eScore

usbank.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

U.S. Bank demonstrates a mature and formidable digital presence, marked by a highly-rated mobile app and a strong digital footprint. Its content strategy, centered around the 'Financial IQ' and resource hubs, effectively targets various customer segments. The bank shows sophistication in leveraging digital channels for geographic penetration and has a healthy mix of branded and non-branded organic traffic, indicating solid search intent alignment. While strong, there is an opportunity to deepen its content authority on niche, high-value topics to better compete with top-tier competitors.

A strong omnichannel presence, effectively using its wide network of over 2,000 branches to complement a robust and award-winning digital banking platform.

Amplify thought leadership by more aggressively promoting its 'World's Most Ethical Companies' status in top-of-funnel content to capture socially-conscious searchers and build a stronger brand preference earlier in the user journey.

U.S. Bank's messaging is highly effective at the product level, with clear, direct language and strong calls-to-action tailored to specific audiences like small businesses and wealth management clients. The brand successfully conveys a voice of being helpful, professional, and supportive. However, the homepage messaging is fragmented, presenting a 'catalog' of products rather than a unified, compelling brand narrative, which dilutes the overall value proposition and differentiation from competitors.

Excellent audience segmentation, skillfully adjusting tone and messaging between the accessible, action-oriented language for the mass market and the sophisticated, relationship-focused language for high-net-worth Private Wealth Management clients.

Restructure the homepage to lead with a single, powerful brand story that unifies its diverse product offerings. Subordinate the individual product promotions to create a cohesive narrative around a core value proposition, such as being the most trusted and ethical financial partner.

The website provides a clean, trustworthy, and intuitive user experience with a clear information hierarchy that reduces cognitive load. Conversion elements like 'Open an Account' CTAs are prominent and effective, and the site's mobile responsiveness is excellent. While the core experience is strong, there is a noted lack of interactive tools (like calculators) and the cookie consent banner could be optimized to reduce friction for users wishing to opt out of non-essential tracking.

A highly effective and logical information architecture, featuring a clean design and intuitive navigation that allows users to quickly find key information and complete primary tasks like logging in or exploring products.

Integrate interactive tools like retirement calculators or mortgage estimators directly onto relevant product pages to transform the user experience from passive information consumption to active engagement, providing tangible value and increasing lead generation.

U.S. Bank excels in establishing credibility through a robust legal and compliance framework and prominent trust signals. The site's meticulous adherence to financial regulations, including conspicuous FDIC disclosures and a comprehensive privacy center for GLBA and CCPA, is a cornerstone of its market position. This is further bolstered by the repeated use of third-party validations, such as being named one of the 'World’s Most Ethical Companies' for over a decade.

Exceptional use of third-party validation, particularly the 'World's Most Ethical Companies' and 'World's Most Admired Companies' awards, which are powerful differentiators that build substantial customer trust across all segments.

Elevate the placement of key trust signals and accolades. While present, they are sometimes located low on the page; moving them higher, especially on key landing pages, would more immediately bolster credibility and could improve conversion rates.

U.S. Bank's competitive advantage is rooted in its highly diversified business model, which creates resilient earnings across consumer banking, payments, and wealth management. This, combined with a strong brand reputation for trust and an effective omnichannel presence, creates a sustainable moat. While it faces a scale disadvantage against the 'Big Four' banks, its strong position in payment services (Elavon) and its focused digital transformation efforts provide a solid defense and path for growth.

A highly diversified business model with significant non-interest income from its Payment Services division, providing stability and resilience against interest rate fluctuations that heavily impact competitors.

Accelerate the pace of innovation to close the gap with the largest competitors. This includes not just building new features but strategically acquiring or partnering with fintechs to quickly integrate cutting-edge technology and maintain a competitive digital experience.

As the 5th largest U.S. bank, U.S. Bank has a proven, scalable model and is actively pursuing expansion, evidenced by the acquisition of MUFG Union Bank to bolster its West Coast presence. The bank is investing heavily in technology and AI to drive operational efficiency and has a clear strategy for growth in high-potential areas like small business banking and wealth management for the mass affluent. Opportunities to develop new revenue streams like Banking-as-a-Service (BaaS) further enhance its expansion potential.

A disciplined strategy of growth through both major acquisitions (like MUFG Union Bank) and organic expansion into new markets and digital products, supported by a strong capital base.

Address legacy core banking systems by adopting a two-speed IT architecture. This would involve maintaining the stable core while building an agile, API-driven layer on top to accelerate innovation, facilitate fintech partnerships, and overcome technical scaling barriers.

U.S. Bank's business model is exceptionally coherent, with diversified revenue streams that are strategically aligned to its core identity as a full-service national bank. Key business lines such as Consumer Banking, Payment Services, and Wealth Management are distinct yet interconnected, allowing for effective cross-selling. The company demonstrates strong strategic focus by investing heavily in its digital-first transformation and pursuing an 'alliance' strategy with fintechs, showing clear alignment between resource allocation and market opportunities.

A well-balanced and diversified business model that generates significant revenue from both traditional net interest income and high-margin, non-interest fee income, particularly from its powerhouse Payment Services division.

Strengthen the connective tissue between business silos. Create a more explicit customer journey that guides clients from their first checking account toward higher-value services like wealth management, positioning the bank as a lifelong financial partner.

As the 5th largest bank by assets, U.S. Bank holds significant market power and a stable market share trajectory. Its strong brand reputation and diversified services grant it a degree of pricing power, while its leadership in specific niches like payment services provides substantial leverage. The bank's influence is demonstrated by its ability to shape customer experiences through a widely adopted digital platform and its strategic focus on being a trusted advisor, a key differentiator against both larger banks and fintechs.

Significant market influence and negotiating power derived from its leadership position in specialized areas like payment services (Elavon), corporate trust, and commercial card payments.

Double down on the 'Most Trusted Advisor' positioning to counter the scale of the 'Big Four' and the unproven trust of neobanks. This involves more prominent marketing of its ethical standing and transforming branches into centers for high-value advisory services, solidifying a unique market position.

Business Overview

Business Classification

Diversified Financial Services

Commercial Banking

Financial Services

Sub Verticals

- •

Retail Banking

- •

Corporate & Commercial Banking

- •

Wealth Management & Investment Services

- •

Payment Services

- •

Mortgage Lending

Mature

Maturity Indicators

- •

Extensive physical branch network (over 2,000 branches).

- •

Ranked as the 5th largest bank in the United States by assets.

- •

Consistent Fortune 500 company (ranked #105).

- •

Long operating history, established in 1863.

- •

Recent large-scale acquisition (MUFG Union Bank consumer business).

- •

Subject to heightened capital requirements as a systemically important bank.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Interest Income

Description:The core revenue driver for the bank, representing the difference between interest earned on assets (loans, securities) and interest paid on liabilities (deposits, borrowings). This is primarily driven by lending activities across all segments.

Estimated Importance:Primary

Customer Segment:All Segments

Estimated Margin:Medium

- Stream Name:

Payment Services Fees

Description:Revenue from retail payment solutions, merchant acquiring and processing services, and corporate payment solutions. This is a significant portion of noninterest income.

Estimated Importance:Primary

Customer Segment:Personal, Business, Corporate

Estimated Margin:High

- Stream Name:

Trust and Investment Management Fees

Description:Fees generated from wealth management, asset management, and corporate trust services. This includes fees based on assets under management (AUM) and administration.

Estimated Importance:Secondary

Customer Segment:Wealth Management, Corporate

Estimated Margin:High

- Stream Name:

Service Charges and Fees

Description:Fees from deposit accounts, credit cards, mortgage banking, treasury management, and other banking services.

Estimated Importance:Secondary

Customer Segment:Personal, Business

Estimated Margin:High

Recurring Revenue Components

- •

Net interest margin from loan portfolios

- •

Monthly/annual account maintenance fees

- •

Credit card annual fees and interest

- •

Asset-based fees from wealth and asset management

- •

Merchant processing fees (volume-based)

- •

Treasury management service subscriptions

Pricing Strategy

Fee-based and Interest Spread Model

Mid-range

Semi-transparent

Pricing Psychology

- •

Tiered pricing (e.g., account benefits based on balance)

- •

Bundling (e.g., checking and savings account promotions)

- •

Promotional pricing (e.g., introductory offers on new accounts or credit cards)

- •

Relationship-based pricing (e.g., preferred rates for wealth management clients).

Monetization Assessment

Strengths

- •

Highly diversified revenue model across multiple business lines (e.g., consumer banking, payments, wealth management), reducing reliance on any single income source.

- •

Significant noninterest income (fee revenue) which is less sensitive to interest rate fluctuations.

- •

Strong position in the lucrative payment services and credit card processing market.

- •

Growing wealth management business targeting a full spectrum of clients from mass affluent to ultra-high-net-worth.

Weaknesses

- •

Net interest income is highly sensitive to macroeconomic conditions and Federal Reserve interest rate policy.

- •

Increasing competition from fintechs and neobanks is putting pressure on traditional fee structures.

- •

Regulatory scrutiny can lead to limitations on certain fees (e.g., overdraft fees).

Opportunities

- •

Expand 'Banking as a Service' (BaaS) and embedded finance offerings through APIs to generate new fee income streams.

- •

Grow the outsourced chief investment officer (OCIO) business to capture more institutional clients.

- •

Leverage data analytics for dynamic, personalized pricing and product offers to increase wallet share.

- •

Increase recurring revenue through subscription-based family banking packages, as seen with the Greenlight partnership.

Threats

- •

Intense competition from other large national banks and agile fintech startups.

- •

Economic downturn leading to increased loan defaults and reduced lending demand.

- •

Regulatory changes that could further compress fee income.

- •

Cybersecurity threats leading to significant financial and reputational damage.

Market Positioning

A trusted, full-service national bank emphasizing digital convenience, a broad product portfolio, and ethical business practices to serve a wide range of customers from individuals to large corporations.

Major Player (Top 5 U.S. Bank by assets)

Target Segments

- Segment Name:

Personal Banking Consumers

Description:Individuals and families seeking standard banking services such as checking/savings accounts, credit cards, auto loans, and mortgages. This is a broad segment with a growing preference for digital and mobile banking.

Demographic Factors

- •

All age groups, with a growing focus on younger, digitally-native generations (Gen Z, Millennials).

- •

Varying income levels

- •

Includes specific initiatives for demographic groups like the Hispanic community.

Psychographic Factors

- •

Value convenience and ease of use

- •

Seek financial stability and security

- •

Increasingly interested in digital tools for budgeting and goal tracking

Behavioral Factors

- •

High adoption of mobile banking apps (over 80% of transactions happen online).

- •

Omnichannel usage: interacts via app, website, ATMs, and physical branches

- •

Responds to promotional offers and bundled services

Pain Points

- •

Complex fee structures

- •

Time-consuming loan application processes

- •

Lack of personalized financial guidance

- •

Difficulty managing all financial accounts in one place

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Business & Commercial Clients

Description:Small businesses, mid-market companies, and large corporations requiring services like business checking, treasury management, commercial loans, and payment processing.

Demographic Factors

Businesses of all sizes, from sole proprietorships to large enterprises

Spans various industries (e.g., manufacturing, agriculture, hospitality).

Psychographic Factors

- •

Focused on operational efficiency and cash flow management

- •

Value strong, relationship-based banking

- •

Seek scalable solutions that grow with their business

Behavioral Factors

- •

Heavy users of treasury management and payment processing services

- •

Increasingly adopting digital tools for financial operations.

- •

Often have complex borrowing and credit needs

Pain Points

- •

Slow, paper-based processes

- •

Lack of integration between banking and ERP systems

- •

Difficulty accessing capital quickly

- •

Managing cross-border payments and foreign exchange risk

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Wealth Management Clients

Description:High-net-worth (HNW) and ultra-high-net-worth (UHNW) individuals and families, as well as mass affluent clients, seeking investment management, financial planning, trusts, and private banking services.

Demographic Factors

- •

Mass Affluent: >$100k in investable assets

- •

High-Net-Worth: $1M - $25M in investable assets

- •

Ultra-High-Net-Worth (via Ascent Private Capital Management): >$25M in investable assets.

Psychographic Factors

- •

Concerned with wealth preservation and legacy planning

- •

Seek sophisticated, personalized advice and a high-touch service model.

- •

Value trust and long-term relationships with advisors

Behavioral Factors

- •

Utilize a dedicated team of specialists (Portfolio Managers, Trust Officers, etc.)

- •

Require complex solutions for investments, estates, and banking.

- •

Expect premium service and benefits, such as preferred rates.

Pain Points

- •

Navigating complex financial markets

- •

Coordinating multiple financial professionals (legal, tax, investment)

- •

Planning for intergenerational wealth transfer

- •

Managing specialty assets like private businesses or real estate.

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Diversified Business Mix

Strength:Strong

Sustainability:Sustainable

- Factor:

Advanced Digital Platform & Mobile App

Strength:Strong

Sustainability:Temporary

- Factor:

Leadership in Payment Services (Elavon)

Strength:Strong

Sustainability:Sustainable

- Factor:

Brand Reputation for Trust and Ethical Practices

Strength:Moderate

Sustainability:Sustainable

Value Proposition

For individuals, businesses, and wealthy families, U.S. Bank provides a comprehensive and integrated suite of financial services, combining the convenience of a top-tier digital banking platform with the security and personalized guidance of a trusted national institution.

Good

Key Benefits

- Benefit:

One-Stop Financial Hub

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Offers personal, business, and wealth management services under one roof

Integrated mobile app to manage banking, investing, and budgeting

- Benefit:

Digital Convenience & Innovation

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Award-winning mobile app with advanced features.

- •

End-to-end digital mortgage applications and same-day business loan approvals.

- •

Use of APIs for embedded finance and real-time payments.

- Benefit:

Trust and Security

Importance:Critical

Differentiation:Common

Proof Elements

- •

FDIC Insured

- •

Recognized as one of the World's Most Ethical Companies for 11 consecutive years

- •

Long history as a major U.S. financial institution.

Unique Selling Points

- Usp:

Integrated Alliance Strategy

Sustainability:Medium-term

Defensibility:Moderate

- Usp:

Comprehensive Digital Platform for Commercial Clients

Sustainability:Medium-term

Defensibility:Moderate

Customer Problems Solved

- Problem:

Financial Complexity and Fragmentation

Severity:Major

Solution Effectiveness:Complete

- Problem:

Inconvenient Access to Banking Services

Severity:Major

Solution Effectiveness:Complete

- Problem:

Lack of Trust in Financial Institutions

Severity:Major

Solution Effectiveness:Partial

Value Alignment Assessment

High

The value proposition strongly aligns with the market's shift towards digital-first, omnichannel banking while still offering the comprehensive services and security expected of a large, established bank.

High

The proposition is well-tailored, with distinct offerings for personal consumers (convenience), businesses (efficiency), and wealth clients (personalized expertise), directly addressing the core needs of each segment.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Fintech Companies (e.g., Greenlight).

- •

Large Affinity Partners (e.g., Edward Jones, State Farm).

- •

Technology Providers (e.g., Adobe, various API partners).

- •

Payment Networks (Visa, Mastercard, American Express)

- •

Correspondent Banks

Key Activities

- •

Digital Product Development & Innovation.

- •

Loan Origination & Servicing

- •

Deposit Gathering & Management

- •

Payment Processing & Network Management

- •

Wealth & Asset Management.

- •

Risk Management & Regulatory Compliance

Key Resources

- •

Capital Base & Balance Sheet.

- •

Brand Reputation & Customer Trust

- •

Proprietary Digital Banking Platform.

- •

Physical Branch & ATM Network

- •

Skilled Workforce (Bankers, Advisors, Technologists)

- •

Customer Data & Analytics Capabilities.

Cost Structure

- •

Employee Compensation & Benefits

- •

Interest Expense on Deposits & Borrowings

- •

Technology & Infrastructure Costs

- •

Marketing & Customer Acquisition

- •

Physical Branch Operations & Maintenance

- •

Provision for Credit Losses

Swot Analysis

Strengths

- •

Diversified business model provides stable, resilient earnings.

- •

Strong market position as the 5th largest U.S. bank.

- •

Advanced digital capabilities and a highly-rated mobile app.

- •

Strong brand recognition and reputation for ethical practices.

- •

Efficient operations, reflected in a well-managed efficiency ratio (59.2% in Q2).

Weaknesses

- •

Vulnerability to macroeconomic cycles and interest rate changes.

- •

Lower brand recognition on the coasts compared to Midwest stronghold, though the MUFG acquisition addresses this.

- •

Potential for operational diseconomies of scale inherent in a large, complex organization.

- •

Exposed to digital security risks due to heavy reliance on online platforms.

Opportunities

- •

Deepen penetration in West Coast markets following the MUFG Union Bank acquisition.

- •

Accelerate adoption of AI and machine learning for hyper-personalization, risk management, and operational efficiency.

- •

Expand strategic alliances (like Edward Jones) to access new customer ecosystems without the cost of acquisition.

- •

Capture the growing market for ESG-focused investment products within wealth management.

- •

Further develop Banking-as-a-Service (BaaS) offerings for corporate clients.

Threats

- •

Intense competition from money-center banks (JPMorgan Chase, Bank of America), super-regionals, and agile fintechs.

- •

Evolving and potentially more stringent regulatory landscape, especially regarding capital requirements.

- •

Persistent cybersecurity threats targeting the financial sector.

- •

An economic downturn could lead to increased credit losses and reduced loan demand.

- •

Disintermediation by Big Tech companies entering financial services.

Recommendations

Priority Improvements

- Area:

Customer Experience Personalization

Recommendation:Leverage AI and the unified data platform (Adobe Experience Platform) to move from segmented to true one-to-one real-time personalization across all channels, including predicting customer needs and proactively offering solutions.

Expected Impact:High

- Area:

West Coast Market Integration

Recommendation:Develop and execute a targeted marketing and product integration plan for former Union Bank customers to maximize cross-sell opportunities and prevent attrition, focusing on wealth management and payment services.

Expected Impact:High

- Area:

Operational Efficiency

Recommendation:Implement generative AI and robotic process automation (RPA) in back-office functions (e.g., compliance, loan processing, call centers) to further reduce the efficiency ratio and free up human capital for value-added tasks.

Expected Impact:Medium

Business Model Innovation

- •

Launch a 'Platform Banking' ecosystem model, where U.S. Bank provides the core regulated infrastructure (deposits, payments, lending) for a curated marketplace of third-party fintech apps and services, generating revenue via API access fees and revenue sharing.

- •

Develop a subscription-based 'Family Financial Wellness' bundle that combines the Greenlight partnership for kids with financial planning tools, identity theft protection, and premium banking benefits for parents, creating a new recurring revenue stream.

- •

Create a dedicated 'Digital Commercial Bank' vertical that is entirely API-driven, targeting tech startups and digital-native businesses with embedded finance solutions (e.g., embedded payments, automated lending, treasury APIs).

Revenue Diversification

- •

Expand the data and analytics-as-a-service offering, providing anonymized transaction data insights to corporate and commercial clients for a subscription fee.

- •

Build out the OCIO (Outsourced Chief Investment Officer) practice to serve more mid-sized institutions (endowments, foundations) that are looking to outsource their investment management.

- •

Develop and monetize a proprietary ESG scoring and analytics platform for wealth and asset management clients, capitalizing on the growing demand for sustainable investing.

U.S. Bancorp operates a robust and highly diversified business model, positioning it as a formidable competitor in the North American financial services industry. Its maturity is a core strength, providing a stable capital base, a trusted brand, and a vast customer network. The business model's foundation rests on the dual pillars of net interest income from its extensive lending operations and a significant, growing stream of noninterest (fee) income, particularly from its powerhouse Payment Services division. This diversification provides resilience against interest rate volatility and economic cycles.

Strategically, U.S. Bank is navigating the industry's digital transformation effectively. Rather than viewing fintech as a pure threat, it has adopted an 'alliance' strategy, partnering with firms like Edward Jones and Greenlight to embed its products into external ecosystems, thereby expanding its reach efficiently. Internally, the heavy investment in a proprietary, award-winning digital platform and the use of sophisticated data analytics tools demonstrate a commitment to owning the customer experience and driving operational efficiency. The recent acquisition of MUFG Union Bank is a pivotal strategic move, addressing a geographic weakness on the West Coast and providing significant synergy and cross-selling opportunities.

The primary opportunity for business model evolution lies in shifting from an integrated bank to a true 'platform' bank. By further opening its infrastructure via APIs, U.S. Bank can become the central hub for a network of specialized financial services, generating new, high-margin revenue. The key challenges will be managing the increasing complexity of a large organization, fending off more agile digital-native competitors, navigating a stringent regulatory environment, and continuing to innovate at pace. Future success will be determined by its ability to fully leverage its data assets for hyper-personalization, successfully integrate its strategic acquisitions, and maintain its disciplined approach to risk and expense management.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

Regulatory Compliance & Capital Requirements

Impact:High

- Barrier:

Brand Trust and Reputation

Impact:High

- Barrier:

Economies of Scale

Impact:High

- Barrier:

Technological Infrastructure

Impact:Medium

Industry Trends

- Trend:

Digital Transformation and AI Integration

Impact On Business:U.S. Bank must continuously invest in its digital platforms (mobile app, online banking, AI assistants) to meet customer expectations and compete with both large banks and nimble fintechs.

Timeline:Immediate

- Trend:

Competition from Neobanks and Fintech

Impact On Business:Digital-first competitors are capturing market share, especially among younger demographics, by offering lower fees and superior user experiences, pressuring U.S. Bank's fee income and customer acquisition.

Timeline:Immediate

- Trend:

Focus on ESG (Environmental, Social, and Governance)

Impact On Business:Increasing consumer and regulatory demand for sustainable and ethical banking practices requires U.S. Bank to demonstrate and market its ESG initiatives to maintain its 'most trusted' brand image.

Timeline:Near-term

- Trend:

Personalization and Customer Experience

Impact On Business:Generic banking products are becoming obsolete. U.S. Bank needs to leverage data analytics to offer personalized advice, products, and services to enhance customer loyalty and share-of-wallet.

Timeline:Immediate

Direct Competitors

- →

JPMorgan Chase & Co.

Market Share Estimate:Largest U.S. bank by assets, consistently a market leader.

Target Audience Overlap:High

Competitive Positioning:Positions itself as a financial titan with a full spectrum of services, from retail to investment banking, emphasizing scale, profitability, and a strong brand.

Strengths

- •

Unmatched scale and profitability, allowing for massive reinvestment.

- •

Dominant position in the credit card market.

- •

Strong brand identity and consumer trust built over a long history.

- •

Advanced digital and technological capabilities.

Weaknesses

Due to its size, may be slower to adapt than smaller, more agile competitors.

Faces intense regulatory scrutiny as a systemically important financial institution.

Differentiators

- •

Largest branch network in the U.S.

- •

Leader in investment banking, which provides a halo effect for its other divisions.

- •

Highly profitable and diversified business model.

- →

Bank of America

Market Share Estimate:One of the 'Big Four' U.S. banks, with a massive retail customer base.

Target Audience Overlap:High

Competitive Positioning:Focuses on a 'high-tech, high-touch' approach, heavily investing in its digital platforms and AI assistant (Erica) while maintaining a significant physical presence.

Strengths

- •

Leading digital banking platform with high user engagement and record-breaking digital interactions.

- •

Strong wealth management division (Merrill).

- •

Extensive network of branches and ATMs.

- •

Successful AI integration (Erica) for personalized customer service.

Weaknesses

Customer satisfaction scores can lag behind top performers.

Perceived as a large, impersonal institution by some consumer segments.

Differentiators

- •

Industry-leading AI-powered virtual assistant, Erica.

- •

Strong integration of banking, investing, and wealth management services.

- •

Focus on digital innovation, such as the digital debit card.

- →

Wells Fargo

Market Share Estimate:One of the 'Big Four' U.S. banks, particularly strong in retail and commercial banking.

Target Audience Overlap:High

Competitive Positioning:Leverages its extensive branch network and history, while working to rebuild trust and modernize its technology after past scandals.

Strengths

- •

One of the largest branch networks in the U.S., providing wide accessibility.

- •

Strong brand recognition and a large, established customer base.

- •

Diversified financial services portfolio.

Weaknesses

- •

Significant reputational damage from past scandals impacts customer trust.

- •

Faces ongoing regulatory scrutiny and growth restrictions.

- •

Perceived as having outdated technology systems compared to competitors.

Differentiators

Deep roots in community banking with a strong physical presence across the country.

Leading provider of mortgages in the U.S.

- →

Citigroup

Market Share Estimate:One of the 'Big Four' U.S. banks with a significant global footprint.

Target Audience Overlap:Medium

Competitive Positioning:Positions as a global bank with a strong focus on institutional clients and credit cards, while offering a full range of consumer banking services.

Strengths

- •

Extensive global presence and expertise in international markets.

- •

Strong credit card business (Citi-branded and retail partnerships).

- •

Well-regarded institutional clients group (investment banking, corporate banking).

Weaknesses

- •

Less extensive U.S. retail branch network compared to the other 'Big Four'.

- •

Has undergone significant restructuring, which can create operational challenges.

- •

Customer satisfaction has seen notable declines in some studies.

Differentiators

Global network and expertise in cross-border banking.

Strong focus on wealth management for high-net-worth clients.

- →

PNC Financial Services

Market Share Estimate:Major super-regional bank, one of the largest in the U.S. by assets and branches.

Target Audience Overlap:Medium

Competitive Positioning:A scaled regional leader with a strong presence in its core markets, focusing on a diversified business model and investing in both digital capabilities and physical branch expansion.

Strengths

- •

Strong regional presence and market share in key states.

- •

Diversified portfolio across retail, corporate, and asset management.

- •

Commitment to investing in technology and digital platforms.

Weaknesses

Brand recognition is not as strong nationally as the 'Big Four'.

Performance is closely tied to the economic health of its primary regions.

Differentiators

Strategic expansion of its physical branch network to gain deposit share.

Acquisition-driven growth strategy (e.g., BBVA USA).

Indirect Competitors

- →

Chime

Description:A leading U.S. neobank offering fee-free checking and savings accounts, early direct deposit, and a credit-builder product, all through a mobile-first platform.

Threat Level:High

Potential For Direct Competition:Increasingly becoming a primary banking choice for a significant portion of the population, directly competing for deposits and daily transactions.

- →

SoFi

Description:A digital personal finance company offering a suite of financial products including student loan refinancing, mortgages, personal loans, credit cards, investing, and banking through SoFi Bank.

Threat Level:Medium

Potential For Direct Competition:High. Already operates with a national bank charter and is aggressively cross-selling its broad product portfolio to create an all-in-one digital financial solution.

- →

PayPal / Venmo

Description:Global leaders in digital payments and peer-to-peer (P2P) transfers. They are expanding into other financial services like savings accounts, crypto, and credit products.

Threat Level:High

Potential For Direct Competition:High. They are leveraging their massive user bases and payment ecosystems to offer more traditional banking services, bypassing the need for a primary bank account for many transactions.

- →

Apple (Apple Card / Apple Pay / Apple Savings)

Description:Big Tech giant offering deeply integrated financial products within its ecosystem, including a credit card (with Goldman Sachs), a P2P payment service, and a high-yield savings account.

Threat Level:Medium

Potential For Direct Competition:High. Apple's seamless user experience and massive, loyal customer base give it a powerful platform to expand further into banking, posing a significant long-term threat.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Diversified Business Model

Sustainability Assessment:Highly sustainable. Revenue streams from retail, business, wealth management, and payments create resilience against economic cycles affecting a single sector.

Competitor Replication Difficulty:Hard

- Advantage:

Established Brand Trust and Reputation

Sustainability Assessment:Sustainable, but requires constant reinforcement. U.S. Bank's emphasis on being 'the most trusted choice,' backed by accolades, is a key differentiator against fintechs and scandal-plagued larger banks.

Competitor Replication Difficulty:Hard

- Advantage:

Omnichannel Presence

Sustainability Assessment:Sustainable. The combination of a strong physical branch network for high-value interactions and a robust digital platform for everyday banking is a powerful advantage that digital-only competitors cannot match.

Competitor Replication Difficulty:Hard

Temporary Advantages

{'advantage': 'Specific Promotional Offers (e.g., $1,000 for new business accounts)', 'estimated_duration': 'Short-term (3-6 months per campaign)'}

Disadvantages

- Disadvantage:

Scale Disadvantage vs. 'Big Four'

Impact:Major

Addressability:Difficult

- Disadvantage:

Pace of Innovation

Impact:Major

Addressability:Moderately

- Disadvantage:

Lower National Brand Recognition

Impact:Minor

Addressability:Moderately

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted marketing campaigns highlighting specific, user-friendly features of the U.S. Bank mobile app that rival or exceed fintech offerings.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Optimize the digital account opening process to be completed in under 5 minutes, reducing friction and abandonment rates.

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Invest heavily in data analytics and AI to deliver hyper-personalized financial insights and product recommendations within the mobile app.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Develop and market specialized banking solutions for underserved, high-growth niches like gig economy workers or specific small business verticals.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Modernize the role of physical branches to focus on complex advisory services (mortgage, investment, small business) and financial wellness education, fully integrated with digital channels.

Expected Impact:Medium

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Explore strategic acquisitions of fintech companies to quickly integrate innovative technology and user bases in key growth areas (e.g., automated savings, investing).

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Build out a 'Banking-as-a-Service' (BaaS) platform to partner with non-financial companies, embedding U.S. Bank's services into third-party ecosystems.

Expected Impact:High

Implementation Difficulty:Difficult

Double down on the 'Most Trusted Advisor' positioning. This uniquely positions U.S. Bank between the impersonal scale of the 'Big Four' and the unproven trust of neobanks. Emphasize the combination of ethical practices, human expertise available in branches, and powerful digital tools as a holistic value proposition.

Differentiate through a superior, integrated 'human + digital' customer experience. Every digital interaction should be seamless and intelligent, while every in-person interaction should be high-value and advisory-focused. The key is making the transition between digital and human channels effortless for the customer.

Whitespace Opportunities

- Opportunity:

Integrated Family Financial Planning Tools

Competitive Gap:Most banking apps focus on individual budgeting. There is a gap for a platform that allows families to collaboratively manage finances, set shared goals (e.g., vacation, college fund), and teach financial literacy to children.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Small Business 'CFO in an App'

Competitive Gap:Small businesses are often underserved, needing more than just a checking account. An integrated solution offering invoicing, payroll, cash flow forecasting, and seamless access to credit lines would be highly valuable and sticky.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Subscription and Recurring Payment Management Hub

Competitive Gap:While some apps help track subscriptions, no major bank has fully integrated a service to easily manage, pause, or cancel recurring payments directly from their banking app, which is a common consumer pain point.

Feasibility:High

Potential Impact:Medium

Competitive Landscape Overview

U.S. Bank operates within the mature and highly concentrated U.S. banking industry, which functions as an oligopoly dominated by the 'Big Four' (JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup). As a leading super-regional bank, U.S. Bank holds a strong position but faces intense, multi-front competition. Barriers to entry, such as immense capital requirements and complex regulatory hurdles, are exceptionally high for new traditional banks, but have been lowered for focused fintech startups attacking specific revenue pools.

Key industry trends are forcing rapid evolution: the non-negotiable shift to digital-first banking, the rise of Artificial Intelligence for personalization and efficiency, intense competition from agile neobanks and fintechs, and growing consumer demand for ESG-conscious financial partners.

Direct Competitor Assessment

U.S. Bank's primary competition comes from the 'Big Four,' all of whom possess significantly greater scale and resources.

- JPMorgan Chase competes on its sheer size, profitability, and brand strength.

- Bank of America is a formidable digital competitor, having successfully integrated its AI assistant 'Erica' and achieving massive digital engagement.

- Wells Fargo competes with a vast branch network but is still recovering from reputational damage.

- Citigroup leverages its global footprint, particularly in credit cards and institutional services.

U.S. Bank's positioning as 'the most trusted choice' is a strategic counter to the scandals of Wells Fargo and the impersonal nature of the other giants. Compared to super-regional peers like PNC, U.S. Bank competes on a relatively even footing, with both leveraging strong regional presence and investing in omnichannel strategies.

Indirect & Disruptive Threats

The most significant threat comes from indirect and disruptive competitors who are unbundling traditional banking services.

- Neobanks like Chime are rapidly gaining market share by offering superior mobile experiences and low-fee structures, directly threatening U.S. Bank's ability to attract younger customers and grow its deposit base.

- Fintech platforms like PayPal and Square are building comprehensive ecosystems around payments, increasingly encroaching on small business banking.

- Big Tech, particularly Apple with its tightly integrated financial products, represents a substantial long-term threat due to its massive user base and brand loyalty.

U.S. Bank's Competitive Position & Path Forward

U.S. Bank's key sustainable advantage is its omnichannel model: a trusted brand with a significant physical footprint combined with a modern digital banking platform. This allows it to serve a broader demographic than digital-only players while offering a more personal touch than the 'Big Four.'

However, its primary disadvantage is a scale and innovation speed gap relative to the largest competitors. Bank of America and JPMorgan Chase can outspend U.S. Bank on technology and marketing, making it critical for U.S. Bank to be a 'fast follower' and an intelligent innovator.

Strategic imperatives must focus on leveraging its unique position. The recommended path is to double down on the 'trusted advisor' role, differentiated through a superior, integrated 'human + digital' experience. This involves making the mobile app a hub for personalized financial wellness and transforming branches into centers for high-value advice. To capture growth, U.S. Bank should aggressively pursue whitespace opportunities in underserved markets, such as integrated tools for family finance and comprehensive digital solutions for small businesses. Strategic fintech acquisitions could accelerate this roadmap. By avoiding a direct scale-based competition with the 'Big Four' and focusing on trust and a seamless omnichannel experience, U.S. Bank can carve out a defensible and profitable niche in the evolving financial landscape.

Messaging

Message Architecture

Key Messages

- Message:

Make your money work as hard as you do.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero (Personal Banking)

- Message:

Banking smarter is easier than ever.

Prominence:Secondary

Clarity Score:High

Location:Homepage Mid-section

- Message:

Let’s make your dream of homeownership a reality — together.

Prominence:Secondary

Clarity Score:High

Location:Homepage (U.S. Bank Home Mortgage)

- Message:

Support for your life and legacy

Prominence:Primary

Clarity Score:High

Location:Private Wealth Management Page

- Message:

Open a new account and earn up to $1,000.

Prominence:Secondary

Clarity Score:High

Location:Homepage (Business banking)

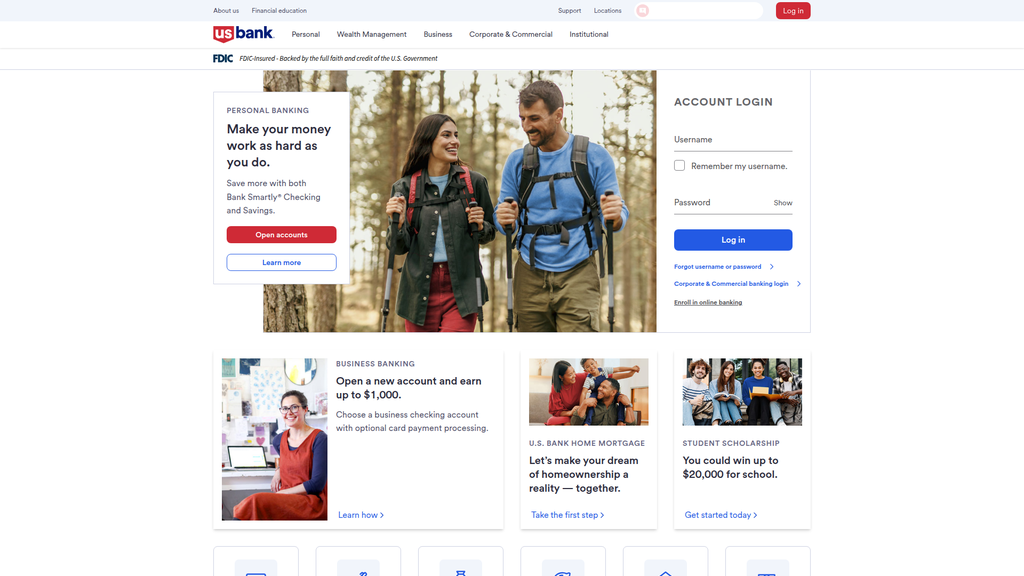

The homepage presents a fragmented message hierarchy. While the primary message for personal banking is clear, it immediately competes with multiple, equally weighted product promotions for business, mortgage, and scholarships. This creates a 'catalog' effect rather than a singular, powerful brand message. The Private Wealth Management page has a much stronger, more focused hierarchy, with a clear primary message ('Support for your life and legacy') that effectively frames the subsequent content.

Messaging is consistent within its specific product silos (e.g., mortgage messaging is consistent, wealth management is consistent). However, there is a lack of a strong, unifying brand message that carries across all sections of the homepage. The idea of 'Banking smarter' or 'making your money work' is present but doesn't feel systematically integrated into every product message, making the overall experience feel less cohesive than it could be.

Brand Voice

Voice Attributes

- Attribute:

Helpful / Supportive

Strength:Strong

Examples

- •

Let’s make your dream of homeownership a reality — together.

- •

We’re ready to help.

- •

We’re here to support your success today...

- Attribute:

Empowering

Strength:Moderate

Examples

- •

Make your money work as hard as you do.

- •

Plan, track and achieve your goals in one place.

- •

Tap into the collective power of your finances.

- Attribute:

Professional / Experienced

Strength:Strong

Examples

- •

With more than 40 years of financial advisory experience...

- •

You’ll have a dedicated Private Wealth Advisor who’ll gather a team of experts...

- •

Recognized as one of the 2025 World’s Most Admired Companies...

- Attribute:

Direct / Action-Oriented

Strength:Strong

Examples

- •

Open accounts

- •

Take the first step

- •

Apply in minutes with just $25.

- •

Get started today

Tone Analysis

Encouraging and straightforward

Secondary Tones

Reassuring

Aspirational

Tone Shifts

The tone shifts noticeably between the general consumer homepage and the Private Wealth Management page. The homepage is broad, accessible, and action-oriented. The wealth management page adopts a more formal, sophisticated, and relationship-focused tone, using words like 'legacy,' 'vision,' and 'dedicated Private Wealth Advisor.'

Voice Consistency Rating

Good

Consistency Issues

The primary inconsistency is less about the voice itself and more about the lack of a cohesive narrative connecting the different product offerings on the homepage. The voice is consistently helpful, but it's applied to a series of disconnected offers rather than a unified customer journey.

Value Proposition Assessment

For personal banking, the core value proposition is to provide smart, easy-to-use digital tools and a wide range of products that empower customers to achieve their financial goals. For wealth management, it is to provide a dedicated, team-based approach of experienced experts to help high-net-worth clients manage and grow their wealth for their life and legacy.

Value Proposition Components

- Component:

Integrated Digital Banking (One App)

Clarity:Clear

Uniqueness:Common

- Component:

Personalized Expert Guidance

Clarity:Clear

Uniqueness:Somewhat Unique (The team-based model for wealth management is a good differentiator)

- Component:

Comprehensive Product Suite

Clarity:Clear

Uniqueness:Common

- Component:

Financial Rewards & Incentives

Clarity:Clear

Uniqueness:Common

The messaging for 'Banking smarter' and having an all-in-one app is not a strong differentiator in the current market, where competitors like Chase and Bank of America offer similar digital experiences. The key differentiation point appears in the specific product bundles, like the Bank Smartly® Checking and Savings, and in the team-based model for Private Wealth Management. However, the top-level brand message on the homepage doesn't effectively communicate a unique market position. The emphasis on being an 'ethical' and 'admired' company in the wealth management section is a good, albeit subtle, differentiator.

U.S. Bank positions itself as a major, credible, and comprehensive financial institution, on par with other superregional and national banks. Its messaging aims to be accessible and helpful for the mass market while signaling prestige and expertise for its high-net-worth segment. The strategy appears to be competing on the breadth of offerings and digital convenience, rather than a single, disruptive feature or price point. Their 'Bank Smartly' product line specifically targets the young affluent, aiming to grow with them.

Audience Messaging

Target Personas

- Persona:

General Consumer / Mass Market

Tailored Messages

- •

Make your money work as hard as you do.

- •

Save more with both Bank Smartly® Checking and Savings.

- •

Banking smarter is easier than ever.

Effectiveness:Effective

- Persona:

Aspiring Homeowner

Tailored Messages

Let’s make your dream of homeownership a reality — together.

Effectiveness:Effective

- Persona:

Small Business Owner

Tailored Messages

Open a new account and earn up to $1,000.

Effectiveness:Somewhat

- Persona:

High-Net-Worth Individual ($3M+)

Tailored Messages

- •

Support for your life and legacy

- •

You’ll have a dedicated Private Wealth Advisor who’ll gather a team of experts...

- •

We’ll work with you to design a strategy that brings your vision to life.

Effectiveness:Effective

- Persona:

Student

Tailored Messages

You could win up to $20,000 for school.

Effectiveness:Effective

Audience Pain Points Addressed

- •

Financial complexity and disorganization ('Plan, track and achieve your goals in one place.')

- •

The intimidating process of borrowing money ('Borrowing money is a big deal. We’re ready to help.')

- •

Needing help with major life events ('Getting married or divorced', 'Starting a new business', 'Nearing retirement')

- •

Worry about market changes affecting investments

Audience Aspirations Addressed

- •

Financial empowerment and control ('Tap into the collective power of your finances')

- •

Achieving the dream of homeownership

- •

Building a legacy and amplifying wealth's impact

- •

Boosting children's financial confidence

Persuasion Elements

Emotional Appeals

- Appeal Type:

Aspiration / Achievement

Effectiveness:High

Examples

- •

Let’s make your dream of homeownership a reality — together.

- •

Support for your life and legacy

- •

achieve your goals in one place.

- Appeal Type:

Security / Peace of Mind

Effectiveness:Medium

Examples

- •

We’re ready to help.

- •

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

- •

We’re here to support your success...

- Appeal Type:

Empowerment

Effectiveness:Medium

Examples

Make your money work as hard as you do.

Tap into the collective power of your finances.

Social Proof Elements

- Proof Type:

Awards and Recognition

Impact:Strong

Examples

U.S. Bank has been recognized as one of the 2025 World’s Most Admired Companies...

For the 11th consecutive year, U.S. Bank has been named one of the World’s Most Ethical Companies® by the Ethisphere Institute...

Trust Indicators

- •

FDIC Insured logo and messaging

- •

Explicit disclosure statements for investment products

- •

Mention of '40 years of financial advisory experience'

- •

Awards for being an 'Ethical' and 'Admired' company

- •

Clear contact information (phone numbers, branch locator)

Scarcity Urgency Tactics

The offer to 'earn up to $1,000' for new business checking accounts is a direct incentive that encourages timely action.

Calls To Action

Primary Ctas

- Text:

Open accounts

Location:Homepage Hero

Clarity:Clear

- Text:

Learn how

Location:Business Banking section

Clarity:Clear

- Text:

Take the first step

Location:Home Mortgage section

Clarity:Clear

- Text:

Download the app

Location:Mobile Banking section

Clarity:Clear

- Text:

Open a checking account

Location:Homepage Mid-section

Clarity:Clear

- Text:

Search

Location:Private Wealth Management Page

Clarity:Clear

The CTAs are highly effective. They are consistently clear, concise, and action-oriented. The use of verbs like 'Open,' 'Learn,' 'Take,' and 'Download' leaves no ambiguity about the expected user action. Their placement is logical, following a headline or short description of a service, which provides immediate context for the user's next step.

Messaging Gaps Analysis

Critical Gaps

A unifying brand story on the homepage. The page functions as a portal to different products but lacks a compelling narrative that ties them all together under a singular, memorable brand promise.

A clear articulation of 'why U.S. Bank' over its primary competitors (Chase, Bank of America, Wells Fargo) at the brand level. The differentiation is buried within specific products rather than being a core part of the top-level message.

Contradiction Points

No itemsUnderdeveloped Areas

The concept of 'Banking smarter' is introduced but not fully developed. The website could do more to define what 'smarter' means in tangible terms for the customer (e.g., saving time, earning more, reducing stress) and show, rather than just tell, how their tools deliver this.

The connection between everyday consumer banking and long-term wealth management is not explicitly made. There is an opportunity to message a 'lifelong financial partner' journey, guiding customers from their first checking account to wealth management.

Messaging Quality

Strengths

- •

Clarity and directness in product-level communication and CTAs.

- •

Effective audience segmentation and tonal adjustment between mass-market and high-net-worth audiences.

- •

Strong use of trust indicators, particularly the FDIC insurance and third-party awards (Ethisphere, Fortune).

- •

Good use of empowering and supportive language that addresses customer aspirations.

Weaknesses

- •

Fragmented message hierarchy on the homepage dilutes the primary brand message.

- •

Core value proposition ('smarter banking') is a common theme in the industry and lacks strong differentiation.

- •

Over-reliance on product promotions on the homepage rather than building a cohesive brand narrative.

Opportunities

- •

Develop a more robust and emotional brand story around what it means for customers to 'make their money work as hard as they do.' Use storytelling to illustrate this concept.

- •

Elevate the 'ethical' and 'admired' social proof from the wealth management section to a more prominent brand-level message to build broader trust.

- •

Create a more guided user journey on the homepage that helps users self-identify and see a clearer path, rather than just presenting a list of products.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Message Hierarchy

Recommendation:Restructure the homepage hero section to focus on a single, powerful brand message that defines the core U.S. Bank value proposition. Subordinate the individual product promotions to a secondary role, perhaps in a more visually integrated 'Products for your goals' section.

Expected Impact:High

- Area:

Value Proposition Differentiation

Recommendation:Expand on the 'Banking Smarter' concept. Create a dedicated content block that explains the three key ways U.S. Bank helps you 'Bank Smarter' (e.g., 'Smarter Savings,' 'Smarter Insights,' 'Smarter Rewards') with tangible examples.

Expected Impact:High

- Area:

Audience Journey

Recommendation:Introduce a simple, goal-oriented navigation element on the homepage (e.g., 'What are you trying to achieve today?') with options like 'Manage my daily finances,' 'Buy a home,' 'Grow my business,' 'Plan for the future' to guide users to the most relevant content.

Expected Impact:Medium

Quick Wins

- •

A/B test the primary homepage headline to see if a more benefit-oriented message (e.g., 'The smarter way to achieve your financial goals') performs better than the current one.

- •

Incorporate the 'World's Most Ethical Companies' badge more prominently on the homepage to enhance brand trust across all segments.

- •

Change the generic 'Learn more' CTA for the Bank Smartly bundle to something more benefit-driven like 'See smart benefits'.

Long Term Recommendations

- •

Develop a comprehensive content marketing strategy around customer success stories that illustrate the brand promise of 'making your money work hard.'

- •

Create a messaging framework that bridges the gap between consumer banking and wealth management, positioning U.S. Bank as a partner for the entire financial lifecycle.

- •

Invest in hyper-personalization of the website experience, so that returning customers see messaging and offers tailored to their specific financial situation and goals, reflecting the banking trend toward data-driven personalization.

U.S. Bank's digital messaging strategy is functionally strong but strategically fragmented. On a tactical level, the communication is clear, direct, and effective. Product descriptions, value propositions within silos (e.g., Private Wealth Management), and calls-to-action are well-executed, leaving little room for confusion. The brand voice is consistently helpful and professional, and it adapts well to different audience segments, from students to high-net-worth individuals.

The primary weakness lies in the overall messaging architecture, particularly on the homepage. The site acts more as a digital catalog of products than a cohesive brand experience. The core message of 'Make your money work as hard as you do' is aspirational but is quickly lost in a sea of competing offers for checking, business accounts, mortgages, and scholarships. This lack of a single, powerful, and differentiated brand narrative makes it difficult for U.S. Bank to stand out in a crowded market where competitors offer similar digital convenience and product ranges.

For market positioning, this fragmented approach positions U.S. Bank as a reliable, full-service utility rather than a strategic financial partner. The brand differentiation is weak at the top of the funnel, relying on the user to dig into specific products to find unique value. This likely impacts customer acquisition economics by increasing reliance on specific, incentive-based offers (e.g., '$1,000 for a new account') rather than a compelling brand reason-to-believe.

The Private Wealth Management section is a notable exception and serves as a model for the rest of the site. It has a clear, singular message ('Support for your life and legacy'), a sophisticated tone, strong social proof, and a well-defined value proposition. To improve overall effectiveness, U.S. Bank should work to instill this level of strategic focus across its entire digital presence, building a stronger, more unified brand story that connects its diverse offerings and clearly articulates why it is the 'smarter' choice in a competitive financial landscape.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Established as one of the largest regional banks in the United States with a comprehensive suite of financial products for personal, business, and wealthy clients.

- •

Significant market capitalization ($75.07 billion) and a large, diversified customer base across multiple segments (Consumer, Business, Wealth Management, Corporate).

- •

Consistent revenue generation, with twelve-month revenue ending June 30, 2025 at $42.328B.

- •

Strong brand recognition and accolades, including being named one of the 'World's Most Ethical Companies' and 'World's Most Admired Companies', which builds trust and attracts customers.

Improvement Areas

- •

Enhancing digital product offerings to better compete with agile fintech startups and neobanks, especially in user experience and speed.

- •

Increasing personalization of services for mass-market and small business customers to counter the tailored offerings of digital-native competitors.

- •

Improving the integration between different service lines (e.g., business banking and wealth management) for a more seamless customer experience.

Market Dynamics

Modest Growth (Expected Real GDP growth of ~2.0% in 2025).

Mature

Market Trends

- Trend:

Digital Transformation and AI Integration

Business Impact:Pressure to continuously invest in technology to enhance customer experience, improve operational efficiency, and offer AI-driven financial advice.

- Trend:

Competition from Fintech and Neobanks

Business Impact:Increased competition for deposits and specific profitable niches like payments and personal loans, requiring traditional banks to innovate faster.

- Trend:

Focus on Non-Interest (Fee) Income

Business Impact:Net interest margins are under pressure, creating a strategic imperative to grow fee-based revenue streams like wealth management, payment services, and investment banking.

- Trend:

Regulatory Scrutiny and Potential Easing

Business Impact:Ongoing compliance costs remain high, but a potentially more favorable regulatory environment could unlock M&A activity and reduce some burdens.

Favorable. While the market is mature, the current economic environment with moderating inflation and a pro-growth policy stance presents an opportunity for well-capitalized banks to gain market share through strategic investments in technology and customer-centric offerings.

Business Model Scalability

Medium

High fixed costs associated with physical branch networks, regulatory compliance, and legacy IT infrastructure. Digital offerings have lower variable costs and higher scalability.

Moderate. U.S. Bank has demonstrated positive operating leverage, with revenue growth outpacing expense growth. However, scaling the traditional, high-touch parts of the business (like Private Wealth Management) is less efficient than scaling digital platforms.

Scalability Constraints

- •

Legacy technology stacks can hinder rapid product development and integration.

- •

Regulatory compliance requirements add complexity and cost to expansion.

- •

Dependence on a physical branch network for certain services limits geographic scalability compared to digital-only banks.

- •

High competition in the banking sector can increase customer acquisition costs, impacting the economics of scaling.

Team Readiness

Experienced leadership team with a stated focus on strategic priorities like digital innovation and disciplined growth.

Traditional, siloed structure organized by business lines (e.g., Consumer Banking, Payment Services). While effective for managing a large organization, it can slow down cross-functional growth initiatives.

Key Capability Gaps

- •

Agile Product Development: Need to accelerate the shift from traditional waterfall development to more agile, customer-focused product pods.

- •

Data Science and AI Talent: Intense competition for top-tier data scientists to build out personalization engines and advanced analytics.

- •

Digital Marketing Expertise: Deeper expertise needed in performance marketing, SEO, and content strategy to compete effectively with digital-native brands.

Growth Engine

Acquisition Channels

- Channel:

Digital Marketing (Paid Search, SEO, Social Media)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Increase investment in content marketing and SEO to build organic traffic. Utilize advanced data analytics to hyper-target paid campaigns and improve conversion rates for specific products like mortgages and investment accounts.

- Channel:

Physical Branch Network

Effectiveness:High

Optimization Potential:Medium

Recommendation:Reposition branches as advisory hubs for complex financial needs (mortgages, wealth management) rather than transactional centers. Leverage foot traffic to cross-sell digital products and drive app adoption.

- Channel:

Promotional Offers & Bonuses

Effectiveness:Medium

Optimization Potential:Medium

Recommendation:Use data to create more personalized and tiered promotions that attract high-value customer segments, rather than broad, costly offers that may attract low-loyalty customers.

- Channel:

Referral Programs

Effectiveness:Low

Optimization Potential:High

Recommendation:Launch a formalized, digitally-enabled referral program that incentivizes existing customers to become brand advocates, a currently underutilized, high-trust channel.

Customer Journey

The digital onboarding process for basic accounts is streamlined ('Apply in minutes'). However, for more complex products like mortgages or wealth management, the journey likely involves multiple channels (digital, phone, in-person), which can introduce friction.

Friction Points

- •

Handoffs between digital application and in-person/phone follow-up.

- •

Complex documentation requirements for loans and investment products.

- •

Lack of a single, unified view of the customer across different bank departments.

- •

Onboarding processes that are not fully optimized for mobile devices can lead to drop-offs.

Journey Enhancement Priorities

{'area': 'Digital Onboarding', 'recommendation': 'Implement a fully digital, end-to-end onboarding process for a wider range of products, using technology to automate identity verification and document submission.'}

{'area': 'Omnichannel Experience', 'recommendation': 'Invest in a CRM and data infrastructure that provides a unified customer profile, allowing for seamless transitions between online, mobile app, and branch interactions.'}

Retention Mechanisms

- Mechanism:

Product Bundling (e.g., Bank Smartly® Checking and Savings)

Effectiveness:High

Improvement Opportunity:Create more sophisticated bundles that integrate banking with investment and insurance products, increasing switching costs.

- Mechanism:

Digital Banking App & Tools

Effectiveness:Medium

Improvement Opportunity:Enhance the app with proactive financial wellness insights, personalized budgeting tools, and integrated goal tracking to increase daily engagement and dependency.

- Mechanism:

Customer Service

Effectiveness:Medium

Improvement Opportunity:Further invest in AI-powered chatbots for instant query resolution while empowering human agents with better data to handle complex issues, creating a superior hybrid service model.

Revenue Economics

Solid. As a mature bank, U.S. Bank has a profitable business model. The key challenge is the high cost of acquiring customers in a competitive market and the pressure on net interest margins.

Undeterminable from public data, but for established banks, this is typically healthy (>5:1) due to long customer tenures and cross-selling opportunities.

Improving. The bank reported an efficiency ratio of 59.2% and has demonstrated positive operating leverage, indicating a disciplined approach to cost management relative to revenue growth.

Optimization Recommendations

- •

Increase focus on acquiring 'primary bank' customers who use multiple products, significantly increasing their lifetime value (LTV).

- •

Drive adoption of lower-cost digital channels for service and transactions to improve the overall efficiency ratio.

- •

Systematically cross-sell higher-margin products like wealth management and treasury services to the existing commercial banking client base.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Banking Systems

Impact:High

Solution Approach:Adopt a two-speed IT architecture: maintain the stable core system while building a more agile, API-driven layer on top for rapid innovation and fintech integration.

- Limitation:

Siloed Data Infrastructure

Impact:High

Solution Approach:Invest in a unified data platform (e.g., a data lakehouse) to create a single source of truth for customer data, enabling true personalization and advanced analytics.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting and Loan Processing

Growth Impact:Slows down loan origination, increases costs, and can lead to a poor customer experience.

Resolution Strategy:Implement AI and machine learning models to automate parts of the underwriting process, flagging exceptions for human review, thereby increasing speed and efficiency.

- Bottleneck:

Compliance and Regulatory Reporting

Growth Impact:Consumes significant resources and can slow down the launch of new products and services.

Resolution Strategy:Invest in RegTech (Regulatory Technology) solutions to automate compliance monitoring and reporting, reducing manual effort and risk.

Market Penetration Challenges

- Challenge:

Intense Competition from Megabanks and Super-Regionals

Severity:Critical

Mitigation Strategy:Differentiate on customer service and trust. Focus on specific niches where U.S. Bank can be a market leader, such as payment services (through its Elavon subsidiary) and specific commercial banking verticals.

- Challenge:

Customer Acquisition by Fintechs in Profitable Niches

Severity:Major

Mitigation Strategy:Develop a 'buy, build, or partner' strategy. Acquire fintechs with innovative technology, build competing products in-house, or partner with them to offer their services to the bank's customer base.

- Challenge:

Low Consumer Switching Behavior

Severity:Major

Mitigation Strategy:Target younger demographics (Gen Z, Millennials) who are more likely to switch banks and are establishing their primary financial relationships. Create a superior digital onboarding experience to capture them.

Resource Limitations

Talent Gaps

- •

AI/ML Engineers

- •

Data Scientists

- •

Digital Product Managers

- •

Cybersecurity Experts

Significant and ongoing capital required for technology modernization, potential M&A activity, and maintaining strong regulatory capital ratios.

Infrastructure Needs

- •

Cloud-native platform for developing and deploying new applications.

- •

Modern API gateway to facilitate partnerships and embedded finance opportunities.

- •

Advanced cybersecurity infrastructure to combat increasing threats.

Growth Opportunities

Market Expansion

- Expansion Vector:

Deeper Penetration within existing Geographic Footprint

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Use data analytics to identify underserved customer segments and businesses within current markets. Launch targeted marketing campaigns and product bundles to increase market share and cross-sell services.

- Expansion Vector:

Targeting Younger Demographics (Gen Z)

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Develop a digital-first banking product with features tailored to Gen Z needs (e.g., subscription management, micro-savings tools, financial literacy content). Use authentic social media marketing to build brand affinity.

Product Opportunities

- Opportunity:

Enhanced Wealth Management for the Mass Affluent

Market Demand Evidence:A growing segment of the population has investable assets but does not meet the high minimums for private wealth services.

Strategic Fit:High. Leverages existing investment management capabilities and provides a crucial step-up product for retail banking customers.

Development Recommendation:Launch a hybrid 'robo-advisor' platform that combines automated investment management with access to human financial advisors for key life moments, offered at a lower cost basis.

- Opportunity:

Banking-as-a-Service (BaaS) / Embedded Finance

Market Demand Evidence:Non-financial companies are increasingly looking to embed financial products (loans, payments, accounts) into their own customer experiences.

Strategic Fit:High. Aligns with U.S. Bank's strength in payment processing (Elavon) and its regulatory status as a chartered bank.

Development Recommendation:Develop a robust set of APIs that allow third-party companies to easily integrate U.S. Bank's financial products, creating a new B2B revenue stream.

Channel Diversification

- Channel:

Fintech Partnerships

Fit Assessment:Excellent

Implementation Strategy:Establish a dedicated corporate venture and partnership team to identify, invest in, and integrate with fintech startups that offer complementary services (e.g., automated expense management for businesses, specialized lending platforms).

- Channel:

Content & Financial Wellness Platforms

Fit Assessment:Good

Implementation Strategy:Build a comprehensive financial education hub (blog, videos, webinars, tools) to attract customers early in their financial journey. Use this platform to build trust and generate leads for banking and investment products.

Strategic Partnerships

- Partnership Type:

Embedded Banking with Large Retailers/Software Platforms

Potential Partners

- •

Major e-commerce platforms

- •

Business management software companies (e.g., ERP, accounting software)

- •

Large retail chains

Expected Benefits:Access to a large, captive customer base for offering services like point-of-sale financing, business checking accounts, and payment processing at a very low acquisition cost.

- Partnership Type:

Technology Alliance with a Major Cloud Provider

Potential Partners

- •

Amazon Web Services (AWS)

- •

Google Cloud

- •

Microsoft Azure

Expected Benefits:Accelerate cloud migration and access to advanced AI/ML tools and talent, improving innovation speed and data analytics capabilities.

Growth Strategy

North Star Metric

Primary Digital Customers

This metric focuses on high-value, digitally-engaged customers who are more likely to use multiple products, have higher retention rates, and are more profitable to serve. It aligns the entire organization around deepening relationships, not just opening single-product accounts.