Engineering: Deepening talent in AI/ML for advanced risk modeling, pricing, and claims automation.

- •

Digital Experience Management: Expertise in creating seamless digital journeys for brokers and strategic partners.

Growth Engine

Acquisition Channels

- Channel:

Broker & MGA Network

Effectiveness:High

Optimization Potential:High

Recommendation:Develop a best-in-class digital broker portal with instant quoting, policy management, and analytics tools to become the preferred partner and increase submission flow-through.

- Channel:

Strategic Partnerships (Banks, Tech Providers)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Actively pursue embedded insurance opportunities with technology platforms and financial institutions to access new customer pools and create diversified revenue streams.

- Channel:

Direct Sales (Corporate & Major Accounts)

Effectiveness:Medium

Optimization Potential:Medium

Recommendation:Leverage thought leadership and content marketing focused on complex risk management to attract and engage large corporate clients directly.

Customer Journey

The 'customer' is primarily a broker or a large corporate risk manager. The journey is relationship-driven, involving presentations, negotiations, and detailed underwriting reviews.

Friction Points

- •

Slow quote and bind process for complex risks.

- •

Lack of real-time visibility into submission or claim status for brokers.

- •

Onboarding and compliance for new distribution partners can be cumbersome.

Journey Enhancement Priorities

{'area': 'Broker Digital Experience', 'recommendation': 'Invest in a unified digital platform that simplifies the entire broker lifecycle from submission to claims, using APIs for seamless integration.'}

{'area': 'Claims Process', 'recommendation': 'Implement AI-driven tools for faster claims triage and processing, providing brokers and policyholders with greater transparency and speed. '}

Retention Mechanisms

- Mechanism:

Policy Renewal Rate

Effectiveness:High

Improvement Opportunity:Utilize predictive analytics to identify policies at risk of non-renewal and proactively engage brokers with competitive pricing or enhanced coverage options.

- Mechanism:

Claims Service & Satisfaction

Effectiveness:High

Improvement Opportunity:Continuously measure and improve claim settlement cycle time, as it is a leading indicator of customer satisfaction and retention.

- Mechanism:

Broker Relationship Management

Effectiveness:High

Improvement Opportunity:Implement a tiered relationship management program with dedicated resources and co-marketing funds for top-performing broker partners.

Revenue Economics

Strong. As a mature insurer, profitability is driven by disciplined underwriting (reflected in the combined ratio) and investment income. The focus is on writing profitable business rather than growth at any cost.

A key metric for the business. A ratio below 100% indicates underwriting profitability. Recent market commentary suggests a focus on maintaining a low combined ratio.

High. The company demonstrates an ability to generate significant premium volume and investment income relative to its operational expense base.

Optimization Recommendations

- •

Continue to shift the portfolio mix towards higher-margin specialty lines like Accident & Health and international business, as indicated in recent performance.

- •

Leverage technology to lower the expense ratio by automating routine underwriting and administrative tasks.

- •

Optimize investment strategy to capitalize on the higher interest rate environment to bolster net income.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Systems

Impact:High

Solution Approach:Adopt a two-speed IT architecture: maintain stable legacy systems for core functions while building a nimble, cloud-native layer for new digital products and broker integrations.

- Limitation:

Fragmented Data Architecture

Impact:Medium

Solution Approach:Invest in a centralized data platform to consolidate data from various systems, enabling advanced analytics, AI model training, and a single view of the customer/broker.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting for Complex Risks

Growth Impact:Limits the volume and speed of quoting, potentially losing business to more agile competitors.

Resolution Strategy:Develop AI-augmented underwriting workbenches that ingest and analyze submission data, providing decision support to human underwriters to increase their throughput and accuracy.

- Bottleneck:

Multi-Jurisdictional Regulatory Compliance

Growth Impact:Slows down geographic expansion and new product launches due to complex and varied compliance requirements.

Resolution Strategy:Invest in RegTech solutions to automate compliance monitoring, reporting, and management across different legal frameworks.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Critical

Mitigation Strategy:Compete on underwriting expertise, financial strength, and superior broker service rather than on price alone. Key competitors include Munich Re, Swiss Re, Chubb, and Arch Capital.

- Challenge:

Disruption from Insurtech Startups

Severity:Major

Mitigation Strategy:Establish a corporate venture arm or strategic partnership program to collaborate with, invest in, or acquire Insurtechs that provide complementary technology or market access.

Resource Limitations

Talent Gaps

- •

Data Scientists and AI/ML Engineers with deep insurance domain knowledge.

- •

Digital Product Managers.

- •

Cybersecurity Underwriting Specialists.

Growth is directly tied to maintaining a strong capital base. Scaling requires continuous capital management to support increased underwriting and maintain high financial strength ratings.

Infrastructure Needs

Cloud-based infrastructure to support agile development and advanced analytics workloads.

Modern API gateway to facilitate seamless integration with brokers, MGAs, and Insurtech partners.

Growth Opportunities

Market Expansion

- Expansion Vector:

Geographic Expansion in Emerging Markets (Asia, LatAm)

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Pursue a strategy of acquiring or partnering with established local insurers to gain market access, licenses, and local expertise, as hinted by investments in international operations.

- Expansion Vector:

Small and Medium-sized Enterprise (SME) Market

Potential Impact:Medium

Implementation Complexity:Medium

Recommended Approach:Develop a digital-first platform to offer standardized commercial insurance products to SMEs through a direct or light-touch broker model, leveraging the Accident & Health segment's mention of portfolio-based SME approaches.

Product Opportunities

- Opportunity:

Advanced Cyber Insurance Products

Market Demand Evidence:Surging demand due to the increasing frequency and sophistication of cyber-attacks.

Strategic Fit:High. Aligns with the company's expertise in underwriting complex specialty risks.

Development Recommendation:Partner with cybersecurity firms to integrate real-time threat intelligence into underwriting and offer risk mitigation services alongside policies.

- Opportunity:

Climate Risk & Parametric Insurance

Market Demand Evidence:Increasing frequency of extreme weather events is driving demand for innovative risk transfer solutions.

Strategic Fit:High. Leverages core competency in catastrophe modeling and reinsurance.

Development Recommendation:Develop data-driven parametric insurance products where claims are paid based on predefined triggers (e.g., wind speed, rainfall level), enabling faster payouts and greater transparency.

- Opportunity:

Embedded Insurance

Market Demand Evidence:Growing trend of integrating insurance into third-party products and services at the point of sale.

Strategic Fit:Medium. Represents a new distribution model that could complement the existing broker channel.

Development Recommendation:Create a dedicated team and a robust API platform to partner with e-commerce, travel, and technology companies to embed Everest's products into their offerings.

Channel Diversification

- Channel:

Insurtech Partnerships

Fit Assessment:High

Implementation Strategy:Establish a formal program to scout, pilot, and integrate with Insurtechs that offer innovative solutions in distribution, underwriting, or claims processing.

- Channel:

Digital-Direct for Niche SME Products

Fit Assessment:Medium

Implementation Strategy:Launch a separate brand or digital platform to test direct-to-SME distribution for specific, simple-to-underwrite products, avoiding channel conflict with the core broker network.

Strategic Partnerships

- Partnership Type:

Technology & Data Partnerships

Potential Partners

- •

Geospatial data providers (e.g., for climate risk)

- •

Cybersecurity firms (e.g., for cyber risk intelligence)

- •

AI/ML platform providers

Expected Benefits:Enhanced underwriting accuracy, improved risk selection, and the ability to create more sophisticated insurance products.

- Partnership Type:

Corporate Venture Capital / M&A

Potential Partners

Early-stage Insurtech startups

Specialized MGAs with unique distribution or underwriting expertise

Expected Benefits:Access to new technologies, talent, and niche markets; potential for high ROI and strategic advantage.

Growth Strategy

North Star Metric

Growth of Gross Written Premium in High-Margin Specialty & International Lines

This metric focuses the organization on profitable growth rather than just top-line expansion in commoditized markets. It aligns directly with the company's stated strategy of portfolio reshaping and disciplined underwriting.

Achieve >15% year-over-year growth in these targeted segments.

Growth Model

Broker-Led & Partnership-Driven Growth

Key Drivers

- •

Deepening relationships with top-tier brokers.

- •

Strategic acquisition of specialized MGAs or smaller competitors.

- •

Expansion of partnerships with technology companies for embedded insurance.

- •

New product development in high-demand areas (cyber, climate).

Focus resources on becoming the 'carrier of choice' for brokers through superior service, digital tools, and underwriting expertise. Simultaneously, build a dedicated corporate development team to pursue M&A and strategic technology partnerships.

Prioritized Initiatives

- Initiative:

Launch a Best-in-Class Digital Broker Platform

Expected Impact:High

Implementation Effort:High

Timeframe:18-24 months

First Steps:Form a cross-functional team of underwriters, IT, and broker relationship managers. Conduct extensive user research with key broker partners to define MVP features.

- Initiative:

Expand Climate & Cyber Risk Product Suites

Expected Impact:High

Implementation Effort:Medium

Timeframe:9-12 months

First Steps:Hire dedicated product managers and lead underwriters with deep expertise in these domains. Establish data partnerships to acquire necessary risk modeling inputs.

- Initiative:

Formalize Insurtech Partnership Program

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:6 months

First Steps:Appoint a Head of Insurtech Partnerships. Define a clear process for scouting, evaluating, and piloting technologies. Allocate a dedicated pilot budget.

Experimentation Plan

High Leverage Tests

{'test_name': 'Dynamic Commissioning for Brokers', 'hypothesis': 'Offering higher commissions for high-quality, complete submissions via the digital portal will increase both submission volume and underwriting efficiency.'}

{'test_name': 'Pilot a Parametric Product in a Single Region', 'hypothesis': 'A parametric insurance product for a specific peril (e.g., hurricane) will attract new customers seeking faster, more transparent claim settlements.'}

Utilize an A/B testing framework for digital initiatives. For product pilots, track submission volume, quote-to-bind ratio, loss ratio, and broker feedback against a predefined control group or baseline.

Quarterly review of experiment pipeline and results, with a monthly cadence for digital channel tests.

Growth Team

A centralized 'Strategic Growth & Innovation' unit that works in conjunction with the core business units (Reinsurance, Insurance). This team would be responsible for M&A, Insurtech partnerships, and incubating new products.

Key Roles

- •

Head of Strategic Growth

- •

Director of Insurtech Partnerships

- •

Venture & M&A Analyst

- •

New Product Incubation Lead

Develop capabilities through a mix of hiring external talent (especially for digital and data science roles) and creating internal rotation programs to bring business unit expertise into the growth team.

Everest Global possesses a strong foundation for growth, built upon decades of underwriting discipline, a diversified global portfolio, and a powerful broker-led distribution model. Its product-market fit is firmly established in the mature but evolving insurance and reinsurance landscape. The market dynamics are favorable, with increasing demand for sophisticated risk management solutions for emerging threats like climate change and cyber-attacks creating significant opportunities in high-margin specialty lines.

The primary growth engine relies on the broker network. The most significant lever for accelerating growth is to digitally empower this channel, transforming from a relationship-based model to a digitally-enabled, relationship-deepened one. This involves creating a best-in-class digital experience that makes Everest the easiest and most efficient partner for brokers to work with, thereby increasing submission volume and improving risk selection.

Key barriers to scaling are characteristic of a large, successful incumbent: potential for operational bottlenecks from legacy systems and the intense competitive pressure from both traditional peers and nimble Insurtechs. Overcoming these requires a dual focus: modernizing the technology stack to enable agility and systematically engaging with the Insurtech ecosystem through partnerships and strategic investments.

Growth opportunities are abundant in both product and market expansion. The most promising vectors are expanding the portfolio of specialty products (particularly in climate and cyber risk), pursuing strategic M&A to acquire new capabilities or market access, and exploring new distribution channels like embedded insurance. A disciplined growth strategy, guided by a North Star Metric focused on profitable premium growth in strategic segments, will allow Everest to leverage its core strengths to capture these opportunities and solidify its market leadership in an increasingly complex world.

Legal Compliance

Everest provides multiple, region-specific privacy notices, including for the US and GDPR, which demonstrates a strong awareness of its global data protection obligations. The US Privacy Notice explicitly details consumer rights under various state laws, including a comprehensive section for California residents that covers the right to know, access, opt-out of sale/sharing, delete, and correct personal information. The policy clearly identifies the categories of personal information collected (including sensitive identifiers like Social Security and driver's license numbers) and the purposes for its use. It also provides multiple contact methods for the Data Privacy & Protection Officer, which is a best practice. However, the primary challenge is the accessibility and integration of these policies. For a global user, navigating to the correct notice can be cumbersome. A central, easily understandable global privacy policy that directs users to regional specifics would enhance user experience and transparency.

The 'Terms of Use' are present and accessible via the website footer. The terms are comprehensive, covering intellectual property rights, limitations of use, disclaimers of warranties, and limitation of liability. The language is standard for a corporate website, establishing that the materials are provided 'as-is' and asserting ownership over the content. It specifies that the site is controlled from the USA and places the responsibility for compliance with local laws on the user accessing the site from other jurisdictions. While legally robust in protecting Everest, the dense legal language could be challenging for the average user to understand, a common issue with such documents. For a company focused on trust and partnership, simplifying key sections could improve customer relations.

The website's cookie consent mechanism presents a significant compliance gap, particularly concerning GDPR. The banner states, 'By continuing to use our site, you consent to the use of cookies,' which is an 'implied consent' model. This model is no longer compliant with GDPR, which requires explicit, affirmative, and granular consent before non-essential cookies are placed. While the banner provides an 'Accept All Cookies' button and a link to the cookie policy, it lacks a visible and equally prominent 'Reject All' or 'Customize' option on the initial banner. This design, often called 'dark patterns,' nudges users towards acceptance and is a primary focus of EU data protection authorities. This represents a high-risk area for regulatory fines in the EU, where Everest has a significant and growing presence.

As a global insurer and reinsurer, Everest is subject to a complex web of data protection laws, including GDPR in Europe, CCPA/CPRA in California, and crucially, the Gramm-Leach-Bliley Act (GLBA) in the United States. The company's privacy notices show a good understanding of these distinct requirements, with specific sections for different jurisdictions. The collection of sensitive data for 'Accident and Health' products elevates risk, bringing regulations like HIPAA into consideration, although GLBA is the primary regulation for financial institutions like insurers. The privacy notices address the sharing of data with affiliates and third parties, a key requirement of GLBA. However, the partial exemption for GLBA-covered data under CCPA does not apply to the private right of action in case of a data breach, meaning any security lapse carries significant liability risk in California. The overall strategy is solid in its documentation, but the website's user-facing implementation (especially cookie consent) weakens its practical compliance posture.

A high-level manual review of the website indicates a reasonable baseline for accessibility, with clear navigation structures and readable text. However, there is no readily apparent Accessibility Statement on the website. Such a statement is a best practice and increasingly a legal expectation, outlining the company's commitment to accessibility, the standards it adheres to (like WCAG 2.1), and providing a contact method for users who encounter accessibility barriers. The absence of this statement creates uncertainty about the company's formal commitment and compliance level with standards like the Americans with Disabilities Act (ADA) and equivalent international laws, potentially creating legal risk and excluding users with disabilities.

For a global insurance leader, specific industry disclosures are paramount for regulatory compliance and building trust. The website content alludes to its strong track record and global affiliates but lacks easily accessible, centralized information on key compliance points. Critical disclosures that are not prominently displayed include:

1. State Licensing Information: No clear, consolidated list or database is available for users to verify which Everest entity is licensed to operate in their specific US state. This is a fundamental requirement for insurers.