eScore

visa.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

Visa possesses exceptional digital authority, reflecting its dominant global market position. The website's content strategy effectively covers the entire customer journey, from consumer-facing card benefits to in-depth B2B thought leadership on topics like AI and global commerce trends. Its global reach is manifested in localized websites and messaging that reinforces worldwide acceptance, while its strong brand recognition ensures high performance for search intent alignment.

The site's content authority is immense, backed by a globally recognized brand and comprehensive thought leadership that positions Visa as an essential source of economic and technological intelligence in the payments industry.

Develop a more formalized 'Fintech & Developer Ecosystem' content hub with open APIs, detailed case studies, and sandbox environments to better capture the next generation of financial innovators, competing more directly with platforms like Stripe.

Visa's brand messaging is a masterclass in clarity and consistency, reinforcing its core values of security, convenience, and global acceptance across all touchpoints. The website effectively segments messaging for different audiences, such as individuals and businesses, addressing their specific pain points with a reassuring and empowering tone. While the functional benefits are crystal clear, the communication lacks the strong emotional resonance of competitors like Mastercard's 'Priceless' campaign.

The brand voice is exceptionally consistent and effectively builds trust, which is the most critical currency in the financial services industry. Messages like 'security is always built in' are simple, powerful, and perfectly aligned with customer needs.

Incorporate more storytelling around card benefits and perks. Instead of just listing partners, create mini-narratives or vignettes that frame the benefits as experiences, helping to forge a stronger emotional connection with consumers.

While Visa's site doesn't have a direct 'buy now' conversion, it excels at its primary goal: guiding users to information and referring them to issuing partners. The information architecture is logical, reducing cognitive load and creating clear user flows for different audience segments. A standout strength is the proactive commitment to accessibility, with an internal 'VGAR' standard aligned with WCAG 2.2 Level AA, which broadens market reach and enhances user experience for all.

The proactive and deeply integrated approach to accessibility (VGAR standard) is a best-in-class example of inclusive design, which not only meets compliance but also serves as a strategic asset to improve usability and brand reputation.

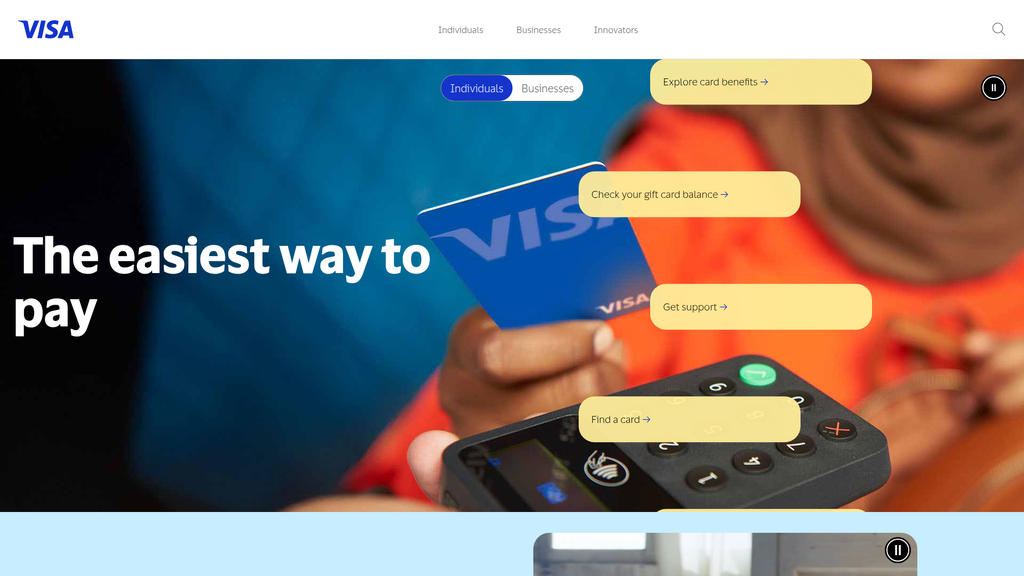

Optimize the homepage hero section's call-to-action (CTA) hierarchy. The current design presents multiple, equally weighted CTAs, which can cause decision paralysis; creating a single, visually dominant primary CTA would more effectively guide new users into the main product exploration funnel.

Visa's credibility is the bedrock of its business, and this is powerfully reflected online. The website is replete with trust signals, from explicit security messaging to a comprehensive, transparent 'Privacy Center' with region-specific policies. The company's foundational role in creating and enforcing the PCI DSS standard for the entire payments industry serves as ultimate third-party validation and risk mitigation, positioning trust not as a feature but as the core product.

The comprehensive and user-friendly 'Privacy Center' is a strategic asset that masterfully handles complex global regulations like GDPR and CCPA, demonstrating a level of transparency that builds profound trust with consumers and regulators.

Create a simplified FAQ or infographic to clarify the complex relationship between the cardholder, issuing bank, merchant, and Visa. This would enhance transparency for end-consumers who may not understand why they can't 'apply for a card' directly on the site.

Visa's competitive advantage is exceptionally strong and sustainable, anchored by one of the most powerful moats in modern business: the two-sided network effect. This effect, combined with unparalleled global brand trust and deeply entrenched infrastructure, creates nearly insurmountable barriers to entry for direct competitors. While facing threats from architectural shifts like real-time payments, its core advantages remain robust, forcing potential disruptors to partner with or build upon its rails.

The self-reinforcing two-sided network effect is the ultimate sustainable advantage; the more consumers use Visa, the more merchants must accept it, and vice-versa, creating a powerful competitive moat that is incredibly difficult and expensive to replicate.

Develop and aggressively market a 'Visa Certified' security and trust mark for partner fintechs and merchants. This would leverage Visa's core brand strength to create a competitive advantage for its ecosystem partners in a crowded fintech space.

Visa's business model is built for massive scalability, with a high fixed-cost structure (the network) that delivers immense operating leverage as transaction volumes grow at a very low marginal cost. The company has a clear and aggressive strategy for expansion beyond consumer payments into 'New Flows' like B2B and Government-to-Consumer (G2C) payments, which represent a multi-trillion dollar opportunity. Strategic acquisitions like Tink and Pismo provide the technological foundation for future growth in open banking and embedded finance.

The strategic pivot to focus on 'New Flows' (B2B, G2C, P2P) and 'Value-Added Services' is a clear and powerful signal of market expansion readiness, moving the company beyond its mature core business into vast, underserved payment markets.

Accelerate the development of a true 'Visa-as-a-Service' (VaaS) platform by consolidating APIs from recent acquisitions (Tink, Pismo) into a single, unified developer portal. This would reduce friction and speed up adoption by the fintech community, which is a key channel for future growth.

Visa's B2B2C platform model is exceptionally coherent and profitable, effectively aligning the interests of banks, merchants, and consumers. The revenue model is robust, with diversified streams from data processing, services, and international transactions. Critically, the company demonstrates strong strategic focus, evolving its model from a 'card network' to a 'network of networks' to address emerging threats from alternative payment rails and capture new opportunities.

The business model's ability to generate revenue that scales directly with payment volume and economic growth creates an incredibly efficient and profitable engine. The expansion into high-margin Value-Added Services further strengthens this core model.

More clearly articulate the value of its network and services directly to merchants. Developing merchant-focused data and analytics tools can help justify network costs and counter the narrative of high interchange fees, strengthening a key part of the ecosystem.

Visa wields immense market power, stemming from its dominant global market share and its central role in the financial ecosystem. This position grants it significant pricing power and strong leverage with financial institution partners, who have high switching costs. More importantly, Visa has the market influence to set industry standards, as evidenced by its role in establishing PCI DSS, shaping the direction and security protocols of the entire payments industry.

The ability to set and enforce industry-wide standards like PCI DSS demonstrates a level of market influence that transcends simple competition. It positions Visa as a quasi-regulatory body that underpins the security and stability of the entire digital payments ecosystem.

Proactively use its market intelligence to publish authoritative data reports, such as a quarterly 'Visa Global Commerce Report.' This would leverage its unique data assets to solidify its position as the definitive source on economic trends, creating a powerful moat against competitors.

Business Overview

Business Classification

Payment Technology Network

B2B2C Platform

Financial Services

Sub Verticals

- •

Payment Processing

- •

Fintech

- •

Data Services

Mature

Maturity Indicators

- •

Dominant global market share in card payments.

- •

Strong, consistent financial performance and revenue growth.

- •

High brand recognition and trust worldwide.

- •

Extensive and deeply integrated global network of financial institutions and merchants.

- •

Focus on incremental innovation and expansion into adjacent services rather than foundational business model changes.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Data Processing Revenues

Description:Fees charged for authorization, clearing, settlement, network access, and other transaction processing services conducted on the VisaNet network. This is Visa's largest revenue segment.

Estimated Importance:Primary

Customer Segment:Financial Institutions (Issuers & Acquirers)

Estimated Margin:High

- Stream Name:

Service Revenues

Description:Fees collected from financial institution clients for their participation in Visa card programs, based on the payments volume of Visa-branded cards and products.

Estimated Importance:Primary

Customer Segment:Financial Institutions (Issuers)

Estimated Margin:High

- Stream Name:

International Transaction Revenues

Description:Fees generated from cross-border transaction processing and currency conversion activities, which carry higher complexity and risk.

Estimated Importance:Primary

Customer Segment:Financial Institutions & Cardholders

Estimated Margin:High

- Stream Name:

Value-Added Services (VAS)

Description:A growing portfolio of over 200 services including fraud management (CyberSource, ARIC Risk Hub), data analytics, consulting, tokenization, and dispute resolution (Verifi). This is a key area for strategic growth.

Estimated Importance:Secondary

Customer Segment:Financial Institutions, Merchants, Fintechs

Estimated Margin:Medium

Recurring Revenue Components

- •

Transaction-based fees from consistent payment volumes

- •

Volume-based service fees from financial institutions

- •

Subscription/licensing fees for Value-Added Services

Pricing Strategy

Transaction-based & Volume-based Fee-for-Service

Premium

Opaque

Pricing Psychology

Network Effect Pricing: The value increases as more participants join, justifying the fees.

Value-Based Pricing: Fees are positioned as a small fraction of the value of enabling secure, global commerce.

Monetization Assessment

Strengths

- •

Highly scalable model where revenue grows with payment volume and inflation.

- •

Diversified across multiple fee types (processing, service, international).

- •

Extremely defensible due to the two-sided network effect; high barriers to entry.

- •

Growing, high-margin revenue from Value-Added Services.

Weaknesses

- •

Heavy reliance on transaction volumes, making it susceptible to global economic downturns.

- •

Complex and opaque fee structures can create tension with merchants and regulators.

- •

Primary revenue streams are concentrated in the traditional card payment ecosystem.

Opportunities

- •

Expand VAS to become a larger percentage of total revenue, reducing reliance on transaction fees.

- •

Monetize new payment flows like B2B, P2P, and Government-to-Consumer (G2C).

- •

Develop new services around data analytics, AI-driven insights, and identity verification.

- •

Integrate and monetize transactions across new payment rails like RTP and blockchain networks.

Threats

- •

Regulatory pressure on interchange and network fees globally.

- •

Competition from alternative payment networks (e.g., real-time payment systems like FedNow, ACH).

- •

Disruption from fintechs (e.g., Stripe, Adyen) and digital wallets (e.g., Apple Pay, Google Pay) that could commoditize the underlying network.

- •

Emergence of decentralized finance (DeFi) and blockchain-based payment solutions bypassing traditional rails.

Market Positioning

Market Leader and Global Standard

Dominant (Leads in global purchase volume and cards in circulation).

Target Segments

- Segment Name:

Financial Institutions (Issuers & Acquirers)

Description:Banks, credit unions, and other financial entities that issue Visa-branded cards to consumers and businesses, and those that acquire transactions from merchants. They are Visa's primary clients.

Demographic Factors

- •

Global, regional, and community banks

- •

Credit unions

- •

Neobanks and fintech issuers

Psychographic Factors

- •

Seeking trusted brand association

- •

Value security and reliability

- •

Desire for innovative payment products to offer customers

Behavioral Factors

- •

Long-term partnership contracts

- •

High switching costs due to deep integration

- •

Purchase value-added services to differentiate offerings

Pain Points

- •

Managing fraud and security risks

- •

High cost of technology development

- •

Competition from fintechs

- •

Navigating complex payment regulations

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Merchants

Description:Businesses of all sizes, from small retailers to multinational corporations, that accept Visa payments. They are indirect customers, typically via an acquiring bank.

Demographic Factors

Retail, eCommerce, Travel, Services

SMBs to large enterprises

Psychographic Factors

- •

Need for reliable and fast payment acceptance

- •

Desire to maximize sales and customer convenience

- •

Concerned about fraud and chargebacks

Behavioral Factors

- •

Seek to increase conversion rates

- •

Adopt new payment technologies (contactless, online)

- •

Integrate payments with business software

Pain Points

- •

High cost of acceptance (interchange fees)

- •

Complexity of payment integration

- •

Managing cross-border transactions

- •

Preventing fraud and managing disputes

Fit Assessment:Good

Segment Potential:High

- Segment Name:

Consumers (Cardholders)

Description:Individuals who use Visa-branded credit, debit, and prepaid cards for purchases. They are the end-users who drive transaction volume.

Demographic Factors

Broad consumer base across all age and income levels

Global presence

Psychographic Factors

- •

Value convenience, security, and global acceptance

- •

Seek rewards and benefits

- •

Trust established brands

Behavioral Factors

- •

Shift from cash to digital payments

- •

Increasing use of mobile and online payments

- •

Travel internationally

Pain Points

- •

Fear of fraud and identity theft

- •

Inconvenience of carrying cash

- •

Difficulty making cross-border payments

Fit Assessment:Excellent

Segment Potential:Medium

- Segment Name:

Governments & Public Sector

Description:Government entities utilizing Visa's network for disbursements (e.g., social benefits, tax refunds) and payment collections. A strategic growth segment.

Demographic Factors

- •

National, state, and local government agencies

- •

Public transit authorities

- •

Central banks

Psychographic Factors

- •

Prioritize efficiency, transparency, and security

- •

Goal of reducing cash handling and associated costs

- •

Aim for financial inclusion

Behavioral Factors

Digitizing tax collection and benefit disbursement

Implementing open-loop transit payment systems

Pain Points

- •

Inefficiency of check and cash-based systems

- •

Fraud in social benefit programs

- •

Lack of financial infrastructure to reach all citizens

Fit Assessment:Good

Segment Potential:High

Market Differentiation

- Factor:

Two-Sided Network Effect

Strength:Strong

Sustainability:Sustainable

- Factor:

Global Acceptance & Brand Trust

Strength:Strong

Sustainability:Sustainable

- Factor:

VisaNet Processing Infrastructure

Strength:Strong

Sustainability:Sustainable

- Factor:

Deeply Entrenched Relationships with Financial Institutions

Strength:Strong

Sustainability:Sustainable

Value Proposition

To provide the most innovative, convenient, reliable, and secure payments network, enabling seamless and trusted commerce for everyone, everywhere.

Excellent

Key Benefits

- Benefit:

Global Acceptance

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Accepted in over 200 countries and territories.

Vast network of merchants and ATMs worldwide.

- Benefit:

Security and Fraud Protection

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

- •

Multi-layered security infrastructure (VisaNet).

- •

Advanced technologies like tokenization and AI-powered fraud detection.

- •

Zero Liability Policy for consumers.

- Benefit:

Convenience and Speed

Importance:Critical

Differentiation:Common

Proof Elements

- •

Contactless 'Tap to Pay' technology.

- •

Fast transaction processing (capable of 65,000+ transactions per second).

- •

Facilitates seamless online and in-app purchases.

Unique Selling Points

- Usp:

The unparalleled scale and reach of its two-sided network, creating a powerful economic moat that is difficult for competitors to replicate.

Sustainability:Long-term

Defensibility:Strong

- Usp:

Decades of accumulated brand trust among consumers, merchants, and financial institutions globally.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

The friction, risk, and inefficiency of cash and check transactions.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

The lack of a universally trusted and accepted method for remote and cross-border commerce.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

The high cost and complexity for financial institutions to build and maintain a global payment network.

Severity:Critical

Solution Effectiveness:Complete

Value Alignment Assessment

High

Visa's core value proposition of secure, convenient digital payments is perfectly aligned with the global macro trend of shifting away from cash towards digital commerce.

High

Visa effectively serves the distinct needs of its multiple target segments: providing reliability and product innovation for banks, sales opportunities for merchants, and secure convenience for consumers.

Strategic Assessment

Business Model Canvas

Key Partners

- •

Financial Institutions (Issuing & Acquiring Banks).

- •

Merchants and Merchant Acquirers.

- •

Payment Technology Providers (Stripe, PayPal, Adyen).

- •

Fintechs and Digital Wallet Platforms (Apple Pay, Google Pay).

- •

Governments and Public Sector entities.

Key Activities

- •

Operating and securing the VisaNet payment network.

- •

Processing transactions (authorization, clearing, settlement).

- •

Product and technology innovation (e.g., contactless, tokenization).

- •

Fraud detection and risk management.

- •

Managing relationships with financial institution partners.

Key Resources

- •

VisaNet global processing network

- •

The Visa brand and reputation

- •

Vast transactional data assets

- •

Partnerships with thousands of financial institutions

- •

Technological expertise and patents

Cost Structure

- •

Personnel expenses

- •

Marketing and advertising to maintain brand presence

- •

Technology and infrastructure maintenance and development.

- •

Client incentives paid to financial institutions to drive volume.

- •

General and administrative expenses

Swot Analysis

Strengths

- •

Dominant market share and powerful global brand.

- •

Immense economic moat due to the two-sided network effect.

- •

Highly profitable and scalable business model.

- •

Advanced technology infrastructure with high processing capacity and security.

- •

Extensive data assets that can be leveraged for value-added services.

Weaknesses

- •

Dependence on financial institutions as intermediaries to reach end customers.

- •

Vulnerability to cybersecurity threats targeting its network.

- •

Perception as a legacy player compared to agile fintech startups.

- •

Complex fee structure is a point of contention for merchants and regulators.

Opportunities

- •

Expansion of Value-Added Services (data analytics, fraud prevention, consulting).

- •

Growth in new payment flows (B2B, G2C, P2P) beyond traditional consumer payments.

- •

Strategic partnerships with fintechs to drive innovation and access new markets.

- •

Leveraging blockchain and stablecoins to enhance cross-border payments and B2B settlements.

- •

Growth in emerging markets with increasing digital payment adoption.

Threats

- •

Intensifying competition from other networks (Mastercard), digital wallets, and fintech platforms (PayPal, Stripe).

- •

Global regulatory scrutiny over interchange fees, competition, and data privacy.

- •

Technological disruption from alternative payment rails (RTP, FedNow) and decentralized finance (DeFi).

- •

Global economic slowdowns reducing consumer and business spending.

- •

Geopolitical instability impacting cross-border transaction volumes.

Recommendations

Priority Improvements

- Area:

Ecosystem Collaboration

Recommendation:Accelerate and simplify the integration process for fintechs and developers via open APIs and sandbox environments. Position Visa as the foundational layer for fintech innovation, not just a card network.

Expected Impact:High

- Area:

Value Proposition for Merchants

Recommendation:Develop and clearly articulate the value of VAS directly to merchants, focusing on how Visa's data and tools can help them reduce fraud, increase conversion, and gain customer insights, thereby better justifying network costs.

Expected Impact:Medium

- Area:

Cross-Border B2B Payments

Recommendation:Aggressively invest in and market Visa's blockchain and stablecoin-based settlement solutions to capture a larger share of the lucrative cross-border B2B payments market, focusing on speed and cost reduction.

Expected Impact:High

Business Model Innovation

- •

Transition from a 'Card Network' to a 'Network of Networks': Act as an interoperability layer connecting various payment systems (card rails, RTP, ACH, blockchain networks) to allow seamless value transfer regardless of the underlying rail.

- •

Develop 'Visa as a Service' (VaaS): Offer a modular platform where clients (banks, fintechs, merchants) can subscribe to specific capabilities like tokenization, fraud scoring, data analytics, or loyalty program management as standalone services.

- •

Data Monetization Platform: Create a sophisticated, privacy-compliant data analytics platform that provides merchants and financial institutions with actionable insights on consumer spending trends, market analysis, and predictive modeling.

Revenue Diversification

- •

Scale Value-Added Services to represent a significantly larger portion of total revenue, focusing on recurring subscription-based models.

- •

Build a robust Digital Identity-as-a-Service offering, leveraging Visa's trusted position to verify identities for high-value online transactions, reducing fraud for the entire digital economy.

- •

Expand into payment orchestration services for large merchants, helping them intelligently route transactions across different payment methods and acquirers to optimize costs and success rates.

Visa's business model is a masterclass in building a defensible, highly profitable platform through the power of the two-sided network effect. Its position as the global leader in payment technology is built on a foundation of unparalleled brand trust, ubiquitous acceptance, and a secure, scalable processing network. The core business operates like a toll road for global commerce, generating massive, high-margin revenue from the sheer volume of transactions it facilitates. This incumbent position provides significant financial strength and stability. However, the future of payments is diverging from a monolithic card-based system to a multi-rail ecosystem. The primary strategic challenge for Visa is not incremental competition from Mastercard, but the systemic threat of disintermediation from new payment technologies like real-time payments, open banking (A2A payments), and decentralized finance. Visa's evolution from a 'card company' to a 'payment technology company' is well underway, with strategic investments in value-added services, fintech partnerships, and blockchain initiatives. The critical path forward requires an acceleration of this transformation. The company must fully embrace its role as a 'network of networks,' leveraging its trust and scale to provide the interoperability, security, and data intelligence layers that connect disparate payment systems. Future growth and sustained market leadership will depend less on defending the card rails and more on aggressively capturing new flows in B2B, G2C, and cross-border payments, while simultaneously embedding its value-added services across the entire digital commerce landscape. The strategic imperative is to evolve from being the primary road for payments to becoming the indispensable air traffic control system for all forms of value movement.

Competitors

Competitive Landscape

Mature

Oligopoly

Barriers To Entry

- Barrier:

Two-Sided Network Effect

Impact:High

- Barrier:

Regulatory Compliance and Licensing

Impact:High

- Barrier:

Brand Recognition and Trust

Impact:High

- Barrier:

Capital Investment in Infrastructure

Impact:High

- Barrier:

Established Relationships with Financial Institutions

Impact:High

Industry Trends

- Trend:

Rise of Real-Time Payments (RTP)

Impact On Business:Potential to bypass card networks for certain A2A (account-to-account) transactions, especially in B2B. Visa must position itself as a value-added layer (e.g., security, data) on top of these new rails or risk disintermediation.

Timeline:Immediate

- Trend:

Growth of Buy Now, Pay Later (BNPL)

Impact On Business:BNPL services compete directly with credit cards for point-of-sale financing, particularly among younger demographics. This could erode credit card transaction volumes over time.

Timeline:Immediate

- Trend:

Digital Wallet and 'Super App' Proliferation

Impact On Business:While wallets like Apple Pay often use Visa's rails, they control the user interface and customer relationship, potentially reducing Visa's brand visibility and influence. 'Super Apps' could create closed-loop payment ecosystems.

Timeline:Near-term

- Trend:

AI and Machine Learning in Fraud Prevention

Impact On Business:An opportunity for Visa to differentiate on security and offer advanced fraud detection services. It's also a competitive necessity as fraud becomes more sophisticated.

Timeline:Immediate

- Trend:

Blockchain, Stablecoins, and CBDCs

Impact On Business:A long-term architectural threat to the traditional four-party model, but also an opportunity. Visa is actively building capabilities to support these new forms of digital currency, aiming to be the bridge between Web3 and traditional finance.

Timeline:Long-term

Direct Competitors

- →

Mastercard

Market Share Estimate:Second largest global payment network after Visa.

Target Audience Overlap:High

Competitive Positioning:Positions itself as a technology company in the global payments industry, focusing on innovation, brand sponsorships (e.g., major sporting events), and expanding into emerging markets.

Strengths

- •

Strong global brand recognition and acceptance.

- •

Aggressive marketing and high-profile sponsorships.

- •

Diversified revenue streams and investment in value-added services like cybersecurity and data analytics.

- •

Strong focus on innovation, including blockchain and digital identity.

Weaknesses

- •

Slightly smaller network reach and transaction volume compared to Visa.

- •

Operates on a similar four-party model, facing the same disintermediation threats as Visa.

- •

High dependence on transaction fees from financial institutions.

Differentiators

- •

"Priceless" marketing campaign and emphasis on experiences.

- •

Strong push into B2B payments and open banking.

- •

Often seen as slightly more agile or innovative in launching new tech initiatives.

- →

American Express (Amex)

Market Share Estimate:Smaller than Visa/Mastercard in transaction volume but significant in high-value transactions.

Target Audience Overlap:Medium

Competitive Positioning:Premium brand targeting affluent individuals and corporate clients, focusing on high-value rewards, travel benefits, and superior customer service.

Strengths

- •

Closed-loop network (acts as issuer, acquirer, and network) allows for greater control, higher merchant fees, and rich data insights.

- •

Strong brand equity associated with luxury and exclusivity.

- •

Highly loyal, affluent customer base with high spending habits.

- •

Excellent rewards programs (Membership Rewards) and travel perks.

Weaknesses

- •

Lower merchant acceptance globally compared to Visa and Mastercard due to higher fees.

- •

Less appeal to budget-conscious consumers or those with lower credit scores.

- •

More sensitive to economic downturns affecting travel and luxury spending.

Differentiators

- •

Operates a closed-loop network.

- •

Focus on premium services, travel, and lifestyle benefits.

- •

Direct relationship with both cardholders and merchants.

- →

Discover Financial Services

Market Share Estimate:Fourth largest US card network.

Target Audience Overlap:Medium

Competitive Positioning:Focuses on the US market, positioning itself as a consumer-friendly brand with cashback rewards, no annual fees on many products, and strong customer service.

Strengths

- •

Strong brand recognition and customer loyalty in the US.

- •

Pioneered cashback rewards, which remains a core value proposition.

- •

Operates its own payment network, providing control and efficiency.

- •

Diversified into banking and loan products.

Weaknesses

- •

Significantly lower international acceptance compared to Visa and Mastercard.

- •

Smaller market share and transaction volume.

- •

Perceived as less prestigious than American Express.

Differentiators

- •

Emphasis on cashback rewards and customer-friendly terms (e.g., no annual fees).

- •

Primarily US-focused market strategy.

- •

Direct banking relationship with its customers.

Indirect Competitors

- →

PayPal

Description:A leading digital wallet and online payment platform that operates its own closed-loop network for PayPal-to-PayPal transactions but also uses traditional card rails for funding.

Threat Level:High

Potential For Direct Competition:High. PayPal is increasingly a 'super app' that could further disintermediate card networks by encouraging direct bank account (ACH) funding and offering its own credit products.

- →

Buy Now, Pay Later (BNPL) Providers (e.g., Klarna, Afterpay, Affirm)

Description:Offer point-of-sale installment loans, providing an alternative to credit cards for financing purchases. They are particularly popular with younger consumers and for e-commerce transactions.

Threat Level:High

Potential For Direct Competition:Medium. They directly reduce the use of credit cards for installment purchases. While some BNPL transactions are ultimately funded by Visa cards, many are not, representing lost volume.

- →

Digital Wallets (e.g., Apple Pay, Google Pay)

Description:Mobile payment services that store tokenized versions of credit and debit cards for easy, secure transactions.

Threat Level:Medium

Potential For Direct Competition:Low. Currently, they are primarily partners, making it easier to use Visa credentials. The threat lies in their control of the consumer relationship and potential to favor or develop alternative payment rails in the future.

- →

Real-Time Payment Networks (e.g., The Clearing House's RTP, FedNow)

Description:New payment rails that allow for instant, 24/7 bank-to-bank transfers.

Threat Level:Medium

Potential For Direct Competition:High. These government and bank-owned networks are designed to be a modern alternative to ACH and card payments for certain use cases (e.g., P2P, bill pay, B2B), potentially bypassing Visa's network entirely.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Two-Sided Network Effect

Sustainability Assessment:Highly sustainable. The more consumers who hold Visa cards, the more merchants must accept them, and vice versa. This creates a powerful, self-reinforcing competitive moat.

Competitor Replication Difficulty:Hard

- Advantage:

Global Brand & Trust

Sustainability Assessment:Highly sustainable. The Visa brand is globally recognized and synonymous with trust, security, and acceptance, a reputation built over decades.

Competitor Replication Difficulty:Hard

- Advantage:

Global Acceptance Infrastructure

Sustainability Assessment:Highly sustainable. The physical and digital infrastructure connecting tens of thousands of financial institutions and millions of merchants worldwide is a massive, entrenched asset.

Competitor Replication Difficulty:Hard

- Advantage:

Deep Incumbent Relationships

Sustainability Assessment:Sustainable. Long-standing partnerships with thousands of banks and financial institutions create high switching costs and collaborative inertia.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Exclusive Sponsorships (e.g., Olympics, FIFA World Cup)', 'estimated_duration': 'Duration of the sponsorship agreement (typically multi-year cycles).'}

{'advantage': 'Specific Co-Branded Card Partnerships', 'estimated_duration': 'Length of the contract with the co-brand partner (e.g., airline, hotel chain).'}

Disadvantages

- Disadvantage:

Indirect Customer Relationship

Impact:Major

Addressability:Difficult

- Disadvantage:

Perception as an Incumbent ('Legacy Tech')

Impact:Minor

Addressability:Moderately

- Disadvantage:

Regulatory Scrutiny

Impact:Major

Addressability:Difficult

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted digital marketing campaigns promoting underutilized Visa card benefits (e.g., travel insurance, concierge services) to reinforce value beyond the issuing bank's brand.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Optimize the 'Find a Card' section of the website with personalized quizzes and filters to better guide consumers to ideal partner-issued cards, capturing more affiliate traffic.

Expected Impact:Medium

Implementation Difficulty:Moderate

Medium Term Strategies

- Recommendation:

Expand Visa Direct's capabilities and marketing for P2P and B2C use cases (e.g., gig economy payouts, insurance disbursements) to directly compete with RTP networks on value-added services.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Develop a 'Visa Certified' security and trust mark for partner fintechs and merchants to display, leveraging Visa's core brand strength in security to create a competitive advantage in a crowded fintech space.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Create partnerships with BNPL providers to offer a 'Pay with Visa Installments' option, embedding Visa into the BNPL flow rather than being bypassed by it.

Expected Impact:High

Implementation Difficulty:Difficult

Long Term Strategies

- Recommendation:

Invest heavily in building out a multi-blockchain settlement network to become the de-facto, trusted intermediary for stablecoin and CBDC transactions between financial institutions and consumers.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Develop and scale value-added data analytics and AI-driven fraud prevention services that can be applied to non-card payment rails (like RTP), creating new revenue streams and ensuring relevance.

Expected Impact:High

Implementation Difficulty:Difficult

Evolve positioning from a 'card network' to the 'trusted network for digital commerce.' Emphasize Visa's role as the secure, reliable, and interoperable foundation that powers everything from cards and digital wallets to remittances and future digital currencies.

Differentiate on the basis of universal trust and security. While fintechs offer novel user experiences, Visa offers unparalleled reliability and fraud protection. This strategy contrasts Visa's established, secure ecosystem with the fragmented and sometimes riskier landscape of emerging payment solutions.

Whitespace Opportunities

- Opportunity:

Identity as a Service (IDaaS)

Competitive Gap:No single payment network has successfully established a universal digital identity solution. Visa could leverage its network and bank partnerships to create a secure, reusable digital ID for online verification, reducing fraud and friction.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Small Business Financial Operating System

Competitive Gap:Small businesses often stitch together multiple services for payments, invoicing, and expense management. Visa could partner with fintechs to bundle these services into a cohesive, Visa-centric platform for SMBs.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Cross-Border B2B Payment Network

Competitive Gap:Cross-border B2B payments remain slow and expensive. While Visa B2B Connect exists, there is a massive opportunity to simplify and accelerate these flows, competing more aggressively with SWIFT and fintechs like Wise and Ripple.

Feasibility:High

Potential Impact:High

- Opportunity:

Carbon Footprint Tracking on Transactions

Competitive Gap:Environmentally conscious consumers lack easy ways to track the carbon impact of their spending. Visa could offer an API that allows issuing banks to provide customers with carbon footprint data for each transaction, a feature that would resonate strongly with younger demographics.

Feasibility:Medium

Potential Impact:Medium

Visa operates from a position of immense strength within a mature, oligopolistic payment processing industry. Its primary competitive advantages—the vast two-sided network effect, global brand recognition synonymous with trust, and deeply integrated infrastructure—create formidable barriers to entry that are nearly impossible for new entrants to replicate. Direct competition is a stable duel with Mastercard, a battle fought on the margins of co-branding deals, marketing, and incremental technology enhancements. American Express and Discover serve more niche, though valuable, segments and do not pose an existential threat to Visa's overall dominance.

The most significant competitive threats are not from direct rivals but from architectural shifts in the payments landscape. The rise of indirect competitors like Buy Now, Pay Later (BNPL) services, real-time payment (RTP) networks, and digital wallet ecosystems like PayPal threatens to disintermediate Visa from the transaction flow. These disruptors attack Visa's core value proposition by offering alternative rails (RTP), alternative credit (BNPL), or by controlling the consumer relationship (digital wallets). While many of these services still utilize Visa's rails today, their long-term strategy is to build their own ecosystems, reducing their dependency and capturing more value.

Visa's strategic imperative is to evolve from being perceived as a 'card company' to becoming the foundational trust and technology layer for all forms of money movement. The company's proactive investments in blockchain, stablecoins, and value-added services like Visa Direct and advanced AI-based security are critical to this evolution. The key to sustaining its advantage lies in ensuring that whether a consumer pays via tap-to-pay, a BNPL installment, a QR code, or a future digital currency, the transaction is ultimately secured, cleared, and settled on Visa's network. Opportunities in data monetization, identity services, and B2B payments represent significant growth vectors outside the traditional consumer card transaction. Visa's challenge is to leverage its incumbent strengths of trust and scale to embrace and integrate new technologies, thereby co-opting potential disruptors and reinforcing its central role in the future of global commerce.

Messaging

Message Architecture

Key Messages

- Message:

Visa provides an easy, convenient way to pay.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Section ('The easiest way to pay'), Card Category Descriptions ('A simple way to pay')

- Message:

Visa is secure and protects your transactions.

Prominence:Primary

Clarity Score:High

Location:Homepage Security Section ('With Visa, security is always built in')

- Message:

Visa offers worldwide acceptance and is ideal for travel.

Prominence:Primary

Clarity Score:High

Location:Homepage Travel Section ('Wherever you’re going in the world, we’re with you')

- Message:

Using Visa comes with valuable perks, offers, and benefits.

Prominence:Secondary

Clarity Score:Medium

Location:Homepage Perks Section, Find a Card Page ('Next level benefits')

- Message:

Visa is at the forefront of payment innovation (AI, Stablecoin).

Prominence:Tertiary

Clarity Score:Medium

Location:Homepage 'What's new at Visa' Section

The message hierarchy is logical and effective for a consumer audience. It leads with the most fundamental user benefits: ease of use, security, and global acceptance. Secondary messages about 'perks' support the primary value proposition by adding tangible value. Tertiary messages about innovation are positioned lower, correctly identifying them as supporting proof points rather than core drivers for the average consumer.

Messaging is highly consistent across the analyzed pages. Core themes of convenience, security, and acceptance are repeated in the descriptions for different card types (credit, debit, prepaid), reinforcing the universal brand promise regardless of the specific product. The language and tone remain uniform, contributing to a cohesive brand experience.

Brand Voice

Voice Attributes

- Attribute:

Reassuring

Strength:Strong

Examples

- •

With Visa, security is always built in

- •

Visa protects transactions

- •

Worldwide acceptance. Advanced protection.

- Attribute:

Empowering

Strength:Strong

Examples

- •

Wherever you’re going in the world, we’re with you

- •

It’s like your bank in your pocket

- •

Resources and solutions to help your business thrive.

- Attribute:

Simple

Strength:Moderate

Examples

- •

The easiest way to pay

- •

A simple way to pay

- •

Fast, convenient & secure

- Attribute:

Authoritative

Strength:Moderate

Examples

- •

What's new at Visa

- •

How AI is transforming fraud — and what you can do

- •

Shaping a future of payments through innovation and trust

Tone Analysis

Helpful and Confident

Secondary Tones

- •

Inspirational (related to travel and experiences)

- •

Secure

- •

Forward-thinking

Tone Shifts

The tone shifts from consumer-benefit-focused on the main homepage to a more corporate, thought-leadership tone in the 'What's new at Visa' section, which links to the corporate domain.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

Visa enables individuals and businesses to pay and be paid securely, conveniently, and globally, unlocking a world of commerce and experiences.

Value Proposition Components

- Component:

Universal Acceptance

Clarity:Clear

Uniqueness:Somewhat Unique

Details:This is a core pillar of the brand, emphasized by phrases like 'Wherever you’re going in the world' and 'accepted all over'. While competitors like Mastercard also have wide acceptance, Visa's historical tagline 'Everywhere you want to be' has cemented this as a primary brand association.

- Component:

Security & Trust

Clarity:Clear

Uniqueness:Common

Details:Explicitly stated with 'security is always built in'. This is table stakes in the payments industry, but Visa communicates it as a foundational, built-in feature, which is a strong positioning.

- Component:

Convenience & Simplicity

Clarity:Clear

Uniqueness:Common

Details:Communicated through headlines like 'The easiest way to pay' and descriptions like 'Fast, convenient & secure'. This addresses a fundamental user need in any transaction.

- Component:

Added Value (Perks & Offers)

Clarity:Somewhat Clear

Uniqueness:Somewhat Unique

Details:The 'Using your Visa has perks' section showcases tangible benefits. The uniqueness comes from the specific partnerships (OpenTable, Sofar Sounds) rather than the concept of perks itself, which is common among card networks.

Visa's differentiation on its consumer-facing website is subtle and relies heavily on its established brand equity of trust and ubiquity. The messaging doesn't directly compare Visa to competitors like Mastercard or American Express. Instead, it focuses on reinforcing its own core strengths. The primary differentiator communicated is breadth of acceptance ('Worldwide acceptance'). While Mastercard's 'Priceless' campaign focuses on the emotional outcome of transactions, Visa's messaging is more functional, centered on the enablement of the transaction itself ('The easiest way to pay', 'we're with you'). This positions Visa as the reliable, default choice for payments everywhere.

The messaging positions Visa as the foundational, ubiquitous, and most reliable payment network. It's not positioned as a luxury brand (like Amex) or an experience-focused brand (like Mastercard's 'Priceless' campaign), but as the essential infrastructure for global commerce. The focus on security and simplicity reinforces its position as a safe and default choice for consumers, businesses, and issuing banks.

Audience Messaging

Target Personas

- Persona:

The Global Traveler

Tailored Messages

- •

Wherever you’re going in the world, we’re with you

- •

Worldwide acceptance.

- •

Our exchange rate calculator.

- •

You can find an ATM in more than 200 countries.

Effectiveness:Effective

- Persona:

The Security-Conscious Online Shopper

Tailored Messages

- •

With Visa, security is always built in

- •

At Visa, we are committed to making online shopping as secure, fast and convenient as purchases you make in a store.

- •

Visa protects transactions

Effectiveness:Effective

- Persona:

The Everyday Consumer

Tailored Messages

- •

The easiest way to pay

- •

Visa Debit cards. It’s like your bank in your pocket.

- •

Fast, convenient & secure

Effectiveness:Effective

- Persona:

The Small Business Owner

Tailored Messages

Open for Business

Resources and solutions to help your business thrive.

Effectiveness:Ineffective

Notes:The consumer-facing site provides only a minimal pointer to business solutions. This audience is clearly not the primary focus of this specific website, and the messaging for them is underdeveloped here.

Audience Pain Points Addressed

- •

Fear of fraud and lack of security in online payments.

- •

Concern that a payment card won't be accepted, especially when traveling.

- •

The inconvenience of carrying cash.

- •

Complexity of managing finances and making payments.

Audience Aspirations Addressed

- •

Freedom to travel and explore the world without financial friction.

- •

Access to unique experiences and perks (dining, music, travel).

- •

Desire for a simpler, more efficient life.

- •

Ambition to grow one's business (though this is minimally addressed).

Persuasion Elements

Emotional Appeals

- Appeal Type:

Peace of Mind / Security

Effectiveness:High

Examples

With Visa, security is always built in

Visa protects transactions

- Appeal Type:

Freedom / Empowerment

Effectiveness:High

Examples

Wherever you’re going in the world, we’re with you

Visa card offers and perks get you closer to your next big move

- Appeal Type:

Belonging / Exclusivity

Effectiveness:Medium

Examples

- •

Using your Visa has perks

- •

Learn more about the Visa Dining Collection

- •

Music like you’ve never experienced it before.

Social Proof Elements

- Proof Type:

Implied Popularity (Ubiquity)

Impact:Strong

Details:The messages 'Worldwide acceptance' and 'ATMs turn your card into any local currency' imply that Visa is used and accepted by millions globally, which is a powerful form of social proof.

Trust Indicators

- •

Prominent and consistent branding

- •

Explicit and repeated messaging about security

- •

Professional and clean website design

- •

Links to thought leadership and corporate news, positioning Visa as an industry leader and innovator.

Scarcity Urgency Tactics

None observed. The messaging strategy is built on long-term trust and reliability, not short-term conversion tactics.

Calls To Action

Primary Ctas

- Text:

Find a card

Location:Homepage Hero

Clarity:Clear

- Text:

Explore card benefits

Location:Homepage Hero

Clarity:Clear

- Text:

Travel with Visa

Location:Homepage Travel Section

Clarity:Clear

- Text:

Browse credit cards

Location:Find a Card Page

Clarity:Clear

- Text:

Learn more about [Perk Partner]

Location:Homepage Perks Section

Clarity:Clear

The CTAs are generally clear and action-oriented, using verbs like 'Find', 'Explore', 'Browse', and 'Learn'. They effectively guide the user journey from understanding the brand promise (on the homepage) to exploring specific products ('Find a card' page). However, they are primarily educational ('Learn more'). The site lacks transactional CTAs because Visa itself does not issue cards; this is a key part of its business model. The CTAs appropriately direct users to the next logical step in their information-gathering process.

Messaging Gaps Analysis

Critical Gaps

Clarifying Visa's Role: The site doesn't explicitly explain that Visa is a payment network, not a card issuer. A user might be confused why they can 'Find a card' but cannot 'Apply for a card' directly. This could lead to a broken user journey for less-informed consumers.

Direct Competitive Differentiation: There is no messaging that explains why a consumer should prefer a Visa card issued by their bank over a Mastercard. The brand relies on its established equity rather than direct persuasion against its main competitor.

Contradiction Points

No major contradictions were found. The messaging is highly consistent.

Underdeveloped Areas

Business Solutions Messaging: The consumer site offers only a very brief mention and link to business solutions. For a company where B2B is a significant part of its model, this audience journey is almost nonexistent from the primary consumer homepage.

Storytelling about Perks: While perks are listed, the site could do more to tell the story of the experience these perks unlock, similar to Mastercard's 'Priceless' campaign. The current presentation is a list of logos and brief taglines.

Messaging Quality

Strengths

- •

Clarity and Simplicity: The core messages of ease, security, and acceptance are communicated with extreme clarity and conciseness.

- •

Audience Focus: The messaging is laser-focused on the primary concerns and aspirations of the end consumer.

- •

Consistency: The brand voice and key messages are applied consistently across different sections and pages.

- •

Trust Building: The heavy emphasis on security and reliability effectively reinforces brand trust, which is paramount in the financial industry.

Weaknesses

- •

Overly Functional: The messaging can be very functional and transactional, lacking the emotional resonance of competitors like Mastercard.

- •

Lack of Direct Differentiation: It relies on brand ubiquity rather than making a case for why Visa is superior to other networks.

- •

Unclear Business Model: The distinction between Visa (the network) and the banks (the issuers) is not explained, which could be a point of confusion for some users.

Opportunities

- •

Incorporate more storytelling around card benefits to create a stronger emotional connection.

- •

Develop clearer pathways and introductory messaging for small business owners who land on the consumer site.

- •

Create content that subtly highlights Visa's technological innovations (e.g., speed, AI fraud detection) in a consumer-friendly way to differentiate on more than just acceptance.

- •

Add a simple infographic or explainer on 'How Visa Works' to clarify its role in the ecosystem and enhance transparency and trust.

Optimization Roadmap

Priority Improvements

- Area:

Value Proposition - Differentiation

Recommendation:Incorporate subtle messaging that hints at technological superiority. For example, alongside 'Security is built in,' add a sub-headline like 'Our AI-powered network analyzes billions of transactions to stop fraud before it happens.' This introduces a tangible differentiator without being overly technical.

Expected Impact:High

- Area:

Audience Messaging - Storytelling

Recommendation:Transform the 'Perks' section from a list of partners into a series of mini-stories or vignettes. Instead of just 'OpenTable - Grab a primetime reservation,' use 'Your Visa card unlocks doors to the city's most sought-after tables.' Frame benefits as experiences.

Expected Impact:Medium

- Area:

Messaging Gaps - Clarifying Role

Recommendation:On the 'Find a Card' page, add a brief, clear sentence at the top: 'Visa partners with leading banks and credit unions to bring you these cards. When you find one you like, we'll connect you to the issuer to apply.' This manages user expectations and clarifies the business model simply.

Expected Impact:High

Quick Wins

Add a more prominent and inviting CTA for 'Business Solutions' in the footer or header to better serve that audience.

Rephrase some functional headlines to be more benefit-oriented (e.g., change 'Visa Debit cards' to 'Your daily spending, simplified and secured with Visa Debit').

Long Term Recommendations

Develop a comprehensive content strategy around key aspirational themes (travel, dining, entrepreneurship) that shows—rather than tells—how Visa enables these pursuits, creating a stronger emotional brand connection.

Conduct a competitive messaging audit against Mastercard, Amex, and emerging fintech players to identify new opportunities for differentiation and proactively address market shifts.

The strategic messaging on visa.com is a masterclass in clarity, consistency, and building trust. The brand effectively communicates its core value proposition of security, convenience, and global acceptance to a mass-consumer audience. The message architecture is logical, prioritizing the most critical user benefits, which directly supports Visa's business objective of being the default, top-of-wallet payment choice. The brand voice is reassuring and empowering, positioning Visa as a reliable enabler of commerce and life experiences.

The primary weakness lies in its subtlety and functional focus. The messaging relies heavily on Visa's pre-existing brand equity and does little to actively differentiate against its primary competitor, Mastercard, on an emotional level. While Mastercard's 'Priceless' campaign sells the outcome of the purchase, Visa's messaging sells the seamlessness of the purchase itself. This positions Visa as a utility—albeit a world-class one—rather than an aspirational brand. Furthermore, the website could better clarify Visa's role as a network, not an issuer, to prevent potential user journey friction. To drive future growth and defend against disruption, the messaging strategy should evolve to incorporate more storytelling and tangible points of technological differentiation, moving beyond its foundational (but now table-stakes) message of universal acceptance.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Global brand recognition and acceptance in over 200 countries.

- •

Dominant market position in consumer payments, with billions of cards in circulation.

- •

High transaction volumes and consistent growth in payments volume, indicating deep market integration.

- •

Strategic shift and investment in 'New Flows' (B2B, government) and 'Value-Added Services' shows adaptation to evolving market needs beyond consumer cards.

Improvement Areas

- •

Accelerate integration and adoption of emerging payment methods like Buy Now, Pay Later (BNPL) and account-to-account (A2A) payments to preempt competitive threats.

- •

Enhance the value proposition for merchants to counter the rise of direct debit solutions and national payment schemes that bypass card rails.

- •

Deepen engagement with Gen Z consumers by providing more personalized, embedded financial experiences through bank and fintech partners.

Market Dynamics

The global digital payments market is projected to grow at a CAGR of approximately 19-21% from 2025 to 2030.

Mature

Market Trends

- Trend:

Real-Time Payments and Open Banking

Business Impact:Threatens traditional card transaction flows but creates a massive opportunity for Visa to provide value-added services (e.g., fraud prevention, tokenization) on top of these new rails through acquisitions like Tink.

- Trend:

Embedded Finance & Financial Super Apps

Business Impact:Payments are becoming invisible and integrated into non-financial platforms, requiring Visa to shift from a consumer-facing brand to an infrastructure provider (Visa-as-a-Service) enabling these experiences.

- Trend:

Rise of Alternative Payment Methods (BNPL, Digital Wallets)

Business Impact:Erodes traditional credit card interchange revenue but offers opportunities to partner with and provide network services to these new players.

- Trend:

Central Bank Digital Currencies (CBDCs)

Business Impact:Potential for significant disruption to the existing financial system, but Visa is proactively positioning itself as a key partner for governments to ensure interoperability between CBDCs and the existing payments ecosystem.

- Trend:

Increased Regulatory Scrutiny

Business Impact:Ongoing pressure on interchange fees and antitrust concerns (e.g., blocked Plaid acquisition, DOJ lawsuit) require strategic navigation and diversification of revenue streams away from transaction fees.

Excellent. While the core market is mature, the industry is at a critical inflection point of technological disruption. Visa's established trust, scale, and strategic investments into new growth areas position it perfectly to capitalize on this shift.

Business Model Scalability

High

Primarily fixed-cost model (maintaining the global VisaNet), which allows for immense operating leverage as transaction volumes increase with minimal marginal cost.

Extremely high. The network effect is the core of the business model; each new financial institution, merchant, or fintech partner added to the network increases the value for all other participants, driving revenue with low incremental cost.

Scalability Constraints

- •

Navigating fragmented and evolving regulatory landscapes across hundreds of countries.

- •

Complexity of integrating legacy infrastructure with new technologies like blockchain and real-time payment systems.

- •

Maintaining security and fraud prevention at a massive, global scale against increasingly sophisticated threats, including AI-driven fraud.

Team Readiness

Strong. The leadership team has demonstrated a clear strategic pivot towards diversification into 'New Flows' and 'Value-Added Services', supported by significant acquisitions (Tink, Pismo) and internal innovation.

Evolving. The creation of dedicated business units for Value-Added Services and a focus on Visa-as-a-Service indicates a strategic shift from a product-centric to a platform/ecosystem-oriented structure.

Key Capability Gaps

- •

Deep expertise in decentralized finance (DeFi) and web3 technologies to move beyond CBDC pilots into scalable solutions.

- •

Agile product development culture to compete with nimble fintech startups on speed-to-market for new services.

- •

Talent in data science and AI to further monetize transaction data through analytics and insights for merchant and bank partners, beyond fraud prevention.

Growth Engine

Acquisition Channels

- Channel:

B2B2C Bank Partnerships (Issuing)

Effectiveness:High

Optimization Potential:Medium

Recommendation:Equip issuing banks with more 'composable,' cloud-native processing solutions (via Pismo acquisition) and value-added services to help them compete with neobanks and retain Gen Z customers.

- Channel:

Merchant & Acquirer Partnerships (Acceptance)

Effectiveness:High

Optimization Potential:High

Recommendation:Expand value-added services for merchants, such as advanced fraud detection (ARIC™ Risk Hub), chargeback management (Verifi), and unified checkout solutions to deepen relationships beyond basic transaction acceptance.

- Channel:

Fintech & Developer Ecosystem (Visa Developer Platform)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Actively foster an 'App Store' model on the Visa Developer Platform, encouraging third parties to build businesses on Visa's rails (Visa Direct, Tokenization, Open Banking APIs) to drive network effects and new revenue streams.

Customer Journey

For consumers, the 'conversion' is a successful, frictionless transaction. For business partners, it's the integration and utilization of Visa's services.

Friction Points

- •

Cross-border transaction complexity and costs for B2B payments.

- •

Integration challenges for banks and fintechs looking to leverage Visa's advanced APIs and data services.

- •

Perceived high fees by merchants, leading them to explore alternative payment rails.

Journey Enhancement Priorities

{'area': 'B2B Cross-Border Payments', 'recommendation': 'Aggressively scale Visa B2B Connect to streamline international payments, providing direct bank-to-bank transfers with transparent fees and settlement times. '}

{'area': 'Developer Onboarding & Support', 'recommendation': 'Simplify API documentation, offer sandboxed environments, and create dedicated support channels to reduce the time-to-value for fintechs building on the Visa platform.'}

Retention Mechanisms

- Mechanism:

Network Effects

Effectiveness:High

Improvement Opportunity:Strengthen the network by becoming the interoperability layer between different payment systems (e.g., card networks, real-time-payments, CBDCs), making Visa indispensable.

- Mechanism:

Value-Added Services (VAS)

Effectiveness:High

Improvement Opportunity:Bundle VAS with core processing services to increase stickiness for bank and merchant clients. VAS revenue is growing significantly faster than core transaction revenue, indicating strong demand.

- Mechanism:

Co-Branded Loyalty Programs

Effectiveness:Medium

Improvement Opportunity:Leverage open banking data (via Tink) to enable hyper-personalized loyalty offers and financial management tools for consumers, delivered through their banking apps.

Revenue Economics

Highly efficient and profitable due to the massive scale of the network. Each incremental transaction adds revenue at a very low marginal cost.

Not directly applicable. A better framing is 'Network Participant Value,' where the focus is on maximizing the total lifetime value of transactions and services for each node (bank, merchant, fintech) in the ecosystem.

High. The company demonstrates strong and consistent revenue growth and exceptionally high profit margins.

Optimization Recommendations

- •

Accelerate the shift in revenue mix towards high-growth, high-margin Value-Added Services and 'New Flows' (B2B, P2P, G2C), which have a target growth rate of 16-18%.

- •

Develop pricing models for API access and platform services (Visa-as-a-Service) to capture value from the developer and fintech ecosystem.

- •

Offer network-agnostic services (e.g., fraud scoring for real-time payments) to generate revenue even when transactions don't run on Visa's core rails.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Infrastructure Interoperability

Impact:Medium

Solution Approach:Continue pursuing a 'network of networks' strategy, creating API-driven abstraction layers (like the Universal Payment Channel concept) to connect VisaNet with disparate systems (CBDCs, RTP networks) without requiring a full core infrastructure overhaul.

Operational Bottlenecks

- Bottleneck:

Global Regulatory Compliance

Growth Impact:Acts as a constant drag on the speed of new product rollouts and market entry, requiring significant investment in legal and compliance resources.

Resolution Strategy:Leverage regulatory expertise as a competitive advantage ('RegTech-as-a-Service'), helping partners navigate complexity and positioning Visa as a trusted infrastructure provider for cross-border compliance.

- Bottleneck:

Managing correspondent banking relationships for B2B payments

Growth Impact:Slows down B2B transactions and adds costs and opacity.

Resolution Strategy:Bypass the traditional system with the Visa B2B Connect multilateral network, enabling direct, faster, and more transparent high-value international payments.

Market Penetration Challenges

- Challenge:

Competition from National Payment Schemes

Severity:Critical

Mitigation Strategy:Instead of competing directly, partner with these schemes to provide value-added services (e.g., security, tokenization, cross-border interoperability) and position Visa as the global bridge for domestic networks.

- Challenge:

Disintermediation by 'Pay-by-Bank' and Closed-Loop Systems

Severity:Major

Mitigation Strategy:Embrace open banking through the Tink acquisition to offer compelling account-to-account payment solutions. Acquire and build best-in-class VAS that are payment-rail agnostic to ensure relevance even if card volume growth slows.

- Challenge:

Consolidation of Issuers, Acquirers, and Merchants

Severity:Major

Mitigation Strategy:Consolidation gives partners more negotiating power over fees. Counter this by deepening the value proposition with indispensable services like advanced data analytics, loyalty platforms, and security solutions that are deeply embedded in their operations.

Resource Limitations

Talent Gaps

- •

Experts in decentralized finance (DeFi) and protocol design.

- •

AI/ML engineers specialized in predictive analytics for business intelligence, not just fraud.

- •

Product managers with experience in building developer-first API platforms.

Not a constraint. The key challenge is strategic capital allocation—identifying and executing the right multi-billion dollar acquisitions (like Tink, Pismo) and internal investments to secure future growth.

Infrastructure Needs

Cloud-native platforms to deliver 'Visa-as-a-Service' solutions globally with high performance and configurability.

Enhanced data infrastructure to support AI-driven value-added services and provide richer analytics to partners.

Growth Opportunities

Market Expansion

- Expansion Vector:

B2B Payments

Potential Impact:High

Implementation Complexity:High

Recommended Approach:Aggressively scale Visa B2B Connect and Visa Commercial Pay for high-value cross-border payments and corporate virtual cards, capturing a larger share of the $200 trillion B2B payments market.

- Expansion Vector:

Government & Small Business Services ('New Flows')

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Partner with governments for Government-to-Consumer (G2C) disbursements and develop tailored payment and cash flow management solutions for small businesses, a traditionally underserved market.

- Expansion Vector:

Value-Added Services (VAS)

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Continue to build and acquire a comprehensive suite of VAS, including risk management, data analytics, loyalty, and open banking solutions, and position them as a core part of Visa's offering to all ecosystem partners.

Product Opportunities

- Opportunity:

Visa-as-a-Service (VaaS) Platform

Market Demand Evidence:The rise of embedded finance and fintechs needing to build on reliable infrastructure.

Strategic Fit:High

Development Recommendation:Package core capabilities (issuing, processing, tokenization, risk) as modular, cloud-native APIs, enabling partners to build their own financial products on top of Visa's trusted infrastructure.

- Opportunity:

CBDC and Stablecoin Interoperability Layer

Market Demand Evidence:Over 87 countries are exploring CBDCs, creating a need for a bridge to the existing financial ecosystem.

Strategic Fit:High

Development Recommendation:Develop and pilot a 'Universal Payment Channel' to facilitate seamless exchange between different CBDCs, stablecoins, and traditional currencies, positioning Visa as the central hub for future digital money movement.

- Opportunity:

Open Banking & Data Monetization

Market Demand Evidence:Acquisition of Tink for €1.8bn and growing demand for personalized financial services.

Strategic Fit:High

Development Recommendation:Leverage Tink's API connectivity to provide financial institutions with tools for data aggregation, risk analysis, and account verification, creating new revenue streams from data and insights.

Channel Diversification

- Channel:

Direct-to-Developer API Platform

Fit Assessment:Excellent

Implementation Strategy:Invest heavily in the Visa Developer Platform, creating a best-in-class developer experience with self-serve onboarding, transparent pricing, and robust support to make Visa the default choice for fintech builders.

- Channel:

Embedded Finance through Non-Financial Partners

Fit Assessment:Excellent

Implementation Strategy:Establish dedicated partnership teams to work with large retailers, tech companies, and gig economy platforms to embed Visa's payment and financing capabilities directly into their user experiences.

Strategic Partnerships

- Partnership Type:

Real-Time Payment Network Integration

Potential Partners

- •

The Clearing House (RTP)

- •

Federal Reserve (FedNow)

- •

National schemes like UPI (India) and Pix (Brazil)

Expected Benefits:Provide overlay services (fraud, tokenization) on A2A payments, ensuring Visa remains part of the transaction flow and generates service revenue even when its rails are not used.

- Partnership Type:

Central Bank and Government Collaborations

Potential Partners

Central banks of G20 nations

Government treasury departments

Expected Benefits:Co-develop CBDC pilots and digital currency infrastructure, ensuring Visa's role in the future of public money and securing contracts for G2C disbursement solutions.

- Partnership Type:

Big Tech & Digital Wallet Providers

Potential Partners

- •

Apple

- •

Google

- •

PayPal

- •

Meta

Expected Benefits:Ensure top-of-wallet presence for Visa credentials and collaborate on next-generation payment experiences (e.g., in-car payments, IoT commerce) to drive transaction volume.

Growth Strategy

North Star Metric

Total Payment Volume (TPV) from New Flows & Value-Added Services

This metric shifts focus from the mature consumer card business to the key growth vectors identified in the corporate strategy. It directly measures the success of the diversification into B2B, G2C, and service-based revenues.

Achieve 16-18% annual growth in this metric, in line with stated corporate financial frameworks.

Growth Model

Ecosystem-led Growth

Key Drivers

- •

Platform Adoption: Number of developers and fintechs actively building on Visa's APIs.

- •

Partner Success: Growth in TPV and revenue of partners utilizing Visa's infrastructure.

- •

Data Network Effects: The more transaction data processed, the smarter the value-added services (like fraud detection) become, attracting more partners.

Treat Visa's capabilities as a platform product. Invest in developer relations, create scalable partner programs, and build a marketplace for third-party services that integrate with Visa's network.

Prioritized Initiatives

- Initiative:

Launch 'Visa Infrastructure Cloud': A comprehensive Visa-as-a-Service platform

Expected Impact:High

Implementation Effort:High

Timeframe:24-36 months

First Steps:Consolidate existing API products (Visa Direct, Tink, Pismo) under a single, unified developer portal with a simplified pricing structure. Launch a marketing campaign targeting the global fintech developer community.

- Initiative:

Scale Visa B2B Connect to 150+ Countries

Expected Impact:High

Implementation Effort:Medium

Timeframe:18-24 months

First Steps:Establish a dedicated sales and integration team focused on signing up the top 100 global commercial banks. Partner with SWIFT to enhance connectivity and interoperability.

- Initiative:

Develop a 'CBDC Sandbox-as-a-Service'

Expected Impact:Medium (long-term High)

Implementation Effort:Medium

Timeframe:12-18 months

First Steps:Productize the existing CBDC pilot framework and offer it to central banks as a turnkey solution for testing digital currency concepts, solidifying Visa's role as a key government partner.

Experimentation Plan

High Leverage Tests

- Test Name:

API Pricing Models

Hypothesis:A usage-based pricing model for Visa's APIs will attract more early-stage fintechs than a fixed-fee enterprise model, leading to higher long-term network value.

- Test Name:

B2B Connect SME Pilot