eScore

home.globelifeinsurance.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Globe Life's digital presence is functional for direct-response marketing but lacks strategic sophistication. The website is heavily geared towards bottom-of-funnel users who are ready to buy, but it fails to capture a wider audience in the awareness and consideration stages due to a weak top-of-funnel content strategy. While they have a multi-channel presence in their business model (mail, phone, agent), this is not well-integrated online, and their digital content authority is low compared to competitors and financial content publishers who invest heavily in educational resources.

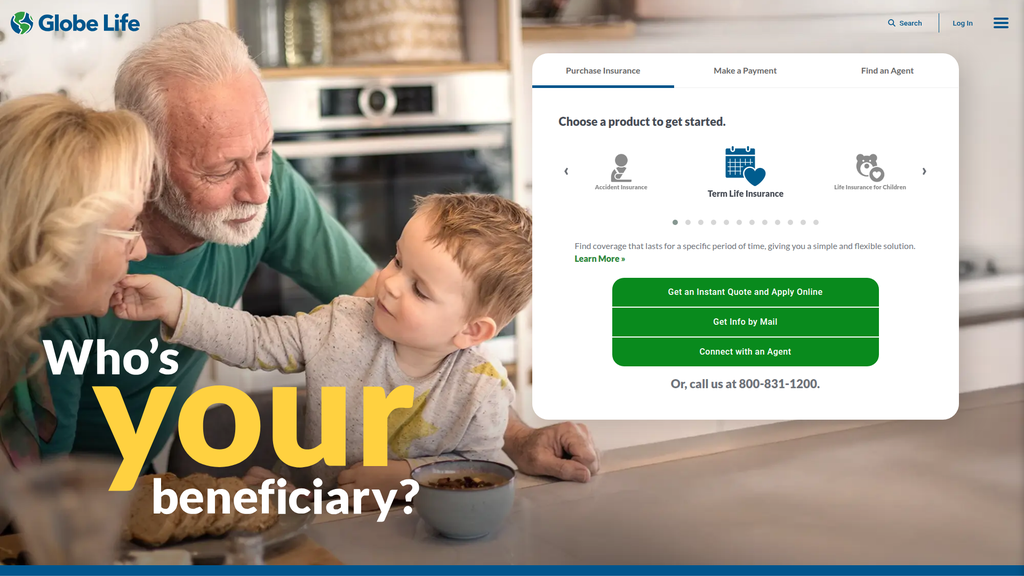

The website offers clear, direct pathways to conversion for users who are already intent on purchasing, such as 'Buy Online' and 'Find an Agent'.

Develop a comprehensive, top-of-funnel content strategy by creating a 'Family Financial Hub' with articles, guides, and tools to attract and nurture users earlier in their journey, positioning Globe Life as a trusted advisor rather than just a product vendor.

The company's messaging is exceptionally clear, consistent, and well-aligned with its target demographic of middle-income families. Core messages of family protection, simplicity, and reliability are powerfully communicated, especially through the prominent display of the large dollar amount of claims paid, which serves as strong social proof. However, the communication is highly rational and functional, missing a significant opportunity to build a deeper emotional connection through human-centric storytelling and testimonials.

The core value proposition of providing simple, accessible, and reliable insurance through multiple channels is communicated with excellent clarity and consistency.

Incorporate customer testimonials and 'beneficiary stories' into the website to transform the abstract promise of protection into a tangible, emotional reality, thereby building a stronger brand affinity beyond the functional benefits.

The conversion experience is hindered by significant friction points and a high cognitive load on the homepage. Users are immediately presented with too many competing choices ('Get a Quote', 'Find an Agent', 'Buy Online', 'Buy by Mail'), which can lead to decision paralysis. While the site is functional on mobile, the overwhelming choices and dense text blocks become even more problematic on smaller screens. The lack of interactive tools like a needs calculator further detracts from a guided, user-centric conversion path.

The site effectively caters to different user preferences by clearly presenting multiple, distinct channels for purchase (Online, Mail, Agent, Phone).

Redesign the homepage to create a single, guided user journey. Replace the multi-path hero section with a primary call-to-action (e.g., 'Get My Free Quote') and introduce a simple needs-assessment tool to direct users to the most appropriate product and purchase path, reducing friction and cognitive load.

Globe Life effectively establishes credibility through strong trust signals, including its long history (since 1900), consistently high financial strength ratings from agencies like A.M. Best (A) and S&P (AA-), and prominent social proof of paying billions in claims. The recent conclusion of SEC and DOJ investigations without enforcement action also mitigates a significant reputational risk. However, the company has a high volume of customer complaints filed with state regulators, which presents a notable weakness.

The company's long history and consistently high financial strength ratings from A.M. Best, S&P, and Fitch provide a powerful foundation of trust and reliability.

Address the root causes of the high volume of NAIC customer complaints to improve customer satisfaction and mitigate reputational damage. Additionally, make legal documents like the Privacy Policy and Terms of Service more accessible from the main marketing pages.

Globe Life's most sustainable competitive advantage is its unique multi-channel distribution model that serves a broad, often underserved, middle-income demographic. This hybrid approach (agent, mail, phone, online) is difficult for digital-only or traditional-only competitors to replicate effectively. However, this advantage is being eroded by a dated digital experience, which puts them at a disadvantage against agile insurtech competitors who offer superior online journeys.

The multi-channel distribution network (agents, mail, phone, online) provides a durable competitive moat by offering unparalleled accessibility to their target market.

Invest significantly in modernizing the online channel's user experience to compete directly with insurtechs like Ethos and Ladder. The goal should be to create a seamless omni-channel experience, turning the multi-channel model into a fully integrated strategic asset.

The business model has proven scalability, as evidenced by its 17 million policies in force. However, future growth is constrained by a heavy reliance on the less-scalable agent-based sales model, which has high variable costs. The under-optimized direct-to-consumer digital channel represents a significant untapped area for more efficient, lower-cost growth. Expansion into younger demographics is a major challenge due to a brand perception that is more traditional.

A massive existing policyholder base (17 million+) provides a stable revenue foundation and significant opportunities for cross-selling and up-selling supplemental products.

Prioritize investment in the direct-to-consumer (D2C) digital channel to create a more efficient and scalable growth engine. This includes optimizing the conversion funnel and developing digital marketing campaigns tailored to younger demographics to lower the blended customer acquisition cost.

Globe Life's business model is exceptionally coherent and focused. The company has a clear strategy of providing simple, affordable insurance products to a well-defined niche of lower-middle to middle-income families. The revenue model, based on recurring premiums and investment income, is stable and proven. All key activities, from the multi-channel distribution to the product design, are tightly aligned with this core strategic focus.

The business model exhibits a rare and powerful strategic focus, with all components—from product design and pricing to distribution channels—purpose-built to serve the specific needs of the middle-income market segment.

Innovate within the existing model by leveraging customer data more effectively. A key opportunity is to develop a robust data analytics program to personalize offers and proactively cross-sell to the 17 million+ policyholders, increasing lifetime value.

Within its niche of the middle-income market, Globe Life exerts considerable market power due to its strong brand recognition and massive policyholder base, which is larger than any other single life insurer. This gives them pricing power within their target affordability range and significant leverage in their distribution network. However, their influence is limited outside of this niche, and they are facing intense pressure from both large traditional insurers and nimble insurtech startups that are setting new standards for digital customer experience.

Having more policies in force than any other U.S. life insurance company provides significant market stability, brand recognition, and a large data asset.

Improve the digital customer experience to defend market share against insurtechs. Failure to innovate in the online channel risks ceding market influence and the next generation of customers to more technologically advanced competitors.

Business Overview

Business Classification

Insurance Provider

Financial Services

Insurance

Sub Verticals

- •

Life Insurance

- •

Supplemental Health Insurance

- •

Medicare Supplement Insurance

Mature

Maturity Indicators

- •

Established in 1900, with over a century of operations.

- •

Significant brand recognition in its target market.

- •

Large and stable customer base with over 17 million policies in force.

- •

Consistent financial performance and dividend payments.

- •

Large-scale claim payouts, demonstrating financial stability ($1.8B in 2024).

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Insurance Premiums

Description:The primary source of revenue is recurring premiums paid by policyholders for life, supplemental health, and Medicare supplement insurance policies. This creates a stable and predictable income stream.

Estimated Importance:Primary

Customer Segment:All Segments

Estimated Margin:Medium

- Stream Name:

Net Investment Income

Description:Income generated from investing the 'float' (premiums collected before claims are paid out) into a portfolio of assets, typically bonds and other secure investments. This is a standard and significant revenue source for insurance companies.

Estimated Importance:Secondary

Customer Segment:Internal/Corporate

Estimated Margin:High

Recurring Revenue Components

Monthly and annual policy premiums from individuals and families.

Pricing Strategy

Actuarial-Based Fixed Premium

Budget-to-Mid-range

Semi-transparent

Pricing Psychology

- •

Affordability Framing (e.g., 'fit any need or budget')

- •

Simplicity Pricing (easy to understand products and applications)

- •

Security-Focused Messaging (emphasizing family protection and peace of mind)

Monetization Assessment

Strengths

- •

High degree of recurring and predictable revenue from premiums.

- •

Focus on a budget-conscious market segment provides a large, stable customer base.

- •

Dual income from underwriting (premiums) and investments creates a resilient model.

Weaknesses

- •

Revenue growth is tied to new policy sales in a competitive market.

- •

Investment income is sensitive to interest rate fluctuations and market volatility.

- •

Focus on lower-premium products may result in a lower average revenue per customer compared to premium insurers.

Opportunities

- •

Leverage data analytics to optimize pricing and cross-sell/upsell additional products to the existing customer base.

- •

Introduce new, simple financial wellness products (e.g., small-scale investment or savings plans) tailored to the target demographic.

- •

Enhance digital self-service tools to reduce administrative costs and improve margins.

Threats

- •

Intense competition from traditional insurers and emerging insurtech startups.

- •

Economic downturns could impact the ability of their target middle-income demographic to afford premiums.

- •

Increasingly stringent regulatory changes could impact product design, pricing, and capital requirements.

Market Positioning

Value-oriented provider of simple, accessible insurance products for working, middle-income American families.

Significant Niche Player

Target Segments

- Segment Name:

Lower-Middle to Middle-Income Families

Description:The core target market, comprising working families who are budget-conscious and seek straightforward, affordable financial protection for their loved ones.

Demographic Factors

- •

Annual household income between $40,000 and $100,000.

- •

Ages 25-65.

- •

Often have dependents.

Psychographic Factors

- •

Value family security and peace of mind.

- •

Risk-averse regarding financial futures.

- •

Prefer clear, simple solutions without complex jargon.

- •

May be first-time insurance buyers.

Behavioral Factors

- •

Responsive to direct marketing channels (mail, phone, online).

- •

Seek convenience and multiple options for purchasing.

- •

Price-sensitive and value-driven.

Pain Points

- •

Fear of leaving dependents with debt (e.g., mortgage, final expenses).

- •

Concern over unexpected medical costs not covered by primary health insurance.

- •

Overwhelmed by complex insurance products and application processes.

- •

Limited disposable income for high-premium policies.

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Seniors & Medicare-Eligibles

Description:Individuals aged 65 and over who are enrolled in Medicare and seek supplemental insurance to cover out-of-pocket costs like deductibles and co-payments.

Demographic Factors

- •

Age 65+.

- •

Enrolled in Medicare.

- •

Often on a fixed income.

Psychographic Factors

- •

Concerned with rising healthcare costs.

- •

Seek to protect retirement savings from medical expenses.

- •

Value stability and trust in an insurance provider.

Behavioral Factors

May prefer traditional purchasing channels like mail, phone, or agent interaction.

Highly responsive to marketing focused on covering Medicare gaps.

Pain Points

- •

High out-of-pocket costs not covered by original Medicare.

- •

Complexity of navigating different Medicare supplement plans.

- •

Financial vulnerability due to unexpected health issues in retirement.

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Multi-Channel Distribution Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Focus on Simplicity and Accessibility

Strength:Strong

Sustainability:Sustainable

- Factor:

Affordable Pricing for a Niche Market

Strength:Moderate

Sustainability:Sustainable

- Factor:

Strong Brand Recognition within Target Demographic

Strength:Strong

Sustainability:Sustainable

Value Proposition

Globe Life provides simple, affordable, and accessible life and supplemental health insurance to protect working families from financial hardship.

Excellent

Key Benefits

- Benefit:

Financial Security for Loved Ones

Importance:Critical

Differentiation:Common

Proof Elements

Statement of '$1.85 billion in claims paid in 2024'

Mission: 'We help families Make Tomorrow Better'

- Benefit:

Simplified Application Process

Importance:Important

Differentiation:Somewhat unique

Proof Elements

Mention of 'simple, Yes/No applications'

Emphasis on 'straightforward language'

- Benefit:

Accessible Purchasing Options

Importance:Important

Differentiation:Unique

Proof Elements

Clear callouts for four distinct channels: Online, Mail, Agent, and Phone

- Benefit:

Affordable Coverage

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Messaging that products are 'designed and priced to fit any need or budget'

Unique Selling Points

- Usp:

Comprehensive Multi-Channel Sales Approach (Online, Mail, Agent, Phone)

Sustainability:Long-term

Defensibility:Strong

- Usp:

Unwavering focus on the underserved middle-income market segment.

Sustainability:Long-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Financial devastation for a family after the death of a primary earner.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Inability to pay for final expenses, leaving debt for beneficiaries.

Severity:Major

Solution Effectiveness:Complete

- Problem:

High out-of-pocket costs from unexpected accidents or critical illnesses.

Severity:Major

Solution Effectiveness:Partial

- Problem:

The insurance buying process is too complex and intimidating.

Severity:Minor

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition directly addresses the growing need for financial protection in a market segment often overlooked by larger insurers focused on high-net-worth individuals. The emphasis on simplicity counters a major industry pain point.

High

The messaging, product design, and pricing are precisely tailored to the psychographics and pain points of middle-income families and seniors, who prioritize affordability, simplicity, and trust.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Independent and captive insurance agent networks.

- •

Reinsurance companies (to manage risk).

- •

Digital marketing and lead generation platforms.

- •

Labor unions and affinity groups (for American Income Life division).

Key Activities

- •

Multi-channel marketing and sales (Direct Mail, Online, Telesales, Agents).

- •

Insurance underwriting and risk assessment.

- •

Claims processing and policy administration.

- •

Investment portfolio management.

- •

Agent recruitment, training, and management.

Key Resources

- •

Strong brand equity and reputation.

- •

Extensive customer data and policyholder base.

- •

Statutory capital reserves.

- •

Proprietary agent network and distribution channels.

- •

Online quoting and application platform.

Cost Structure

- •

Policy obligations (claims payouts).

- •

Agent commissions and sales expenses.

- •

Marketing and advertising expenditures (especially direct mail and online).

- •

Employee salaries and administrative costs.

- •

Technology and infrastructure maintenance.

Swot Analysis

Strengths

- •

Dominant and established multi-channel distribution strategy.

- •

Strong brand recognition and trust within its niche market.

- •

Resilient business model with recurring premium revenue and investment income.

- •

Large, diversified book of business with 17 million+ policies.

- •

Clear, simple value proposition that resonates with its target audience.

Weaknesses

- •

Direct-to-consumer division has seen recent sales declines, indicating potential challenges in digital marketing efficiency.

- •

The simplified product portfolio may lack the flexibility and higher margins of more complex, customizable policies.

- •

Agent-heavy channels are less scalable and have higher acquisition costs than purely digital models.

- •

Perception as a 'budget' provider may limit appeal to higher-income segments.

Opportunities

- •

Enhance digital capabilities to improve the direct-to-consumer experience and operational efficiency.

- •

Utilize data analytics for improved customer segmentation, personalized marketing, and cross-selling.

- •

Expand product offerings into adjacent, simple financial wellness services to increase customer lifetime value.

- •

Growth in the Medicare-eligible population presents a significant opportunity for the Medicare Supplement business.

Threats

- •

Intense competition from traditional insurers (Aflac, MetLife, Prudential) and agile insurtech startups.

- •

Economic downturns disproportionately affecting their middle-income customer base, leading to policy lapses.

- •

Negative publicity or regulatory scrutiny impacting brand reputation.

- •

Shifting consumer preferences towards fully digital, self-service insurance platforms.

Recommendations

Priority Improvements

- Area:

Digital Customer Experience

Recommendation:Invest in a unified, end-to-end digital platform that allows customers to not only apply but also fully manage their policies, file claims, and interact with support online or via a mobile app. This will improve efficiency and meet the expectations of younger demographics.

Expected Impact:High

- Area:

Data Analytics & Personalization

Recommendation:Develop a centralized data analytics capability to gain deeper insights into the existing 17M+ policyholder base. Use these insights to create personalized cross-sell/upsell campaigns and improve customer retention.

Expected Impact:High

- Area:

Agent Technology Enablement

Recommendation:Equip the agent network with modern digital tools (CRM, analytics dashboards, mobile apps) to improve productivity, streamline sales processes, and provide a more consistent customer experience across channels.

Expected Impact:Medium

Business Model Innovation

- •

Develop a 'Family Financial Security' subscription bundle that combines a base life insurance policy with other relevant services (e.g., identity theft protection, basic will creation) for a single monthly fee.

- •

Explore embedded insurance partnerships with companies that also serve the middle-income demographic (e.g., tax preparation services, credit unions) to offer simple, point-of-sale insurance products.

- •

Pilot a 'try-before-you-buy' model for supplemental health, offering a very low-cost, limited-duration accident policy that can be easily converted to a full policy, reducing customer acquisition friction.

Revenue Diversification

- •

Introduce simple, low-cost savings or investment products tailored for long-term goals like education or retirement, leveraging the existing trust and customer relationships.

- •

Offer financial literacy and planning services as a premium add-on or a lead-generation tool for higher-value insurance packages.

- •

Create and market 'worksite' benefit packages for small to medium-sized businesses, bundling life and supplemental health products for their employees.

Globe Life has engineered a highly successful and resilient business model by maintaining a disciplined focus on the middle-income American market, a segment often underserved by more complex financial institutions. The company's core strength lies in its multi-channel distribution network, which masterfully blends traditional (direct mail, agents) and modern (online, phone) sales approaches, creating exceptional market accessibility. This strategy, combined with a value proposition centered on simplicity, affordability, and trust, has allowed Globe Life to build a massive and loyal policyholder base. The business is mature, financially stable, and generates predictable, recurring revenue from both premiums and investments.

However, the model faces strategic challenges from evolving market dynamics. While its traditional channels are a key differentiator, they are less scalable and more costly than the digital-first models of emerging insurtech competitors. The recent decline in sales for its Direct to Consumer division suggests that its online marketing strategy may require optimization to compete effectively for digital natives. Future growth and sustained market leadership will depend on Globe Life's ability to strategically evolve its business model. The primary opportunity lies in leveraging its vast customer data to enhance digital engagement and personalization. By investing in a seamless, end-to-end digital customer lifecycle—from acquisition to claims—and empowering its agent force with better technology, Globe Life can improve operational efficiency and defend its market position. Furthermore, innovating beyond core insurance into adjacent, simple financial wellness products could unlock significant new revenue streams and deepen customer relationships, transforming the company from a simple insurance provider into a comprehensive financial security partner for its target demographic.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

High Capital and Solvency Requirements

Impact:High

- Barrier:

Regulatory and Licensing Hurdles

Impact:High

- Barrier:

Brand Trust and Reputation

Impact:Medium

- Barrier:

Distribution Channel Access (Agent Networks)

Impact:Medium

Industry Trends

- Trend:

Digital Transformation and AI/ML Integration

Impact On Business:Legacy systems may struggle to compete with the streamlined, data-driven underwriting and customer experience of modern insurtechs. Failure to adapt will lead to loss of market share, especially with younger demographics.

Timeline:Immediate

- Trend:

Growth of Direct-to-Consumer (D2C) Channels

Impact On Business:While still a small portion of the market, the D2C channel is growing, driven by consumer demand for online, self-service options. This both complements and competes with Globe Life's existing multi-channel approach.

Timeline:Near-term

- Trend:

Demand for Personalized and Simplified Products

Impact On Business:Globe Life's emphasis on 'simple, Yes/No applications' aligns well with this trend. However, competitors are using data analytics to offer more personalized pricing and products, which could become a competitive disadvantage for Globe Life.

Timeline:Near-term

- Trend:

Focus on Holistic Financial Wellness

Impact On Business:Consumers, especially younger ones, are seeking advisors who can address a wide range of financial needs (investments, insurance, etc.). This may put pressure on insurers to broaden their offerings or partner with other financial service providers.

Timeline:Long-term

Direct Competitors

- →

Aflac

Market Share Estimate:Significant, especially in supplemental health

Target Audience Overlap:High

Competitive Positioning:Leading provider of supplemental insurance, primarily through worksite marketing, with very strong brand recognition (the Aflac Duck).

Strengths

- •

Exceptional brand awareness and recall.

- •

Dominant position in the worksite marketing channel.

- •

Strong focus and expertise in the supplemental health insurance niche.

- •

Strong financial position and long-standing relationships.

Weaknesses

- •

Heavy reliance on agent-based sales and worksite access.

- •

Less emphasis on direct-to-consumer online sales compared to insurtechs.

- •

Brand is more associated with supplemental health than traditional life insurance.

- •

Commission rates for agents may be lower than some competitors.

Differentiators

- •

Iconic brand mascot (Aflac Duck).

- •

Worksite sales model.

- •

Specialization in supplemental benefits.

- →

Mutual of Omaha

Market Share Estimate:1.84% (ranked 15th).

Target Audience Overlap:High

Competitive Positioning:A well-established, policyholder-owned company with a strong reputation, offering a broad portfolio of insurance and financial products, particularly strong in Medicare Supplement and life insurance.

Strengths

- •

Strong brand recognition and reputation for reliability.

- •

Diverse product portfolio including life, health, annuities, and investments.

- •

Recognized for a strong digital user experience.

- •

Mutual company structure (owned by policyholders) can build trust.

Weaknesses

- •

Can be perceived as more traditional and less innovative than newer players.

- •

Customer ratings on product quality are moderate, ranking below some key competitors.

- •

Distribution is still heavily reliant on a traditional agent network.

Differentiators

- •

Mutual ownership structure.

- •

Strong position in the Medicare Supplement market.

- •

Long-standing brand history and 'Wild Kingdom' association.

- →

New York Life Insurance Company

Market Share Estimate:6.35% (ranked 3rd).

Target Audience Overlap:Medium

Competitive Positioning:A premium, policyholder-owned mutual company with a reputation for financial strength and a highly trained career agent force, targeting a slightly more affluent market but overlapping in the middle market.

Strengths

- •

Top-tier brand reputation and financial strength ratings.

- •

Large, professional, and well-regarded career agent force.

- •

Mutual company structure aligns interests with policyholders.

- •

Extensive product portfolio including life, long-term care, and investment products.

Weaknesses

- •

Products can be more expensive than competitors like Globe Life.

- •

Complex products often require agent involvement, limiting direct-to-consumer appeal.

- •

Sales process can be longer and more involved.

- •

Less focused on the simple, low-face-value policies that are Globe Life's specialty.

Differentiators

- •

Mutual ownership structure.

- •

Emphasis on career agent professionalism and training.

- •

Strong brand associated with financial stability and trust.

- →

Colonial Life & Accident Insurance Company

Market Share Estimate:Significant in voluntary benefits space

Target Audience Overlap:High

Competitive Positioning:A leading provider of voluntary, employee-paid benefits sold at the worksite, very similar to Aflac. Positions itself as a partner to businesses to protect their workers.

Strengths

- •

Deep expertise in worksite marketing and enrollment solutions.

- •

Strong relationships with businesses and brokers.

- •

Offers a wide array of supplemental products (disability, accident, life, etc.).

- •

Backed by a large parent company (Unum Group).

Weaknesses

- •

Limited brand recognition among the general public compared to Aflac or Globe Life.

- •

Primarily reliant on the worksite channel, with less focus on individual D2C sales.

- •

Business model is vulnerable to economic downturns that affect employment levels.

Differentiators

- •

Focus exclusively on the worksite voluntary benefits market.

- •

One-on-one benefits counseling for employees during enrollment.

- •

Sister company of Unum, a leader in disability insurance.

Indirect Competitors

- →

Ethos Life

Description:An insurtech company acting as a technology-driven insurance distributor. It leverages data and AI to offer a fast, online application process for term and whole life insurance with often no medical exam required.

Threat Level:High

Potential For Direct Competition:Ethos is already a direct competitor in the online D2C space, directly challenging Globe Life's 'Buy Online' value proposition with a superior user experience.

- →

Ladder Life

Description:A digital-first insurance platform focused exclusively on flexible term life insurance. Their key differentiator is the ability for policyholders to easily increase or decrease their coverage online as their needs change (the 'laddering' concept).

Threat Level:Medium

Potential For Direct Competition:Ladder directly competes for the segment of the market that prefers a purely digital, self-service experience, a growing threat to Globe Life's less modern online offerings.

- →

Workplace Benefits

Description:Life and supplemental health insurance offered through employers as part of a benefits package. This channel (e.g., benefits provided by companies like MetLife, Prudential, Unum) competes for the same customer dollars before they reach the open market.

Threat Level:High

Potential For Direct Competition:This is a fundamental, ongoing form of indirect competition. As more employers offer robust benefits, the need for individuals to seek out their own primary coverage from companies like Globe Life can be reduced.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Multi-Channel Distribution Network

Sustainability Assessment:Globe Life's ability to sell via agents, mail, phone, and online provides broad market access that purely digital or purely agent-driven competitors lack. This hybrid model is a durable strength.

Competitor Replication Difficulty:Medium

- Advantage:

Established Brand in the Middle Market

Sustainability Assessment:With over a century of history, the brand has recognition among its target demographic of working families, which can be a barrier to newer entrants.

Competitor Replication Difficulty:Hard

- Advantage:

Large Existing Policyholder Base

Sustainability Assessment:A substantial customer base provides a stable stream of premium revenue and opportunities for cross-selling and up-selling new products.

Competitor Replication Difficulty:Hard

Temporary Advantages

- Advantage:

Simple Application Process

Estimated Duration:1-3 Years

Sustainability Assessment:While currently a key selling point, insurtech competitors are rapidly innovating to make their digital application processes even faster and more seamless, eroding this advantage.

Disadvantages

- Disadvantage:

Outdated Digital Customer Experience

Impact:Major

Addressability:Moderately

Description:The website, particularly the broken 'Find an Agent' functionality, indicates an underinvestment in digital channels compared to insurtech competitors, potentially deterring digitally-native customers.

- Disadvantage:

Perception as a Traditional/Legacy Insurer

Impact:Major

Addressability:Difficult

Description:The brand may be perceived as less innovative or tech-savvy, making it harder to attract younger demographics who prioritize digital convenience and modern brand identities.

- Disadvantage:

Dependence on Simplified Underwriting

Impact:Minor

Addressability:Moderately

Description:While simple applications are an advantage, they may lead to less competitive pricing for healthier individuals compared to companies using more sophisticated, data-driven underwriting.

Strategic Recommendations

Quick Wins

- Recommendation:

Immediately Fix and Enhance the 'Find an Agent' Web Tool

Expected Impact:High

Implementation Difficulty:Easy

Details:A non-functional core feature damages credibility and creates a poor customer experience. Fixing this is critical to supporting the agent-driven sales channel.

- Recommendation:

Prominently Feature Customer Testimonials on the Homepage

Expected Impact:Medium

Implementation Difficulty:Easy

Details:Add social proof to build trust and highlight the value proposition for working families, countering the abstract nature of insurance.

Medium Term Strategies

- Recommendation:

Overhaul the Online Quoting and Application Process

Expected Impact:High

Implementation Difficulty:Difficult

Details:Invest in a modern, mobile-first UI/UX to create a seamless, fast, and intuitive digital purchasing experience that can compete directly with insurtechs like Ethos and Ladder.

- Recommendation:

Develop Targeted Digital Marketing Campaigns

Expected Impact:Medium

Implementation Difficulty:Moderate

Details:Create specific digital campaigns for products like 'Final Expense' or 'Mortgage Protection' targeting relevant demographics on platforms like Facebook and through search engine marketing.

Long Term Strategies

- Recommendation:

Invest in a Unified Customer Relationship Management (CRM) Platform

Expected Impact:High

Implementation Difficulty:Difficult

Details:Integrate customer data across all four sales channels (online, mail, phone, agent) to provide a single view of the customer, enabling better service, targeted cross-selling, and personalized communication.

- Recommendation:

Modernize the Agent Toolkit

Expected Impact:High

Implementation Difficulty:Difficult

Details:Equip agents with digital tools (e.g., tablets with quoting software, CRM access, e-applications) to bridge the gap between high-touch personal service and digital efficiency.

Reinforce the position as the most accessible and reliable insurance provider for working families. Emphasize the unique strength of choice—'Your Life, Your Choice, Your Way'—highlighting the convenience of buying online, by mail, over the phone, or with a local agent, a flexibility that purely digital or purely traditional competitors cannot match.

Differentiate on the basis of 'Omni-channel Convenience.' While competitors focus on being either the best digital provider or the best agent-led provider, Globe Life can win by being the best at letting the customer choose their preferred channel seamlessly.

Whitespace Opportunities

- Opportunity:

Develop Products for the Gig Economy Workforce

Competitive Gap:Many traditional and worksite competitors focus on full-time, salaried employees. Gig workers and independent contractors are an underserved market for simple, portable life and supplemental health benefits.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Create an Educational 'Insurance 101' Digital Hub

Competitive Gap:While the website has articles, there's a gap for a comprehensive, interactive resource hub designed for first-time insurance buyers in the 'working families' demographic. This can build trust and generate leads.

Feasibility:High

Potential Impact:Medium

- Opportunity:

Offer Bundled 'Family Protection' Packages

Competitive Gap:Competitors often sell life and supplemental health as separate products. There is an opportunity to create straightforward, pre-packaged bundles (e.g., Term Life + Accident Insurance) at a slight discount, simplifying the choice for busy families.

Feasibility:Medium

Potential Impact:Medium

Globe Life operates in the mature and highly regulated U.S. life insurance market, positioning itself as a provider of simple, accessible insurance for 'working families.' Its core competitive advantage is its unique multi-channel distribution model, allowing customers to purchase policies online, through the mail, over the phone, or via a local agent. This flexibility provides a broad market reach that purely digital insurtechs or traditional agent-focused carriers lack.

Direct competitors like Aflac and Colonial Life are formidable, particularly in the worksite marketing space for supplemental health benefits, an area where Globe Life also competes. Mutual of Omaha and New York Life compete on the basis of brand trust and a broad product portfolio, with New York Life targeting a more affluent segment but still overlapping in the middle market. Globe Life's key differentiators against these players are its emphasis on simplicity and its direct-to-consumer channels (mail, phone, web), which have been part of its model for decades.

The most significant threat comes from indirect competitors, specifically insurtech disruptors like Ethos and Ladder. These companies offer a superior, seamless digital-first experience that makes Globe Life's online presence appear dated. The fact that Globe Life's 'Find an Agent' tool is non-functional is a critical tactical failure that undermines its multi-channel promise and cedes ground to tech-savvy rivals. While the direct-to-consumer market is still evolving and has faced challenges, the underlying consumer expectation for digital convenience is a permanent trend.

Strategically, Globe Life is at a crossroads. Its historical strengths—brand recognition and a diverse distribution network—remain valuable but are insufficient to guarantee future growth. The company's 'simple application' value proposition is being rapidly eroded by insurtechs who offer not just simplicity but also speed and data-driven personalization. The primary whitespace opportunity lies in better serving niche segments within its broad 'working families' target market, such as the growing gig economy workforce, and in creating a truly seamless omni-channel experience where a customer can start the process online and finish with an agent without friction.

Immediate recommendations include fixing critical website functionality and better leveraging social proof. Longer-term strategy must focus on a significant investment in digital transformation, not to abandon its traditional channels, but to modernize and integrate them, thereby turning its multi-channel approach from a collection of silos into a powerful, sustainable competitive advantage.

Messaging

Message Architecture

Key Messages

- Message:

In 2024, Globe Life paid $1,856,086,935 in claims.

Prominence:Primary

Clarity Score:High

Location:Top banner, above the fold

- Message:

Globe Life Insurance Helps Protect Your Family.

Prominence:Primary

Clarity Score:High

Location:Main headline (H1)

- Message:

Globe Life offers several convenient ways to purchase life and supplemental health products to suit your needs (Online, Mail, Agent, Phone).

Prominence:Secondary

Clarity Score:High

Location:Mid-page section

- Message:

Our life and supplemental health insurance products have simple, Yes/No applications that are easy to understand...

Prominence:Secondary

Clarity Score:High

Location:Body content in 'Why choose coverage with Globe Life?'

- Message:

At Globe Life, everything we do is to help Make Tomorrow Better.

Prominence:Tertiary

Clarity Score:Medium

Location:Tagline, end of 'Why choose' section, community section

The message hierarchy is strong and logical. The most powerful message—the massive dollar amount of claims paid—is placed at the very top, immediately establishing credibility and scale. This is followed by the core emotional benefit ('Helps Protect Your Family'). Functional differentiators like convenience and simplicity are presented next, which is a sensible flow from 'why' to 'how'. The corporate mission ('Make Tomorrow Better') is appropriately used as a supporting message.

Messaging is highly consistent across the homepage. The core themes of family protection, financial security, convenience, and simplicity are repeated and reinforced in headlines, body copy, and section titles. There is no discernible conflicting information, creating a unified and clear narrative.

Brand Voice

Voice Attributes

- Attribute:

Reassuring

Strength:Strong

Examples

- •

help protect your loved ones from financial stress

- •

Providing working families protection against the unexpected is a responsibility we don’t take lightly

- •

You and your family will always be our highest priority

- Attribute:

Direct & Simple

Strength:Strong

Examples

- •

simple, Yes/No applications

- •

we discuss policy benefits in everyday, straightforward language

- •

It’s that simple.

- Attribute:

Traditional & Established

Strength:Moderate

Examples

- •

For more than a century, we’ve secured the financial futures of working families

- •

committed to doing what is right and fair

- •

Globe Life is experienced and committed

Tone Analysis

Paternalistic & Protective

Secondary Tones

- •

Trustworthy

- •

Straightforward

- •

Community-Oriented

Tone Shifts

The tone shifts from being highly customer-focused and protective ('Helps Protect Your Family') to more corporate and philanthropic in the lower sections about community pledges and the Globe Life Foundation. This is a standard and acceptable shift.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Globe Life provides simple, accessible, and reliable life and health insurance for working families, with the unique convenience of being able to apply and purchase through multiple channels (online, mail, phone, or agent) to fit any comfort level or need.

Value Proposition Components

- Component:

Multi-Channel Convenience

Clarity:Clear

Uniqueness:Unique

- Component:

Application Simplicity

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Financial Stability & Reliability

Clarity:Clear

Uniqueness:Common

- Component:

Focus on 'Working Families'

Clarity:Clear

Uniqueness:Somewhat Unique

Globe Life's primary point of differentiation is its multi-channel purchasing model. While competitors may offer online quotes or agent meetings, explicitly promoting four distinct paths (including direct mail) is a powerful differentiator that caters to a broad demographic, particularly those who may be less tech-savvy or prefer traditional methods. The emphasis on 'simple, Yes/No applications' further distinguishes them from the often complex and jargon-filled insurance industry. While financial stability is a common claim, they substantiate it effectively with the large claims-paid figure.

The messaging positions Globe Life as the practical, no-nonsense insurance provider for middle-income America. It avoids the complex financial planning language of high-end insurers and the purely digital, impersonal approach of insurtech startups. It carves out a niche as a trustworthy and accessible option for families who value security and simplicity over sophisticated investment features.

Audience Messaging

Target Personas

- Persona:

The Budget-Conscious Head of Household: A primary earner in a 'working family' who is likely time-poor, seeks straightforward solutions, and is concerned about protecting their family's financial future without overcomplicating things.

Tailored Messages

- •

Globe Life Insurance Helps Protect Your Family

- •

designed and priced to fit any need or budget

- •

simple, Yes/No applications

Effectiveness:Effective

- Persona:

The Traditionalist/Less Tech-Savvy Buyer: An older individual or someone who prefers tangible, traditional business interactions. They may be wary of online-only services.

Tailored Messages

- •

Buy Through the Mail

- •

Meet with an Agent

- •

Call us at 800-831-1200

Effectiveness:Effective

- Persona:

Seniors & Retirees: Individuals on or nearing Medicare, concerned with out-of-pocket healthcare costs.

Tailored Messages

- •

Medicare Supplement insurance

- •

Final Expense Insurance

- •

What are Lifetime Reserve Days for Medicare Part A?

Effectiveness:Somewhat Effective

Audience Pain Points Addressed

- •

The complexity and confusion of buying insurance ('simple, Yes/No applications').

- •

The fear of a company not paying out claims ('paid $1,856,086,935 in claims').

- •

The inconvenience of the application process ('several convenient ways to purchase').

- •

The financial burden left on a family after an unexpected death or illness ('protect your loved ones from financial stress').

Audience Aspirations Addressed

- •

Achieving peace of mind about their family's future.

- •

Being a responsible protector and provider for their loved ones.

- •

Making a smart, simple financial decision without hassle.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Security & Fear Mitigation

Effectiveness:High

Examples

- •

Helps Protect Your Family

- •

protection against the unexpected

- •

protect your loved ones from financial stress

- Appeal Type:

Trust & Reliability

Effectiveness:High

Examples

- •

In 2024, Globe Life paid $1,856,086,935 in claims.

- •

For more than a century

- •

committed to doing what is right and fair

Social Proof Elements

{'proof_type': 'Scale of Operations (Claims Paid)', 'impact': 'Strong'}

{'proof_type': "Longevity & Heritage ('For more than a century')", 'impact': 'Moderate'}

Trust Indicators

- •

Displaying the massive dollar amount of claims paid

- •

Highlighting the company's long history ('more than a century')

- •

Showcasing community involvement (National Medal of Honor Museum, Globe Life Foundation)

- •

Providing multiple, clear contact methods (Phone, Mail, Agent, Online)

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

Get an Instant Quote and Apply Online

Location:Convenience section

Clarity:Clear

- Text:

Get Info by Mail

Location:Convenience section

Clarity:Clear

- Text:

Meet with an Agent

Location:Convenience section

Clarity:Clear

- Text:

Call us at 800-831-1200

Location:Convenience section

Clarity:Clear

The CTAs are highly effective. They are clear, concise, and directly tied to the unique value proposition of multi-channel convenience. By offering four distinct and equally weighted CTAs, Globe Life effectively segments its audience by their preferred method of interaction, reducing friction and increasing the likelihood of conversion for different user types.

Messaging Gaps Analysis

Critical Gaps

Lack of Human-Centric Storytelling: The site is missing customer testimonials, case studies, or relatable stories. The tagline 'Who's Your Beneficiary?™' is a powerful narrative hook that is completely unexplored. Showing, not just telling, how Globe Life has helped families would significantly increase emotional connection.

No Product-Level Differentiation: While the corporate value proposition is clear, the individual product descriptions are generic (e.g., 'Term and whole life insurance solutions designed with your family in mind'). There's no clear message on why a customer should choose Globe Life's Term Life over a competitor's.

Contradiction Points

No itemsUnderdeveloped Areas

The 'Make Tomorrow Better' Narrative: This corporate tagline is present but feels disconnected from the core product messaging. It's used in the context of community giving but isn't effectively woven into the customer-benefit story.

Agent Value Proposition: The 'Meet with an Agent' option is presented as a channel, but the value of an agent (e.g., personalized advice, needs analysis) is not messaged, potentially undervaluing that channel compared to the direct options.

Messaging Quality

Strengths

- •

Crystal Clear Core Proposition: The messaging around family protection, simplicity, and convenience is exceptionally clear and easy to understand.

- •

Powerful Social Proof: The prominent placement of the claims-paid statistic is a highly effective and persuasive use of data to build immediate trust.

- •

Effective Audience Targeting: The language, simplicity, and channel options are well-aligned with their target demographic of 'working families'.

- •

Action-Oriented CTAs: The calls to action are unambiguous and cater to a wide range of customer preferences.

Weaknesses

- •

Overly Functional and Lacks Emotion: The messaging is very rational and functional. It explains the 'what' and 'how' but fails to connect on a deeper emotional level through storytelling.

- •

Generic and Impersonal Tone: The brand voice, while consistent, feels corporate and lacks personality. It could be perceived as dated compared to more modern, customer-centric brands.

- •

Fails to Build a Brand Beyond the Product: The messaging focuses entirely on the insurance product and process. There is little effort to build a brand that customers feel an affinity for.

Optimization Roadmap

Priority Improvements

- Area:

Emotional Connection & Storytelling

Recommendation:Develop a 'Beneficiary Stories' section featuring short, powerful video or written testimonials from real customers. This would directly support the 'Who's Your Beneficiary?™' tagline and transform the abstract promise of protection into a tangible, emotional reality.

Expected Impact:High

- Area:

Value Proposition Communication

Recommendation:On the homepage, A/B test a new headline that is more emotionally resonant. For example, instead of 'Helps Protect Your Family,' test something like 'The Promise You Make to Them, Secured.'

Expected Impact:Medium

- Area:

Audience Messaging

Recommendation:Create dedicated, simplified landing pages for each of the four main purchasing paths ('Buy Online', 'By Mail', etc.). Each page should reinforce why that specific path is a great choice, tailored to the mindset of the user who selected it.

Expected Impact:Medium

Quick Wins

- •

In the 'Why choose Globe Life?' section, add a bulleted list to summarize the key benefits (Simplicity, Convenience, Reliability, History) for better scannability.

- •

Expand the 'Meet with an Agent' section with a short sentence on the benefit of personalized advice.

- •

Add customer satisfaction ratings or awards if available, as additional social proof.

Long Term Recommendations

- •

Invest in brand-level content marketing that tells stories about family, legacy, and 'Making Tomorrow Better' in a way that transcends the insurance product itself.

- •

Conduct persona research to refine messaging for different life stages (e.g., new parents, pre-retirees, small business owners) to move beyond the generic 'working families' segment.

- •

Evolve the brand voice to be more empathetic and human, using more 'you' and 'your family' language and less 'we' and 'our company' language.

Globe Life's strategic messaging is highly effective at achieving its primary business objective: converting security-seeking, middle-income families by emphasizing simplicity, reliability, and unparalleled purchasing convenience. The message architecture is logical and powerful, leading with a multi-billion dollar social proof point that immediately addresses the core industry pain point of claim reliability. The brand's key differentiator—its multi-channel purchasing model—is clearly articulated and supported by direct, action-oriented CTAs that cater to a broad demographic.

However, the messaging is overwhelmingly functional and rational, operating on a foundational level of fear-mitigation and practicality. This leaves a significant opportunity on the table for building a more resilient, emotionally resonant brand. The current messaging successfully acquires customers by being a simple and safe choice, but it does not build brand affinity that would make it the only choice.

The most critical gap is the absence of human-centric storytelling. The messaging explains the features of the shield but never tells the stories of the people it protects. By failing to build a narrative around its powerful 'Who's Your Beneficiary?™' concept, the brand feels impersonal and corporate. To achieve next-level growth and defend against more modern, story-driven competitors, the optimization roadmap must focus on infusing the brand with genuine emotional connection, transforming it from a mere utility into a trusted partner in protecting family legacies.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Long-standing market presence since 1900, indicating sustained demand.

- •

Over 17 million policies in force, more than any other single life insurance provider.

- •

Clear value proposition targeting underserved lower-middle to middle-income families with simple, accessible products.

- •

Multi-channel distribution (Online, Mail, Agent, Phone) caters to a wide range of customer preferences within their target demographic.

- •

Consistent payment of claims, with over $1.8 billion paid in 2024, builds trust and reinforces the core product value.

Improvement Areas

- •

Enhance digital product personalization to compete with Insurtech offerings.

- •

Develop products specifically tailored to the financial needs and buying habits of younger demographics (Millennials and Gen Z).

- •

Improve the seamlessness of the online-to-agent customer journey.

Market Dynamics

2% to 6% projected for the U.S. individual life insurance market in 2025.

Mature

Market Trends

- Trend:

Digital Transformation and Insurtech Growth

Business Impact:Increased competition from digital-first insurers and rising consumer expectations for seamless online experiences. Creates an urgent need for Globe Life to enhance its direct-to-consumer (D2C) channel.

- Trend:

Demand for Supplemental Health and Hybrid Products

Business Impact:Growing consumer awareness of health-related financial risks creates significant cross-selling and upselling opportunities for Globe Life's supplemental health products.

- Trend:

Personalization and Data Analytics

Business Impact:Shift from one-size-fits-all products to tailored coverage. Requires investment in data analytics to better underwrite risk and customize offerings, moving beyond simple 'Yes/No' applications.

- Trend:

Demographic Shifts (Aging Population and Younger Buyers)

Business Impact:Aging population drives demand for Medicare Supplement products, a key area for Globe Life. Younger buyers (Millennials/Gen Z) demand digital-first engagement, posing a challenge to traditional agent-led models.

Favorable. While the market is mature, current trends like the focus on financial security, the need for supplemental health coverage, and the growth of the middle-income market align well with Globe Life's core offerings. The primary challenge is adapting to the speed of digital change.

Business Model Scalability

Medium

The model has high variable costs tied to agent commissions, which can be substantial for new policies. Digital and direct mail channels offer a more scalable, lower variable cost structure.

Moderate. The core insurance product is digitally scalable, but the heavy reliance on a large, growing agent force (a key part of their strategy) limits operational leverage and requires significant ongoing investment in recruitment and training.

Scalability Constraints

- •

Dependence on agent network growth for a significant portion of sales.

- •

Potential for legacy IT systems to hinder rapid development of digital products and services.

- •

Managing compliance and quality control across a large, distributed agent network.

Team Readiness

Experienced leadership team accustomed to managing a large, profitable insurance enterprise. The key challenge is fostering a culture of rapid digital innovation alongside a traditional sales culture.

The structure is well-suited for managing existing, distinct business lines (e.g., Liberty National, Family Heritage). However, it may create silos that hinder the creation of a seamless, unified, and digitally-native customer experience.

Key Capability Gaps

- •

Digital Product Management and UX/UI Design to create a best-in-class online experience.

- •

Advanced Data Science and Analytics for dynamic underwriting, pricing, and marketing personalization.

- •

Growth Marketing expertise focused on digital customer acquisition and conversion rate optimization.

Growth Engine

Acquisition Channels

- Channel:

Exclusive and Independent Agent Network

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip agents with superior digital tools (CRM, personalized sales funnels, social media content) to increase their efficiency and reach, particularly with younger demographics.

- Channel:

Direct to Consumer (D2C) - Online

Effectiveness:Medium

Optimization Potential:High

Recommendation:Overhaul the online quote-to-purchase journey. Implement A/B testing, streamline the application, and provide instant underwriting decisions for simpler products to compete with Insurtechs.

- Channel:

Direct Mail

Effectiveness:Medium

Optimization Potential:Low

Recommendation:Integrate direct mail with digital campaigns (e.g., QR codes to personalized landing pages) and use data analytics to improve targeting and ROI.

- Channel:

Content Marketing / SEO

Effectiveness:Low

Optimization Potential:High

Recommendation:Expand the article library to target a wider range of financial wellness and life-event keywords. Develop more engaging content formats like videos, calculators, and webinars to capture top-of-funnel interest.

Customer Journey

The website presents multiple, clear but separate conversion paths (Online, Mail, Agent, Phone). The journey appears straightforward but lacks a sophisticated, integrated digital experience.

Friction Points

- •

Potential disconnect when moving from online information gathering to speaking with an agent.

- •

The online application process is not transparent; its simplicity and speed are claimed but not demonstrated.

- •

Lack of digital tools for self-service comparison and needs-analysis, pushing customers to agent or phone channels prematurely.

Journey Enhancement Priorities

{'area': 'Online Quote & Apply Process', 'recommendation': 'Implement a fully digital, mobile-first application process with AI-driven instant underwriting for term life products. '}

{'area': 'Channel Integration', 'recommendation': 'Develop an omnichannel customer profile allowing users to start online, save progress, and seamlessly transition to a call or agent meeting without repeating information.'}

Retention Mechanisms

- Mechanism:

Core Product Stickiness

Effectiveness:High

Improvement Opportunity:Life insurance has naturally high retention. This can be improved by more proactive communication regarding policy value and benefits.

- Mechanism:

Cross-selling/Upselling

Effectiveness:Moderate

Improvement Opportunity:Systematically target existing life policyholders with supplemental health or children's life insurance offers based on life events (e.g., mortgage, childbirth, reaching Medicare eligibility age).

- Mechanism:

Brand Trust & Claims Payment

Effectiveness:High

Improvement Opportunity:Continuously highlight the company's financial strength and history of paying claims in customer communications and marketing materials to reinforce trust.

Revenue Economics

Likely positive but varies significantly by channel. The agent-led model has a high Customer Acquisition Cost (CAC) but potentially higher Customer Lifetime Value (LTV) through stronger relationships and cross-selling. The D2C channel should aim for a much lower CAC to be competitive.

Undeterminable without internal data. However, the life insurance industry generally has a high LTV due to long policy durations. A key challenge is managing the high upfront CAC, especially agent commissions.

Moderate. The company is profitable and growing, but there is a significant opportunity to improve efficiency by scaling the lower-cost D2C channel and improving digital marketing ROI.

Optimization Recommendations

- •

Invest heavily in optimizing the D2C channel's conversion rate to lower the blended CAC.

- •

Develop a robust customer referral program for both agents and direct customers.

- •

Focus marketing efforts on acquiring customers with a high propensity to buy multiple policies over their lifetime.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Systems

Impact:High

Solution Approach:Adopt a two-speed IT architecture, maintaining legacy systems for policy administration while building a modern, API-driven front-end for a flexible and fast digital customer experience.

- Limitation:

Siloed Customer Data

Impact:Medium

Solution Approach:Implement a Customer Data Platform (CDP) to create a single view of the customer across all channels (D2C, agent, phone) to enable personalization and omnichannel service.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting Processes

Growth Impact:Slows down customer acquisition, especially in the D2C channel, and increases operational costs.

Resolution Strategy:Invest in AI and machine learning-based underwriting platforms to automate and accelerate decisions for a majority of applications.

- Bottleneck:

Agent Recruitment and Onboarding

Growth Impact:Scaling the primary sales channel is dependent on the ability to attract, train, and retain a large number of agents.

Resolution Strategy:Develop a more efficient, technology-enabled onboarding and continuous training program for agents. Improve agent value proposition with better digital tools and lead generation support.

Market Penetration Challenges

- Challenge:

Intense Competition from Insurtechs

Severity:Major

Mitigation Strategy:Compete by leveraging brand trust and financial stability while aggressively investing in a superior digital D2C experience. Acquire or partner with Insurtechs to accelerate technology adoption.

- Challenge:

Brand Perception with Younger Demographics

Severity:Major

Mitigation Strategy:Launch a targeted brand campaign focused on digital channels (social media, content marketing) that speaks to the financial concerns of Millennials and Gen Z. Simplify product offerings for this audience.

- Challenge:

Commoditization of Simple Products

Severity:Minor

Mitigation Strategy:Focus on the value of human advice (via agents) for more complex needs while offering competitive, simple products online. Emphasize brand, service, and reliability over price alone.

Resource Limitations

Talent Gaps

- •

Digital Growth & Performance Marketing

- •

Data Science & AI/ML Engineering

- •

Modern Product Management

As a profitable public company, capital is not a primary constraint. The challenge is allocating capital effectively towards technology and digital transformation initiatives versus traditional channels like agent expansion.

Infrastructure Needs

Cloud-based, scalable infrastructure to support modern digital applications and data analytics.

Modern marketing technology (Martech) stack, including a CDP and marketing automation platform.

Growth Opportunities

Market Expansion

- Expansion Vector:

Younger Demographics (Ages 25-40)

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Develop a digital-first sub-brand or product line with simplified language, mobile-native experience, and marketing focused on platforms like Instagram, TikTok, and YouTube.

- Expansion Vector:

Hispanic Middle-Market

Potential Impact:Medium

Implementation Complexity:Medium

Recommended Approach:Develop culturally relevant marketing campaigns and bilingual support across all channels (online, phone, agent materials). Partner with community influencers.

Product Opportunities

- Opportunity:

Modular / Customizable Online Policies

Market Demand Evidence:Insurtech success with customizable coverage (e.g., Ladder) shows demand for flexibility.

Strategic Fit:Evolves the 'simple' value proposition to 'simple and flexible,' appealing to digital-native consumers.

Development Recommendation:Pilot a modular term life product online where users can easily adjust coverage amounts and term lengths and add/remove riders.

- Opportunity:

Wellness-Integrated Supplemental Health Products

Market Demand Evidence:Growing consumer trend towards proactive health and wellness.

Strategic Fit:Strengthens the value proposition of health products and provides more touchpoints with customers.

Development Recommendation:Partner with health and wellness apps to offer premium discounts or rewards for healthy behaviors, integrating this into new or existing health policies.

Channel Diversification

- Channel:

Embedded Insurance / Partnerships

Fit Assessment:High. Aligns with reaching customers at key life moments.

Implementation Strategy:Develop APIs to partner with mortgage lenders, credit unions, and financial planning platforms to offer life or mortgage protection insurance at the point of sale.

- Channel:

Worksite / Employer Benefits

Fit Assessment:Medium. Competes with established players but leverages existing product portfolio.

Implementation Strategy:Develop a streamlined platform for small-to-medium-sized businesses to offer Globe Life's supplemental health and life products as voluntary benefits.

Strategic Partnerships

- Partnership Type:

Technology / Insurtech

Potential Partners

- •

AI underwriting platforms

- •

Digital claims processing providers

- •

UX/UI design agencies specializing in fintech

Expected Benefits:Accelerate digital transformation, reduce operational costs, and improve customer experience without building all capabilities in-house.

- Partnership Type:

Affinity Groups

Potential Partners

- •

AARP

- •

Alumni Associations

- •

Professional Organizations

Expected Benefits:Access to large, targeted customer bases with a trusted endorsement, potentially lowering customer acquisition costs.

Growth Strategy

North Star Metric

Number of Active Policies In Force

This metric combines new customer acquisition with retention (persistency), reflecting the long-term health and growth of the business. It aligns the entire organization on both selling new policies and serving existing policyholders.

Target a 5-7% year-over-year increase, outpacing the general market growth rate.

Growth Model

Hybrid: Performance Marketing + Sales-Led + Product-Led

Key Drivers

- •

Agent Productivity (policies per agent)

- •

D2C Funnel Conversion Rate

- •

Cross-Sell Rate (policies per household)

Continue to support and grow the agent channel (Sales-Led) while aggressively investing in the D2C channel (Performance Marketing). Begin introducing Product-Led elements like a seamless online experience, in-app upgrade paths, and a customer referral program.

Prioritized Initiatives

- Initiative:

Digital D2C Funnel Overhaul

Expected Impact:High

Implementation Effort:Medium

Timeframe:6-9 Months

First Steps:Map the current online customer journey, identify key drop-off points, and begin A/B testing new landing pages and quote forms.

- Initiative:

Agent Digital Enablement Toolkit

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:9-12 Months

First Steps:Survey top-performing agents to identify their needs. Pilot a new CRM and content-sharing platform with a select group of agents.

- Initiative:

Develop Millennial-Focused Term Life Product & Campaign

Expected Impact:High

Implementation Effort:High

Timeframe:12-18 Months

First Steps:Conduct market research and focus groups with the target demographic. Develop a product MVP (Minimum Viable Product) for online-only sales.

Experimentation Plan

High Leverage Tests

- Test:

Landing page messaging (e.g., 'Protection for Families' vs. 'Simple, Fast Online Insurance').

- Test:

Online quote form simplification (reducing number of fields).

- Test:

Call-to-Action variations ('Get Quote' vs. 'Apply Now' vs. 'See My Price').

Use a framework like AARRR (Acquisition, Activation, Retention, Referral, Revenue) tailored for the insurance funnel. Key metrics: Cost Per Quote, Quote-to-Application Rate, Application-to-Policy Rate, Cost Per Acquisition.

Run at least two concurrent A/B tests on the D2C website at all times, with a bi-weekly review of results and iteration planning.

Growth Team

A cross-functional 'Growth Squad' dedicated to the D2C channel, operating with autonomy and a dedicated budget. This team should report to a Head of Growth or Chief Digital Officer.

Key Roles

- •

Growth Product Manager

- •

Performance Marketing Manager (SEM/SEO/Social)

- •

Conversion Rate Optimization (CRO) Specialist

- •

Data Analyst

Hire key external talent for critical roles while upskilling current marketing and IT team members through training and involvement in growth experiments. Foster a 'test and learn' culture.

Globe Life Inc. possesses a formidable growth foundation built on a strong product-market fit within the middle-income family demographic, a long-standing brand reputation, and a powerful, diversified distribution model. The company is well-positioned to capitalize on stable market growth and demographic trends favoring its supplemental health and Medicare products.

The primary challenge and greatest opportunity for Globe Life lies in navigating the industry's digital transformation. While its traditional agent-led model is a current strength, it also presents scalability constraints and may not effectively reach younger, digital-native customer segments. The company's direct-to-consumer (D2C) channel is functional but appears to lack the sophistication and seamless user experience of modern Insurtech competitors, creating a significant barrier to capturing the next generation of policyholders.

Future growth is contingent on a dual strategy: empowering the existing agent network with modern digital tools to increase their efficiency and reach, while simultaneously aggressively investing to transform the D2C channel into a best-in-class, product-led growth engine. This requires not just capital, but a cultural shift towards rapid experimentation, data-driven decision-making, and a deep focus on the digital customer journey.

Key strategic imperatives should be:

1. Overhauling the digital funnel to offer a truly simple, fast, and mobile-first purchasing experience.

2. Expanding the product portfolio with more flexible and personalized options that appeal to a younger audience.

3. Leveraging data and analytics to create a single view of the customer, enabling effective cross-selling and personalized communication across all channels.

By successfully executing this hybrid strategy, Globe Life can leverage its established strengths in brand trust and market penetration to bridge the gap with digital innovators, securing sustainable growth and market leadership for the future.

Legal Compliance

Globe Life's website presence includes multiple privacy policies across different domains, which could create consumer confusion. While a main policy exists, it is not clearly accessible from the homepage content provided, a significant usability and compliance gap. The policy states it collects personal information you voluntarily provide and explains how it's used and shared. It includes a section for California Privacy Rights (CCPA/CPRA), allowing users to opt out of sharing information with third parties for direct marketing. However, the process requires an email or phone call, which is less user-friendly than a dedicated 'Do Not Sell/Share' link typically found in website footers. The policy also mentions that it follows industry standards for security but correctly notes that no system is impenetrable, a standard but important disclosure. A key concern is that data may be shared with third-party insurance carriers, and Globe Life disclaims responsibility for the privacy practices of those third parties, shifting a significant burden to the consumer.

A 'Terms and Conditions' page exists, though its visibility from the main marketing pages provided is not evident. The terms are broad and heavily favor the company. They include standard clauses such as limiting liability, disclaiming warranties ('AS IS' basis), and requiring users to indemnify Globe Life for any claims arising from their use of the site. The language is dense and likely challenging for the average consumer to understand fully. The terms prohibit commercial use of the site's content without prior written consent. From a strategic perspective, while these terms offer strong legal protection for the company, their lack of visibility and clarity could be challenged on the grounds of enforceability if a user claims they were not reasonably made aware of them.

The provided website content and available privacy policies show a significant deficiency in modern cookie compliance. There is no mention or evidence of a cookie consent banner or a granular consent management tool. This is a major gap under CPRA, VCDPA, and other state privacy laws that require opt-in or clear opt-out mechanisms for tracking and advertising cookies. One of the company's privacy policies states it does not use cookies to collect personal information but uses them to 'identify you to the web server', which is a functionally necessary but overly simplistic explanation that fails to address tracking technologies used for analytics or advertising. This lack of a clear consent mechanism for non-essential cookies presents a high risk of non-compliance with multiple state privacy laws.