eScore

principal.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Principal.com has a well-structured digital presence with a professional design, excellent mobile responsiveness, and content that logically maps to the customer journey. Its content authority is solid within its niche, particularly for B2B financial services, but it faces intense competition for broader keywords from larger players like Fidelity. The digital strategy appears heavily focused on the US market, with less visible localized content for its international operations, and could benefit from more aggressive voice search optimization and targeting of long-tail keywords.

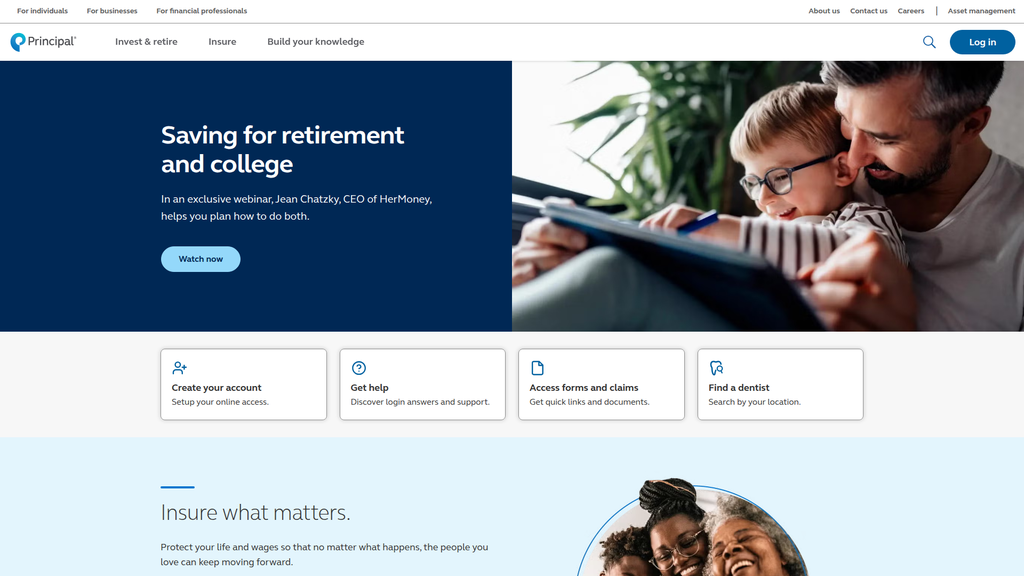

The website's information architecture is a key strength, with clear, audience-segmented navigation ('For individuals', 'For businesses') that allows users to quickly find relevant information, reducing friction and improving user flow.

Focus organic search strategy on high-intent, long-tail keywords related to their core small-to-medium business (SMB) audience (e.g., 'key person insurance for startups') to attract more qualified leads instead of competing on broad, high-cost terms.

The brand's messaging is clear, consistent, and effectively segmented for its core audiences of individuals and businesses, using a reassuring and straightforward voice. It successfully communicates its value proposition around the three pillars of 'Insure, Invest, Retire'. However, the messaging lacks a unique, compelling brand story that differentiates it from the 'sea of sameness' in financial services and relies heavily on functional benefits over deeper emotional connections.

Excellent message architecture, simplifying complex offerings into an easy-to-understand three-pillar structure ('Insure', 'Invest', 'Retire') that is highly effective for user comprehension.

Develop and integrate a core brand narrative that answers 'Why Principal?' to build a stronger emotional connection and differentiate the brand beyond its product features and functional benefits.

The website provides a low-friction experience with an intuitive navigation and a clean, professional aesthetic that reduces cognitive load. However, there are notable opportunities for conversion optimization. Key calls-to-action on the homepage are not always aligned with direct business drivers (e.g., 'Watch Now' CTA), and the primary conversion path often creates a significant friction point by funneling users to an offline, advisor-led process rather than offering direct digital onboarding for simpler products.

The site's clean design, logical information architecture, and effective use of white space create a low cognitive load, making it easy for users to navigate and understand complex information.

A/B test the primary homepage hero CTA, replacing content-focused CTAs with more direct, product-oriented actions (e.g., 'Get an Instant Quote', 'Open an IRA') to improve lead generation and guide users more effectively into the sales funnel.

Credibility is exceptionally high, rooted in a long corporate history since 1879 and reinforced by a sophisticated approach to legal and regulatory compliance. The website features a dedicated accessibility commitment to WCAG 2.1 AA, a comprehensive global privacy framework, and meticulous, industry-specific disclosures required by FINRA and the SEC. Trust signals like the FINRA BrokerCheck link are prominently displayed, showcasing a mature and proactive stance on transparency and risk mitigation.

A public, detailed commitment to WCAG 2.1 AA accessibility standards, including a user feedback mechanism, is a best-in-class practice that significantly builds trust and mitigates legal risk.

Create a simplified landing page that explains the hierarchy between the 'Global Privacy Statement' and the 'Customer Privacy Notice' (GLBA) to reduce potential user confusion and enhance transparency.

Principal's most sustainable competitive advantage is its integrated business model and deep expertise serving the small-to-medium business (SMB) market, a niche underserved by larger competitors. This creates sticky relationships and a defensible moat. However, this advantage is threatened by a perceived lag in technology compared to fintech disruptors and a dependence on traditional advisor-led distribution, which is less appealing to digitally-native customers.

The ability to provide a holistic suite of financial products (retirement, insurance, investments) tailored to the specific needs of the SMB market is a powerful and defensible differentiator.

Develop a direct-to-consumer 'hybrid' robo-advisory platform that integrates automated investing with access to human advisors to neutralize the threat from fintechs and capture a younger demographic.

The business model is highly scalable, benefiting from high operational leverage and recurring, fee-based revenue streams in asset management and retirement solutions. The company shows clear market expansion signals through its focus on international markets like Latin America and Asia and its strategic digital transformation initiatives. Scalability is somewhat constrained by legacy technology and processes that are less efficient than modern, cloud-native platforms, which the company is actively working to address.

A scalable, asset-light business model with a high proportion of recurring revenue from asset-based fees and insurance premiums, providing predictable cash flow and strong operating leverage.

Accelerate the modernization of the legacy technology stack by migrating core functions to modern platforms to increase agility, reduce operational bottlenecks, and speed up new product deployment.

Principal's business model is highly coherent, with a clear strategic focus on high-growth, fee-based businesses like retirement, asset management, and SMB benefits. A recent strategic review, which resulted in exiting lower-growth segments like retail fixed annuities, demonstrates strong strategic focus and efficient resource allocation. The model shows excellent alignment between its value proposition of integrated solutions and the needs of its core SMB target market.

A well-defined and executed strategic focus on the SMB market, where the company's integrated product suite (retirement, benefits, insurance) creates a holistic value proposition that directly addresses key customer pain points.

Innovate the revenue model by developing a subscription-based financial wellness service for individuals, decoupling a portion of revenue from Assets Under Management (AUM) to create a new, predictable income stream.

As a major player in the U.S. retirement and benefits market, Principal exerts significant market influence, particularly within its SMB niche. This position grants it a degree of pricing power, especially with bundled service offerings. However, in the broader asset management space, it faces intense fee compression from low-cost leaders like Vanguard, and its brand recognition in the direct-to-consumer retail market is weaker than giants like Fidelity.

Market leadership in providing comprehensive retirement and benefits solutions to the U.S. small-to-medium business market, creating strong partner leverage and a stable market share trajectory.

Launch targeted digital marketing campaigns and develop a distinct direct-to-consumer product line to address the weaker brand recognition in retail investing and better compete with fintechs and large brokerage firms.

Business Overview

Business Classification

Diversified Financial Services Provider

Asset Management & Insurance

Financial Services

Sub Verticals

- •

Retirement & Pension Solutions

- •

Global Asset Management

- •

Life & Disability Insurance

- •

Workplace Benefits

Mature

Maturity Indicators

- •

Founded in 1879, indicating a long and stable operating history.

- •

Publicly traded company (Nasdaq: PFG) with a large market capitalization.

- •

Consistently high Assets Under Management (AUM), recently reported around $712B to $741B.

- •

Large, global employee base (approx. 18,600+).

- •

Recent strategic review focused on optimizing a mature portfolio by exiting lower-growth segments (e.g., U.S. retail fixed annuities) to focus on core growth areas.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Retirement and Income Solutions

Description:Fees from administrating and managing employer-sponsored retirement plans (e.g., 401(k)s), defined contribution and benefit plans, and other pension solutions. Constitutes the largest portion of revenue.

Estimated Importance:Primary

Customer Segment:Small to Medium-sized Businesses (SMBs) & Large Enterprises

Estimated Margin:Medium

- Stream Name:

Benefits and Protection

Description:Premiums collected from specialty benefits (e.g., group life, disability insurance) sold to businesses for their employees.

Estimated Importance:Primary

Customer Segment:Small to Medium-sized Businesses (SMBs)

Estimated Margin:Medium

- Stream Name:

Principal Asset Management

Description:Fees generated from managing investment portfolios for institutional, retirement, and retail clients. This includes revenue from equity, fixed income, real estate, and alternative investments.

Estimated Importance:Primary

Customer Segment:Institutional Investors, High Net Worth Individuals, Retail Investors

Estimated Margin:High

- Stream Name:

Net Investment Income

Description:Income earned by investing the company's own capital and the 'float' from insurance premiums before claims are paid out.

Estimated Importance:Secondary

Customer Segment:Internal

Estimated Margin:Varies (Market Dependent)

Recurring Revenue Components

- •

Asset-based fees (AUM)

- •

Recurring insurance premiums

- •

Plan administration and service fees

Pricing Strategy

Hybrid (Fee-for-Service, Asset-based, Risk-based)

Mid-range to Premium

Opaque

Pricing Psychology

- •

Bundling

- •

Value-Based Pricing

- •

Tiered Offerings

Monetization Assessment

Strengths

- •

Highly diversified revenue streams across different financial products and client types reduces dependency on any single market segment.

- •

Significant recurring revenue from asset management fees and insurance premiums provides predictable cash flow.

- •

Strong focus on the underserved SMB market for retirement and benefits offers a durable competitive advantage.

Weaknesses

- •

Revenue is sensitive to market volatility, which can negatively impact AUM and fee-based income.

- •

Complex fee structures can be a deterrent for retail customers and smaller businesses compared to simpler fintech alternatives.

- •

Exposure to interest rate fluctuations can impact investment income and the profitability of certain insurance products.

Opportunities

- •

Expand fee-based financial wellness and advisory services to both corporate clients and individuals.

- •

Develop and market ESG-focused investment products to meet growing investor demand.

- •

Leverage technology to offer scalable, lower-cost investment solutions (robo-advisory/hybrid models) to capture a wider audience.

Threats

- •

Intense competition from low-cost robo-advisors and passive investment funds (e.g., Vanguard, Fidelity).

- •

Increasing regulatory scrutiny in the financial services industry could raise compliance costs and limit product offerings.

- •

Disruption from fintech startups offering unbundled, user-friendly, and lower-cost financial products.

Market Positioning

A comprehensive financial partner specializing in retirement, asset management, and benefits for small-to-medium-sized businesses (SMBs) and individuals seeking long-term financial security.

Significant Player

Target Segments

- Segment Name:

Small to Medium-sized Businesses (SMBs)

Description:Businesses seeking to offer competitive employee benefits, including retirement plans (401k, ESOPs) and specialty insurance (group life, disability), as well as business protection solutions like key person insurance.

Demographic Factors

Varying employee counts (typically 10-500)

Across multiple industries

Psychographic Factors

- •

Value ease of administration

- •

Seek to attract and retain talent

- •

Desire a trusted partner to navigate complex regulations

Behavioral Factors

- •

Often work through financial advisors or brokers

- •

Prefer bundled solutions for simplicity

- •

Long sales cycles

Pain Points

- •

Complexity of setting up and managing retirement plans

- •

Lack of resources to administer benefits programs effectively

- •

Concern over fiduciary responsibilities

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Pre-Retirees & Accumulators

Description:Individuals and households focused on long-term goals like saving for retirement and investing for the future. They are often employees of the SMBs Principal serves.

Demographic Factors

- •

Age 35-65

- •

Mid-to-high income levels

- •

Often have families or dependents

Psychographic Factors

- •

Seek financial peace of mind

- •

Value professional guidance but are increasingly tech-savvy

- •

Concerned about outliving their savings

Behavioral Factors

- •

Participate in workplace retirement plans

- •

May seek out financial professionals for advice

- •

Responsive to educational content about investing and retirement

Pain Points

- •

Feeling overwhelmed by investment choices

- •

Uncertainty about how much they need to save for retirement

- •

Balancing multiple financial goals (e.g., retirement, college savings)

Fit Assessment:Good

Segment Potential:Medium

- Segment Name:

Institutional Investors

Description:Pension funds, endowments, foundations, and other large entities seeking sophisticated asset management services across various asset classes.

Demographic Factors

Large asset bases

Global in scope

Psychographic Factors

Highly sophisticated and data-driven

Focus on risk-adjusted returns and fiduciary duty

Behavioral Factors

- •

Long-term investment horizons

- •

Engage in extensive due diligence

- •

Require customized reporting and high-touch service

Pain Points

- •

Finding unique sources of alpha

- •

Accessing specialized or alternative asset classes

- •

Navigating complex global markets

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Integrated Service Model

Strength:Strong

Sustainability:Sustainable

- Factor:

Deep Expertise in the SMB Market

Strength:Strong

Sustainability:Sustainable

- Factor:

Global Asset Management Capabilities

Strength:Moderate

Sustainability:Sustainable

- Factor:

Network of Financial Professionals

Strength:Moderate

Sustainability:Temporary

Value Proposition

For businesses and individuals planning for their financial future, Principal provides integrated retirement, investment, and insurance solutions, simplifying complex decisions and delivering long-term security.

Good

Key Benefits

- Benefit:

Financial Security & Peace of Mind

Importance:Critical

Differentiation:Common

Proof Elements

- •

Long company history (since 1879)

- •

Strong financial ratings

- •

Large AUM

- Benefit:

Simplified Financial Management

Importance:Important

Differentiation:Somewhat unique

Proof Elements

- •

Bundled product offerings for businesses

- •

Website messaging: 'Let's keep your finances simple.'

- •

Tools like the 'Retirement Wellness Planner'

- Benefit:

Access to Professional Guidance

Importance:Important

Differentiation:Common

Proof Elements

'Find a financial professional' call-to-action

Distribution network of independent brokers and advisors

Unique Selling Points

- Usp:

Holistic benefits and retirement solutions provider specifically tailored for the SMB market.

Sustainability:Long-term

Defensibility:Strong

- Usp:

Integrated portfolio combining retirement solutions, global asset management, and specialty benefits under one brand.

Sustainability:Long-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Employers struggle with the complexity and administrative burden of offering competitive retirement and benefits packages.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Individuals feel overwhelmed by financial planning and are uncertain if they are on track for retirement.

Severity:Major

Solution Effectiveness:Partial

- Problem:

Businesses face significant financial risk from the loss of a key employee or owner.

Severity:Major

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition is well-aligned with the persistent market need for retirement savings and financial protection, especially given demographic trends of aging populations.

High

The focus on simplifying complexity and providing integrated solutions directly addresses the core pain points of their primary SMB and individual pre-retiree segments.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Independent Financial Advisors & Brokers

- •

Employers (SMBs)

- •

Clearing Corporations (e.g., Apex Clearing)

- •

Technology Platform Providers

Key Activities

- •

Asset Management & Investment Research

- •

Insurance Underwriting & Risk Management

- •

Retirement Plan Administration

- •

Sales & Distribution through Advisor Networks

- •

Regulatory Compliance

Key Resources

- •

Brand Reputation & Trust

- •

Financial Capital & Balance Sheet Strength

- •

Proprietary Investment Products & Expertise

- •

Global Distribution Network

- •

Technology & Data Infrastructure

Cost Structure

- •

Employee Compensation & Commissions

- •

Technology & Infrastructure Costs

- •

Insurance Claims & Benefits Payouts

- •

Marketing & Sales Expenses

- •

Compliance & Regulatory Costs

Swot Analysis

Strengths

- •

Strong brand recognition and a long-standing reputation for stability.

- •

Diversified and integrated business model across high-growth sectors like retirement and asset management.

- •

Market leadership position in the U.S. SMB retirement and benefits market.

- •

Robust capital position and disciplined financial management.

Weaknesses

- •

Legacy technology systems can hinder agility and create a less seamless customer experience compared to digital-native competitors.

- •

A perception of being more traditional, which may be less appealing to younger, tech-first demographics.

- •

Dependence on intermediary-led distribution (advisors) can be costly and slow to adapt.

Opportunities

- •

Accelerate digital transformation to create a superior, omni-channel customer experience.

- •

Expand into adjacent B2B financial wellness services beyond retirement (e.g., student loan assistance, health savings accounts).

- •

Capitalize on the growing demand for alternative investments and sustainable (ESG) funds.

- •

Strategic acquisitions of fintech companies to quickly gain new technology and talent.

Threats

- •

Disruption from fintechs and robo-advisors offering lower-cost, automated investment solutions.

- •

Persistent macroeconomic pressures such as interest rate volatility and potential market downturns impacting AUM.

- •

Evolving regulatory landscape, including new fiduciary standards and data privacy laws, which increase compliance costs.

- •

Fee compression across the asset management industry, pressuring margins.

Recommendations

Priority Improvements

- Area:

Digital Customer Experience

Recommendation:Invest heavily in a unified digital platform that provides clients with a seamless, self-service experience for all their Principal products, from viewing 401(k) balances to managing insurance policies.

Expected Impact:High

- Area:

Data Analytics & Personalization

Recommendation:Leverage customer data to provide proactive, personalized financial guidance and product recommendations at scale, anticipating client needs before they arise.

Expected Impact:High

- Area:

Product & Communication Simplification

Recommendation:Overhaul product literature and digital interfaces to use clear, simple language, reducing financial jargon to make products more accessible and appealing to a broader audience.

Expected Impact:Medium

Business Model Innovation

- •

Develop a 'Hybrid-Advisor' model that combines a low-cost, automated investment platform for emerging investors with seamless access to human financial professionals for more complex planning needs.

- •

Launch a subscription-based financial wellness service for individuals, offering ongoing planning and advice for a flat monthly fee, decoupling revenue from AUM for a key segment.

- •

Explore offering 'Benefits-as-a-Service' by white-labeling the company's robust SMB benefits administration platform to other financial institutions or professional employer organizations (PEOs).

Revenue Diversification

- •

Expand the suite of alternative investment products (e.g., private credit, infrastructure) available to accredited investors and smaller institutional clients.

- •

Create and monetize a comprehensive corporate financial wellness program that employers can offer as a value-added benefit, covering topics from budgeting to estate planning.

- •

Further penetrate high-growth international markets, particularly in Latin America and Southeast Asia, by tailoring retirement and investment solutions to local needs.

Principal Financial Group operates on a robust and mature business model, strategically positioned as a leader in the high-growth retirement and employee benefits markets, with a particular stronghold in the underserved small-to-medium-sized business (SMB) segment. Its diversified revenue streams—spanning asset management fees, insurance premiums, and administrative services—provide significant resilience against market volatility. A recent strategic review, leading to the divestiture of capital-intensive, lower-growth business lines like retail fixed annuities, demonstrates a clear focus on optimizing its portfolio for fee-based, capital-efficient growth.

The primary challenge and opportunity for strategic evolution lies in navigating the digital disruption posed by fintech competitors. While Principal's strength has been its integrated offerings and advisor-led distribution, the future demands a more agile, technology-driven, and customer-centric approach. The key to sustainable competitive advantage will be to successfully evolve into a 'hybrid' model: augmenting its established human advisory network with a best-in-class digital experience. This involves creating a seamless, personalized, and simplified omni-channel platform that can attract and retain a wider demographic. Innovations such as subscription-based financial planning and white-labeling its administrative technology could unlock new, scalable revenue streams and solidify its market leadership in an increasingly competitive landscape. The firm's ability to execute this digital transformation while preserving its core value proposition of trusted, comprehensive financial guidance will determine its long-term success.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

Regulatory Compliance (SEC, FINRA, etc.)

Impact:High

- Barrier:

Brand Trust and Reputation

Impact:High

- Barrier:

Capital Requirements for Insurance Underwriting

Impact:High

- Barrier:

Established Distribution Networks (Advisors)

Impact:Medium

- Barrier:

Technology and Infrastructure Scale

Impact:Medium

Industry Trends

- Trend:

Digital Transformation and AI Integration

Impact On Business:Requires significant investment in technology to meet customer expectations for seamless digital experiences, personalized advice, and operational efficiency.

Timeline:Immediate

- Trend:

Fee Compression

Impact On Business:Pressure from low-cost providers like Vanguard and robo-advisors is forcing a re-evaluation of fee structures, especially in investment management and 401(k) services.

Timeline:Immediate

- Trend:

Demand for Holistic Financial Wellness

Impact On Business:Customers increasingly expect integrated solutions that combine retirement, insurance, and investments, creating an opportunity for firms with diverse product portfolios.

Timeline:Near-term

- Trend:

Rise of Fintech and Robo-Advisors

Impact On Business:Direct competition for retail investment clients and pressure to enhance digital capabilities. Robo-advisors are transforming the retirement planning landscape.

Timeline:Near-term

- Trend:

Focus on ESG (Environmental, Social, Governance) Investing

Impact On Business:Growing demand from clients for ESG-focused investment options requires product development and expertise in sustainable investing.

Timeline:Near-term

Direct Competitors

- →

Fidelity Investments

Market Share Estimate:One of the largest 401(k) and retail brokerage providers.

Target Audience Overlap:High

Competitive Positioning:A financial supermarket offering a vast range of products (brokerage, retirement, funds) with a strong technology platform and brand recognition.

Strengths

- •

Dominant brand and massive scale.

- •

Leading-edge technology and user-friendly digital platforms.

- •

Broad, integrated product suite for individuals and businesses.

- •

Extensive educational resources and research tools.

- •

Strong retail and workplace (401k) presence.

Weaknesses

- •

Can be perceived as more expensive than low-cost leaders.

- •

Customer service can be impersonal due to sheer size.

- •

Less focused on the insurance and protection side of the business compared to Principal.

Differentiators

- •

Commission-free trading and low-cost index funds.

- •

Robust, all-in-one platform for investing, retirement, and banking.

- •

Strong direct-to-consumer brand appeal.

- →

Vanguard

Market Share Estimate:A top-tier 401(k) provider and the leader in low-cost index funds.

Target Audience Overlap:High

Competitive Positioning:The undisputed low-cost leader, focusing on passive investing and a client-owned structure.

Strengths

- •

Industry-leading low expense ratios.

- •

Extremely strong brand reputation for being investor-first.

- •

Massive assets under management (AUM).

- •

Simple, straightforward investment philosophy.

Weaknesses

- •

Technology and digital user experience often lag competitors.

- •

Less emphasis on personalized financial advice and active management.

- •

Limited product set outside of mutual funds and ETFs (e.g., no insurance).

Differentiators

- •

Unique client-owned corporate structure.

- •

Relentless focus on lowering investment costs.

- •

Primary focus on passive, index-based investing.

- →

Empower Retirement

Market Share Estimate:A top 2 provider of 401(k) plans by participants.

Target Audience Overlap:High

Competitive Positioning:A specialist in workplace retirement solutions, focusing on providing comprehensive 401(k) services to businesses of all sizes.

Strengths

- •

Significant market share in the 401(k) recordkeeping industry.

- •

Strong B2B relationships with plan sponsors and advisors.

- •

Advanced digital tools and a focus on participant experience.

- •

Acquisitions (like Prudential's retirement business) have increased scale.

Weaknesses

- •

Lower brand recognition among individual retail investors compared to Fidelity or Schwab.

- •

Less diversified product offering outside of retirement services.

- •

Customer service reviews can be mixed.

Differentiators

- •

Singular focus on the retirement plan market.

- •

Holistic financial wellness tools integrated into their platform.

- •

Strong focus on the government and non-profit plan sectors (457, 403b).

- →

Voya Financial

Market Share Estimate:Significant player in retirement, investment management, and employee benefits markets.

Target Audience Overlap:High

Competitive Positioning:A diversified financial services firm with a strong focus on workplace solutions, similar to Principal's business model.

Strengths

- •

Strong market position in retirement solutions and employee benefits.

- •

Diversified business model across wealth, health, and investment management.

- •

Capital-light business model with good cash flow generation.

- •

Recognizable brand in the employee benefits space.

Weaknesses

- •

Less scale than giants like Fidelity and Vanguard.

- •

Reputation for customer service has been noted as a challenge.

- •

Exited the individual life insurance market, focusing only on group policies.

Differentiators

- •

Focus on serving the needs of institutional and workplace clients.

- •

Comprehensive suite of employee benefits (health, disability, life) alongside retirement plans.

- •

Strong investment management capabilities across multiple asset classes.

Indirect Competitors

- →

Robo-Advisors (e.g., Betterment, Wealthfront)

Description:Automated, algorithm-driven investment platforms that offer low-cost portfolio management directly to consumers.

Threat Level:Medium

Potential For Direct Competition:They are already direct competitors in the retail investment space and are beginning to enter the 401(k) market for small businesses, encroaching on Principal's core territory.

- →

Fintech Insurers (e.g., Ladder, Ethos)

Description:Digital-first insurance companies that use technology and data to offer streamlined, direct-to-consumer life insurance policies, bypassing traditional agents.

Threat Level:Low

Potential For Direct Competition:They challenge the traditional, agent-driven sales model for insurance but currently lack the broad product suite and workplace integration of Principal. The threat will grow as they expand their offerings.

- →

Large Banks with Wealth Management (e.g., J.P. Morgan Chase, Bank of America)

Description:Major banking institutions that leverage their vast existing customer base to offer integrated banking, lending, and wealth management/investment services.

Threat Level:Medium

Potential For Direct Competition:High. They compete for the same mass affluent customers and are increasingly offering their own automated and hybrid investment advisory services, posing a threat to Principal's retail investment business.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Integrated Business Model (Retirement, Insurance, Investments)

Sustainability Assessment:Principal's ability to offer a holistic suite of products—particularly to small and medium-sized businesses—creates sticky client relationships and opportunities for cross-selling. This is a core differentiator from competitors focused on just one area (e.g., Vanguard).

Competitor Replication Difficulty:Hard

- Advantage:

Strong Position in the SMB Market

Sustainability Assessment:Principal has deep expertise and product offerings tailored to the needs of business owners and their employees (e.g., Key Person insurance, retirement plans). This niche is often underserved by the largest competitors who focus on enterprise clients or pure retail.

Competitor Replication Difficulty:Medium

- Advantage:

Established Distribution Network

Sustainability Assessment:A long-standing network of financial advisors provides a powerful sales and service channel, particularly for complex products and clients who value human advice.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Specific Proprietary Investment Products', 'estimated_duration': '1-3 years'}

{'advantage': 'Current Marketing Campaigns and Brand Messaging', 'estimated_duration': '1-2 years'}

Disadvantages

- Disadvantage:

Perception of Outdated Technology

Impact:Major

Addressability:Moderately

Comment:Compared to fintechs and giants like Fidelity, Principal's digital tools and user experience can be perceived as less modern, which is a significant handicap with younger demographics.

- Disadvantage:

Dependence on Advisor-Led Distribution

Impact:Major

Addressability:Difficult

Comment:While a strength, this model can be a disadvantage for attracting digital-native customers who prefer a direct, self-service approach. It also presents higher distribution costs than a direct-to-consumer model.

- Disadvantage:

Weaker Brand Recognition in Retail Investing

Impact:Minor

Addressability:Moderately

Comment:While strong in the B2B/workplace space, the Principal brand does not have the same top-of-mind awareness for individual brokerage accounts as Fidelity, Schwab, or Vanguard.

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted digital campaigns emphasizing the 'human + tech' value proposition to counter pure robo-advisors.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Simplify the online user journey for core tasks like account opening and retirement readiness checks to reduce friction.

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Invest significantly in a direct-to-consumer 'hybrid' robo-advisory platform that integrates automated investing with access to human advisors.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Develop bundled solutions specifically for SMBs that seamlessly integrate 401(k), group insurance, and key person policies with simplified onboarding and administration.

Expected Impact:High

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Leverage AI and machine learning to create hyper-personalized financial plans and product recommendations that span a customer's entire financial life (insurance, retirement, investing).

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Explore strategic acquisitions of or partnerships with fintech companies to accelerate technology adoption and acquire new customer segments.

Expected Impact:High

Implementation Difficulty:Difficult

Position Principal as the premier financial partner for small-to-medium-sized businesses and the individuals they employ. Emphasize the unique ability to provide integrated, holistic advice that covers both business protection and personal financial wellness, blending trusted human expertise with modern digital convenience.

Differentiate on the seamless integration of services. While competitors offer pieces of the puzzle, Principal's strategy should be to own the entire financial wellness ecosystem for its target market, from setting up a 401(k) and key person insurance for a business to helping that same business owner and their employees plan for retirement and protect their families.

Whitespace Opportunities

- Opportunity:

Holistic Financial Wellness for Small and Medium Businesses (SMBs)

Competitive Gap:Many large competitors focus on enterprise-level clients, while fintechs target individuals. There is a significant gap in providing a truly integrated, affordable suite of financial services (retirement, group insurance, business protection) tailored specifically for the SMB segment.

Feasibility:High

Potential Impact:High

- Opportunity:

Hybrid Advisory Model for the Mass Affluent

Competitive Gap:There is a large market segment that finds pure robo-advisors too impersonal and traditional full-service advisors too expensive. A 'hybrid' model combining a low-cost digital platform with on-demand access to certified financial planners for key life events could capture this underserved market.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Retirement Income and Decumulation Solutions

Competitive Gap:Most of the industry is focused on asset accumulation. As more baby boomers enter retirement, there is a growing, unmet need for sophisticated tools and products designed to help retirees generate a sustainable income stream from their savings. Principal's expertise in annuities and income solutions provides a strong foundation to build on here.

Feasibility:Medium

Potential Impact:High

Comprehensive Competitive Landscape Analysis: Principal Financial Group

1. Market Overview

Principal Financial Group operates in the mature and moderately concentrated financial services industry. The market is characterized by intense competition from a diverse set of players, including large-scale financial supermarkets, low-cost passive investment giants, specialized retirement providers, and a growing number of agile fintech disruptors. Key industry trends exerting significant pressure are digital transformation, fee compression, and a customer-driven shift towards holistic financial wellness. Barriers to entry, such as regulatory hurdles and the need for significant brand trust, remain high, protecting established players like Principal from new, full-stack entrants but not from niche fintech disruptors attacking specific product lines.

2. Direct Competitive Arena

Principal's primary competition comes from multifaceted financial institutions.

- Fidelity Investments represents the primary threat, competing fiercely on technology, brand recognition, and scale. Fidelity's strength lies in its integrated, user-friendly digital platform that serves as a financial hub for millions of retail and workplace clients. Principal's key disadvantage here is a perceived lag in technological sophistication.

- Vanguard competes on a singular, powerful dimension: cost. Its relentless focus on lowering fees pressures margins across the entire industry, particularly in the 401(k) and asset management spaces.

- Empower Retirement and Voya Financial mirror Principal's business model most closely, with a strong focus on workplace solutions (retirement and employee benefits). The competition with these players is often head-to-head for 401(k) plan sponsorships. Principal's advantage over these peers is its more robust and integrated insurance offering, particularly for business owners.

3. Indirect and Disruptive Threats

The most significant long-term threats come from non-traditional players. Robo-advisors (Betterment, Wealthfront) are fundamentally changing consumer expectations for investment management with low-cost, automated, and digitally native solutions. They have successfully captured a younger demographic and are now expanding into the SMB 401(k) market, directly challenging a core Principal business line. Similarly, fintech insurers are disintermediating the traditional agent-based sales process, threatening a key part of Principal's distribution model.

4. Principal's Competitive Position & Advantages

Principal's core sustainable advantage is its integrated business model focused on the Small and Medium Business (SMB) market. While competitors may excel in individual verticals, Principal is uniquely positioned to offer a comprehensive suite of solutions—retirement plans, group benefits, and business protection insurance—to this often-underserved market. This creates deep, sticky relationships. Their established network of financial advisors is a powerful asset for distributing complex products and providing the high-touch service that business owners often require.

However, this reliance on traditional distribution is also a weakness in an increasingly digital world. The company's primary competitive disadvantage is a digital platform and brand perception that lags behind the most tech-forward competitors. Anecdotal evidence suggests customers find their technology outdated and service lacking compared to leaders like Fidelity.

5. Strategic Whitespace and Recommendations

The most significant opportunity for Principal is to double down on its SMB niche and build an unbeatable, integrated digital ecosystem around it. This involves moving beyond selling individual products to offering a holistic 'financial OS' for businesses that seamlessly connects their retirement plan, group benefits, and business insurance.

Another key opportunity lies in bridging the gap between pure digital and traditional advice with a 'hybrid' advisory model. This would cater to the mass affluent who desire digital convenience but still want access to human expertise for major financial decisions.

To succeed, Principal must make aggressive investments in technology to modernize its user experience and leverage data for hyper-personalization. The strategic imperative is to evolve from a traditional financial services firm into a tech-enabled company that blends the best of human advice with a superior digital platform. The winning strategy is not to out-scale Fidelity or out-price Vanguard, but to become the undisputed leader in integrated financial wellness for the SMB market.

Messaging

Message Architecture

Key Messages

- Message:

Insure what matters.

Prominence:Primary

Clarity Score:High

Location:Homepage - Core Service Pillar

- Message:

Invest when you’re ready.

Prominence:Primary

Clarity Score:High

Location:Homepage - Core Service Pillar

- Message:

Retire on your terms.

Prominence:Primary

Clarity Score:High

Location:Homepage - Core Service Pillar

- Message:

Let’s work together for all life’s moments.

Prominence:Secondary

Clarity Score:High

Location:Homepage - Concluding Section

- Message:

Planning for the unexpected can protect your business—and everyone who depends on it.

Prominence:Primary

Clarity Score:High

Location:Business - Key Person Protection Page

Excellent. The homepage effectively uses a three-pillar structure ('Insure', 'Invest', 'Retire') to simplify its core offerings. This creates a clear, logical flow for individual users. The business-focused page is also well-structured, immediately addressing a specific business pain point.

Good. The core themes of protection and planning are consistent across both individual and business sections. The transition from the broad, life-stage messaging on the homepage to the specific, risk-mitigation messaging on the business page is logical and maintains brand integrity.

Brand Voice

Voice Attributes

- Attribute:

Supportive & Reassuring

Strength:Strong

Examples

- •

Protect your life and wages so that no matter what happens, the people you love can keep moving forward.

- •

Feel confident about investing

- •

Retire with confidence.

- Attribute:

Straightforward & Simple

Strength:Strong

Examples

- •

Insure what matters.

- •

Invest when you’re ready.

- •

Retire on your terms.

- •

DIY financial plan: 8 simple steps...

- Attribute:

Action-Oriented & Empowering

Strength:Moderate

Examples

- •

Calculate your income protection needs

- •

Check your retirement readiness

- •

See 3 steps to start investing

- Attribute:

Professional & Credible

Strength:Strong

Examples

- •

You can research our firm with FINRA’s BrokerCheck.

- •

Insurance products issued by Principal National Life Insurance Co...

- •

Referenced companies are members of the Principal Financial Group®

Tone Analysis

Reassuring

Secondary Tones

- •

Empowering

- •

Educational

- •

Formal (in disclaimers)

Tone Shifts

The tone shifts from an approachable, educational voice in the main marketing copy to a formal, legalistic tone in the footnotes and disclaimers, which is standard and necessary for the industry.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Principal provides a comprehensive and simplified suite of financial products (insurance, investments, retirement) to help individuals and businesses achieve financial security and confidence throughout all stages of life and business.

Value Proposition Components

- Component:

Comprehensive Protection

Clarity:Clear

Uniqueness:Common

- Component:

Accessible Investing

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Confident Retirement Planning

Clarity:Clear

Uniqueness:Common

- Component:

Business Continuity Protection

Clarity:Clear

Uniqueness:Somewhat Unique

Principal's messaging attempts to differentiate through simplicity ('Let's keep your finances simple') and a holistic, lifelong partnership model ('for all life’s moments'). While the product offerings (insurance, retirement) are common in the industry, the framing is less about complex financial instruments and more about achieving life goals. This approachability is a key differentiator against more trading-focused or high-net-worth-oriented competitors like Fidelity or Charles Schwab.

The messaging positions Principal as a stable, reliable, and approachable partner for a broad audience, including individuals and small-to-medium-sized businesses. It avoids the jargon-heavy language of some competitors, aiming for the center of the market rather than niche, high-expertise segments. The focus on both individual and business needs under one brand umbrella positions it as a versatile, full-service provider.

Audience Messaging

Target Personas

- Persona:

The Individual Planner: An individual at various life stages looking to manage their personal finances, from starting out to planning for retirement.

Tailored Messages

- •

Dedicate part of each paycheck to big goals, such as retirement or education...

- •

Save a little each month and increase it over time.

- •

DIY financial plan: 8 simple steps...

Effectiveness:Effective

- Persona:

The Business Owner/Manager: A decision-maker concerned with protecting their business from financial disruption and retaining key talent.

Tailored Messages

- •

If the loss of a key employee or owner would create a financial challenge that puts the business at risk, explore our protection solutions.

- •

What would happen to your business if: An owner or key employee became too sick or hurt to work?

- •

Key person life insurance policies generally pay an income-tax-free death benefit to the business...

Effectiveness:Effective

Audience Pain Points Addressed

- •

Financial complexity and overwhelm

- •

Fear of the unexpected (death, disability)

- •

Uncertainty about having enough for retirement

- •

Risk of business disruption due to loss of key personnel

Audience Aspirations Addressed

- •

Retiring 'on your terms'

- •

Financial confidence and peace of mind

- •

Protecting loved ones

- •

Ensuring business longevity and stability

Persuasion Elements

Emotional Appeals

- Appeal Type:

Security & Peace of Mind

Effectiveness:High

Examples

Protect your life and wages so that no matter what happens, the people you love can keep moving forward.

Planning for the unexpected can protect your business—and everyone who depends on it.

- Appeal Type:

Empowerment & Control

Effectiveness:Medium

Examples

- •

Retire on your terms.

- •

Feel confident about investing

- •

Create your account

Social Proof Elements

- Proof Type:

Expert Endorsement

Impact:Moderate

Examples

In an exclusive webinar, Jean Chatzky, CEO of HerMoney, helps you plan...

Trust Indicators

- •

Reference to FINRA’s BrokerCheck

- •

Longevity and established brand name (Principal Financial Group®)

- •

Clear, detailed legal disclaimers and footnotes

- •

Professional website design and secure user account functionality

Scarcity Urgency Tactics

None observed; the messaging focuses on long-term planning, where urgency tactics would be inappropriate and counterproductive.

Calls To Action

Primary Ctas

- Text:

Calculate your income protection needs

Location:Homepage - 'Insure' Section

Clarity:Clear

- Text:

Check your retirement readiness

Location:Homepage - 'Retire' Section

Clarity:Clear

- Text:

Find a financial professional

Location:Homepage & Business Page

Clarity:Clear

- Text:

Watch now

Location:Homepage - Webinar Banner

Clarity:Clear

High. The CTAs are effective because they are varied, well-placed, and logically follow the messaging in each section. They offer a good mix of educational, tool-based actions ('Calculate', 'Check') and direct contact actions ('Find a financial professional'). The language is clear and sets accurate expectations for the user's next step.

Messaging Gaps Analysis

Critical Gaps

Lack of a strong, unifying brand story or 'Why'. The messaging is highly functional and explains what Principal does, but not the deeper purpose or belief system that drives the company.

Limited use of customer stories or case studies. The site would benefit from real-world examples of how Principal has helped individuals and businesses achieve their goals, which would make the value proposition more tangible and relatable.

Contradiction Points

No direct contradictions were found. However, there is a natural tension between the stated goal of 'simplicity' and the inherent complexity of financial products, evidenced by the extensive legal disclaimers.

Underdeveloped Areas

Competitive differentiation could be sharper. While 'simplicity' and 'holistic' are good themes, the messaging doesn't explicitly state why Principal's approach to these is superior to competitors like Voya, Prudential, or Ameriprise.

The emotional connection could be deepened. The messaging appeals to security, but it could also tap into more aspirational emotions like freedom, legacy, and achieving lifelong dreams.

Messaging Quality

Strengths

- •

Excellent clarity and structure. The three-pillar architecture on the homepage is very effective.

- •

Strong audience segmentation between individual and business needs.

- •

Consistent and trustworthy brand voice.

- •

Clear, logical, and effective calls-to-action.

Weaknesses

- •

Messaging is somewhat generic to the financial services industry; it lacks a memorable, unique narrative.

- •

Over-reliance on functional benefits (what the products do) versus emotional or philosophical benefits (what life looks like with Principal as a partner).

- •

Minimal use of social proof like customer testimonials or ratings.

Opportunities

- •

Develop a brand narrative around 'for all life's moments' by showcasing customer journeys and stories.

- •

Create more content that demonstrates the promise of 'simplicity' in action, such as explainer videos or interactive guides.

- •

Quantify the value provided where possible (e.g., 'Join X million people who trust Principal for their retirement').

Optimization Roadmap

Priority Improvements

- Area:

Brand Storytelling

Recommendation:Develop a core brand narrative that answers 'Why Principal?'. This story should be woven into the homepage and key landing pages to create a stronger emotional connection beyond the product features.

Expected Impact:High

- Area:

Differentiation

Recommendation:Sharpen the value proposition against 2-3 key competitors. Create messaging that explicitly contrasts Principal's 'simple, holistic' approach with the more complex, niche, or impersonal alternatives in the market.

Expected Impact:High

- Area:

Social Proof

Recommendation:Integrate customer testimonials, case studies (for businesses), and trust ratings (e.g., from industry bodies) more prominently across the site to validate claims and build trust.

Expected Impact:Medium

Quick Wins

- •

A/B test CTA button copy to optimize for conversion (e.g., 'Get My Readiness Score' vs. 'Check your retirement readiness').

- •

Add a concise, compelling tagline near the logo on the homepage that encapsulates the core value proposition.

- •

Feature a 'Customer Success Story of the Month' on the homepage to start building a library of relatable content.

Long Term Recommendations

- •

Invest in a content marketing strategy focused on telling customer stories across different life stages and business sizes, using video and written formats.

- •

Conduct audience research to further refine messaging for sub-segments (e.g., young investors vs. pre-retirees) to enhance personalization.

- •

Develop a messaging playbook that clearly defines the brand story, voice, tone, and competitive positioning to ensure consistency across all future marketing efforts.

Principal Financial Group's website messaging is strategically sound, with a clear architecture, consistent voice, and effective segmentation. Its core strength lies in its simplicity and clarity, successfully breaking down complex financial services into three understandable pillars: insuring, investing, and retiring. The brand voice is reassuring and professional, which is appropriate for the industry and effective at building foundational trust. However, the overall messaging, while functional, lacks a compelling, differentiated narrative that elevates it above the 'sea of sameness' in the financial services sector. The value proposition of being a simple, holistic partner is strong but not unique. The primary opportunity for Principal is to move from explaining what it does to evangelizing why it matters. By building a powerful brand story, incorporating tangible proof points like customer stories, and sharpening its competitive positioning, Principal can transform its solid but conventional messaging into a powerful engine for brand preference and customer acquisition.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Long-standing market presence since 1879, indicating sustained demand for its core products.

- •

Diversified portfolio of essential financial products: retirement, insurance, and investment management for individuals and businesses.

- •

Large and growing Assets Under Management (AUM), reaching $753 billion in Q2 2025, demonstrating significant customer trust and scale.

- •

Clear value proposition articulated on the website for both B2C ('Insure what matters. Invest when you’re ready. Retire on your terms.') and B2B ('Key person protection') segments.

Improvement Areas

- •

Enhancing digital-first product offerings to better attract and serve younger, digitally-native demographics.

- •

Improving the user experience for direct-to-consumer online onboarding to reduce friction.

- •

Developing more personalized, holistic financial wellness platforms rather than offering siloed products.

Market Dynamics

Moderate to High (Wealth management sector estimated CAGR of 8.5% - 10.7%).

Mature

Market Trends

- Trend:

Digital Transformation and FinTech Disruption

Business Impact:Traditional firms must invest in technology to compete with agile FinTechs on user experience, cost, and accessibility. This is a major focus for Principal.

- Trend:

Increased Demand for Retirement Income Solutions

Business Impact:An aging population and legislative changes (e.g., SECURE 2.0 Act) are creating a massive market for in-plan annuities and retirement income products, a core strength for Principal.

- Trend:

Growing Interest in ESG and Sustainable Investing

Business Impact:There is a significant opportunity to attract new assets by expanding ESG product offerings to meet rising investor demand.

- Trend:

Personalization through AI and Data Analytics

Business Impact:Leveraging AI to offer personalized advice and product recommendations can significantly improve customer acquisition and retention. Principal is actively investing in this area.

Favorable. Key market trends such as the focus on retirement income, digital adoption, and demand for wealth management services align directly with Principal's core competencies and strategic growth initiatives.

Business Model Scalability

High

Scalable cost structure with high initial fixed costs in technology and compliance, but low marginal costs for serving additional customers with financial products.

High. Increased AUM and customer base can be managed with proportionally smaller increases in operational staff, especially through digital platforms.

Scalability Constraints

- •

Regulatory compliance overhead, which increases with scale and expansion into new markets.

- •

Dependence on a human financial advisor network for certain products, which scales less efficiently than pure-tech models.

- •

Legacy IT systems can hinder the rapid deployment of new digital products and features.

Team Readiness

Experienced leadership team with a stated focus on strategic growth, digital transformation, and shareholder returns.

Traditional corporate structure appropriate for a mature company, but may need more agile, cross-functional teams to accelerate digital innovation.

Key Capability Gaps

- •

Agile product development and user experience (UX) design to compete with FinTech startups.

- •

Advanced data science and AI talent to fully leverage customer data for personalization.

- •

Digital marketing and direct-to-consumer (D2C) customer acquisition expertise.

Growth Engine

Acquisition Channels

- Channel:

Workplace Solutions (B2B2C)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Develop and promote more in-plan lifetime income solutions and financial wellness tools to deepen relationships with plan participants.

- Channel:

Financial Advisor Network

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip advisors with better digital tools for client management, prospecting, and delivering personalized advice to improve their efficiency and reach.

- Channel:

Direct Digital (SEO/Content Marketing)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Invest heavily in SEO and content marketing around key financial planning topics to attract and capture organic D2C leads for simpler products like IRAs or term life insurance.

- Channel:

Third-Party Administrators (TPAs)

Effectiveness:High

Optimization Potential:Low

Recommendation:Continue to nurture and support this highly effective channel, which has shown a 157% sales increase over four years.

Customer Journey

Primarily advisor-led. The website offers educational content and tools, but the main CTAs direct users to 'Find a financial professional', which can be a friction point for users seeking self-service options.

Friction Points

- •

Lack of fully online, self-service purchasing options for more complex products.

- •

Handoff between digital discovery (website) and offline action (meeting an advisor).

- •

Potentially fragmented user experience across different product silos (e.g., insurance vs. investments).

Journey Enhancement Priorities

{'area': 'Digital Onboarding', 'recommendation': 'Develop a streamlined, mobile-first onboarding process for core products like IRAs and simple investment accounts to capture D2C customers.'}

{'area': 'Holistic Customer View', 'recommendation': 'Leverage the Salesforce Data Cloud implementation to create a unified 360-degree customer view, enabling personalized cross-sell and upsell recommendations. '}

Retention Mechanisms

- Mechanism:

Product Stickiness & High Switching Costs

Effectiveness:High

Improvement Opportunity:Bundle related products (e.g., life insurance with retirement planning) to increase the 'moat' and make the customer relationship even stickier.

- Mechanism:

Advisor Relationships

Effectiveness:High

Improvement Opportunity:Augment human relationships with personalized digital nudges, alerts, and content based on customer data and life events.

- Mechanism:

Workplace Plan Default

Effectiveness:High

Improvement Opportunity:Improve post-employment engagement to capture rollovers and retain assets when an employee leaves their job.

Revenue Economics

Strong. The financial services industry is characterized by high-lifetime value (LTV) customers. The key is managing the customer acquisition cost (CAC) across different channels.

Undeterminable (Internal Data). Likely very healthy for established channels like workplace retirement plans; variable for direct D2C acquisition which requires optimization.

High. The company demonstrates consistent revenue growth, strong operating earnings, and a focus on returning capital to shareholders, indicating an efficient revenue model.

Optimization Recommendations

- •

Shift acquisition mix towards lower-cost digital channels for less complex products to improve overall CAC.

- •

Focus on increasing 'products per household' to maximize LTV of existing customer base.

- •

Leverage automation and AI to reduce the cost-to-serve, especially for smaller accounts.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Technology Stack

Impact:Medium

Solution Approach:Continue the stated digital transformation strategy, migrating core functions to modern platforms like the Accenture Life Insurance & Annuity Platform (ALIP) to increase agility and speed to market.

- Limitation:

Data Silos

Impact:Medium

Solution Approach:Accelerate the implementation and use of the Salesforce Data Cloud to unify customer data across business lines, enabling true personalization and a holistic customer view.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting and Onboarding Processes

Growth Impact:Slows down customer acquisition and increases operational costs.

Resolution Strategy:Implement straight-through processing and leverage AI/automation for underwriting simpler insurance products and opening investment accounts.

- Bottleneck:

Complex Regulatory and Compliance Workflows

Growth Impact:Can delay new product launches and market entry.

Resolution Strategy:Invest in 'RegTech' (Regulatory Technology) to automate compliance monitoring, reporting, and workflow management, reducing manual overhead.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Critical

Mitigation Strategy:Differentiate through superior customer experience, personalized advice (human + digital), and specialized product offerings (e.g., retirement income solutions). Competing on price alone is a losing battle against giants like Vanguard.

- Challenge:

Brand Perception with Younger Demographics

Severity:Major

Mitigation Strategy:Develop a sub-brand or a distinct product line with a modern, tech-focused value proposition. Use digital marketing channels and financial literacy content to build trust and relevance with millennials and Gen Z.

Resource Limitations

Talent Gaps

- •

Top-tier data scientists and AI/ML engineers.

- •

Growth marketing and product management talent with D2C FinTech experience.

- •

Cybersecurity experts to protect expanding digital infrastructure.

Moderate. Capital is needed for continued investment in technology, digital transformation, and potential strategic acquisitions of FinTech companies to accelerate capability building.

Infrastructure Needs

- •

Cloud-native platforms to replace legacy systems.

- •

A robust API infrastructure to enable partnerships and embedded finance opportunities.

- •

Advanced data analytics and customer data platform (CDP) capabilities.

Growth Opportunities

Market Expansion

- Expansion Vector:

Younger Demographics (Millennials/Gen Z)

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Launch a mobile-first, low-fee investment and financial planning platform. Focus on education, ease-of-use, and values-based investing (ESG).

- Expansion Vector:

International Emerging Markets

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Continue strategic expansion in Latin America and Asia, focusing on regions with a growing middle class and developing private pension systems.

- Expansion Vector:

Mass Affluent Segment

Potential Impact:Medium

Implementation Complexity:Medium

Recommended Approach:Develop a 'hybrid' advisory model that combines a digital platform with access to human advisors for a lower fee than traditional wealth management.

Product Opportunities

- Opportunity:

Integrated Financial Wellness Platform

Market Demand Evidence:Growing consumer demand for holistic financial management tools that combine saving, investing, insurance, and budgeting.

Strategic Fit:High

Development Recommendation:Leverage existing product lines and unified customer data to create a single dashboard view of a customer's entire financial life, offering AI-driven insights and recommendations.

- Opportunity:

Expanded ESG/Sustainable Investment Funds

Market Demand Evidence:Increasing inflows into ESG funds and stated interest from institutional investors.

Strategic Fit:High

Development Recommendation:Launch new thematic funds (e.g., clean energy, social impact) and ensure ESG options are prominently featured in all retirement plan offerings.

- Opportunity:

Retirement Income Solutions

Market Demand Evidence:An aging population and new regulations are driving massive demand for products that turn retirement savings into a reliable income stream.

Strategic Fit:Very High

Development Recommendation:Innovate on in-plan annuity products and develop new tools to help retirees manage decumulation, making this a key competitive differentiator.

Channel Diversification

- Channel:

Direct-to-Consumer (D2C) E-commerce

Fit Assessment:High (for simpler products)

Implementation Strategy:Build a fully digital purchase funnel for products like term life insurance, disability insurance, and IRAs, supported by transparent pricing and strong educational content.

- Channel:

Embedded Finance (B2B2C Partnerships)

Fit Assessment:Medium

Implementation Strategy:Develop APIs to allow FinTech apps (e.g., budgeting, payroll providers) to offer Principal's insurance or investment products directly within their platforms.

Strategic Partnerships

- Partnership Type:

FinTech Acquisition/Partnership

Potential Partners

- •

Robo-advisors (e.g., Betterment, Wealthfront - for technology/audience)

- •

Financial wellness apps (e.g., Mint, Personal Capital - for data/user engagement)

- •

InsurTech startups

Expected Benefits:Rapidly acquire modern technology, specialized talent, and access to new customer segments.

Growth Strategy

North Star Metric

Number of Households with >1 Principal Product

This metric focuses on deepening customer relationships, which directly increases LTV and retention. It encourages cross-selling across the company's diversified product lines (insurance, retirement, investments) and shifts focus from single transactions to long-term customer value.

Increase by 15% annually over the next 3 years.

Growth Model

Hybrid: Sales-Led & Product-Led Growth (PLG)

Key Drivers

- •

Advisor & TPA Network Productivity (Sales-Led)

- •

Workplace Plan Enrollment (Sales-Led)

- •

D2C Product Activation & Engagement (PLG)

- •

Digital Cross-Sell & Upsell Funnels (PLG)

Maintain and enhance the existing high-touch, sales-led model for complex B2B and high-net-worth clients while building a separate, fast-moving product-led growth engine for simpler, direct-to-consumer products.

Prioritized Initiatives

- Initiative:

Launch a 'Principal Digital' Mobile-First Investment Platform

Expected Impact:High

Implementation Effort:High

Timeframe:18-24 months

First Steps:Establish a dedicated, agile product team. Conduct market research on the target demographic (25-45 years old). Develop an MVP focused on IRA and taxable brokerage accounts.

- Initiative:

Optimize D2C Insurance Funnel

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:9-12 months

First Steps:A/B test website CTAs to offer 'Get an Instant Quote' alongside 'Find an Advisor'. Simplify the online application form. Implement a lead nurturing email sequence for abandoned applications.

- Initiative:

Develop a Retirement Income Planner Tool

Expected Impact:High

Implementation Effort:Medium

Timeframe:12 months

First Steps:Prototype a user-friendly digital tool that models different retirement income scenarios using Principal's annuity and investment products. Promote this tool heavily to existing 401(k) participants nearing retirement.

Experimentation Plan

High Leverage Tests

- Test:

Pricing models for hybrid advisory services.

Hypothesis:A tiered subscription fee model will attract more mass-affluent customers than a traditional AUM-based fee.

- Test:

Digital marketing channel allocation.

Hypothesis:Content marketing on platforms like TikTok and YouTube focused on 'Financial Literacy 101' will generate a lower CAC for young investors than traditional search ads.

- Test:

Onboarding flow for workplace retirement plans.

Hypothesis:A gamified, mobile-first onboarding experience will increase participant contribution rates by 5% compared to the current process.

Use a standard framework like AARRR (Acquisition, Activation, Retention, Referral, Revenue) for D2C products and track metrics like Funnel Conversion Rate, CAC, LTV, and Churn Rate for all experiments.

Weekly sprint-based testing for digital product teams; monthly reviews for larger marketing channel experiments.

Growth Team

Centralized Growth Leadership with Decentralized, Pod-Based Execution. A central Head of Growth sets strategy, but cross-functional 'pods' (each with a PM, engineer, marketer, analyst) are embedded within business units (e.g., 'D2C Growth Pod', 'Small Business Growth Pod') to drive initiatives.

Key Roles

- •

Head of Growth

- •

Growth Product Manager

- •

Data Scientist/Analyst

- •

Lifecycle Marketing Manager

- •

Acquisition Marketing Specialist

Acquire a small, agile FinTech company to inject talent and a growth mindset into the organization. Simultaneously, create an internal 'Growth Academy' to upskill existing employees in experimentation, data analysis, and growth marketing principles.

Principal Financial Group possesses a strong growth foundation, characterized by excellent product-market fit in the mature, yet evolving, financial services industry. Its diversified business across retirement, insurance, and asset management provides stability and significant cross-selling opportunities. The company's primary growth engine has historically been a successful sales-led model targeting workplace solutions and leveraging a network of financial advisors. However, the market is being fundamentally reshaped by digital transformation and competition from agile FinTech firms. The most significant barrier to accelerated growth is the potential for organizational inertia and legacy technology to slow adaptation to new consumer behaviors, particularly among younger demographics who expect seamless, digital-first experiences. The greatest growth opportunities lie in complementing its traditional strengths with a robust, product-led, direct-to-consumer (D2C) engine. This involves expanding into new demographic segments (the mass affluent and younger investors) with tailored digital products, diversifying acquisition channels beyond the advisor network, and creating integrated, personalized financial wellness platforms. A key strategic imperative is to bridge the gap between their high-quality products and the modern, digital customer journey. By successfully implementing a hybrid growth model that pairs its trusted brand and advisor network with an innovative, data-driven digital experience, Principal can capture new market segments, deepen existing relationships, and solidify its market leadership for the long term.

Legal Compliance

Principal maintains a comprehensive and globally focused 'Global Privacy Statement', which is a significant strength. The policy is layered, allowing users to navigate to specific sections of interest, and a downloadable PDF is available, enhancing accessibility. It explicitly addresses the rights of residents in California (CCPA/CPRA), the EEA, UK, and Switzerland (GDPR), demonstrating a clear intent to comply with major international data protection regimes. The policy details the categories of personal information collected, the sources, and the purposes for processing. A specific 'Principal Financial Group Customer Privacy Notice' also exists, tailored to the Gramm-Leach-Bliley Act (GLBA), which governs how US financial institutions handle nonpublic personal information (NPI). This GLBA notice clearly defines its scope, outlines the types of NPI collected, and describes the strict security standards in place to protect that data. The policy is transparent about data sharing practices, stating they do not share personal information with third parties for their marketing purposes, except in specific scenarios involving a client's financial professional. This aligns with GLBA provisions that give consumers the right to opt-out of sharing NPI with nonaffiliated third parties.

The 'Terms of Use' are present and clearly state that by accessing the website, users agree to the terms and conditions. The terms establish the website as the property of Principal and its affiliates and outline user responsibilities, including the certification of identity when accessing secure areas. This is crucial for a financial services site to prevent unauthorized access. The terms include an important 'Consent to do Business Electronically', which is vital for their business model of online account management and transactions. They also contain standard clauses regarding intellectual property (trademarks, logos), limitations of liability for links to third-party sites, and prohibitions on modifying third-party applications provided through the site. The enforceability appears standard, governed by the acceptance of terms through use.