eScore

jackhenry.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Jack Henry demonstrates a formidable digital presence within its specific niche of U.S. community and regional financial institutions. Content is expertly aligned with the B2B customer journey, establishing strong topical authority in areas like core modernization and digital banking. This focused strategy, however, results in a deliberately limited global reach and underdeveloped areas like voice search optimization, which are less critical for its enterprise sales model.

Deep content authority and thought leadership, exemplified by comprehensive resources like the '2025 Strategy Benchmark' that positions them as an educational partner.

Create dedicated, persona-based content hubs for high-value segments like 'De Novo Banks' and 'Fintech Partners' to dominate those niche search landscapes and improve lead quality.

The brand messaging is exceptionally consistent and effectively differentiates Jack Henry by emphasizing partnership, advocacy, and a pragmatic approach to modernization. This narrative is strong and resonates with their target audience's fear of disruption. However, the overall effectiveness is significantly weakened by understated and vague calls-to-action that lack urgency and fail to guide high-intent prospects to conversion points like demos or sales consultations.

A unique and defensible brand position as the 'advocate' for community financial institutions, which builds strong emotional resonance and trust.

A/B test the primary homepage CTA ('See Our Vision') against more direct, action-oriented alternatives like 'Explore the Platform' or 'Request a Demo' to increase high-intent lead generation.

The website provides a logical information architecture and a good responsive design, making the user journey relatively smooth. The primary friction points are the ineffective, low-prominence CTAs that fail to direct users toward conversion. A critical weakness is the lack of a visible Accessibility Statement, which not only impacts inclusive design but also poses a legal and reputational risk, particularly for a company serving the highly regulated financial sector.

A clear and logical information architecture that guides users from a high-level value proposition down to specific solutions and social proof, aligning well with the B2B buyer's journey.

Conduct a third-party accessibility audit against WCAG 2.1 AA standards and publish a formal Accessibility Statement to mitigate legal risk under the ADA and demonstrate a commitment to digital inclusion.

Credibility is extremely high, built upon a 45+ year history, a strong market position, and prominent trust signals like the strategic partnership with Google Cloud. The website effectively showcases third-party validation through testimonials and deep industry content. The primary weakness is the lack of quantifiable customer success metrics; while testimonials build trust, detailed case studies with tangible ROI data would provide more powerful proof for C-level decision-makers.

Leveraging the partnership with Google Cloud as a powerful trust signal, which lends significant credibility to their technology modernization and security strategy.

Develop a comprehensive library of in-depth case studies that feature specific, quantifiable business outcomes (e.g., 'reduced operational overhead by 15%', 'increased digital engagement by 25%') and showcase them prominently.

Jack Henry's competitive moat is exceptionally strong and sustainable, rooted in the high switching costs of core banking systems and deep, long-term client relationships. Their strategy to evolve into an open platform ecosystem is a forward-thinking move to build network effects, which will further deepen this moat. While smaller in scale than competitors like Fiserv and FIS, their focus on service and partnership for a specific niche is a powerful and defensible advantage.

Extremely high customer switching costs due to the mission-critical nature of their core processing solutions, which are deeply embedded in client operations.

Accelerate the development and adoption of the open API ecosystem by actively co-marketing solutions built by fintech partners to more rapidly build network effects and make the platform indispensable.

The business model is highly scalable, characterized by strong recurring revenue, excellent unit economics, and a zero-debt balance sheet that allows for self-funded growth. The strategic push to a cloud-native platform will further enhance scalability and margins. Expansion potential is strong in moving upmarket to larger FIs and targeting the fintech segment, though growth velocity is constrained by a US-only focus and a high-touch, lengthy enterprise sales cycle.

A robust financial model with a high percentage of recurring revenue (~85%), strong operating margins, and zero debt, providing a stable foundation for strategic investments in growth.

Develop a dedicated 'Fintech Partner Program' with streamlined onboarding and flexible pricing to capture the high-growth fintech segment and create a new revenue stream.

The business model demonstrates exceptional coherence, with a clear and consistent strategic focus on transforming into a cloud-native, open-platform provider. This strategy is perfectly timed with the market's demand for digital modernization and is supported by a stable, highly profitable revenue model. All facets of the business, from messaging to R&D investment, appear tightly aligned with this singular, well-articulated vision.

Excellent market timing and strategic focus, aligning the entire company's resources behind the pivot to a cloud-native, open-banking platform precisely when the industry is demanding such a shift.

Simplify the navigation and presentation of the vast 'What We Offer' menu to better reflect the core message of a single, unified platform, reducing perceived complexity.

As one of the 'Big Three' core providers, Jack Henry wields significant market power and influence within its niche. High switching costs grant them substantial pricing power and create a stable market share trajectory. Their influence is demonstrated by their ability to shape the modernization conversation around a 'pragmatic, gradual transition,' directly countering the strategies of more disruptive players. The primary concentration risk is their deep dependency on the health of the U.S. financial institution sector.

Significant pricing power derived from long-term contracts and the high costs and operational risks clients face when considering a switch to a competitor.

Sharpen messaging around their 'open API' strategy to create a stronger contrast with the perceived inflexibility of larger competitors, explicitly positioning it as a key technological and business advantage.

Business Overview

Business Classification

B2B Technology & Services Platform

Fintech SaaS/PaaS

Financial Technology (Fintech)

Sub Verticals

- •

Core Banking Solutions

- •

Digital Banking Platforms

- •

Payment Processing

- •

Cybersecurity & Fraud Prevention

- •

Lending Technology

- •

Data Analytics

Mature

Maturity Indicators

- •

Publicly traded company (NASDAQ: JKHY) since 1985.

- •

Established in 1976, demonstrating long-term market presence.

- •

Consistent revenue growth and profitability over multiple decades.

- •

Significant market share in the core banking provider space for community and regional financial institutions.

- •

Large, established customer base of approximately 7,400 institutions.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Services and Support

Description:Recurring revenue from data processing, hosting/cloud services, and ongoing software support and maintenance. This is a significant portion of revenue, representing over half of the total. Cloud services are a key growth driver within this stream.

Estimated Importance:Primary

Customer Segment:Banks, Credit Unions, and other Financial Institutions

Estimated Margin:High

- Stream Name:

Processing

Description:Transactional and usage-based fees from payment processing, including card transactions, digital payments, and other payment-related services. This is the second-largest revenue component.

Estimated Importance:Primary

Customer Segment:Banks, Credit Unions, and their end-customers (accountholders)

Estimated Margin:Medium

- Stream Name:

Professional Services & Consulting

Description:One-time or project-based fees for implementation, customization, consulting, and training services related to their technology platforms.

Estimated Importance:Secondary

Customer Segment:Banks, Credit Unions, De Novo Banks

Estimated Margin:Medium

Recurring Revenue Components

- •

SaaS subscriptions for digital banking platforms (e.g., Banno)

- •

Data processing and hosting fees (private/public cloud)

- •

Software support and maintenance contracts

- •

Usage-based payment processing fees

Pricing Strategy

Hybrid (Subscription, Usage-Based, and Fixed-Fee Contracts)

Premium/Mid-range

Opaque

Pricing Psychology

- •

Bundling (offering integrated suites of products)

- •

Long-term contracts (typically 7-10 years) to increase customer lifetime value and create high switching costs.

- •

Value-based pricing (aligning cost with the critical operational nature of their core systems).

Monetization Assessment

Strengths

- •

High percentage of recurring revenue provides stability and predictability.

- •

Strong customer retention due to high switching costs and deep integration into client operations.

- •

Diversified revenue streams across core processing, payments, and digital services reduces reliance on any single product line.

- •

Ability to cross-sell and upsell complementary solutions to a large, captive customer base.

Weaknesses

- •

Long sales cycles and complex enterprise contracts can slow new revenue acquisition.

- •

Dependence on the health of the U.S. banking and credit union sector.

- •

Potential pricing pressure from a highly concentrated competitive landscape.

Opportunities

- •

Transitioning more clients to cloud-native platforms can increase subscription revenue and margins.

- •

Expanding usage-based pricing for new API-driven services and open banking solutions.

- •

Developing premium, AI-powered analytics and security services as add-on modules.

- •

Offering more services to the emerging fintech segment, which is a growing customer category.

Threats

- •

Industry consolidation (bank mergers) can lead to a reduction in the total number of clients.

- •

Aggressive pricing from primary competitors like Fiserv and FIS.

- •

Emergence of nimble, cloud-native fintech startups that could erode market share for specific point solutions.

Market Positioning

Technology and service leader for community and regional financial institutions, emphasizing partnership, comprehensive solutions, and a people-first approach.

Major Player. Jack Henry is one of the 'Big Three' core providers in the U.S., serving approximately 21% of banks and 12% of credit unions.

Target Segments

- Segment Name:

Community & Regional Banks

Description:Small to mid-sized banks ($500M to $30B in assets) that require a comprehensive, integrated technology backbone to compete with larger institutions. Often value long-term partnerships and high-touch support.

Demographic Factors

Located across the United States

Varying asset sizes, typically below the top-tier national banks

Psychographic Factors

- •

Risk-averse and value stability and reliability.

- •

Focused on community relationships.

- •

Seeking to modernize but often lack large in-house IT development teams.

Behavioral Factors

- •

Prefer integrated solutions from a single vendor.

- •

Long decision-making cycles for core system changes.

- •

High value placed on regulatory compliance and security.

Pain Points

- •

Inability to innovate at the pace of larger banks or fintechs.

- •

Legacy technology stacks that are inefficient and difficult to integrate.

- •

Increasing pressure from regulatory compliance and cybersecurity threats.

- •

Competing for commercial and retail accountholders against digitally native options.

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Credit Unions

Description:Member-owned financial cooperatives of all sizes that prioritize member experience and financial wellness. They require technology that is both modern and aligns with their service-oriented mission.

Demographic Factors

Varying asset sizes, from small local CUs to large regional ones.

Psychographic Factors

- •

Highly focused on member service and satisfaction.

- •

Collaborative nature, often sharing best practices within the industry.

- •

Value vendors who understand the unique needs of the credit union model.

Behavioral Factors

Looking for technology that enhances the member journey.

Often utilize specific core platforms tailored to credit unions (e.g., Symitar).

Pain Points

- •

Keeping up with member expectations for digital services.

- •

Limited resources for technology investment compared to large banks.

- •

Operational efficiency challenges.

- •

Attracting and retaining younger members.

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Fintechs

Description:Emerging and established financial technology companies that need to integrate with the traditional banking ecosystem to offer their services, requiring access via APIs and open banking platforms.

Demographic Factors

Varies from startups to established tech companies.

Psychographic Factors

Focused on innovation, speed-to-market, and user experience.

Seek flexible and scalable technology partners.

Behavioral Factors

API-first integration approach.

Often focus on a specific niche in the financial services value chain.

Pain Points

- •

Gaining access to the banking system's infrastructure (payments, accounts).

- •

Navigating complex regulatory and compliance landscapes.

- •

Scaling their solutions by connecting with a broad network of financial institutions.

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Focus on Community & Regional Institutions

Strength:Strong

Sustainability:Sustainable

- Factor:

Customer Service and Partnership Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Open, API-First Technology Strategy

Strength:Moderate

Sustainability:Sustainable

- Factor:

Comprehensive, Integrated Product Suite

Strength:Strong

Sustainability:Sustainable

Value Proposition

To strengthen the connections between people and their financial institutions through a comprehensive, open, and modern technology ecosystem that empowers community and regional banks and credit unions to compete, innovate, and improve financial health.

Good

Key Benefits

- Benefit:

Operational Efficiency

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Integrated core, digital, and payment platforms.

- •

Cloud-native architecture for scalability and reduced maintenance.

- •

Automation of business processes.

- Benefit:

Competitive Modernization

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Banno Digital Platform for modern user experiences.

- •

Open API ecosystem for fintech integration.

- •

Ongoing investment in R&D and strategic acquisitions like Payrailz.

- Benefit:

Risk Reduction & Security

Importance:Critical

Differentiation:Common

Proof Elements

- •

Financial Crimes Defender™ suite.

- •

Partnership with Google Cloud for enhanced security.

- •

Solutions for cybersecurity, disaster preparedness, and regulatory compliance.

Unique Selling Points

- Usp:

A stated commitment to open banking and an API-first ecosystem, enabling clients to integrate with over 950 third-party fintechs.

Sustainability:Long-term

Defensibility:Moderate

- Usp:

A gradual, flexible technology modernization path, allowing clients to transition to a cloud-native platform over time without a disruptive 'rip-and-replace' of their existing core.

Sustainability:Medium-term

Defensibility:Strong

- Usp:

A singular focus on serving U.S. community and regional financial institutions, fostering deep domain expertise and a partnership-based culture.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

Legacy technology is hindering our ability to compete and serve our accountholders effectively.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

We lack the resources to develop and maintain a modern, secure, and compliant digital banking experience.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

We need to improve operational efficiency and reduce costs to maintain profitability.

Severity:Major

Solution Effectiveness:Partial

- Problem:

Integrating with innovative fintech solutions is complex and risky.

Severity:Major

Solution Effectiveness:Partial

Value Alignment Assessment

High

The value proposition directly addresses the existential challenges faced by community and regional financial institutions: the need to modernize, compete with larger players, and enhance efficiency in a rapidly changing digital landscape.

High

The messaging and solutions are tailored specifically to the pain points of community banks and credit unions, focusing on partnership, stability, and enabling them to serve their local communities better.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Google Cloud (for public cloud infrastructure)

- •

A network of over 950 third-party fintech companies (via API integrations)

- •

Payment networks (e.g., Visa, Mastercard, The Clearing House)

- •

Technology hardware providers (e.g., IBM for iSeries platforms)

Key Activities

- •

Software research & development

- •

Data hosting and cloud infrastructure management

- •

Customer service and technical support

- •

Payment and transaction processing

- •

Strategic acquisitions

- •

Sales and marketing to financial institutions

Key Resources

- •

Proprietary software and technology platforms (e.g., SilverLake, Symitar, Banno)

- •

Skilled workforce (engineers, support staff, industry experts)

- •

Extensive and loyal customer base

- •

Strong brand reputation and industry relationships

- •

Data centers and cloud infrastructure

Cost Structure

- •

Personnel costs (majority of expenses)

- •

Research and development

- •

Data center and cloud hosting costs

- •

Sales, general, and administrative (SG&A) expenses

- •

Third-party technology licensing fees

Swot Analysis

Strengths

- •

Entrenched position as a top-tier core provider with high customer switching costs.

- •

Strong, stable financial performance with a high proportion of recurring revenue.

- •

Comprehensive and diversified product portfolio covering the full spectrum of banking needs.

- •

Loyal customer base and a strong reputation for service and partnership.

Weaknesses

- •

Dependence on the U.S. financial services market, lacking geographic diversification.

- •

Perception of being a legacy provider, despite modernization efforts.

- •

Performance is closely tied to the health and consolidation trends of the banking sector.

Opportunities

- •

Accelerate the transition of the existing customer base to the new cloud-native Jack Henry Platform.

- •

Expand the open banking ecosystem, creating a platform-based revenue model by monetizing API access and fintech partnerships.

- •

Leverage AI and machine learning to offer advanced data analytics, personalization, and fraud detection services.

- •

Increase market share among larger financial institutions as the platform's scalability is proven.

Threats

- •

Intense competition from Fiserv and FIS, who are also investing heavily in modernization.

- •

Cybersecurity breaches, which could severely damage reputation and trust.

- •

Economic downturns that could slow down IT spending by financial institutions.

- •

Disruption from new, highly capitalized fintech challengers offering standalone, best-in-class solutions.

Recommendations

Priority Improvements

- Area:

Marketing & Communication

Recommendation:Aggressively market the technology modernization strategy to shift market perception from 'legacy provider' to 'innovative platform enabler'. Emphasize the 'open ecosystem' and 'cloud-native' aspects to attract new, tech-forward clients.

Expected Impact:High

- Area:

Product Strategy

Recommendation:Accelerate the development and migration path for the cloud-native Jack Henry Platform. Create incentive programs for existing clients to migrate from legacy core systems to the new platform, locking in future revenue streams.

Expected Impact:High

- Area:

Sales Strategy

Recommendation:Develop a dedicated sales and partnership team focused exclusively on the fintech segment. Create a streamlined onboarding process and flexible pricing models (e.g., usage-based) to capture this high-growth market.

Expected Impact:Medium

Business Model Innovation

- •

Launch a 'Fintech Marketplace' to formalize and monetize the open banking ecosystem. Charge fintechs for premium API access, certification, and co-marketing opportunities to the Jack Henry client base.

- •

Develop a 'Data-as-a-Service' (DaaS) offering, providing anonymized, aggregated data insights and benchmarking tools to financial institutions for a recurring fee.

- •

Explore 'Banking-as-a-Service' (BaaS) capabilities, enabling non-financial companies to embed banking products (e.g., accounts, payments) through the Jack Henry platform, creating a new customer category.

Revenue Diversification

- •

Expand consulting services beyond technology implementation to include strategic advice on digital transformation, efficiency optimization, and navigating the fintech landscape.

- •

Offer managed services for cybersecurity and compliance, moving beyond software to provide ongoing operational support for a premium subscription fee.

- •

Investigate targeted international expansion into markets with similar community banking structures, such as Canada or the UK, to reduce dependency on the U.S. market.

Jack Henry & Associates operates a robust and highly defensible business model, deeply embedded within the operational core of the U.S. community and regional financial institution landscape. As one of the 'Big Three' core providers, its primary strengths are a large, loyal customer base, significant recurring revenues, and high switching costs, which create a formidable competitive moat. The company has demonstrated a clear understanding of the primary threat to its long-term viability—technological disruption—and is actively executing a strategic transformation. The pivot towards an open, API-first, cloud-native platform, supported by a key partnership with Google Cloud, is a critical and necessary evolution. This strategy positions Jack Henry not just as a provider of core banking software, but as a central hub in a broader financial ecosystem. This shift is vital for retaining existing clients who need to innovate and for attracting new segments, particularly fintechs. The primary challenge will be the pace and execution of this transition, managing the migration of a large, risk-averse client base from legacy systems while simultaneously competing with other major incumbents and nimble startups. Future growth hinges on their ability to successfully evolve their business model from a service-oriented software provider to a platform-centric ecosystem orchestrator. Success in this transformation will unlock new revenue streams through fintech partnerships and data services, ensuring their relevance and continued steady growth for the next decade.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

High Customer Switching Costs

Impact:High

- Barrier:

Complex Regulatory & Compliance Requirements

Impact:High

- Barrier:

Long Sales & Implementation Cycles

Impact:High

- Barrier:

Significant Capital Investment for R&D

Impact:Medium

- Barrier:

Established Relationships & Brand Loyalty

Impact:Medium

Industry Trends

- Trend:

Shift to Cloud-Native & SaaS Models

Impact On Business:Requires significant R&D investment to modernize legacy platforms but offers recurring revenue and scalability. Jack Henry is actively pursuing this with its Google Cloud partnership.

Timeline:Immediate

- Trend:

Open Banking & API-Driven Ecosystems

Impact On Business:Demands a strategic shift from closed, monolithic systems to open platforms that integrate with third-party fintechs. This is a core part of Jack Henry's stated strategy.

Timeline:Immediate

- Trend:

AI & Machine Learning Integration

Impact On Business:Crucial for developing competitive solutions in fraud detection, data analytics, risk management, and personalized customer experiences.

Timeline:Near-term

- Trend:

Focus on Digital User Experience (UX)

Impact On Business:Financial institutions are demanding consumer-grade UX for their customers, pressuring core providers to deliver modern, intuitive digital banking front-ends.

Timeline:Immediate

- Trend:

Embedded Finance & BaaS (Banking-as-a-Service)

Impact On Business:Creates new revenue opportunities by enabling non-financial companies to offer banking products, but requires a flexible, API-first architecture.

Timeline:Long-term

Direct Competitors

- →

Fiserv

Market Share Estimate:Largest market share, serving 42% of banks and 31% of credit unions.

Target Audience Overlap:High

Competitive Positioning:Global leader with a comprehensive suite of solutions for financial institutions of all sizes, with a strong foothold in payments processing.

Strengths

- •

Dominant market share and brand recognition.

- •

Extensive product portfolio, including the popular Clover platform for merchants.

- •

Large scale and resources for R&D and acquisitions.

- •

Strong position serving both large and small financial institutions.

Weaknesses

- •

Perceived as having slower innovation and market response.

- •

Customer service and support can be a pain point for smaller clients.

- •

Complex, sometimes fragmented product integrations due to acquisitions.

- •

Often seen as less flexible and more expensive than smaller competitors.

Differentiators

- •

End-to-end solutions covering core processing, digital banking, and extensive payment services.

- •

Strong focus on the merchant acquiring space (Clover).

- •

Global operational scale.

- →

FIS (Fidelity National Information Services)

Market Share Estimate:Significant market share, serving 9% of banks and 3% of credit unions, with a strong focus on larger institutions.

Target Audience Overlap:High

Competitive Positioning:A global financial technology leader, specializing in technology solutions for merchants, banks, and capital markets firms.

Strengths

- •

Leading provider for large banks with assets over $10 billion.

- •

Broad portfolio of solutions for banking, payments, and capital markets.

- •

Global presence and diverse customer base.

- •

Considered to have an advanced API strategy by some industry analysts.

Weaknesses

- •

Less focus and smaller market share in the community bank and credit union space compared to Jack Henry and Fiserv.

- •

Like Fiserv, can be perceived as a legacy provider with complex systems.

- •

Slower to adapt to new market trends compared to more nimble competitors.

Differentiators

- •

Strong expertise in serving large, complex financial institutions.

- •

Integrated solutions that span across banking and capital markets.

- •

Extensive global footprint.

- →

Finastra

Market Share Estimate:A notable player, particularly among credit unions and in specific lending niches, but smaller overall core market share in the U.S. than the 'Big Three'.

Target Audience Overlap:Medium

Competitive Positioning:Global fintech with a broad portfolio of financial software, emphasizing open platforms and componentized solutions for retail banking, lending, treasury, and payments.

Strengths

- •

Strong emphasis on open architecture (FusionFabric.cloud platform) to foster integration and innovation.

- •

Comprehensive, end-to-end solutions in areas like commercial and syndicated lending.

- •

Global reach with a large number of clients, including many of the world's top banks.

- •

SQL-based open architecture is seen as a benefit by clients for custom integrations.

Weaknesses

- •

Complexity of offerings can be overwhelming for smaller institutions.

- •

Customer support can be slow to resolve issues.

- •

Perceived as slow to adapt core offerings compared to competitors.

- •

Less dominant in the U.S. community bank core market.

Differentiators

- •

'Platformification' strategy centered on their FusionFabric.cloud open development platform.

- •

Componentized solutions that can be deployed individually, offering flexibility.

- •

Strong global presence outside of the U.S. core market.

- →

Q2 Holdings

Market Share Estimate:A growing, digital-focused player with a smaller but significant presence, often seen as an alternative to the 'Big Three' for digital solutions.

Target Audience Overlap:Medium

Competitive Positioning:A provider of cloud-based digital banking and lending solutions, positioning itself as a modern, innovative partner for FIs focused on the digital experience.

Strengths

- •

Strong reputation for modern, user-friendly digital banking platforms.

- •

Focus on a unified, cloud-based platform.

- •

High revenue growth, driven by a successful subscription-based model.

- •

Reputation for high-quality customer support.

Weaknesses

- •

Smaller scale and brand recognition compared to the 'Big Three'.

- •

Less comprehensive suite of core banking products compared to incumbents, although they are expanding.

- •

Primarily focused on the U.S. market.

Differentiators

- •

Digital-first approach to banking solutions.

- •

Strong emphasis on user experience and innovation.

- •

Unified platform for digital banking, lending, and other services.

Indirect Competitors

- →

Point Solution & Specialized Fintechs (e.g., Stripe, Plaid, Alkami)

Description:Companies that offer best-in-class solutions for specific functions like payment processing, open banking data aggregation, or digital account opening. Financial institutions may opt to integrate these solutions rather than use the modules offered by their core provider.

Threat Level:Medium

Potential For Direct Competition:Low, but they erode the all-in-one value proposition of core providers and can disintermediate them from key revenue streams.

- →

Cloud-Native Core Providers (e.g., Mambu, Thought Machine)

Description:Modern, API-first, cloud-based core banking platforms that offer high flexibility and scalability. They are gaining traction with digital-only banks (neobanks) and fintechs.

Threat Level:Medium

Potential For Direct Competition:High, as they represent the next generation of core banking technology that legacy providers are currently building towards.

- →

Major Cloud Providers (AWS, Google Cloud, Microsoft Azure)

Description:Provide the underlying infrastructure and a growing set of financial services-specific tools that enable banks and new entrants to build their own technology stacks, potentially bypassing traditional core vendors.

Threat Level:Low

Potential For Direct Competition:Low. More likely to be partners (as seen with Jack Henry and Google Cloud) or enablers of new competitors rather than direct competitors themselves.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

High Customer Satisfaction & Service Reputation

Sustainability Assessment:Highly sustainable. Consistently rated higher for customer service and support compared to larger rivals like Fiserv and Finastra. This is a key differentiator in a market with high switching costs.

Competitor Replication Difficulty:Hard

- Advantage:

Strong Focus on Community & Regional Financial Institutions

Sustainability Assessment:Sustainable. This focus allows Jack Henry to tailor its products, services, and support model to a specific market segment that is often underserved by larger, more globally-focused competitors.

Competitor Replication Difficulty:Medium

- Advantage:

Growing Open Integration Ecosystem

Sustainability Assessment:Moderately sustainable. Their investment in an open, API-first strategy (e.g., jackhenry.dev) is a key trend, but competitors like Finastra are also heavily invested in this area. Continued investment and developer adoption are crucial.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Technology Modernization Narrative', 'estimated_duration': '1-3 years. The current strategic push towards a unified, cloud-native platform with Google Cloud is a powerful marketing and sales tool. However, all major competitors are on a similar modernization journey, which will diminish this advantage over time.'}

Disadvantages

- Disadvantage:

Scale and R&D Budget

Impact:Major

Addressability:Difficult. Jack Henry is significantly smaller than Fiserv and FIS in terms of revenue and market cap, which limits its ability to match their sheer scale in R&D spending and M&A activity.

- Disadvantage:

Perception as a Legacy Provider (in transition)

Impact:Major

Addressability:Moderately. While actively working to change this perception with their new platform strategy, they are still often grouped with other legacy core providers, making them vulnerable to newer, cloud-native competitors.

- Disadvantage:

Execution Risk on Platform Modernization

Impact:Critical

Addressability:Moderately. The transition to a new cloud-native core platform is a massive, multi-year undertaking. Any significant delays, migration issues for clients, or failure to deliver on promised capabilities could severely damage their competitive standing.

Strategic Recommendations

Quick Wins

- Recommendation:

Launch a targeted marketing campaign highlighting superior customer satisfaction scores and client testimonials, directly contrasting with known weaknesses of larger competitors.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Promote the 'Jack Henry Marketing Center' as a value-add service to help smaller FIs compete, reinforcing the 'partnership' positioning.

Expected Impact:Low

Implementation Difficulty:Easy

Medium Term Strategies

- Recommendation:

Accelerate the development and showcase of the open API ecosystem by actively co-marketing solutions built by fintech partners.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Develop and market a streamlined, 'De Novo in-a-box' offering on the new cloud-native platform to capture the next generation of banks.

Expected Impact:Medium

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Successfully execute the transition to the single, cloud-native core platform, ensuring a smooth migration path for existing clients to maintain high retention.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Expand into adjacent services that leverage the open platform, such as advanced data analytics consulting or becoming a BaaS enablement partner for embedded finance.

Expected Impact:High

Implementation Difficulty:Difficult

Solidify positioning as the 'Modern, Open, and Trusted Partner' for community and regional financial institutions, emphasizing a clear, low-risk path to modernization and superior service that the mega-vendors cannot match.

Differentiate on three key pillars: 1) A pragmatic and proven modernization strategy (not rip-and-replace), 2) A truly open platform that empowers choice for FIs, and 3) A culture of partnership and best-in-class customer support.

Whitespace Opportunities

- Opportunity:

Compliance-as-a-Service (RegTech)

Competitive Gap:While all core providers offer compliance features, a dedicated, proactive RegTech solution suite built on the new cloud platform could automate and simplify the growing compliance burden for smaller FIs, which lack large internal teams.

Feasibility:Medium

Potential Impact:High

- Opportunity:

AI-Powered Financial Wellness Platform for FIs

Competitive Gap:Beyond basic financial health tools, Jack Henry can leverage its data and AI capabilities to provide its client FIs with a platform to offer hyper-personalized financial coaching and recommendations to their end-customers, creating a new value proposition.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Specialized Technology Solutions for Credit Unions

Competitive Gap:The credit union market is more fragmented than the banking market. Developing unique, credit-union-specific modules and workflows (e.g., for member voting, dividend calculation, or specialized lending) could deepen their moat in this segment.

Feasibility:High

Potential Impact:Medium

Jack Henry & Associates operates within the mature and highly concentrated core banking technology industry, which is an oligopoly dominated by the 'Big Three': Fiserv, FIS, and Jack Henry itself. The primary barriers to entry are exceptionally high switching costs, complex regulatory hurdles, and long-standing institutional relationships, which insulate the incumbents but also stifle rapid innovation.

Jack Henry's primary direct competitors are the industry giants, Fiserv and FIS. Fiserv holds the largest market share across banks and credit unions, while FIS is particularly strong with the largest banking institutions. Jack Henry effectively competes by focusing on a specific niche—community and regional banks and credit unions—where it has cultivated a powerful reputation for superior customer service and partnership. This is its most sustainable competitive advantage. While smaller in scale, Jack Henry is consistently rated higher in customer satisfaction and support, a critical factor for smaller institutions that feel underserved by the mega-vendors.

Emerging competitive threats are significant. More agile, digital-first competitors like Q2 Holdings are challenging the incumbents on user experience and cloud technology. Furthermore, a new generation of cloud-native, API-first core providers (e.g., Mambu) poses a long-term architectural threat, particularly with new banks and those looking for a complete overhaul. Indirect competition also comes from specialized fintechs offering 'best-of-breed' point solutions that can chip away at the all-in-one value proposition of a core provider.

The entire industry is in a state of massive transition, driven by trends toward open banking, cloud adoption, and AI integration. Jack Henry's strategic response—building a modern, unified, cloud-native platform in partnership with Google Cloud—is directionally correct and essential for future survival and growth. This technology modernization initiative is currently their key message and a temporary advantage. However, the execution of this multi-year strategy carries significant risk.

Strategic whitespace for Jack Henry exists in deepening its value proposition beyond core processing. Opportunities in areas like Compliance-as-a-Service (RegTech) and providing AI-driven financial wellness platforms for their clients could create new, high-margin revenue streams and further entrench them as an indispensable partner.

Ultimately, Jack Henry's strategy should be to double down on its strengths. It cannot out-spend Fiserv or FIS, but it can win by being the most trusted, open, and supportive technology partner for community and regional financial institutions navigating the complex path to digital modernization.

Messaging

Message Architecture

Key Messages

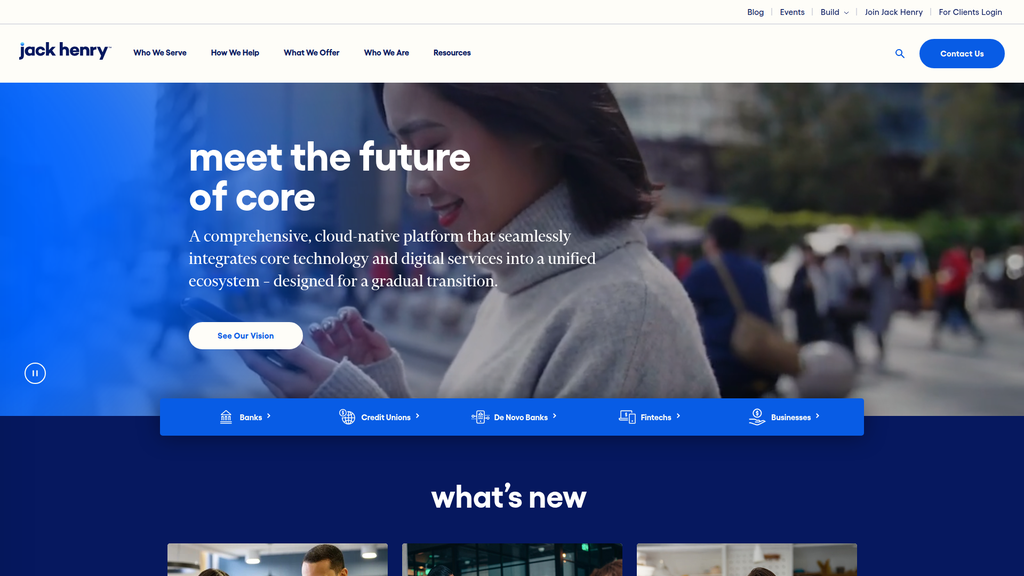

- Message:

Meet the future of core: A comprehensive, cloud-native platform that seamlessly integrates core technology and digital services into a unified ecosystem – designed for a gradual transition.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Banner

- Message:

We strengthen the connections between people and their financial institutions through technology and services that reduce the barriers to financial health.

Prominence:Secondary

Clarity Score:Medium

Location:Company Mission Statement (Implicit across site)

- Message:

We are an advocate for you. Our advocacy of community and regional financial institutions is rooted in the belief that the world is better with you in it.

Prominence:Secondary

Clarity Score:High

Location:Homepage 'Who We Are' Section

- Message:

We understand the industry-wide challenges you face. Jack Henry™ is ready to address these evolving needs.

Prominence:Tertiary

Clarity Score:High

Location:Homepage 'How We Help' Section

The message hierarchy is well-defined, with the primary focus squarely on the new, cloud-native 'Jack Henry Platform' as the 'future of core'. This effectively signals the company's strategic direction. Secondary messages successfully build a supporting narrative around partnership, advocacy, and problem-solving for their target market. However, the sheer volume of offerings under 'What We Offer' can slightly dilute the primary message's impact if a user explores too broadly without a clear path.

Messaging is highly consistent. The core themes of modernization, unification (ecosystem), partnership, and solving specific industry challenges are woven throughout the homepage, from the hero banner to the detailed descriptions of how they help and what they offer. This consistency reinforces their strategic shift while honoring their long-standing brand identity as a partner to community financial institutions.

Brand Voice

Voice Attributes

- Attribute:

Expert & Knowledgeable

Strength:Strong

Examples

Stay on top of industry trends with insights from authors who are well-versed on the inner workings of the fintech industry.

Managing enterprise risk is complex. Protect your organization and your accountholders against a variety of sophisticated and frequent risk management challenges.

- Attribute:

Supportive & Advocating

Strength:Strong

Examples

- •

We are an advocate for you.

- •

Our advocacy of community and regional financial institutions is rooted in the belief that the world is better with you in it.

- •

They take time to listen, understand our unique challenges, and work with us to develop a strategy...

- Attribute:

Innovative & Forward-Looking

Strength:Strong

Examples

- •

meet the future of core

- •

We’re building a comprehensive, cloud-native platform...

- •

Regulatory upheaval is opening new doors for banks and credit unions. Will you lead or fall behind?

- Attribute:

Corporate & Professional

Strength:Moderate

Examples

We are dedicated to our stakeholders and delivering a strong return on investment and long-term sustainability for our business model.

Jack Henry has long incorporated a commitment to corporate sustainability into the way we do business.

Tone Analysis

Consultative

Secondary Tones

Aspirational

Reassuring

Tone Shifts

- •

Shifts from high-level, aspirational language in the hero section to a more direct, problem-solution tone in the 'How We Help' section.

- •

The testimonials introduce a more personal and relational tone.

- •

The 'Investor Relations' and 'Sustainability' sections adopt a formal, corporate tone as expected.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Jack Henry provides a comprehensive, open, cloud-native technology ecosystem that empowers community and regional financial institutions to modernize at their own pace, compete effectively, and thrive in a changing financial landscape.

Value Proposition Components

- Component:

Future-Proof Technology Modernization

Clarity:Clear

Uniqueness:Somewhat Unique

Details:The emphasis on a 'cloud-native platform' built with Google Cloud is a strong, modern value prop. The specific callout of a 'gradual transition' is a key unique selling point for established institutions fearing a disruptive 'rip and replace'.

- Component:

Comprehensive, Unified Ecosystem

Clarity:Clear

Uniqueness:Common

Details:Offering a full suite of services (core, digital, payments, lending) is common among large competitors like Fiserv and FIS. The value here is in the promise of unification into a 'single, adaptable ecosystem'.

- Component:

Advocacy and Partnership for Community FIs

Clarity:Clear

Uniqueness:Unique

Details:The explicit messaging of being an 'advocate' for community and regional financial institutions is a powerful differentiator, positioning them as a partner who is on their clients' side, rather than just a vendor.

- Component:

Problem-Solving for Industry Challenges

Clarity:Clear

Uniqueness:Common

Details:Addressing specific pain points like efficiency, revenue growth, and fraud is a necessary component of their value prop. The clarity with which they list these challenges in the 'How We Help' section is effective.

Jack Henry effectively differentiates itself from larger, more monolithic competitors by combining technological innovation with a strong message of partnership and advocacy. The key differentiator is the promise of a modern, open platform without the pain of a forced, all-at-once conversion. This 'gradual transition' messaging directly addresses a major fear for their target market and positions them as a more flexible and understanding partner.

The messaging positions Jack Henry as a strategic partner that enables legacy institutions (community/regional banks, credit unions) to achieve technological parity with larger banks and fintech challengers. They are not just a technology provider but a champion for their clients' success, leveraging top-tier partnerships (Google Cloud) to deliver secure, modern solutions. This positioning carves out a defensible niche focused on deep client relationships and tailored modernization.

Audience Messaging

Target Personas

- Persona:

Bank & Credit Union Executives (CEO, COO, CTO)

Tailored Messages

- •

We deliver the insight and technology ecosystem that new banks need – from meeting initial business goals to achieving long-term strategic success.

- •

Our platform is designed to integrate and streamline your banking operations, enhancing efficiency, security, and scalability.

- •

Strategically plan to improve your near- and long-term financial performance.

Effectiveness:Effective

- Persona:

De Novo Bank Founders

Tailored Messages

We deliver the insight and technology ecosystem that new banks need – from meeting initial business goals to achieving long-term strategic success.

Effectiveness:Somewhat

- Persona:

Fintech Partners

Tailored Messages

- •

We help fintechs expand their reach and deliver their innovative solutions to a broader financial ecosystem.

- •

For Developers

- •

For Designers

Effectiveness:Somewhat

Audience Pain Points Addressed

- •

Operational inefficiency

- •

Revenue challenges and pressure on traditional income sources

- •

Risk of fraud and complex security landscape

- •

Difficulty attracting and growing commercial accountholders

- •

Pressure to improve the digital accountholder experience

- •

Fear of being left behind by technological disruption

Audience Aspirations Addressed

- •

To thrive today and in the future

- •

To innovate faster and differentiate strategically

- •

To be at the center of their accountholders' financial lives

- •

To achieve long-term strategic success and profitability

Persuasion Elements

Emotional Appeals

- Appeal Type:

Fear of Missing Out (FOMO) / Falling Behind

Effectiveness:High

Examples

Regulatory upheaval is opening new doors for banks and credit unions. Will you lead or fall behind?

Competing for business accountholders in today's environment requires a whole new strategy.

- Appeal Type:

Security & Trust

Effectiveness:High

Examples

Jack Henry and Google Cloud Collaborate to Secure Accountholder Data

Protect your organization and your accountholders against a variety of sophisticated and frequent risk management challenges.

- Appeal Type:

Empowerment & Confidence

Effectiveness:Medium

Examples

- •

Unlock Your Advantage

- •

Boost Your Impact

- •

empower businesses to expedite payments processing, improve cash flow, and manage financials

Social Proof Elements

- Proof Type:

Client Testimonials

Impact:Strong

Details:The quote from the EVP & CTO at Old Second National Bank is highly credible and directly supports the technology modernization message.

- Proof Type:

Authority/Expertise

Impact:Strong

Details:Extensive resource library with eBooks ('2025 Strategy Benchmark'), white papers, podcasts, and blog posts from industry experts establishes thought leadership.

- Proof Type:

Borrowed Authority (Partnerships)

Impact:Strong

Details:Prominently featuring the partnership with Google Cloud Platform lends significant credibility and trust to their cloud strategy.

Trust Indicators

- •

Explicit 'Investor Relations' section

- •

Detailed 'Privacy Policy' and 'Terms of Use'

- •

Showcasing the leadership team

- •

Long-standing company history (implied)

- •

Partnership with a major tech company (Google Cloud)

Scarcity Urgency Tactics

Event promotion with specific dates ('Strategy Summit - Session 1: Digital Front Door Overview August 25, 2025') creates time-based urgency.

Calls To Action

Primary Ctas

- Text:

See Our Vision

Location:Homepage Hero Banner

Clarity:Somewhat Clear

Assessment:This is aspirational but lacks a direct action. It's unclear what the user will get. A more concrete CTA like 'Explore the Platform' would be more effective.

- Text:

Contact Us

Location:Main Navigation, Footer, and Final Homepage section

Clarity:Clear

Assessment:A standard and necessary CTA for a B2B business, clearly placed.

- Text:

Learn More

Location:Throughout solution/challenge sections

Clarity:Clear

Assessment:Effectively moves users deeper into the site to learn about specific topics of interest.

- Text:

Get the eBook / Read More / Watch the Video

Location:Content marketing sections

Clarity:Clear

Assessment:Strong, value-driven CTAs for lead generation and thought leadership engagement.

The CTAs are generally effective at guiding users to relevant content and educational resources, which aligns with a long B2B sales cycle. However, the top-of-funnel, primary CTA ('See Our Vision') is vague. There is a noticeable lack of a high-prominence, bottom-of-funnel CTA like 'Request a Demo' or 'Talk to an Expert' on the homepage, which could be a missed opportunity for converting high-intent visitors.

Messaging Gaps Analysis

Critical Gaps

- •

Lack of quantifiable outcomes. The messaging explains what they do and how they help, but rarely provides quantifiable proof points (e.g., 'reduce processing time by X%', 'increase commercial loan applications by Y%').

- •

Absence of a prominent, high-intent 'Request a Demo' CTA on the homepage, which is a standard for enterprise software and SaaS companies.

- •

Limited competitive comparison. While they differentiate on partnership, they don't explicitly address how their technology is superior to specific competitors in the market (e.g., Fiserv, FIS).

Contradiction Points

The message of a 'unified' and 'single' ecosystem can feel at odds with the vast, sprawling list of individual products and services under the 'What We Offer' menu. This could create a perception of complexity rather than simplicity.

Underdeveloped Areas

The messaging for 'Fintechs' and 'Businesses' as target audiences is significantly less developed on the homepage compared to that for Banks and Credit Unions. The value proposition for these segments needs more articulation.

While client testimonials exist, a more robust 'Case Studies' or 'Success Stories' section with detailed narratives and results would be more powerful than a single rotating quote.

Messaging Quality

Strengths

- •

Excellent alignment with the core audience's (community FIs) primary pain points and aspirations.

- •

Strong, clear articulation of the company's forward-looking technology strategy ('future of core').

- •

Effective use of a supportive, partnership-focused brand voice to build trust and differentiate.

- •

Robust content marketing (eBooks, benchmarks, podcasts) that establishes authority and provides value.

Weaknesses

- •

The primary CTA in the hero section is vague and lacks impact.

- •

The sheer volume of information can be overwhelming, potentially causing message dilution.

- •

Heavy reliance on feature- and process-based language rather than benefit- and outcome-based language.

- •

Lack of prominent, quantifiable results or success metrics in the marketing copy.

Opportunities

- •

Feature a rotating banner of client logos on the homepage to provide immediate social proof.

- •

Develop interactive tools, such as an ROI calculator or a modernization assessment, to engage prospects and quantify value.

- •

Create dedicated, in-depth content and landing pages that speak directly to the Fintech and Business personas.

- •

Elevate customer success stories into full-fledged case studies with metrics, showcasing them more prominently on the site.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Hero CTA

Recommendation:A/B test the 'See Our Vision' CTA against more action-oriented and concrete alternatives like 'Explore the Platform', 'How It Works', or 'Request a Demo'.

Expected Impact:High

- Area:

Value Proposition Quantification

Recommendation:Incorporate specific data points and metrics into key messaging. For example, instead of 'Operate more efficiently,' use 'Clients have reduced operational overhead by up to 15%'.

Expected Impact:High

- Area:

Navigation & Information Architecture

Recommendation:Simplify the 'What We Offer' section. Instead of a long list of products, group them into solution-oriented categories that align with the 'How We Help' section to reduce cognitive load and guide users more effectively.

Expected Impact:Medium

Quick Wins

- •

Add a 'Client Logos' section to the homepage for instant credibility.

- •

Rewrite headlines in the 'How We Help' section to be more benefit-driven (e.g., Change 'Operate More Efficiently' to 'Streamline Operations and Reduce Costs').

- •

Add a secondary CTA for 'Request a Demo' in the main navigation bar.

Long Term Recommendations

- •

Build out a comprehensive library of video testimonials and detailed, metric-rich case studies for different client types (Banks, CUs, De Novos).

- •

Develop distinct messaging tracks and user journeys for the Fintech and Business audiences, with dedicated content hubs.

- •

Invest in persona-based personalization for the website experience, surfacing the most relevant solutions and content based on user behavior or self-selection.

Jack Henry's strategic messaging is highly effective at positioning the company as a forward-thinking, indispensable partner for community and regional financial institutions. The core message successfully communicates a major strategic pivot towards a cloud-native, open-banking platform while reassuring its established client base with the promise of a 'gradual transition'. The brand voice is expertly crafted, balancing innovation with a deep-seated identity as an advocate for its clients, a key differentiator against larger, more impersonal competitors.

The messaging architecture is logical, guiding visitors from a high-level vision ('the future of core') to specific industry pain points ('How We Help') and the corresponding solutions ('What We Offer'). This structure effectively qualifies the audience and aligns the company's capabilities with market needs. Persuasion is skillfully employed through a mix of expert authority, social proof via testimonials and partnerships (notably with Google Cloud), and emotional appeals that tap into both the fear of being left behind and the desire for security and trust.

However, there are clear opportunities for optimization that could significantly impact business outcomes. The messaging is heavy on features and processes but light on quantifiable benefits and outcomes, a critical gap in B2B marketing where ROI is paramount. Calls-to-action, while plentiful, lack a prominent, high-intent option like 'Request a Demo' on the homepage, potentially slowing the conversion of interested prospects into qualified leads. Furthermore, the sheer breadth of offerings can feel overwhelming, slightly undermining the core message of a single, unified platform. By sharpening its focus on tangible results, clarifying its primary CTAs, and simplifying the presentation of its ecosystem, Jack Henry can transform a strong messaging strategy into a more powerful engine for customer acquisition and market leadership.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Long-standing market presence (approaching 50 years) with a large, established client base of approximately 7,400 financial institutions.

- •

Comprehensive, end-to-end product suite covering core processing, digital banking, payments, lending, and fraud, which creates high switching costs.

- •

Consistent revenue growth, with a reported 7.2% increase in fiscal 2025 to $2.38 billion, demonstrating sustained demand.

- •

Strong client adoption of new digital solutions and a high private cloud hosting rate (77% of core clients), indicating alignment with current market needs.

- •

Successful upmarket push, with the total assets of new core clients won nearly tripling over the past three years.

Improvement Areas

- •

Accelerate the transition from legacy on-premise solutions to the new cloud-native platform to meet the agility demands of modern banking.

- •

Enhance the user experience and customizability of core platforms like SilverLake, which are sometimes viewed as clunky or outdated.

- •

Further develop the open banking ecosystem to attract more third-party fintechs, making the platform stickier and more valuable.

Market Dynamics

10-18% CAGR for Core Banking Software Market.

Mature

Market Trends

- Trend:

Digital Transformation & Cloud Adoption

Business Impact:Massive tailwind for Jack Henry's cloud-native strategy. Banks and credit unions are actively increasing tech spending, with a focus on cloud-based solutions to improve customer experience and operational efficiency.

- Trend:

Open Banking & Embedded Finance

Business Impact:Creates a significant opportunity for Jack Henry's platform strategy. By enabling integrations with fintechs (like Plaid, Finicity), they become the central hub for their clients, driving growth beyond core services.

- Trend:

AI in Financial Services

Business Impact:Opportunity to differentiate by embedding AI for fraud detection (Financial Crimes Defender), lending decisions, and personalized banking, which is a top investment priority for FIs.

- Trend:

Focus on Small and Medium Business (SMB) Banking

Business Impact:Strong growth vector. 80% of FIs plan to expand SMB services, and Jack Henry's Banno Business platform and payment solutions are well-positioned to capture this demand.

Excellent. The industry is at a critical inflection point, moving away from legacy systems towards modern, cloud-based, and open platforms. Jack Henry's strategic shift, initiated a few years ago, positions them perfectly to capture this wave of modernization.

Business Model Scalability

High

High fixed costs for R&D and infrastructure, but low variable costs per new software client, leading to high gross margins and operating leverage as the customer base grows. Cloud services revenue grew 12% in FY2025.

High. As a software provider moving to a cloud-native platform, each additional client or service sold adds incremental revenue with minimal marginal cost, evidenced by expanding operating margins.

Scalability Constraints

- •

Complex and lengthy sales cycles for core banking systems.

- •

Significant implementation and data migration effort required for new clients, which can be a bottleneck to rapid onboarding.

- •

Dependence on a highly skilled workforce for implementation, support, and R&D.

Team Readiness

Strong. The company has a long history of stable growth, consistent dividend payments for over 22 years, and a clear strategic vision for its technology modernization, indicating a capable and disciplined leadership team.

Appears well-structured for its current sales-led model. However, growth will require strengthening the organizational muscle around platform/ecosystem management and developer relations.

Key Capability Gaps

- •

Developer Evangelism: To build a thriving third-party ecosystem on the new open platform, a team dedicated to attracting and supporting external developers is crucial.

- •

Product-Led Growth (PLG) Expertise: As they unbundle services on the new platform, capabilities in PLG will be needed to drive adoption of individual modules without high-touch sales.

- •

Cloud-Native Talent: Continued investment in recruiting and training top-tier cloud engineering and cybersecurity talent is critical for the platform transition.

Growth Engine

Acquisition Channels

- Channel:

Direct Enterprise Sales

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip the sales team to sell the new cloud-native platform vision, focusing on business agility and ecosystem value over feature-by-feature comparisons. Continue focus on winning larger FI clients.

- Channel:

Content Marketing (Whitepapers, Blogs, Webinars)

Effectiveness:High

Optimization Potential:High

Recommendation:Double down on content that addresses the strategic challenges of FI leadership (e.g., competing with neobanks, leveraging AI). Create a dedicated content track for third-party developers and fintech partners.

- Channel:

Industry Events & Conferences

Effectiveness:Medium

Optimization Potential:Medium

Recommendation:Shift focus from purely lead generation to also building the brand as a modern technology platform. Host developer-focused events or 'hackathons' to stimulate the partner ecosystem.

- Channel:

Cross-sell / Upsell to Existing Clients

Effectiveness:High

Optimization Potential:High

Recommendation:Develop targeted campaigns to migrate the remaining 23% of core clients to the private cloud and aggressively cross-sell new cloud-native modules (e.g., Financial Crimes Defender, Banno Business) to the installed base.

Customer Journey

Traditional, high-touch enterprise sales journey: Awareness (content, events) -> Consideration (demos, consultations) -> Negotiation -> Long-term contract. Sales cycles are likely 6-18 months.

Friction Points

- •

Perception of legacy technology (which the new platform strategy aims to solve).

- •

High perceived risk and cost of switching core banking providers for clients.

- •

Complexity of navigating Jack Henry's extensive product suite to find the right solutions.

Journey Enhancement Priorities

{'area': 'Early-stage Consideration', 'recommendation': "Develop an interactive, self-service 'solution builder' on the website to help prospective clients explore product combinations and understand potential ROI before engaging with sales."}

{'area': 'Migration & Onboarding', 'recommendation': 'Invest heavily in tools and processes that de-risk and accelerate the migration from competitor or legacy systems to the new cloud-native platform. Market this as a key competitive advantage.'}

Retention Mechanisms

- Mechanism:

High Switching Costs

Effectiveness:High

Improvement Opportunity:Increase stickiness further by fostering a third-party application ecosystem on the open platform, making the Jack Henry platform indispensable.

- Mechanism:

Integrated Product Ecosystem

Effectiveness:High

Improvement Opportunity:Strengthen the data integration and unified user experience across all modules (core, payments, digital) to create a seamless platform feel, reinforcing the value of the all-in-one solution.

- Mechanism:

Long-Term Contracts & Support

Effectiveness:High

Improvement Opportunity:Evolve the support model from reactive problem-solving to proactive strategic partnership, using data analytics to advise clients on how to optimize their operations and growth using Jack Henry tools.

Revenue Economics

Excellent. The business model is characterized by high-margin recurring revenue from services, processing, and cloud hosting, which constitutes approximately 85% of total revenue.

Estimated to be Very High (>10:1). Long contract lengths, high retention rates, and significant cross-sell/upsell potential lead to a very high customer lifetime value, justifying the high cost of enterprise sales.

Strong. The company demonstrates consistent revenue growth (7-10% annually) and expanding operating margins (23-25%), indicating efficient conversion of investment into revenue.

Optimization Recommendations

- •

Increase revenue per customer by driving adoption of newer, high-margin cloud services and AI-powered products.

- •

Develop more efficient channels for selling to smaller FIs or selling modular services, potentially through a lower-touch inside sales or product-led model.

- •

Implement value-based pricing for new platform services that is tied to customer outcomes (e.g., efficiency gains, fraud reduction) rather than just transaction volume.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Product Architecture

Impact:High

Solution Approach:Aggressively execute the current multi-year strategy to rebuild all core components on a single cloud-native, open platform. This is the correct, albeit complex, solution.

- Limitation:

Technical Debt in Existing Systems

Impact:Medium

Solution Approach:Continue to support existing systems to ensure client retention while strategically creating migration paths and incentives for customers to move to the new platform over time.

Operational Bottlenecks

- Bottleneck:

Client Implementation & Migration

Growth Impact:Limits the velocity of new customer acquisition and platform adoption.

Resolution Strategy:Invest in automation, standardized playbooks, and certified implementation partners to streamline and scale the onboarding process.

- Bottleneck:

Integrating Acquisitions

Growth Impact:Can divert resources and create disjointed product experiences if not managed well.

Resolution Strategy:Adopt a 'platform-first' acquisition strategy, where targets are chosen for their ability to easily integrate into the open platform architecture, rather than as standalone solutions.

Market Penetration Challenges

- Challenge:

Intense Competition from Incumbents

Severity:Critical

Mitigation Strategy:Compete not on features, but on platform openness and agility. Position Jack Henry as the best partner for future-ready banks, not just a provider of legacy software. Key competitors include Fiserv and FIS.

- Challenge:

Market Consolidation (FI Mergers)

Severity:Major

Mitigation Strategy:Develop a dedicated M&A support team to ensure Jack Henry is retained as the provider of choice when two client banks merge. Also, focus on winning larger FI clients to offset the shrinking number of smaller FIs.

Resource Limitations

Talent Gaps

- •

Cloud-Native and Microservices Architects

- •

API Product Managers

- •

AI/ML Engineers with Financial Services expertise

Low. The company has a strong balance sheet with zero debt and significant cash flow, enabling it to self-fund its strategic R&D and growth initiatives.

Infrastructure Needs

Continued investment in public cloud infrastructure (via Google Cloud partnership) to ensure scalability, security, and reliability of the new platform.

Creation of a robust developer portal and sandbox environment to support the third-party ecosystem.

Growth Opportunities

Market Expansion

- Expansion Vector:

Serving Larger Financial Institutions

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Continue the current successful strategy of gradually moving upmarket by proving the scalability and capability of the new cloud platform with flagship large clients. This has already shown success.

- Expansion Vector:

Embedded Finance for Non-Financial Companies

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Leverage the open platform to offer 'Banking-as-a-Service' (BaaS) components (e.g., payments, lending) that tech companies can embed into their own products, creating a new B2B revenue stream.

- Expansion Vector:

International Expansion

Potential Impact:High

Implementation Complexity:Very High

Recommended Approach:Defer until the US cloud-native platform transition is mature. Initial entry could be via strategic partnerships in markets with similar regulatory structures (e.g., Canada, UK).

Product Opportunities

- Opportunity:

Platform-as-a-Service (PaaS) Offering

Market Demand Evidence:The entire banking industry is shifting towards open, component-based architectures to increase agility and innovation.

Strategic Fit:Perfectly aligned with the new cloud-native, open-API strategy.

Development Recommendation:Productize the core components (e.g., general ledger, data hub, payments engine) as standalone APIs that can be consumed by FIs, fintechs, and other third parties, creating a marketplace model.

- Opportunity:

AI-Powered Predictive Analytics Suite

Market Demand Evidence:40% of FIs plan to prioritize AI investments. High demand for solutions that improve efficiency, reduce fraud, and offer personalized customer insights.

Strategic Fit:Natural extension of their role as the central data processor for their clients.

Development Recommendation:Build a suite of AI tools on the new platform that leverage clients' core data for cash flow forecasting, credit risk analysis, and hyper-personalized marketing.

- Opportunity:

Vertical-Specific SMB Solutions

Market Demand Evidence:High demand from FIs to better serve lucrative SMB verticals (e.g., healthcare, legal, construction).

Strategic Fit:Strengthens the value proposition of the Banno Business platform.

Development Recommendation:Develop or partner to create tailored treasury management, payment, and lending workflows for specific SMB verticals, offered as add-on modules.

Channel Diversification

- Channel:

Fintech Partner Program

Fit Assessment:Excellent

Implementation Strategy:Formalize a partner program with tiered benefits, technical support, and co-marketing opportunities. Create a marketplace/app store for partners to promote their integrated solutions.

- Channel:

Inside Sales / Digital Acquisition

Fit Assessment:Good (for modular products)

Implementation Strategy:Build a lower-cost inside sales team to sell individual, easy-to-deploy cloud-native solutions (e.g., a specific payment module) to existing clients and new prospects via a more transactional sales process.

Strategic Partnerships

- Partnership Type:

Technology Platform Partner

Potential Partners

- •

Google Cloud (existing)

- •

Microsoft Azure

- •

AWS

Expected Benefits:Ensures best-in-class scalability, security, and access to advanced AI/ML tools for the core platform. The Google Cloud partnership is a key strategic asset.

- Partnership Type:

Fintech 'App Store' Partners

Potential Partners

- •

nCino (Loan Origination)

- •

Plaid (Data Aggregation)

- •

Stripe (Payment Processing)

- •

Various vertical SaaS companies

Expected Benefits:Rapidly expands the platform's capabilities, increases value for FI clients, creates a competitive moat, and generates new revenue through marketplace fees.

Growth Strategy

North Star Metric

Platform Adoption Rate (PAR)

This metric measures the percentage of clients using the new cloud-native platform and the average number of new platform services (APIs, modules) adopted per client. It directly tracks the success of the core strategic initiative—the technology modernization—and captures both migration progress and expansion revenue, which are the primary drivers of future growth.

Increase PAR by 20% annually for the next 3 years.

Growth Model

Hybrid: Enterprise Sales-Led + Platform Ecosystem

Key Drivers

- •

New core client acquisition by the enterprise sales team.

- •

Migration of the existing client base to the new cloud platform.

- •

Cross-sell of new cloud-native services (e.g., AI fraud, SMB tools).

- •

Third-party developer and fintech adoption of the open platform, creating network effects.

Maintain and empower the high-performing enterprise sales team while simultaneously building a dedicated 'Platform & Ecosystem' team responsible for developer relations, partner success, and fostering the third-party marketplace.

Prioritized Initiatives

- Initiative:

Accelerate Cloud-Native Platform Rollout

Expected Impact:Critical

Implementation Effort:Very High

Timeframe:1-3 Years

First Steps:Publicly release the platform roadmap, launch a developer sandbox, and create a dedicated migration team to hand-hold the first 50 clients moving to the new platform.

- Initiative:

Launch a Formal Fintech Partner Program & App Marketplace

Expected Impact:High

Implementation Effort:Medium

Timeframe:6-12 Months