eScore

synchrony.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Synchrony demonstrates a sophisticated digital presence, effectively targeting different user journeys. The 'Mover Hub' content strategy is a best-in-class example of capturing high-intent users early through excellent search intent alignment. While content authority is strong due to its market position and partner network, its multi-channel presence is somewhat bifurcated, with the Synchrony brand often being secondary to its retail partners in the consumer's mind.

Excellent execution of niche, high-value content hubs (e.g., 'Mover Hub') that align perfectly with user search intent for major life events.

Develop a more unified multi-channel brand voice that elevates the Synchrony brand itself, reducing its perceptual dependence on retail partners' branding.

The website effectively tailors transactional messages to specific audiences, such as 'Deal-Seeking Shoppers' and 'Life-Stage Planners'. However, the analysis reveals a significant weakness in brand-level communication; there is no single, unifying narrative that connects its disparate financing, banking, and B2B arms. This messaging fragmentation hinders the development of a strong, primary consumer brand and creates a disconnect between its mission of 'healthier financial lives' and its overwhelmingly promotional tone.

Clear and effective messaging for tactical, point-of-sale financing offers, leveraging partner brands as powerful social proof to drive conversions.

Develop and integrate a master brand narrative that cohesively links spending (financing), saving (banking), and business solutions under a single, unified value proposition.

The visual and UX analysis points to a well-structured site with a clear visual hierarchy and intuitive navigation, which minimizes cognitive load for users. Primary CTAs are prominent and effective, guiding users toward conversion. However, friction points are identified in the hand-off to application portals, a lack of interactive decision-support tools (like calculators), and a sub-optimal cookie consent banner that lacks a one-click 'Reject All' option.

A strong visual hierarchy and logical information architecture guide users effectively to primary CTAs like 'Apply Now' and 'Explore options'.

Introduce interactive decision-support tools, such as savings or financing calculators, to increase user engagement and provide personalized value, helping to guide users to the right product.

As a major financial institution, Synchrony excels in this dimension, demonstrating a mature and sophisticated legal compliance posture. The website prominently features key trust signals like 'FDIC-insured' logos, clear disclosures for financing (adhering to TILA), and a stated commitment to WCAG 2.1 AA accessibility standards. The use of dozens of major partner logos (Amazon, Lowe's, PayPal) serves as powerful third-party validation, mitigating perceived risk for consumers.

Meticulous adherence to industry-specific regulations like the Truth in Lending Act (TILA), with clear and conspicuous disclosures for complex financing offers, which builds trust and mitigates regulatory risk.

Consolidate the multiple, layered privacy policies into a simplified summary or FAQ page to improve transparency and reduce confusion for the average consumer.

Synchrony's competitive moat is deep and sustainable, built upon its market-leading scale and deeply entrenched, long-term partnerships with a vast network of retailers. This B2B2C model creates high switching costs for partners and generates a proprietary dataset on consumer spending that is extremely difficult for competitors to replicate. While threatened by agile fintechs, its established banking charter and compliance framework provide a significant, durable advantage.

The deeply entrenched network of exclusive, long-term retail partnerships creates a formidable barrier to entry and high switching costs for competitors.

Address the perception of being a 'traditional lender' by accelerating the development and integration of seamless, BNPL-like digital application processes to better compete with fintech challengers at the point-of-sale.

The B2B2C business model is inherently highly scalable, allowing revenue to grow faster than costs as transaction volume increases through its partner network. The direct digital bank provides a low-cost, scalable funding base (deposits) that supports the lending operations, a key strategic advantage for maintaining healthy unit economics. Expansion potential is strong, particularly in developing a 'Financing-as-a-Service' API platform to tap into the SMB market beyond large enterprise partners.

The dual-engine model, combining a low-cost, scalable deposit-gathering digital bank with a high-margin consumer lending business, creates a highly efficient and self-sustaining financial ecosystem.

Develop a scalable, self-service partner portal and standardized API library to streamline the onboarding process, which is currently a bottleneck for activating new revenue streams from mid-market and digital-native businesses.

Synchrony's B2B2C model is powerful and coherent, effectively aligning its resources (low-cost bank deposits) with its primary revenue driver (net interest income from partner-originated loans). The model is strategically focused on being the indispensable financing engine for its partners. However, a key incoherence exists at the brand level, where the direct-to-consumer banking arm and the B2B2C financing arm feel like separate entities, missing a significant opportunity for synergistic growth.

A highly effective dual-engine model where the digital bank gathers low-cost deposits to fund the profitable consumer lending business, creating a self-sustaining and cost-efficient value chain.

Better align the banking and financing arms by creating integrated products and messaging that encourage the vast cardholder base to become depositors, strengthening the model's funding advantage and increasing customer LTV.

As the largest provider of private label credit cards in the U.S., Synchrony exerts significant market power. Its pricing power is evident in the high net interest margins generated from its loan portfolio. The company's leverage with partners is substantial due to deep integration and the immense sales volume it facilitates, making it a critical component of their business strategy. This market leadership position is a clear indicator of its strong competitive standing.

Dominant market share as the largest provider of private label credit cards in the U.S., which provides significant leverage with partners and pricing power.

Mitigate customer dependency risk by continuing to diversify into new verticals and growing the direct-to-consumer business, reducing reliance on a few key mega-retailers for revenue.

Business Overview

Business Classification

Consumer Financial Services Platform

Private-Label Credit Card Issuer

Financial Services

Sub Verticals

- •

Consumer Lending

- •

Point-of-Sale (POS) Financing

- •

Digital Banking

- •

Healthcare Finance (CareCredit)

Mature

Maturity Indicators

- •

Publicly traded company (NYSE: SYF) spun off from GE Capital in 2014.

- •

Largest provider of private-label credit cards in the U.S. based on purchase volume and receivables.

- •

Extensive and long-standing partnerships with major national and regional brands.

- •

Significant scale with over 71.5 million active accounts and ~$105 billion in loan receivables.

- •

Consistent history of returning capital to shareholders through dividends and buybacks.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Interest Income

Description:The primary revenue driver, representing the difference between interest earned on consumer and commercial credit products (like credit card balances) and the interest paid on funding sources like high-yield savings accounts and CDs.

Estimated Importance:Primary

Customer Segment:B2C Credit Card Holders

Estimated Margin:High

- Stream Name:

Retailer Share Arrangements (Merchant Discounts)

Description:Fees paid by retail partners. This can be a percentage of the transaction value or other arrangements in exchange for providing financing solutions that drive sales and customer loyalty.

Estimated Importance:Secondary

Customer Segment:B2B Retail Partners

Estimated Margin:Medium

- Stream Name:

Cardholder Fees

Description:Non-interest income generated from cardholders, including late fees and other ancillary charges on credit accounts.

Estimated Importance:Tertiary

Customer Segment:B2C Credit Card Holders

Estimated Margin:High

- Stream Name:

Interchange Fees

Description:Fees earned on transactions made with Synchrony's general-purpose co-branded cards (e.g., Synchrony Premier Mastercard) through payment networks.

Estimated Importance:Tertiary

Customer Segment:B2C Co-branded Card Holders

Estimated Margin:Low

Recurring Revenue Components

Interest on revolving credit card balances

Contractual fees from retail partners

Pricing Strategy

Risk-Based Interest & Negotiated B2B Fees

Mid-range to Premium (for promotional financing)

Opaque

Pricing Psychology

- •

Promotional Pricing (0% APR for a limited time)

- •

Deferred Interest (No interest if paid in full within the promo period)

- •

Tiered Rewards

Monetization Assessment

Strengths

- •

Highly profitable net interest margin due to higher-than-average APRs on store cards.

- •

Diversified revenue across a wide range of retail partners and industries.

- •

Strong B2B value proposition drives partner acquisition and retention, securing revenue streams.

Weaknesses

- •

High sensitivity to economic downturns, which can increase credit losses and reduce consumer spending.

- •

Dependence on a concentrated number of large retail partners for a significant portion of revenue.

- •

Margin compression risk from rising interest rates on their deposit-based funding.

Opportunities

- •

Expanding the direct-to-consumer general-purpose card portfolio (e.g., Synchrony Premier Mastercard).

- •

Further penetration into the Buy Now, Pay Later (BNPL) market to compete with fintech rivals.

- •

Leveraging vast transaction data to offer value-added analytics services to retail partners.

Threats

- •

Intense competition from other large private-label issuers (e.g., Citi Retail Services, Capital One) and fintechs (e.g., Affirm, Klarna).

- •

Potential loss of a major retail partner could significantly impact revenue.

- •

Increased regulatory scrutiny on lending practices, late fees, and interest rates.

Market Positioning

B2B2C Partnership-Driven Model

Market Leader (Largest provider of private-label credit cards in the U.S.).

Target Segments

- Segment Name:

B2B: Enterprise & National Retailers

Description:Large, established retailers across sectors like home improvement, digital, apparel, and automotive (e.g., Lowe's, Amazon, JCPenney) seeking integrated, co-branded, or private-label credit programs to drive sales and loyalty.

Demographic Factors

- •

High purchase volume

- •

National or significant regional footprint

- •

Established customer base

Psychographic Factors

- •

Value customer loyalty

- •

Seek to increase average transaction value

- •

Data-driven marketing approach

Behavioral Factors

- •

Invest in point-of-sale marketing

- •

Desire for seamless digital and in-store financing integration

- •

Often have existing loyalty programs

Pain Points

- •

Complexity of managing a credit program in-house

- •

Need to increase sales and customer lifetime value

- •

Lack of deep consumer credit underwriting expertise

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

B2B: Healthcare & Wellness Providers (CareCredit)

Description:A diverse network of healthcare providers (dental, veterinary, vision, cosmetic) and wellness services seeking a simple way to offer patient financing for out-of-pocket expenses.

Demographic Factors

Small practices to large multi-location clinics

Services often not fully covered by insurance

Psychographic Factors

Focused on patient care and outcomes

Desire to reduce accounts receivable and payment collection burdens

Behavioral Factors

Seek trusted, well-known financing brands (endorsed by ADA, etc.)

Value integration with practice management software

Pain Points

- •

Patients delaying or declining care due to cost

- •

Administrative burden of billing and collections

- •

Risk of non-payment

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

B2C: Shoppers Seeking Promotional Financing

Description:Consumers making large, considered purchases (e.g., furniture, electronics, home repairs) who are attracted by special financing offers like 0% APR or equal monthly payments.

Demographic Factors

- •

Middle to upper-middle income

- •

Homeowners

- •

Varies widely based on retail partner

Psychographic Factors

- •

Value-conscious and deal-seeking

- •

Plan major purchases

- •

Desire financial flexibility and budget control

Behavioral Factors

- •

Triggered by life events (moving, renovating)

- •

Responsive to point-of-sale advertising

- •

Willing to apply for new credit for a significant benefit

Pain Points

- •

Inability to pay for a large purchase upfront

- •

Desire to avoid high interest rates from general-purpose credit cards

- •

Need for predictable, manageable monthly payments

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

B2C: Digital-First Savers

Description:Individuals comfortable with online-only banking who are seeking higher-than-average yields on their savings products (HYSAs, CDs, Money Market accounts) with the security of FDIC insurance.

Demographic Factors

Digitally savvy

All age and income levels, but trends younger

Psychographic Factors

- •

Rate-sensitive

- •

Prioritize returns and low fees over physical branch access

- •

Goal-oriented (saving for a down payment, emergency fund, etc.)

Behavioral Factors

Regularly compare interest rates online

Comfortable managing finances via web and mobile apps

Pain Points

- •

Low interest rates offered by traditional brick-and-mortar banks

- •

High fees associated with traditional banking

- •

Inconvenience of visiting a physical branch

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Unparalleled Partner Network Breadth

Strength:Strong

Sustainability:Sustainable

- Factor:

Specialized Healthcare Financing Network (CareCredit)

Strength:Strong

Sustainability:Sustainable

- Factor:

Proprietary Consumer Data & Analytics

Strength:Moderate

Sustainability:Sustainable

- Factor:

Integrated Digital and In-Store Technology Platform

Strength:Moderate

Sustainability:Sustainable

Value Proposition

For Business Partners: We provide a comprehensive, data-driven suite of financing solutions that seamlessly integrate into your sales process, driving increased sales, customer loyalty, and growth. For Consumers: We offer flexible and accessible ways to pay over time at your favorite brands and provide high-yield savings products to help you achieve your financial goals.

Good

Key Benefits

- Benefit:

Access to Promotional Financing (e.g., 0% APR)

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Homepage offers from Lowe's, Google, and Mattress Firm

Dedicated 'Marketplace' to browse offers

- Benefit:

Increased Sales and Average Order Value (for B2B)

Importance:Critical

Differentiation:Common

Proof Elements

Explicit statements in the 'For your business' section

The entire business model is predicated on this benefit

- Benefit:

High-Yield, FDIC-Insured Savings Products

Importance:Important

Differentiation:Common

Proof Elements

Competitive APY displayed on the homepage

Clear messaging on no fees and no minimums

- Benefit:

Specialized Healthcare Financing (CareCredit)

Importance:Critical

Differentiation:Unique

Proof Elements

Dedicated section on the homepage

Wide acceptance at over 266,000 provider locations.

Unique Selling Points

- Usp:

The largest and most diverse network of private-label credit card partnerships in the U.S.

Sustainability:Long-term

Defensibility:Strong

- Usp:

CareCredit's dominant and highly trusted position in the elective healthcare financing market.

Sustainability:Long-term

Defensibility:Strong

- Usp:

A dual-engine model that combines a low-cost, deposit-gathering digital bank with a high-margin consumer lending business.

Sustainability:Long-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Inability for consumers to afford large, necessary purchases upfront.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Retailers losing sales due to a lack of affordable customer financing options.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Consumers earning negligible interest on savings at traditional banks.

Severity:Major

Solution Effectiveness:Complete

- Problem:

Patients being unable to access or afford elective healthcare, dental, or veterinary procedures.

Severity:Critical

Solution Effectiveness:Complete

Value Alignment Assessment

High

Synchrony's model is perfectly aligned with the enduring market need for consumer credit at the point of sale, a key driver of retail and healthcare commerce. Their digital bank addresses the modern consumer's demand for higher yields and lower fees.

High

The value propositions are tailored directly to the primary pain points of their B2B and B2C segments, offering clear, tangible benefits (increased sales for partners, affordability for consumers).

Strategic Assessment

Business Model Canvas

Key Partners

- •

National and Regional Retailers (e.g., Lowe's, Amazon, Sam's Club, JCPenney)

- •

Digital Brands (e.g., PayPal, Verizon)

- •

Healthcare Providers & Networks (Dental, Veterinary, Vision, etc.)

- •

Automotive Service Centers

- •

Payment Networks (Mastercard, Visa)

- •

Technology Partners (e.g., Marqeta, Stripe)

Key Activities

- •

Credit Underwriting and Risk Management

- •

Developing and Managing Partner Programs

- •

Digital Platform and Mobile App Development

- •

Marketing and Customer Acquisition (for partners and direct)

- •

Deposit Gathering via Online Bank

- •

Data Analytics and Fraud Detection

Key Resources

- •

Banking License (Synchrony Bank)

- •

Extensive Consumer Credit and Spending Data

- •

Proprietary Technology and Analytics Platforms

- •

Large Capital Base and Diverse Funding Sources (primarily deposits)

- •

Brand Equity and Trusted Partner Relationships

- •

Skilled Workforce in Technology, Risk, and Marketing

Cost Structure

- •

Interest Expense (paid on deposits and other funding)

- •

Provision for Credit Losses (Net Charge-Offs)

- •

Employee Compensation and Benefits

- •

Retailer Share Arrangements (payments to partners)

- •

Marketing and Business Development

- •

Technology Infrastructure and Development

Swot Analysis

Strengths

- •

Market leadership as the largest U.S. private-label credit card issuer.

- •

Highly diversified portfolio across multiple industries, reducing single-sector risk.

- •

Strong, long-term relationships with premier retail and digital brands.

- •

Profitable business model with high net interest margins.

- •

Stable, low-cost funding base from its direct digital bank.

Weaknesses

- •

High exposure to the cyclicality of consumer spending and credit health.

- •

Revenue concentration with a few key partners represents a significant risk.

- •

Perception as a 'store card' company may limit appeal for direct-to-consumer products.

- •

Loan growth has shown signs of recent deceleration.

Opportunities

- •

Expansion of Buy Now, Pay Later (BNPL) offerings to better compete with fintechs.

- •

Growth in direct-to-consumer products, including general-purpose cards and digital banking services.

- •

Leverage AI and machine learning for enhanced underwriting, fraud detection, and personalized marketing.

- •

Further penetrate the high-growth wellness and healthcare financing market.

- •

Innovate in embedded finance and Web3 applications to deepen partner integration.

Threats

- •

Intense competition from established banks, credit card issuers, and agile fintechs.

- •

Potential for increased regulatory oversight on interest rates, fees, and lending practices.

- •

A significant economic downturn leading to higher unemployment and credit defaults.

- •

Shift in consumer preference away from traditional credit products.

- •

Loss or non-renewal of a major partner agreement (e.g., Amazon, Lowe's).

Recommendations

Priority Improvements

- Area:

Digital User Experience

Recommendation:Invest in a unified, best-in-class mobile application that seamlessly integrates all Synchrony products (retail cards, bank accounts, BNPL loans) to increase engagement and cross-selling opportunities with direct consumers.

Expected Impact:Medium

- Area:

Competitive Positioning vs. BNPL

Recommendation:Aggressively market and integrate 'Synchrony Pay Later' at the point of sale with existing and new partners, emphasizing the benefits of a trusted, established financial institution over newer fintech players.

Expected Impact:High

- Area:

Small & Mid-Sized Business (SMB) Offering

Recommendation:Develop a scalable, self-service financing platform for SMBs, bundling private-label credit and BNPL solutions to tap into a large, underserved market segment beyond enterprise retail.

Expected Impact:High

Business Model Innovation

- •

Develop a 'Financing-as-a-Service' (FaaS) API platform, allowing digital businesses of all sizes to embed Synchrony's credit and BNPL products directly into their checkout flows with minimal custom development.

- •

Create a premium, integrated financial product that links the Synchrony Premier Mastercard with the High Yield Savings account, automatically sweeping cash-back rewards into savings to create a powerful customer retention loop.

- •

Launch a data analytics subscription service for B2B partners, offering anonymized spending insights and customer behavior trends to help them optimize marketing and inventory beyond just financing.

Revenue Diversification

- •

Expand the portfolio of co-branded, general-purpose credit cards with partners in high-growth sectors not traditionally associated with store cards, such as travel, entertainment, and subscription services.

- •

Build out the Synchrony Bank offering with additional products like checking accounts or robo-advisory services to capture a greater share of the consumer's financial life.

- •

Monetize the 'Synchrony Marketplace' by introducing sponsored listings or affiliate marketing fees for partners looking to promote specific offers to Synchrony's large cardholder base.

Synchrony Financial operates a robust and highly profitable B2B2C business model, cementing its position as the market leader in private-label credit. Its core strength lies in its deeply entrenched, symbiotic relationships with a vast network of the nation's top retailers and healthcare providers. By providing the financial engine for point-of-sale financing, Synchrony makes itself indispensable to its partners' sales strategies while gaining access to millions of end consumers. The company's strategic masterstroke is its dual structure: a high-margin consumer lending operation funded by a stable, low-cost digital bank (Synchrony Bank), which gathers FDIC-insured deposits by offering competitive interest rates. This creates a powerful, self-sustaining financial ecosystem.

However, the model's reliance on consumer credit health and spending makes it vulnerable to macroeconomic headwinds. A slowdown in consumer spending or a rise in unemployment could lead to decelerating loan growth and increased credit losses, which are inherent risks. The competitive landscape is also intensifying, with agile fintechs in the Buy Now, Pay Later (BNPL) space challenging traditional credit models at the point of sale. While Synchrony has introduced its own BNPL products, market perception and partner adoption will be critical to defending its turf.

Future evolution hinges on three key areas: First, deepening its direct-to-consumer relationships. Evolving from a background partner into a primary financial brand in the consumer's mind will require significant investment in user experience and marketing for its direct products like the Synchrony Premier Mastercard and Synchrony Bank. Second, leveraging its vast data and AI capabilities not just for risk management, but as a value-added service for partners and a tool for hyper-personalization. Third, innovating beyond the traditional card framework by embracing embedded finance and scalable 'Financing-as-a-Service' models to capture the next generation of digital and SMB commerce. Successfully navigating these strategic shifts will be crucial for sustaining its market leadership and ensuring long-term, scalable growth.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

Regulatory Compliance and Banking Licenses

Impact:High

- Barrier:

Capital Requirements for Lending

Impact:High

- Barrier:

Establishing Retail Partnerships

Impact:High

- Barrier:

Brand Trust and Reputation

Impact:Medium

- Barrier:

Technology and Risk Management Infrastructure

Impact:Medium

Industry Trends

- Trend:

Rise of Buy Now, Pay Later (BNPL)

Impact On Business:Significant threat to traditional private label credit cards at the point ofsale, especially with younger demographics. It pressures interest income and forces issuers to offer more flexible, transparent financing options.

Timeline:Immediate

- Trend:

Digital and Mobile-First Transformation

Impact On Business:Consumers expect seamless digital application, account management, and payment experiences. Investment in user-friendly mobile apps and digital wallets is critical for retention.

Timeline:Immediate

- Trend:

Hyper-Personalization through Data Analytics

Impact On Business:Leveraging vast transaction data to provide personalized offers and financing terms is a key differentiator. Competitors are using AI to enhance these efforts.

Timeline:Near-term

- Trend:

Increased Regulatory Scrutiny

Impact On Business:Authorities like the CFPB are focusing on late fees and lending practices, which could compress profitability and require changes to business models.

Timeline:Immediate

- Trend:

Integration of Financial Products (Embedded Finance)

Impact On Business:Financing is becoming a more integrated part of the shopping experience, not a separate step. This requires deep technical integration with retail partners.

Timeline:Near-term

Direct Competitors

- →

Bread Financial (formerly Alliance Data)

Market Share Estimate:One of the top 6 PLCC issuers in the US.

Target Audience Overlap:High

Competitive Positioning:Positions itself as a tech-forward financial services company combining the stability of a bank with the agility of a fintech.

Strengths

- •

Strong portfolio of retail partners (e.g., Victoria's Secret, HSN).

- •

Acquired Bread (a BNPL player) to integrate modern payment options.

- •

Investing heavily in digital transformation and data analytics.

Weaknesses

- •

Undergoing a major brand and business model transition, which can create market confusion.

- •

Historically reliant on a traditional PLCC model, now playing catch-up in the fintech space.

- •

Revenue model is significantly dependent on late fees from subprime consumers, posing a regulatory risk.

Differentiators

Explicitly branding as a 'tech-forward' company to appeal to modern consumers and partners.

Offers a white-label product suite that includes PLCC, co-brand cards, installment loans, and BNPL.

- →

Citi Retail Services

Market Share Estimate:A top 6 PLCC issuer, part of one of the world's largest banking institutions.

Target Audience Overlap:High

Competitive Positioning:Leverages the power, stability, and global brand recognition of Citi to provide reliable credit solutions for major national retailers.

Strengths

- •

Backed by the immense resources and brand trust of Citigroup.

- •

Long-standing partnerships with major retailers like The Home Depot and Best Buy.

- •

Global operational scale and sophisticated risk management.

Weaknesses

- •

May be perceived as less agile or innovative compared to smaller, fintech-focused competitors.

- •

Large corporate structure could slow down decision-making and adaptation to new trends.

- •

Overall Citi brand faces competition from other major banks like JPMorgan Chase and Bank of America across all financial services.

Differentiators

The ability to offer partners the full suite of Citi's global banking capabilities.

Focus on co-branding that leverages the powerful Citi brand alongside the retailer's.

- →

Capital One

Market Share Estimate:A top 6 PLCC issuer and a major player in general-purpose credit cards.

Target Audience Overlap:High

Competitive Positioning:A technology-driven financial institution known for its strong data analytics capabilities and focus on digital-first customer experiences.

Strengths

- •

Strong direct-to-consumer brand recognition and marketing prowess.

- •

Advanced data analytics for underwriting and personalization.

- •

Successful history of acquiring and integrating large retail card portfolios (e.g., Williams-Sonoma).

- •

Strong digital tools and a highly-rated mobile app.

Weaknesses

- •

Recently ended its major partnership with Walmart, losing a significant portfolio.

- •

Potential for channel conflict between its own branded cards and its retail partner cards.

- •

Focus on transactors who don't carry a balance for co-brand cards may not align with all retail partners' goals.

Differentiators

Positions itself as a technology company that does banking.

Strong emphasis on simple, rewarding credit products for consumers.

- →

Wells Fargo Retail Services

Market Share Estimate:One of the top 6 PLCC issuers in the US.

Target Audience Overlap:High

Competitive Positioning:A traditional, full-service bank offering financing solutions to retail partners as part of a broader suite of financial services.

Strengths

- •

Vast, established customer base from its consumer banking operations.

- •

Extensive cross-selling opportunities through its branch network.

- •

Also a competitor in healthcare financing, directly challenging CareCredit.

Weaknesses

- •

Brand has suffered from reputational damage in the past.

- •

Often perceived as a more traditional and less innovative player.

- •

Retail services are a division of a massive bank, not its sole focus, potentially leading to less dedicated innovation.

Differentiators

Offers a turnkey PLCC platform for small to mid-sized merchants.

Ability to integrate financing with a wide range of Wells Fargo consumer and business banking products.

- →

Ally Bank

Market Share Estimate:N/A (Direct competitor to Synchrony's digital banking arm, not PLCC)

Target Audience Overlap:Medium

Competitive Positioning:A leading all-digital bank focused on customer-centricity, competitive rates, and no-fee banking.

Strengths

- •

Strong, trusted brand in the digital banking space.

- •

Highly competitive APYs on savings products.

- •

Excellent customer service reputation and user-friendly digital platform.

- •

Offers a broader range of consumer banking products including checking, investing, and auto loans.

Weaknesses

- •

No physical branch network, which may deter some customers.

- •

Does not have the embedded retail financing ecosystem that Synchrony possesses.

- •

Less focused on point-of-sale financing as a core business.

Differentiators

Customer-first branding and 'ally' positioning.

Comprehensive suite of digital-native financial products beyond just savings.

Indirect Competitors

- →

Affirm

Description:A leading Buy Now, Pay Later (BNPL) provider that offers consumers transparent, interest-bearing and non-interest-bearing installment loans at the point of sale.

Threat Level:High

Potential For Direct Competition:High, as it directly competes for financing decisions on large purchases where Synchrony's cards would be used.

- →

Klarna

Description:A global BNPL provider and shopping ecosystem that offers a range of payment options, from interest-free installments to longer-term financing, often integrated directly into a retailer's checkout.

Threat Level:High

Potential For Direct Competition:High, as its 'Pay in 4' model is a direct substitute for credit cards on smaller purchases, and its financing options compete on larger ones.

- →

PayPal

Description:A dominant digital wallet that offers its own BNPL services ('Pay in 4') and a revolving credit line (PayPal Credit), competing at checkout with a massive existing user base.

Threat Level:High

Potential For Direct Competition:Already a direct competitor at the point of sale through PayPal Credit.

- →

JPMorgan Chase & Co.

Description:The largest US credit card issuer by outstanding balance. Its general-purpose rewards cards (e.g., Sapphire, Freedom) compete for 'top-of-wallet' status for all consumer spending.

Threat Level:Medium

Potential For Direct Competition:Is a direct competitor in the co-brand space and competes indirectly for all other consumer spending.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Deeply Entrenched Retail Partnerships

Sustainability Assessment:Highly sustainable due to long-term contracts, deep technical integration, and the high switching costs for large retail partners.

Competitor Replication Difficulty:Hard

- Advantage:

Scale and Data Analytics

Sustainability Assessment:Sustainable due to the massive volume of transaction data collected across a diverse set of retail categories, which creates a powerful network effect for risk modeling and marketing.

Competitor Replication Difficulty:Hard

- Advantage:

Diversified Portfolio and Expertise

Sustainability Assessment:Highly sustainable. Expertise spans dozens of retail sectors from home goods to healthcare (CareCredit), reducing reliance on any single industry.

Competitor Replication Difficulty:Medium

- Advantage:

Established Banking Charter and Compliance Framework

Sustainability Assessment:Very sustainable, as obtaining a banking charter and building the necessary compliance and regulatory infrastructure is a significant barrier to entry for non-bank competitors.

Competitor Replication Difficulty:Hard

Temporary Advantages

{'advantage': 'Exclusive Promotional Financing Offers', 'estimated_duration': 'Short-term (per promotional period)'}

{'advantage': 'First-Mover in Niche Financing Categories', 'estimated_duration': '1-3 years'}

Disadvantages

- Disadvantage:

Perception as a Traditional Lender

Impact:Major

Addressability:Moderately

- Disadvantage:

Dependence on Retail Partner Health

Impact:Major

Addressability:Difficult

- Disadvantage:

Negative Sentiment from High Post-Promotional APRs

Impact:Major

Addressability:Moderately

- Disadvantage:

Complex User Experience vs. BNPL

Impact:Critical

Addressability:Easily

Strategic Recommendations

Quick Wins

- Recommendation:

Simplify the Digital Application Process

Expected Impact:High

Implementation Difficulty:Easy

- Recommendation:

Increase Transparency of Promotional Terms

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Prominently Feature BNPL-like 'Pay Later' Options on Partner Sites

Expected Impact:High

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Expand 'Life Event' Content Hubs

Expected Impact:Medium

Implementation Difficulty:Moderate

- Recommendation:

Develop a Unified 'Synchrony Wallet' App

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Leverage AI to Proactively Offer Personalized Financing

Expected Impact:High

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Build a Stronger Direct-to-Consumer Brand

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Acquire a Fintech to Accelerate Digital Product Development

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Expand into Adjacent Financial Wellness and Advisory Services

Expected Impact:Medium

Implementation Difficulty:Difficult

Reposition Synchrony as a comprehensive 'Life & Commerce' financing partner, moving beyond the perception of just a 'store card company'. Emphasize the breadth of its offerings from healthcare (CareCredit) to home goods to high-yield savings, all enabled by powerful technology.

Differentiate through the unparalleled breadth of its partner network and the depth of its consumer data. While fintechs may win on simplicity for a single transaction, Synchrony can win on creating lifelong value and personalized financing across all of a consumer's major life purchases.

Whitespace Opportunities

- Opportunity:

Financing for the Subscription/Creator Economy

Competitive Gap:Few traditional lenders offer tailored financing solutions for recurring revenue businesses or for individuals purchasing high-value digital goods and services.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Integrated B2B2C Financing Solutions

Competitive Gap:Provide financing not just to the end consumer, but also to the small businesses within the ecosystem of large retail partners (e.g., financing for contractors who shop at Lowe's).

Feasibility:Medium

Potential Impact:High

- Opportunity:

Sustainable/Green Purchase Financing

Competitive Gap:There is growing consumer demand for financing products that incentivize sustainable purchases (e.g., energy-efficient appliances, EVs). This is a gap most PLCC issuers have not addressed.

Feasibility:High

Potential Impact:Medium

- Opportunity:

Expanded 'Life Event' Financing Hubs

Competitive Gap:The 'Mover Hub' concept is strong but underdeveloped. Competitors focus on transactional financing. Synchrony can own life-event financing (e.g., Wedding Hub, New Parent Hub, Home Renovation Hub) by bundling content, partner offers, and financing.

Feasibility:High

Potential Impact:High

Synchrony Financial operates in the mature and highly concentrated consumer financial services industry, where it holds a formidable position as a leading issuer of private label and co-branded credit cards. Its core sustainable advantages are its deeply embedded, long-term partnerships with a vast and diverse network of retailers, the immense scale of its operations, and the rich consumer spending data it generates. These create significant barriers to entry for new players and are difficult for existing competitors to replicate at scale.

The competitive landscape is defined by a primary tension between established issuers and agile, tech-forward disruptors. Direct competitors like Bread Financial and Capital One are aggressively rebranding and investing in technology to bridge the gap between traditional credit and modern fintech. Bread Financial's acquisition of a BNPL player and its 'tech-forward' positioning is a direct response to the industry's biggest threat. Meanwhile, giants like Citi Retail Services and Wells Fargo leverage the stability and brand power of their parent banking institutions to maintain their market position.

The most significant threat comes from indirect competitors, specifically Buy Now, Pay Later (BNPL) providers like Affirm, Klarna, and PayPal. These firms have fundamentally altered consumer expectations at the point of sale, offering simple, transparent, and often interest-free installment options that directly cannibalize the use case for traditional credit cards, especially for younger consumers. This has shifted the competitive battleground from securing a spot in the physical wallet to being the most convenient, integrated option in the digital checkout.

Synchrony's own digital banking arm competes in a different but equally fierce arena against customer-centric online banks like Ally and Marcus by Goldman Sachs, who often lead on APY and digital experience.

Opportunities for Synchrony lie in leveraging its greatest asset—its diverse partner network—in more innovative ways. The 'Mover Hub' on its website is a nascent example of a key strategic direction: moving from transactional financing to 'life-event' based financial solutions. By creating ecosystems around major life purchases (moving, home renovation, healthcare), Synchrony can differentiate itself from the single-transaction focus of BNPL providers. Further whitespace exists in financing for the growing subscription and creator economies, and in offering integrated financing for the small business customers of its large retail partners.

To secure its future, Synchrony must accelerate its digital transformation to match the seamless experience of its fintech rivals, enhance the transparency of its credit products to rebuild consumer trust, and strategically reposition its brand as a comprehensive, tech-enabled partner for financing life's most important moments.

Messaging

Message Architecture

Key Messages

- Message:

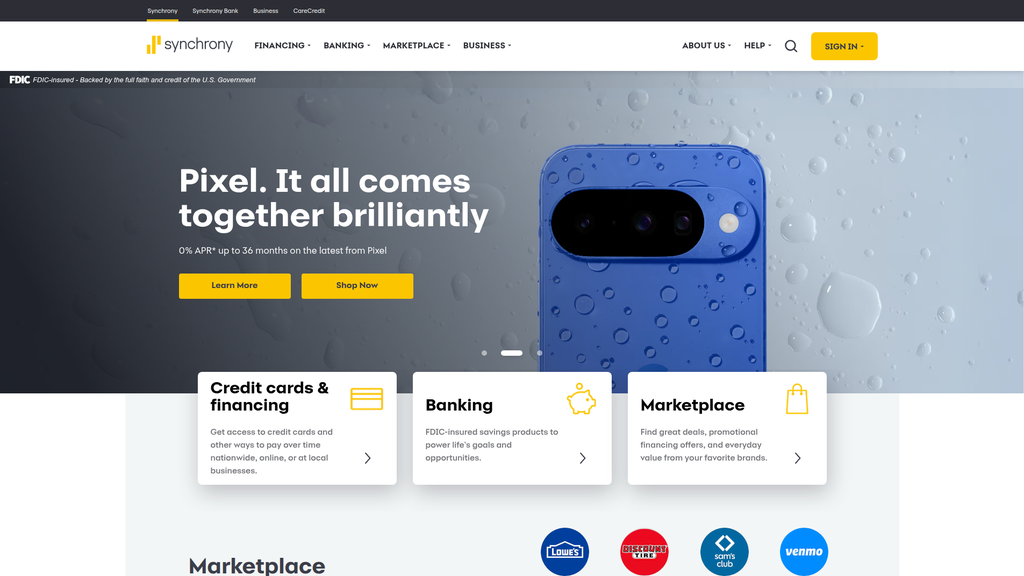

Access promotional financing and special offers from top brands (e.g., 0% APR* up to 36 months on the latest from Pixel).

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Carousel

- Message:

Get access to credit cards and other ways to pay over time nationwide.

Prominence:Primary

Clarity Score:High

Location:Homepage Body - 'Credit cards & financing'

- Message:

Grow your savings with FDIC-insured products like High Yield Savings Accounts.

Prominence:Secondary

Clarity Score:High

Location:Homepage Body - 'Banking'

- Message:

Synchrony provides payment solutions your customers can count on.

Prominence:Secondary

Clarity Score:Medium

Location:Homepage Body - 'For your business'

- Message:

Shop special offers that help you get back on track on Synchrony Marketplace.

Prominence:Primary

Clarity Score:Medium

Location:Homepage Hero Carousel / Body

The message hierarchy is heavily skewed towards immediate, transactional consumer financing offers with retail partners. The hero section, which gets the most attention, rotates through these tactical deals. Core brand pillars like 'Credit cards & financing,' 'Banking,' and 'Marketplace' are presented with equal weight just below the hero, but the 'Marketplace' and financing messages dominate the rest of the page. The B2B messaging ('For your business') and direct banking products feel secondary and are positioned further down the page, suggesting they are not the primary focus for a first-time website visitor.

Messaging is consistent within its silos but lacks a strong, unifying thread across them. The 'Financing/Marketplace' sections consistently use promotional, offer-driven language. The 'Banking' section adopts a more stable, reassuring tone focused on security (FDIC insured) and value (APY). The 'Business' section uses standard B2B language about growth and solutions. The 'Mover Hub' content page successfully maintains a helpful, advisory tone. However, there is no clear narrative that connects these disparate offerings into a single, cohesive brand story about what Synchrony stands for.

Brand Voice

Voice Attributes

- Attribute:

Promotional

Strength:Strong

Examples

- •

0% APR* up to 36 months on the latest from Pixel

- •

Enjoy 12 or 18 Months Special Financing!*

- •

Join the club for just $20. That’s 60% off!

- Attribute:

Transactional

Strength:Strong

Examples

- •

See If I Prequalify

- •

Shop Now

- •

Apply now

- Attribute:

Helpful / Advisory

Strength:Moderate

Examples

- •

This checklist offers actionable steps you can take before, during and after the move to make the transition a little more simple and a little less stressful.

- •

Learn how to make your home irresistible to potential buyers!

- •

Tips to Create a Helpful Moving Budget

- Attribute:

Reassuring / Secure

Strength:Weak

Examples

FDIC-insured - Backed by the full faith and credit of the U.S. Government

Bank with confidence through competitive, FDIC insured products.

Tone Analysis

Promotional

Secondary Tones

Transactional

Helpful

Tone Shifts

Shifts from a highly promotional, sales-driven tone on the homepage to a more helpful, advisory tone on the 'Mover Hub' content page.

A noticeable shift occurs when moving from financing offers to the 'Banking' section, where the tone becomes more conservative and security-focused.

Voice Consistency Rating

Fair

Consistency Issues

The brand voice is not unified. It changes significantly depending on the product line (financing vs. banking vs. B2B). This creates a fragmented brand experience.

The overwhelmingly promotional tone of the homepage overshadows the company's stated mission of supporting 'healthier financial lives,' creating a potential disconnect between brand promise and brand experience.

Value Proposition Assessment

Synchrony's core value proposition is providing consumers with flexible and accessible financing options through a vast network of retail and service partners, enabling them to make purchases over time.

Value Proposition Components

- Component:

Promotional Financing (0% APR, special terms)

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Broad Partner Network (Lowe's, Amazon, etc.)

Clarity:Clear

Uniqueness:Unique

- Component:

Competitive High-Yield Savings Products

Clarity:Clear

Uniqueness:Common

- Component:

Centralized Marketplace for Deals

Clarity:Somewhat Clear

Uniqueness:Somewhat Unique

Synchrony's primary differentiation comes from the sheer breadth and scale of its partner network. While competitors exist in point-of-sale financing (e.g., Affirm, Klarna) and co-branded cards (e.g., Capital One, American Express), Synchrony's model is deeply integrated with a massive number of retailers, positioning them as a key enabler of commerce. The 'Marketplace' concept is an attempt to leverage this network into a consumer-facing destination, which is a moderate differentiator. The direct banking offering, while solid, competes in a crowded market and is not a primary differentiator.

The messaging positions Synchrony as a ubiquitous financing partner that makes purchasing easier. By showcasing logos of major brands like Lowe's, Amazon, and Sam's Club, they position themselves as a trusted, established player. However, the brand itself is positioned in the background, acting as the engine for its partners. The website struggles to position Synchrony as a primary consumer brand, instead functioning more like a portal to its partners' offers.

Audience Messaging

Target Personas

- Persona:

Deal-Seeking Shopper

Tailored Messages

- •

Shop special offers that help you get back on track on Synchrony Marketplace.

- •

0% Interest for 72 Months††

- •

Enjoy 12 or 18 Months Special Financing!*

Effectiveness:Effective

- Persona:

Life-Stage Planner (e.g., Home Mover)

Tailored Messages

- •

Mover Hub by Synchrony HOME makes it simpler for movers to budget, plan, and pay for moving expenses.

- •

The Ultimate Synchrony HOME™ Moving Checklist

- •

Tips to Create a Helpful Moving Budget

Effectiveness:Effective

- Persona:

Business Owner / Manager

Tailored Messages

Synchrony provides payment solutions your customers can count on so you can focus on what matters — your business.

Big solutions for small businesses

Effectiveness:Somewhat Effective

- Persona:

Safety-Conscious Saver

Tailored Messages

Bank with confidence through competitive, FDIC insured products.

Save for everything that matters to you—with great rates and no monthly fees or minimum balance requirements.

Effectiveness:Somewhat Effective

Audience Pain Points Addressed

- •

Inability to afford large purchases upfront.

- •

The stress and complexity of managing moving expenses.

- •

Desire to find the best deals and financing offers.

- •

Concern about the safety and security of savings.

Audience Aspirations Addressed

- •

Acquiring desired goods and services immediately (e.g., new phone, mattress).

- •

Achieving life's goals and opportunities through savings.

- •

Creating a new home that reflects personal style.

- •

Growing a business by offering flexible payment options to customers.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Aspiration / Achievement

Effectiveness:Medium

Examples

Invest in you with Synchrony Bank

FDIC-insured savings products to power life's goals and opportunities.

- Appeal Type:

Convenience / Simplicity

Effectiveness:High

Examples

Find your way to pay

Mover Hub by Synchrony HOME makes it simpler for movers to budget, plan, and pay for moving expenses.

Social Proof Elements

- Proof Type:

Partner Logos / 'As seen in'

Impact:Strong

Examples

Displaying logos of dozens of well-known brands like Lowe's, Amazon, Sam's Club, Venmo, and Walgreens.

Trust Indicators

- •

FDIC-insured - Backed by the full faith and credit of the U.S. Government

- •

Prominent display of trusted partner logos

- •

Clear disclosure links (*DISCLOSURES)

Scarcity Urgency Tactics

- •

Valid now through 9/3/25.

- •

Expiring in 3 days

- •

Limited time.

Calls To Action

Primary Ctas

- Text:

See If I Prequalify

Location:Homepage Hero / Partner Offers

Clarity:Clear

- Text:

Shop Now

Location:Homepage Hero

Clarity:Clear

- Text:

Explore offers

Location:Homepage Hero / Marketplace Sections

Clarity:Clear

- Text:

Apply now

Location:Homepage - Synchrony Premier Mastercard

Clarity:Clear

- Text:

Explore Synchrony Bank

Location:Homepage - Banking Section

Clarity:Clear

The CTAs are generally clear, transactional, and action-oriented. They effectively guide users toward the next step for a specific offer (e.g., 'Apply Now', 'Shop Now'). However, the sheer volume of competing CTAs on the homepage can create cognitive overload, potentially reducing the effectiveness of any single one. There's a lack of higher-funnel, relationship-building CTAs; the focus is almost entirely on immediate conversion.

Messaging Gaps Analysis

Critical Gaps

- •

A clear, overarching brand narrative. The website fails to answer 'What is Synchrony and why should I choose it as my primary financial partner?' It presents itself as a collection of products and partner offers rather than a cohesive brand.

- •

A unified value proposition. The messaging for financing, banking, and B2B services is disconnected, making it difficult for a user to understand the holistic value of having a relationship with Synchrony.

- •

Customer-centric storytelling. The site lacks stories or testimonials from customers who have benefited from Synchrony's products, which would add an emotional connection and build trust.

Contradiction Points

There is a subtle tension between the company mission of promoting 'healthier financial lives' and the website's heavy emphasis on promotional credit, spending, and taking on debt. The 'savings' message is present but significantly downplayed compared to the 'financing' message.

Underdeveloped Areas

- •

The 'Marketplace' concept is underdeveloped. It's presented as a collection of logos and offers but could be a much richer experience that guides users through discovery and financial planning.

- •

The B2B value proposition is generic. Messaging like 'Big impact for your customers' and 'Your business is our business' could be strengthened with concrete data, case studies, or more specific benefits.

- •

The connection between the products is not messaged. There is no narrative explaining how using Synchrony financing could be a pathway to building a better financial future with Synchrony Bank, for example.

Messaging Quality

Strengths

- •

Clear communication of tactical offers. The terms, duration, and benefits of specific financing deals are easy to understand.

- •

Effective use of partner brands as social proof, which immediately builds credibility and trust.

- •

Strong, direct calls-to-action that leave no ambiguity about the desired next step.

- •

Good content marketing execution on specific pages like the 'Mover Hub,' which provides genuine value to a niche audience.

Weaknesses

- •

Lack of a unifying brand story and a clear 'why' for the consumer.

- •

Fragmented messaging and inconsistent voice across different business units.

- •

Overwhelmingly transactional focus on the homepage, which can feel cluttered and may alienate users not immediately looking for a loan.

- •

The Synchrony brand itself feels secondary to its partners' brands.

Opportunities

- •

Develop a master brand narrative around 'financial flexibility' or 'powering your possibilities,' connecting the acts of spending, saving, and financing.

- •

Create clearer user journeys from the homepage for different personas (Shopper, Saver, Business Owner) to reduce clutter and improve relevance.

- •

Humanize the brand by featuring customer success stories and testimonials.

- •

Elevate the 'Marketplace' from a simple offer grid to a guided shopping and financing experience.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Message Hierarchy

Recommendation:Revise the homepage to lead with a single, clear brand value proposition about what Synchrony does for people, before branching into the three main product areas (Financing, Banking, Business). This will establish the brand first, then the products.

Expected Impact:High

- Area:

Brand Narrative

Recommendation:Develop and integrate a consistent brand story across all sections. For example, frame all offerings as tools that give people more control and options for their financial lives, linking the mission to the products.

Expected Impact:High

- Area:

Audience Segmentation

Recommendation:Implement a simple segmentation choice high on the homepage (e.g., 'I want to...', 'I am a...'). This would allow for more tailored messaging paths for consumers, savers, and business clients from the very first interaction.

Expected Impact:Medium

Quick Wins

- •

Simplify the homepage hero section. Instead of a carousel of disparate partner offers, use the space to communicate the core brand value proposition with a single, powerful CTA.

- •

Add a 'Who We Are' or 'What We Do' module on the homepage that explains the Synchrony brand in simple terms, bridging the gap between financing and banking.

- •

Incorporate more trust-building language from the banking section (e.g., 'partnering in your financial future') into the financing sections to soften the purely transactional tone.

Long Term Recommendations

- •

Invest in content marketing that tells the stories of how real customers have used Synchrony's suite of products to achieve significant life goals, thereby giving substance to the 'healthier financial lives' mission.

- •

Conduct a comprehensive brand voice and messaging architecture overhaul to create a single, cohesive communication strategy that can be adapted for different audiences without feeling disconnected.

- •

Re-evaluate the user experience of the 'Marketplace' to transform it from a passive list of offers into an active, guided tool for financial planning and smart shopping.

Synchrony's strategic messaging is a tale of two different approaches that are not yet in 'sync.' On one hand, its tactical, product-level messaging is highly effective. For consumers seeking financing for a specific purchase, the value propositions are clear, compelling, and backed by the powerful social proof of major retail partners. The calls-to-action are direct and unambiguous, driving conversion effectively. On the other hand, its brand-level strategic messaging is fragmented and underdeveloped. The website does an excellent job of presenting what Synchrony offers but a poor job of explaining who Synchrony is and why a customer should build a broader relationship with the brand.

The core challenge is the lack of a unifying narrative. The website functions as three separate businesses—a B2B2C financing arm, a direct-to-consumer bank, and a B2B solutions provider—housed under one URL. The messaging for each is siloed, with distinct tones and value propositions. This creates a disjointed user experience and fails to build brand equity for 'Synchrony' itself. The brand's mission to support 'healthier financial lives' feels aspirational rather than actualized in the messaging, which is overwhelmingly weighted towards enabling spending and credit.

From a business perspective, this messaging gap presents a significant missed opportunity. By not connecting the dots between its services, Synchrony makes it difficult to cross-sell its banking products to its massive base of financing customers. A user who gets a Lowe's card might never realize Synchrony also offers a high-yield savings account because the brand story doesn't bridge that gap. The differentiation, which lies in Synchrony's immense partner ecosystem, is used effectively for credibility but not leveraged to build a unique consumer-facing brand identity.

To drive better business outcomes, the messaging strategy must pivot from being product-led to being brand-led. This involves establishing a clear, customer-centric value proposition at the top of the communication hierarchy that unites the disparate product lines under a single, compelling promise of financial empowerment and flexibility. By clarifying its identity and telling a more cohesive story, Synchrony can more effectively position itself not just as a means to a transaction, but as a long-term financial partner.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Synchrony is the largest provider of private label credit cards in the U.S. by purchase volume and receivables, indicating deep integration with major retailers.

- •

Long-term, exclusive partnerships with hundreds of major brands like Lowe's, Amazon, Sam's Club, and PayPal demonstrate significant B2B value proposition.

- •

Operates a massive network with approximately 480,000 partner locations and 71.5 million active accounts.

- •

The CareCredit platform is a market leader in healthcare financing, with over 250,000 enrolled providers, showing strong fit in a specialized, high-growth vertical.

- •

Successful direct-to-consumer banking arm (Synchrony Bank) with competitive high-yield savings products provides a stable, low-cost funding base.

Improvement Areas

- •

Enhancing the value proposition of its own branded products (e.g., Synchrony Premier Mastercard) to reduce reliance on partner brands.

- •

Improving the digital user experience to match the seamlessness of fintech competitors like Klarna and Affirm.

- •

Further integrating Buy Now, Pay Later (BNPL) options across all partner platforms to capture changing consumer preferences.

Market Dynamics

Private Label Credit Card market expected to grow at a CAGR of 7.2% from 2025 to 2033. The Buy Now, Pay Later (BNPL) market is forecasted to grow exponentially, with some projections at a CAGR of over 40%.

Mature but Evolving

Market Trends

- Trend:

Explosive Growth of Buy Now, Pay Later (BNPL)

Business Impact:BNPL presents both a threat and an opportunity. It competes with traditional credit cards but also offers a new product line. Synchrony is integrating BNPL but faces intense competition from fintech pure-plays.

- Trend:

Digital Transformation and Fintech Competition

Business Impact:Consumers expect seamless, mobile-first digital experiences. Fintechs are setting a high bar, pushing Synchrony to accelerate its own digital innovation in areas like AI-powered underwriting and personalization.

- Trend:

Increased Regulatory Scrutiny

Business Impact:BNPL and consumer credit are facing increased regulatory oversight globally, which could impact product structuring, fee income (e.g., late fees), and affordability checks, increasing compliance costs.

- Trend:

Demand for Personalization and Data Analytics

Business Impact:Leveraging its vast transactional data to offer personalized financing and rewards is critical for retaining customers and providing value to partners. Failure to do so creates an opening for competitors.

Favorable, but requires rapid adaptation. The market for consumer credit is robust, but the shift in consumer behavior towards flexible, digital-first financing solutions means Synchrony must accelerate its transformation to capitalize on growth trends and fend off disruption.

Business Model Scalability

High

The B2B2C model has a scalable cost structure. The core technology platform and risk management infrastructure can support new partners with incremental costs, rather than linear increases.

High. As transaction volume grows through its partner network, revenue should increase faster than the fixed costs of technology, compliance, and core operations.

Scalability Constraints

- •

Partner integration complexity and timeline for onboarding major new retailers.

- •

Ability to maintain robust credit risk and fraud models at scale, especially in new product areas like BNPL.

- •

Scaling customer service operations to handle a growing and diverse cardholder base.

Team Readiness

Experienced. The leadership team has a history of managing large-scale financial operations and has recently reorganized to accelerate growth and digital transformation, indicating adaptability.

Recently Optimized for Growth. The 2021 reorganization into five market-focused platforms (Digital, Health & Wellness, Home & Auto, etc.) and the creation of a dedicated Growth Organization suggest a structure designed for deeper industry expertise and faster execution.

Key Capability Gaps

- •

Agile Product Development talent to compete with fintech speed.

- •

User Experience (UX) and Design Thinking expertise to create best-in-class consumer-facing digital products.

- •

Data Science and Machine Learning talent focused on hyper-personalization and advanced risk modeling beyond traditional credit metrics.

Growth Engine

Acquisition Channels

- Channel:

Retail Partner Point-of-Sale (In-store & Online)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Deploy more seamless, API-driven integration for partner checkouts (like the Adobe Commerce integration) to reduce friction and improve conversion. Use data to prompt targeted financing offers at the moment of consideration.

- Channel:

Direct-to-Consumer Digital (Synchrony Bank & Website)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Invest in SEO and content marketing (e.g., expanding the 'Mover Hub' concept to other life events) to attract customers directly for high-yield savings and the Premier Mastercard. This diversifies away from partner reliance.

- Channel:

Healthcare Provider Network (CareCredit)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Expand the definition of 'wellness' to include more elective procedures and services, and create digital tools for providers to easily present financing options to patients.

Customer Journey

Primarily partner-led. The journey starts at a retail partner's site or store, where a financing offer is presented. The application and approval process is the key conversion funnel.

Friction Points

- •

Hand-off from partner website to Synchrony's application portal can feel disjointed.

- •

Lengthy or complex application forms can lead to abandonment, especially on mobile devices.

- •

Lack of clarity on credit approval criteria for consumers before they apply.

Journey Enhancement Priorities

{'area': 'Application Process', 'recommendation': "Implement a 'one-click' application for existing Synchrony customers and leverage embedded finance APIs for a fully native partner checkout experience."}

{'area': 'Onboarding & Activation', 'recommendation': 'Develop a personalized digital onboarding sequence that highlights card benefits relevant to the originating partner and cross-promotes other relevant Synchrony services.'}

Retention Mechanisms

- Mechanism:

Partner-Specific Utility & Rewards

Effectiveness:High

Improvement Opportunity:Use data analytics to create personalized, dynamic reward offers instead of static, one-size-fits-all promotions. Deepen integration with partner loyalty programs.

- Mechanism:

Direct Bank Ecosystem

Effectiveness:Medium

Improvement Opportunity:Create stronger incentives for cardholders to open a Synchrony Bank savings account, creating stickiness beyond a single retail relationship (e.g., preferential rates, enhanced cashback).

- Mechanism:

Promotional Financing Offers

Effectiveness:High

Improvement Opportunity:Proactively offer new financing deals to existing customers based on their purchase history across the Synchrony network, not just with the original partner.

Revenue Economics

Strong but under pressure. Primarily driven by Net Interest Margin (NIM) from card receivables. This is supplemented by fee income, which is facing regulatory headwinds. The direct bank provides a low-cost source of funds, protecting margins.

Favorable. The B2B2C model results in a very low direct Customer Acquisition Cost (CAC), as partners bear much of the marketing expense. Lifetime Value (LTV) is driven by long-term credit usage and the potential for cross-selling.

High, due to the low-cost funding model and scalable partner-based acquisition strategy.

Optimization Recommendations

- •

Develop data-driven products to sell to enterprise partners (e.g., consumer spending insights, market trend analysis) to create new, non-interest revenue streams.

- •

Optimize credit line management and pricing using AI to maximize interest income while managing risk.

- •

Focus on cross-selling direct banking products to the existing 71.5M cardholder base to increase LTV.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Technology Stack

Impact:Medium

Solution Approach:While Synchrony has invested heavily in modernizing its tech stack since its IPO , continued migration to cloud-native architecture and microservices is needed to enable faster product development and easier partner integrations.

- Limitation:

Data Silos

Impact:Medium

Solution Approach:Implement a unified data platform to consolidate customer data across all partner cards and banking products to enable a true 360-degree customer view for personalization and risk management.

Operational Bottlenecks

- Bottleneck:

Partner Onboarding Process

Growth Impact:Slows down the rate at which new revenue streams can be activated.

Resolution Strategy:Develop a self-service partner portal and standardized API library to streamline the technical and operational integration for new partners.

- Bottleneck:

Credit Risk Management in Economic Downturns

Growth Impact:Could lead to significant increases in charge-offs and delinquencies, impacting profitability and forcing a pullback on lending, thus stalling growth.

Resolution Strategy:Invest further in AI/ML-based predictive models that can identify early warning signs of consumer distress and dynamically adjust credit lines or offer forbearance options.

Market Penetration Challenges

- Challenge:

Intense Competition from Fintechs (Affirm, Klarna)

Severity:Critical

Mitigation Strategy:Compete by offering a more comprehensive suite of products (cards, BNPL, banking) and leveraging deep partner relationships. Acquire or partner with fintechs to accelerate innovation, as seen with the Loop Commerce acquisition.

- Challenge:

Partner Concentration Risk

Severity:Major

Mitigation Strategy:Continue diversifying the partner portfolio into new verticals (e.g., digital, wellness) and reduce dependency on a few key mega-retailers. Grow the direct-to-consumer business to create a revenue stream independent of partners.

- Challenge:

Increasing Regulatory Hurdles for Consumer Credit

Severity:Major

Mitigation Strategy:Proactively invest in compliance technology and talent. Design products with transparency and consumer protection as core features. Actively participate in industry discussions to help shape future regulation.

Resource Limitations

Talent Gaps

- •

Product managers with experience in agile, consumer-facing fintech.

- •

AI/ML engineers for advanced underwriting and personalization models.

- •

Cybersecurity experts to protect a vast and complex financial ecosystem.

Moderate. While profitable, scaling lending requires a substantial capital base. The digital bank deposit-taking is a key strategic asset that mitigates the need for constant external funding.

Infrastructure Needs

Continued investment in cloud infrastructure to enhance scalability and reduce latency.

Advanced data analytics and AI platforms to derive actionable insights from massive datasets.

Growth Opportunities

Market Expansion

- Expansion Vector:

Small and Medium-Sized Businesses (SMBs)

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Develop a 'Synchrony-in-a-box' solution that allows SMBs (via platforms like Shopify or Adobe Commerce) to easily embed financing options, moving beyond the current focus on large enterprise partners.

- Expansion Vector:

Emerging Affluent Consumers

Potential Impact:Medium

Implementation Complexity:Medium

Recommended Approach:Launch a premium co-branded card program targeting this demographic, which is digitally savvy and values rewards. Partner with brands that appeal to this segment.

Product Opportunities

- Opportunity:

Embedded Finance & Banking-as-a-Service (BaaS)

Market Demand Evidence:The growth of embedded finance is a major trend, with non-financial companies looking to offer financial products to their customers.

Strategic Fit:High. This is a natural evolution of Synchrony's core business model, moving from offering just credit to providing a broader suite of financial tools via API to partners.

Development Recommendation:Pilot a BaaS offering with a key digital partner, providing services like branded savings accounts or payment processing in addition to credit.

- Opportunity:

Data Monetization and Insights-as-a-Service

Market Demand Evidence:Retail partners are hungry for data on consumer spending habits and trends to inform their own business strategies.

Strategic Fit:High. Leverages Synchrony's greatest asset: its vast, multi-retailer transactional data.

Development Recommendation:Develop an anonymized and aggregated data analytics platform for partners, providing insights on customer behavior, market basket analysis, and competitive benchmarking as a premium service.

Channel Diversification

- Channel:

Digital Wallets and Super Apps

Fit Assessment:Excellent

Implementation Strategy:Seek deeper integration with major digital wallets (Apple Pay, Google Pay) and explore becoming a key financing provider within emerging 'super apps' to reach consumers in their preferred digital environments.

- Channel:

Financial Influencers and Content Marketing

Fit Assessment:Good

Implementation Strategy:Develop an affiliate program for financial influencers to promote Synchrony Bank's savings products, leveraging third-party credibility to drive direct-to-consumer growth at a lower cost than traditional advertising.

Strategic Partnerships

- Partnership Type:

Fintech & Technology Integration

Potential Partners

- •

Plaid

- •

Stripe

- •

Leading AI/ML Platform providers

Expected Benefits:Accelerate digital transformation, enable seamless open banking integrations, improve data analytics capabilities, and enhance fraud detection.

- Partnership Type:

New Industry Verticals

Potential Partners

- •

Travel & hospitality aggregators

- •

Subscription-based service providers (SaaS, media)

- •

Home services platforms

Expected Benefits:Diversify revenue streams and reduce reliance on traditional retail, tapping into recurring revenue models and large-ticket service expenditures.

Growth Strategy

North Star Metric

Total Payment Volume (TPV)

TPV represents the total value of all transactions flowing through the Synchrony network. It's a holistic measure that captures both the number of active users and their engagement level, reflecting the health of both the partner and consumer sides of the business.

10-15% year-over-year growth, outpacing the general retail sales growth rate.

Growth Model

Platform/Ecosystem Growth Model

Key Drivers

- •

Number of active partners

- •

Number of active accounts per partner

- •

Average transaction value and frequency

- •

Cross-product adoption rate (e.g., cardholder opening a bank account)

Focus on a dual-loop strategy: 1) A 'Partner Acquisition Loop' to continuously add new merchants to the platform, and 2) a 'Customer Activation & Engagement Loop' to drive usage and cross-sell new products within the existing customer base.

Prioritized Initiatives

- Initiative:

Develop and launch an 'Embedded Finance' API platform for digital partners.

Expected Impact:High

Implementation Effort:High

Timeframe:18-24 months