eScore

mtb.comThe eScore is a comprehensive evaluation of a business's online presence and effectiveness. It analyzes multiple factors including digital presence, brand communication, conversion optimization, and competitive advantage.

M&T Bank demonstrates strong digital intelligence within its specific regional footprint, effectively aligning with local search intent for core banking products. Its multi-channel presence is solid, grounded in a significant branch network and community engagement that supports its digital efforts. However, its content authority on a national level is weaker than larger competitors, with a strategic gap in top-of-funnel educational content that could capture users earlier in their financial journey.

Excellent alignment with local and regional search intent, leveraging its community-focused brand to dominate geographically specific banking queries.

Invest in creating a robust, hyper-local financial education content hub to capture top-of-funnel search traffic and build authority beyond branded and product-specific terms.

The bank's brand communication is exceptionally effective, clearly differentiating itself from national competitors by consistently reinforcing its community-centric value proposition. Messaging is tailored effectively to small business owners and community-minded individuals, supported by powerful social proof like being a top SBA lender and quantifiable community impact data. While the core message is strong, it lacks a memorable, customer-facing tagline to fully encapsulate this identity.

Powerful and consistent use of social proof (testimonials, awards, data) to substantiate its core brand message of being a community and business-focused bank.

Develop and prominently feature a concise, memorable brand tagline on the homepage that encapsulates the unique value proposition (e.g., 'Your Community's Bank').

The website provides a clear, logically structured user journey with good mobile responsiveness and a strong commitment to accessibility. However, the conversion experience is significantly hampered by key friction points, including understated, low-contrast 'ghost button' CTAs on primary landing pages. Furthermore, analysis indicates the digital account opening process is a critical area for improvement to reduce complexity and compete with the streamlined experiences offered by fintechs.

A strong commitment to accessibility, aligning with WCAG standards, which reduces legal risk and expands the addressable market.

Redesign all primary call-to-action buttons from the current 'ghost button' style to a solid, high-contrast design to significantly improve their visibility and click-through rates.

M&T Bank establishes exceptional credibility through a robust and mature legal compliance framework, including prominent FDIC and Equal Housing Lender disclosures. Trust is further bolstered by a transparent 'Privacy & Preference Center' and a public commitment to WCAG accessibility standards. The strategic use of third-party validation, such as its consistent ranking as a top SBA lender, provides powerful, data-backed evidence of its expertise and reliability.

A centralized and transparent hub for all legal policies, combined with a detailed accessibility statement, demonstrates a mature approach to compliance that builds significant user trust.

Audit all financial product pages to ensure disclosures (e.g., APR, APY) are not only present but are presented with maximum clarity and simplicity for the average consumer to mitigate regulatory risk.

M&T's competitive moat is highly sustainable, built on a deeply entrenched community-focused banking model and an established history of brand trust that is difficult for competitors to replicate. This is further solidified by its market leadership in SBA lending, creating a strong niche. The primary weakness is a perception of slower innovation compared to fintech challengers, which could erode its advantage over time if the digital experience gap widens.

The community-focused banking model, especially for small and mid-sized businesses, creates deep customer loyalty and is a defensible moat against large national banks and digital-only competitors.

Forge strategic partnerships with fintech companies to offer specialized services (e.g., advanced budgeting tools, international payments) to accelerate innovation without having to build all capabilities in-house.

The bank has proven its ability to scale through large strategic acquisitions, most notably the recent purchase of People's United, which significantly expanded its market footprint into New England. However, its organic scalability is constrained by high fixed costs associated with its large branch network and legacy technology infrastructure. While unit economics are solid, future growth hinges more on successful post-merger integration and M&A than on rapid, digitally-native expansion.

A proven track record of executing large-scale M&A to expand its geographic footprint and asset base, demonstrating a clear path for continued inorganic growth.

Modernize the core banking infrastructure to an API-driven architecture to reduce reliance on legacy systems and accelerate future digital product development and integration.

M&T Bank's business model is highly coherent, with diversified revenue streams from both net interest income and fee-based services that are well-aligned with its core activities. Its strategic focus on community banking and SMBs is clear and consistently executed, creating a strong value proposition for its target segments. The model's primary challenge is navigating the integration of its largest-ever acquisition while simultaneously investing to fend off digital disruption.

Excellent alignment between its value proposition (community-focused, relationship-based banking) and its most profitable target segments (SMBs and high-net-worth clients via Wilmington Trust).

Accelerate the technological and cultural integration of the People's United acquisition to fully realize projected cost savings and revenue synergies, which is critical to the model's success.

As a top super-regional bank, M&T wields considerable market power within its established geographic footprint, demonstrating a stable and growing market share trajectory, particularly after its New England expansion. Its national leadership in the SBA lending niche gives it significant pricing power and influence in that specific market. However, on a broader national scale, it has less influence and brand recognition than money-center banks, limiting its power outside of its core regions.

Sustained national leadership as a top SBA lender provides significant market power and a strong reputation within the highly valuable small business banking sector.

Develop and execute a targeted 'Digital Welcome' marketing and content strategy for the new New England markets to build brand equity and solidify market share post-acquisition.

Business Overview

Business Classification

Full-Service Super-Regional Bank

Wealth Management & Institutional Services

Banking & Financial Services

Sub Verticals

- •

Retail Banking

- •

Commercial Banking

- •

Small Business Banking (SBA Lending)

- •

Mortgage Lending

- •

Wealth Management & Advisory

- •

Institutional Client Services

Mature

Maturity Indicators

- •

Founded in 1856, indicating a very long and stable operating history.

- •

Significant scale with over 1,000 branches and a large employee base of over 22,000.

- •

History of strategic acquisitions to drive growth, notably the $8.3 billion acquisition of People's United Financial.

- •

Consistent ranking as a top national SBA lender for 16 consecutive years, demonstrating sustained market leadership in a key niche.

- •

Established brand presence in core markets across the Northeast and Mid-Atlantic regions.

Enterprise

Steady

Revenue Model

Primary Revenue Streams

- Stream Name:

Net Interest Income

Description:The primary driver of revenue, generated from the spread between the interest earned on assets (such as commercial loans, mortgages, and investment securities) and the interest paid on liabilities (like customer deposits and borrowings).

Estimated Importance:Primary

Customer Segment:All lending and deposit customers

Estimated Margin:Medium

- Stream Name:

Noninterest Income (Fee-Based Revenue)

Description:A diverse and crucial secondary revenue source, comprising fees from various services including deposit account service charges, trust and wealth management fees, mortgage banking revenues, and credit card fees.

Estimated Importance:Secondary

Customer Segment:Retail, Commercial, and Wealth Management clients

Estimated Margin:High

Recurring Revenue Components

- •

Interest income from loan and securities portfolios

- •

Account maintenance and service fees

- •

Wealth management and trust advisory fees

- •

Mortgage servicing rights income

Pricing Strategy

Relationship & Risk-Based Pricing

Mid-range

Semi-transparent

Pricing Psychology

- •

Relationship-based discounts for bundled services

- •

Promotional rates for new products (e.g., mortgages, CDs)

- •

Fee waivers for maintaining minimum balances

Monetization Assessment

Strengths

- •

Diversified revenue streams between net interest income and a strong base of noninterest income.

- •

Large, low-cost deposit base provides stable funding for lending activities.

- •

Strong fee generation from specialized services like wealth management (Wilmington Trust) and top-tier SBA lending.

Weaknesses

Net Interest Margin (NIM) is susceptible to volatility from macroeconomic interest rate changes.

Fee income from mortgage banking can be cyclical and dependent on housing market conditions.

Opportunities

- •

Increase penetration of fee-based wealth management and insurance services to the newly acquired People's United customer base.

- •

Expand digital-only products with tiered subscription fees for value-added services.

- •

Grow noninterest income by further developing treasury and cash management solutions for commercial clients.

Threats

- •

Margin compression from FinTech competitors and neobanks offering low-to-no fee banking products.

- •

Regulatory pressure on certain fee categories, such as overdraft fees.

- •

Economic downturns could reduce lending demand and increase credit loss provisions, impacting net interest income.

Market Positioning

Community-Focused Super-Regional Bank

Leading Super-Regional Player

Target Segments

- Segment Name:

Small to Medium-Sized Businesses (SMBs)

Description:A core target segment, including local businesses, independent companies, and professional service firms requiring capital, treasury management, and personalized banking relationships.

Demographic Factors

Located within M&T's 12-state footprint (Maine to Virginia).

Psychographic Factors

- •

Value strong, long-term relationships with their bankers.

- •

Seek out banks that demonstrate commitment to the local community.

- •

Appreciate direct access to decision-makers and specialized advice.

Behavioral Factors

Frequently apply for SBA-backed loans for capital and expansion.

Utilize a mix of branch services for complex transactions and digital banking for daily operations.

Pain Points

- •

Feeling underserved or overlooked by large national banks.

- •

Difficulty navigating the complex process of securing business loans.

- •

Lack of integrated, efficient cash management and payroll services.

Fit Assessment:Excellent

Segment Potential:High

- Segment Name:

Mass Affluent & Personal Banking Consumers

Description:Individuals and families residing in M&T's operating regions, seeking a full suite of personal banking products from checking and savings to mortgages and credit cards.

Demographic Factors

Geographically concentrated in the Northeastern and Mid-Atlantic U.S.

Psychographic Factors

- •

Desire a blend of digital convenience and accessible in-person branch support.

- •

Prefer a trusted, established institution for major financial decisions.

- •

Are community-oriented and value a bank that invests locally.

Behavioral Factors

Utilize mobile banking for daily transactions like check deposits and transfers.

Visit branches for advisory services, problem resolution, and opening major accounts like mortgages.

Pain Points

- •

Impersonal service from larger, nationwide banking giants.

- •

Clunky or unintuitive digital banking interfaces.

- •

Finding competitive rates for mortgages and savings from a trusted provider.

Fit Assessment:Good

Segment Potential:Medium

- Segment Name:

High-Net-Worth & Institutional Clients

Description:Wealthy individuals, families, foundations, and corporate clients served by the Wilmington Trust subsidiary, requiring sophisticated wealth planning, investment management, and corporate trust services.

Demographic Factors

High concentration of assets and complex financial needs.

Psychographic Factors

- •

Prioritize trust, discretion, and fiduciary responsibility.

- •

Seek highly customized, expert-led financial strategies.

- •

Value institutional stability and a long-term advisory relationship.

Behavioral Factors

Engage in long-term financial planning, estate planning, and trust services.

Utilize institutional-grade investment management and custody services.

Pain Points

- •

Need for integrated management of complex personal and business assets.

- •

Protecting and growing wealth across generations.

- •

Navigating complex tax, legal, and philanthropic structures.

Fit Assessment:Excellent

Segment Potential:High

Market Differentiation

- Factor:

Deep Community Integration and Focus

Strength:Strong

Sustainability:Sustainable

- Factor:

Market Leadership in Small Business (SBA) Lending

Strength:Strong

Sustainability:Sustainable

- Factor:

Premier Wealth Management Brand (Wilmington Trust)

Strength:Strong

Sustainability:Sustainable

- Factor:

Significant Regional Scale and Density

Strength:Moderate

Sustainability:Sustainable

Value Proposition

M&T Bank provides the comprehensive capabilities and stability of a large financial institution, delivered through a community-focused, relationship-based model that is deeply committed to the success of individuals, businesses, and communities it serves.

Good

Key Benefits

- Benefit:

Comprehensive Product Suite

Importance:Critical

Differentiation:Somewhat unique

Proof Elements

Wide range of personal, business, and wealth products listed on website.

Integrated services from banking to investments and insurance.

- Benefit:

Small Business Expertise and Access to Capital

Importance:Critical

Differentiation:Unique

Proof Elements

Consistent Top 10 national ranking as an SBA lender.

Customer testimonials from small business owners.

- Benefit:

Community Commitment

Importance:Important

Differentiation:Unique

Proof Elements

- •

Published Community Impact Reports.

- •

Employee volunteer program (40 hours per employee).

- •

Prominent 'Multicultural Banking' initiatives.

Unique Selling Points

- Usp:

The combination of super-regional scale with a genuine, proven community banking ethos.

Sustainability:Long-term

Defensibility:Strong

- Usp:

A nationally recognized SBA lending powerhouse, making it a go-to bank for small businesses in its footprint.

Sustainability:Long-term

Defensibility:Strong

Customer Problems Solved

- Problem:

Lack of personalized banking relationships and support for SMBs at large national banks.

Severity:Critical

Solution Effectiveness:Complete

- Problem:

Need for a single, trusted provider for a wide array of personal financial needs (daily banking, mortgage, investments).

Severity:Major

Solution Effectiveness:Complete

- Problem:

Requirement for sophisticated, fiduciary-level wealth management for high-net-worth clients.

Severity:Critical

Solution Effectiveness:Complete

Value Alignment Assessment

High

The value proposition strongly aligns with the market's need for stable, relationship-focused banking, especially in the SMB segment where it excels.

High

The proposition resonates deeply with its core SMB and community-oriented individual customers who prioritize trust and local engagement over the scale of national competitors.

Strategic Assessment

Business Model Canvas

Key Partners

- •

U.S. Small Business Administration (SBA)

- •

Financial technology partners (e.g., Blend for digital mortgage).

- •

Payment networks (Visa, Mastercard)

- •

Local non-profit and community organizations

- •

Federal and state regulators (FDIC, Federal Reserve)

Key Activities

- •

Retail and Commercial Lending

- •

Deposit Gathering and Management

- •

Wealth and Asset Management (via Wilmington Trust)

- •

Risk Management and Underwriting

- •

Customer Relationship Management

- •

Digital Platform Development and Maintenance

Key Resources

- •

Extensive branch and ATM network.

- •

Large and stable customer deposit base.

- •

Brand reputation and community trust.

- •

FDIC Insurance

- •

Specialized lending expertise (SBA, Commercial Real Estate)

- •

Wilmington Trust brand and expertise.

Cost Structure

- •

Interest expense on deposits

- •

Employee compensation and benefits

- •

Technology infrastructure and digital transformation investments.

- •

Physical branch network operations and maintenance

- •

Regulatory compliance and risk management costs.

Swot Analysis

Strengths

- •

Dominant market share and brand recognition in core Northeastern and Mid-Atlantic regions.

- •

Highly diversified business model across retail, commercial, and wealth management.

- •

Strong credit culture and conservative risk management approach.

- •

Proven expertise and national leadership in the profitable SBA lending niche.

Weaknesses

- •

Geographic concentration makes the bank vulnerable to regional economic downturns.

- •

Potential for operational inefficiencies and customer disruption during the integration of the large People's United acquisition.

- •

Pace of digital innovation may lag behind more agile FinTech competitors and larger national banks.

Opportunities

- •

Successfully integrate and cross-sell to the expanded customer base from the People's United acquisition, particularly in New England.

- •

Accelerate digital transformation to enhance customer experience and improve operational efficiency.

- •

Leverage data analytics and AI to personalize offerings, improve underwriting, and optimize operations.

- •

Expand fee-based services in treasury management and capital markets for mid-size commercial clients.

Threats

- •

Intense competition from well-capitalized national banks (e.g., Bank of America, PNC) and disruptive FinTech companies.

- •

Evolving regulatory landscape, including increased capital requirements and compliance costs.

- •

Persistent cybersecurity threats targeting financial institutions.

- •

Macroeconomic uncertainty, including interest rate fluctuations and the potential for a recession impacting loan quality.

Recommendations

Priority Improvements

- Area:

Post-Acquisition Integration

Recommendation:Accelerate the cultural and technological integration of People's United to unlock projected cost savings and revenue synergies, focusing on a seamless customer experience to minimize attrition.

Expected Impact:High

- Area:

Digital Customer Experience

Recommendation:Increase investment in digital platform capabilities, focusing on creating a unified, intuitive experience across mobile and web for both retail and business clients to better compete with FinTechs and national players.

Expected Impact:High

- Area:

Data Analytics & AI

Recommendation:Establish a centralized data analytics function to leverage the combined entity's data for enhanced credit risk modeling, personalized marketing, and identifying cross-sell opportunities.

Expected Impact:Medium

Business Model Innovation

- •

Develop industry-specific 'banking-as-a-service' verticals, bundling lending, treasury management, and advisory services for key regional industries (e.g., healthcare, manufacturing).

- •

Launch a digital-first sub-brand to attract younger demographics who are less reliant on physical branches, allowing for a more cost-effective service model.

- •

Create a specialized advisory practice for business succession planning, targeting the aging ownership base of its core SMB customers.

Revenue Diversification

- •

Expand the suite of Treasury Management and international banking services to larger commercial clients.

- •

Further build out insurance brokerage services, offering a wider range of personal and commercial lines to its existing customer base.

- •

Grow the capital markets advisory business to provide services like M&A advice and private placements to middle-market companies.

M&T Bank represents a highly successful super-regional bank with a mature, well-diversified business model. Its core strengths are a deeply entrenched community banking ethos, a dominant position in its geographic footprint, and a nationally recognized expertise in the lucrative small business lending market. The acquisition of People's United Financial was a transformative move, significantly expanding its scale and geographic reach into New England. This presents the single largest opportunity and threat: a successful integration will create a formidable regional powerhouse, while a fraught integration could lead to significant customer attrition and operational disruption. The primary strategic challenge for M&T is to evolve its traditional, relationship-centric model for the digital age. While its community focus is a powerful differentiator against impersonal national giants, it faces significant threats from agile FinTechs that are setting new standards for customer experience and operational efficiency. The bank's future success hinges on its ability to successfully execute a 'dual-track' strategy: preserving its valuable community-based culture and personalized service while aggressively investing in digital transformation, data analytics, and platform modernization. By creating a seamless hybrid of physical and digital channels, M&T can leverage its scale and trust to defend its core markets and drive sustainable, profitable growth.

Competitors

Competitive Landscape

Mature

Moderately concentrated

Barriers To Entry

- Barrier:

Regulatory Compliance & Licensing

Impact:High

- Barrier:

High Capital Requirements

Impact:High

- Barrier:

Brand Trust and Customer Acquisition Cost

Impact:High

- Barrier:

Legacy Technology Integration

Impact:Medium

- Barrier:

Access to Payment Networks

Impact:High

Industry Trends

- Trend:

Digital Transformation & Mobile-First Banking

Impact On Business:Requires continuous investment in digital platforms to meet customer expectations and compete with neobanks. Failure to adapt leads to customer attrition.

Timeline:Immediate

- Trend:

Rise of Fintech and Neobanks

Impact On Business:Increased competition for specific products (e.g., personal loans, payments), forcing traditional banks to innovate, partner, or acquire to stay competitive.

Timeline:Immediate

- Trend:

Personalization through AI and Data Analytics

Impact On Business:Opportunity to deepen customer relationships and increase wallet share by offering tailored products and advice. Requires significant data infrastructure investment.

Timeline:Near-term

- Trend:

Industry Consolidation (M&A)

Impact On Business:Potential for M&A activity to increase scale and market share. Also poses a threat as competitors may merge to create stronger entities.

Timeline:Near-term

- Trend:

Evolving Regulatory Environment

Impact On Business:Changes in capital requirements and consumer protection laws can impact profitability and operational processes. A potential easing of regulations could unlock growth.

Timeline:Long-term

Direct Competitors

- →

PNC Financial Services

Market Share Estimate:One of the largest U.S. banks by assets, with significant overlap in M&T's core markets.

Target Audience Overlap:High

Competitive Positioning:Positions as a national 'main street bank' with a broad range of services for retail, business, and corporate clients. Strong focus on its 'Virtual Wallet' digital product.

Strengths

- •

Strong brand recognition and a larger national footprint.

- •

Diversified revenue streams across retail, corporate, and asset management.

- •

Robust and mature digital banking platform ('Virtual Wallet').

- •

Significant scale and resources for technological investment.

Weaknesses

- •

Higher efficiency ratio compared to some peers, indicating higher operating costs.

- •

Can be perceived as less agile than smaller regional competitors.

- •

Potential for inconsistent customer service experiences across its vast network.

Differentiators

- •

'Virtual Wallet' product suite integrates checking, savings, and budgeting tools effectively.

- •

Stronger presence in corporate and institutional banking.

- •

Acquisitive growth strategy has expanded its market reach significantly.

- →

KeyBank

Market Share Estimate:Major regional bank with assets over $180 billion and significant branch overlap in the Northeast and Midwest.

Target Audience Overlap:High

Competitive Positioning:Focuses on relationship banking for individuals and businesses, with specialized expertise in specific industries like healthcare, real estate, and public sector.

Strengths

- •

Strong focus on specific commercial industry verticals, creating deep expertise.

- •

Commitment to digital transformation and technology investment.

- •

Large ATM network through its own and Allpoint's network.

- •

Strong capital position.

Weaknesses

- •

Profitability and net interest margin can be below industry average.

- •

Customer service reviews are often mixed, with some customers reporting issues.

- •

Less geographic diversity compared to larger national banks.

Differentiators

- •

Niche expertise in targeted commercial sectors.

- •

Focus on financial wellness programs and tools for consumers.

- •

Acquisition of Laurel Road provides a strong platform for lending to healthcare professionals.

- →

Citizens Financial Group

Market Share Estimate:Prominent regional bank with a strong presence in the New England, Mid-Atlantic, and Midwest regions, directly competing with M&T.

Target Audience Overlap:High

Competitive Positioning:Positions as a convenient, customer-focused regional bank with a full suite of products and a growing national consumer digital bank.

Strengths

- •

Extensive branch and ATM network in its core geographic footprint.

- •

Strong brand recognition and long history in the Northeast.

- •

Highly rated mobile apps and a robust digital platform.

- •

Diversified product portfolio, including wealth management and business services.

Weaknesses

- •

Interest rates on deposit accounts are often uncompetitive compared to online banks.

- •

Overdraft fees are considered high.

- •

Geographically concentrated, making it vulnerable to regional economic downturns.

Differentiators

- •

Early direct deposit feature for all deposit accounts.

- •

Strong focus on student lending and refinancing.

- •

'Citizens Access' online-only bank competes for deposits nationally with higher rates.

Indirect Competitors

- →

Chime

Description:A leading neobank offering fee-free checking and savings accounts, early direct deposit, and a credit-builder product, primarily through a mobile app.

Threat Level:High

Potential For Direct Competition:High, as it continues to expand its product suite to resemble a full-service bank for its target demographic.

- →

SoFi

Description:A digital personal finance company offering student loan refinancing, mortgages, personal loans, investing, and banking services through a single platform.

Threat Level:Medium

Potential For Direct Competition:High. Already operates as a chartered bank and is aggressively cross-selling its expanding product set to a desirable, high-earning customer base.

- →

Rocket Mortgage

Description:A major online mortgage lender that has disrupted the traditional mortgage application process with a streamlined, digital-first approach.

Threat Level:High

Potential For Direct Competition:Medium. While primarily focused on mortgages, its parent company (Rocket Companies) is expanding into other financial services, which could eventually include deposit accounts.

- →

PayPal / Venmo

Description:Digital payment platforms that have expanded to offer business services, debit cards, credit cards, and crypto trading, effectively disintermediating banks from daily transactions.

Threat Level:Medium

Potential For Direct Competition:Medium. They hold consumer balances and are a primary financial interface for many users, though they are not chartered banks.

Competitive Advantage Analysis

Sustainable Advantages

- Advantage:

Community-Focused Banking Model

Sustainability Assessment:Highly sustainable. This model builds deep customer loyalty and trust, especially within the small and mid-sized business segment, which is harder for large national banks or digital-only players to replicate.

Competitor Replication Difficulty:Hard

- Advantage:

Established Brand Trust and History

Sustainability Assessment:Sustainable. Having operated profitably for decades, including through financial crises, M&T has built a reputation for stability that is a key consideration for customers with significant deposits.

Competitor Replication Difficulty:Hard

- Advantage:

Physical Branch Network

Sustainability Assessment:Moderately sustainable. While less important for digital-native customers, branches remain a key channel for complex transactions, wealth management, and small business banking, serving as a trust and service anchor.

Competitor Replication Difficulty:Medium

Temporary Advantages

{'advantage': 'Specific Promotional Rates (e.g., CDs)', 'estimated_duration': '3-12 months. Competitors can and will match aggressive rate promotions, making this a short-term customer acquisition tool rather than a long-term advantage.'}

Disadvantages

- Disadvantage:

Negative Customer Sentiment on Digital Experience

Impact:Major

Addressability:Moderately

- Disadvantage:

Perception of Slower Innovation vs. Fintech

Impact:Major

Addressability:Difficult

- Disadvantage:

Lower National Brand Recognition

Impact:Minor

Addressability:Difficult

Strategic Recommendations

Quick Wins

- Recommendation:

Launch targeted marketing campaigns highlighting specific customer success stories from their SBA lending and community programs.

Expected Impact:Medium

Implementation Difficulty:Easy

- Recommendation:

Optimize the digital account opening process to reduce friction and abandonment, benchmarked against top neobanks.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Deploy an in-app feedback tool to systematically collect and address user pain points with the mobile banking experience.

Expected Impact:Medium

Implementation Difficulty:Easy

Medium Term Strategies

- Recommendation:

Develop an integrated financial wellness platform for SMBs, bundling banking, cash flow forecasting, and payroll integration.

Expected Impact:High

Implementation Difficulty:Moderate

- Recommendation:

Invest in AI-driven personalization to provide proactive financial advice and relevant product offers through digital channels.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Forge strategic partnerships with fintech companies to offer specialized services (e.g., international payments, advanced budgeting tools) without building them in-house.

Expected Impact:Medium

Implementation Difficulty:Moderate

Long Term Strategies

- Recommendation:

Modernize the core banking infrastructure to a more agile, API-driven architecture to accelerate future product development.

Expected Impact:High

Implementation Difficulty:Difficult

- Recommendation:

Expand the Wilmington Trust wealth management brand to serve the mass affluent, creating a stronger customer lifecycle pathway.

Expected Impact:High

Implementation Difficulty:Difficult

Reinforce the position as 'The Digital Community Bank,' combining the trust and personalized service of a local bank with a seamless, modern digital experience that rivals fintech competitors.

Double down on the relationship model. Differentiate by empowering relationship managers with superior data and digital tools to provide proactive, personalized advice to both individuals and businesses, creating a 'high-tech, high-touch' experience that neither massive national banks nor purely digital players can easily match.

Whitespace Opportunities

- Opportunity:

Targeted banking solutions for specific community sectors (e.g., nonprofits, local government contractors) that align with M&T's community focus.

Competitive Gap:Large national banks often provide generic solutions, while smaller community banks may lack the sophisticated products (e.g., treasury management) these organizations need.

Feasibility:High

Potential Impact:Medium

- Opportunity:

Develop a 'Family Office' service tier for multi-generational wealth management, integrating personal banking, business banking, and Wilmington Trust services for affluent families.

Competitive Gap:Many competitors have siloed personal, business, and wealth divisions, creating a disjointed experience for high-value clients who operate across all three.

Feasibility:Medium

Potential Impact:High

- Opportunity:

Offer 'Banking-as-a-Service' (BaaS) infrastructure for local businesses or municipalities wanting to embed financial products into their own ecosystems.

Competitive Gap:Most BaaS providers are tech companies without a community banking charter or ethos. M&T can offer both the tech stack and the regulatory trust.

Feasibility:Low

Potential Impact:High

M&T Bank operates in a mature and highly competitive U.S. regional banking industry, facing a two-front war. On one side are large national competitors like PNC and scaled regional players such as KeyBank and Citizens Bank, who compete directly on product breadth, branch presence, and marketing spend. On the other side is the ever-growing threat from nimble, digital-first indirect competitors like Chime and SoFi, which are eroding market share in profitable niches and setting high customer expectations for user experience.

M&T's core sustainable advantage is its deeply entrenched, community-focused banking model. This resonates strongly with small and medium-sized businesses (SMBs), a segment where trust, local decision-making, and relationship management are paramount. This is a difficult advantage for larger, more centralized banks or faceless digital platforms to replicate. However, this strength is undermined by a significant competitive disadvantage: a digital customer experience that is perceived as lagging. Customer sentiment analysis reveals frustrations with digital functionality, which is a critical vulnerability when even traditional competitors are investing heavily in their mobile and online platforms.

Direct competitors like PNC have successfully leveraged their scale to build robust digital ecosystems (e.g., Virtual Wallet), while Citizens Bank is pursuing a dual strategy with its 'Citizens Access' online bank to compete on rates nationally. M&T is at risk of being outmaneuvered if it cannot bridge the digital gap while simultaneously leaning into its community-centric differentiator.

The strategic imperative for M&T is to fuse its traditional strength with modern execution. It must aggressively invest in its digital channels, not to simply catch up, but to create a 'high-touch, high-tech' experience. This involves empowering its local relationship managers with superior AI-driven tools to offer proactive, personalized advice. The key opportunity lies in owning the SMB relationship in a way no competitor can—by being the bank that understands the local community and provides digital tools that are as good as or better than the fintech disruptors. Failure to modernize the digital experience will render its core community advantage obsolete over time, while abandoning its community focus in a pure technology race would be a strategic error against better-capitalized national players.

Messaging

Message Architecture

Key Messages

- Message:

We provide personalized checking accounts tailored to your lifestyle.

Prominence:Primary

Clarity Score:High

Location:Homepage Hero Section

- Message:

We are deeply committed to supporting our communities and small businesses.

Prominence:Primary

Clarity Score:High

Location:Homepage Body (Testimonial, Community Impact, Volunteering Sections)

- Message:

We offer a comprehensive suite of financial products and services to help you reach your goals.

Prominence:Secondary

Clarity Score:High

Location:Homepage Body ('More Choices. More Possibilities.' Section)

- Message:

Our digital banking is simple, secure, and convenient.

Prominence:Secondary

Clarity Score:High

Location:Homepage Body (M&T Mobile Banking Section)

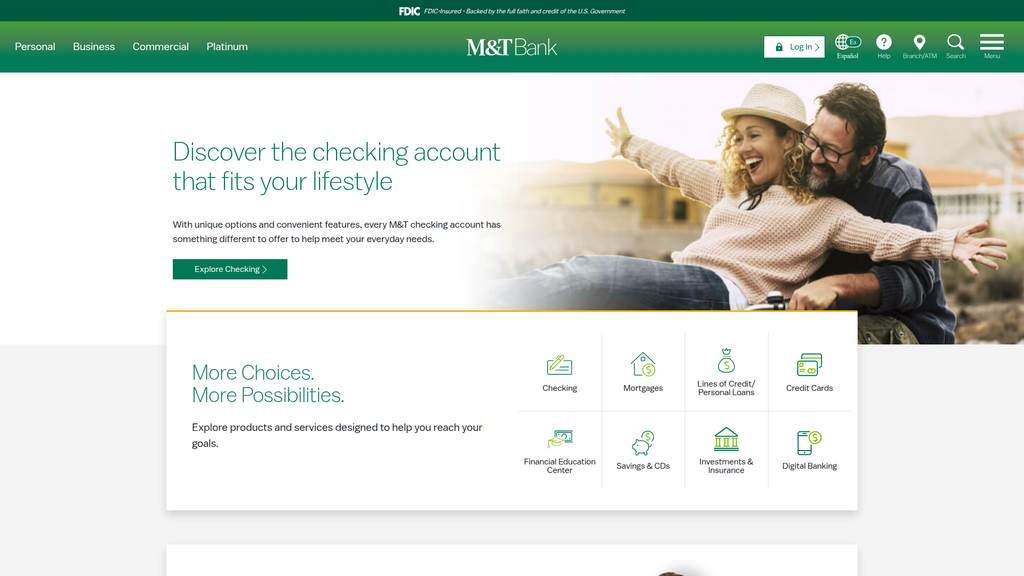

The message hierarchy is strategically sound. It leads with a relatable consumer product (checking) to draw users in, but quickly pivots to its core brand differentiators: community and small business support. This structure effectively balances immediate customer needs with long-term brand building. Product offerings and digital convenience are positioned as foundational, supporting the primary value proposition.

Messaging is exceptionally consistent across the homepage. The central theme of being a supportive partner—to individuals, businesses, and communities—is reinforced in nearly every section, from the small business testimonial to the detailed community impact statistics and employee volunteering initiatives.

Brand Voice

Voice Attributes

- Attribute:

Community-Oriented

Strength:Strong

Examples

- •

Reflecting our communities.

- •

Partnering for Change in the Communities We Serve

- •

Small business is the heartbeat of a community.

- Attribute:

Helpful

Strength:Strong

Examples

- •

What can we help you with today?

- •

We're here to help.

- •

Explore products and services designed to help you reach your goals.

- Attribute:

Straightforward

Strength:Moderate

Examples

Simple, encrypted and always in your pocket

Discover the checking account that fits your lifestyle

- Attribute:

Professional

Strength:Moderate

Examples

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

Investments & Insurance

Tone Analysis

Supportive

Secondary Tones

- •

Community-focused

- •

Reassuring

- •

Empowering

Tone Shifts

The tone shifts from consumer-focused and benefit-driven in the hero section ('fits your lifestyle') to a more corporate, socially-responsible tone in the community impact sections.

Voice Consistency Rating

Excellent

Consistency Issues

No itemsValue Proposition Assessment

M&T Bank is a comprehensive, full-service bank that differentiates itself by being an active and invested partner in the financial success of its customers, the growth of local businesses, and the vitality of its communities.

Value Proposition Components

- Component:

Community Investment and Partnership

Clarity:Clear

Uniqueness:Unique

- Component:

Expertise in Small Business Lending

Clarity:Clear

Uniqueness:Unique

- Component:

Personalized Financial Solutions

Clarity:Clear

Uniqueness:Somewhat Unique

- Component:

Convenient and Secure Digital Banking

Clarity:Clear

Uniqueness:Common

M&T's messaging carves out a powerful niche against larger, national competitors like Bank of America by heavily emphasizing its community-centric model. While all banks offer similar products, M&T's focus on quantifiable community impact ($67.4M, 245K volunteer hours) and proven small business support ('Top 10 SBA Lender') creates a tangible and emotionally resonant point of difference. This is a classic regional bank strategy executed with exceptional clarity and evidence.

The messaging positions M&T as a 'big enough to serve you, small enough to know you' institution. It competes on trust, shared values, and local expertise rather than on rates or technology alone. This positions it as a more purpose-driven choice for customers who want their banking relationship to have a positive local impact, a key differentiator from larger, less localized national banks.

Audience Messaging

Target Personas

- Persona:

The Community-Minded Individual

Tailored Messages

- •

Reflecting our communities.

- •

Partnering for Change in the Communities We Serve

- •

Our employees receive 40 hours of volunteer time...

Effectiveness:Effective

- Persona:

The Small Business Owner

Tailored Messages

"Small business is the heartbeat of a community. M&T Bank is definitely committed to independent businesses."

Top 10 SBA Lender

Effectiveness:Effective

- Persona:

The Everyday Banking Customer

Tailored Messages

- •

Discover the checking account that fits your lifestyle

- •

Simple, encrypted and always in your pocket

- •

Mortgage Assistance Programs

Effectiveness:Somewhat

Audience Pain Points Addressed

- •

Finding a bank that understands and supports local communities.

- •

Securing financing and support for a small business.

- •

Navigating financial hardship, specifically with mortgages.

- •

Finding the right financial products without feeling overwhelmed.

Audience Aspirations Addressed

- •

Contributing to the well-being and sustainability of their community.

- •

Successfully growing a small business.

- •

Achieving personal financial goals.

- •

Banking with an ethical and socially responsible institution.

Persuasion Elements

Emotional Appeals

- Appeal Type:

Belonging & Community

Effectiveness:High

Examples

Reflecting our communities.

Partnering for Change in the Communities We Serve

- Appeal Type:

Trust & Security

Effectiveness:High

Examples

FDIC-Insured

Simple, encrypted and always in your pocket

- Appeal Type:

Empathy & Support

Effectiveness:Medium

Examples

We're here to help. Learn about the programs we offer to help you through your mortgage and home equity loan hardship.

Social Proof Elements

- Proof Type:

Expert Endorsement / Awards

Impact:Strong

Examples

Top 10 SBA Lender

Top 5% of Banks

- Proof Type:

Customer Testimonial

Impact:Strong

Examples

The quote from Laura and David Alima, owners of The Charmery.

- Proof Type:

Data & Statistics

Impact:Strong

Examples

- •

$67.4M IN COMMUNITY IMPACT

- •

4,006 NON-PROFIT ORGANIZATIONS

- •

245,895 EMPLOYEE VOLUNTEER HOURS

Trust Indicators

- •

FDIC-Insured notice prominently displayed

- •

Specific, verifiable data on community impact

- •

Third-party validation (SBA Lender ranking)

- •

Customer testimonials with names and business affiliations

Scarcity Urgency Tactics

No itemsCalls To Action

Primary Ctas

- Text:

Explore Checking

Location:Hero Section

Clarity:Clear

- Text:

Mobile Banking

Location:Mobile Banking Section

Clarity:Clear

- Text:

Learn More

Location:Community, Multicultural, and Volunteering Sections

Clarity:Clear

The CTAs are clear and contextually appropriate. However, they are predominantly educational ('Explore', 'Learn More') rather than conversion-focused ('Open Account', 'Apply Now'). This suggests a strategy of guiding users deeper into the site for consideration rather than pushing for immediate action on the homepage, which is a reasonable approach for this industry. There is an opportunity to test more action-oriented language to potentially increase conversion rates from motivated users.

Messaging Gaps Analysis

Critical Gaps

A clear, concise, and memorable customer-facing tagline that encapsulates the brand's unique value proposition. The internal mission 'We make a difference in people’s lives' is powerful, but a distilled, external version is missing from the homepage.

The direct link between the bank's community support and the tangible benefits for an individual customer is implied but not explicitly stated. Answering 'How does M&T's community work benefit me?' would close the value loop.

Contradiction Points

No itemsUnderdeveloped Areas

While the mobile banking section lists features, it could be enhanced with messaging that speaks more to the feeling of control, freedom, or time-saving that these features provide to the user.

The 'Financial Education Center' is listed as an option but its value is not messaged on the homepage, representing a missed opportunity to reinforce the bank's role as a helpful guide.

Messaging Quality

Strengths

- •

Excellent brand differentiation through a clear, consistent, and well-supported focus on community and small business support.

- •

Powerful and effective use of multiple forms of social proof (testimonials, data, awards) to build credibility and trust.

- •

A highly consistent and appropriate brand voice that is both helpful and community-minded.

- •

Strong message hierarchy that balances product promotion with brand building.

Weaknesses

- •

Absence of a strong, overarching brand tagline on the homepage.

- •

CTAs are clear but could be more action-oriented to capture high-intent visitors.

- •

The value proposition for the everyday banking customer, beyond product features, is less developed than the propositions for small business and community-minded personas.

Opportunities

- •

Develop a brand-level tagline to summarize the 'Why M&T' story (e.g., 'Your Bank for Your Community').

- •

Integrate the community message more directly into product messaging, framing banking choices as a way to also support local initiatives.

- •

Create more content that tells the stories behind the community impact numbers, further strengthening the emotional connection.

Optimization Roadmap

Priority Improvements

- Area:

Homepage Hero Messaging

Recommendation:Develop and A/B test a customer-facing tagline to be placed under the main headline. The tagline should connect the banking experience with the community-focused mission.

Expected Impact:High

- Area:

Value Proposition Clarity

Recommendation:Create a dedicated 'Why M&T?' summary section on the homepage that explicitly articulates the three core pillars: Personal Service, Small Business Expertise, and Community Commitment.

Expected Impact:High

- Area:

Audience-Message Fit

Recommendation:Strengthen messaging for the 'Everyday Banking Customer' by connecting product features to life benefits and subtly linking their choice of bank to the community impact they care about.

Expected Impact:Medium

Quick Wins

Test more action-oriented CTA copy, such as changing 'Explore Checking' to 'See Account Options' or 'Find Your Fit'.

Add a brief, benefit-oriented sub-headline to the 'Financial Education Center' link to message its value upfront.

Long Term Recommendations

Develop a content marketing strategy focused on customer success stories that showcase how M&T's community-first approach has directly benefited individuals and businesses.

Create integrated marketing campaigns where product promotions are explicitly tied to community initiatives (e.g., 'For every new account opened, we donate to X local cause').

M&T Bank's homepage messaging is a masterclass in strategic differentiation for a regional bank. Instead of competing with national giants on scale or technology alone, the strategy wisely focuses on a purpose-driven narrative centered on tangible community and small business support. The message architecture is logical, starting with a broad consumer need (checking accounts) and then systematically building a case for why M&T is different and better. This differentiation is powerfully substantiated through a robust use of social proof, including specific data, a compelling small business testimonial, and notable third-party awards ('Top 10 SBA Lender').

The brand voice is consistently helpful and community-oriented, successfully positioning M&T as a supportive partner rather than just a financial utility. The primary persuasion tactic is an emotional appeal to community and belonging, which is highly effective for its target personas. The most significant gap is the lack of a succinct, memorable tagline that encapsulates this powerful story at a glance. While the community message is strong, explicitly connecting that corporate value to a direct personal benefit for the average customer would further strengthen the overall value proposition. The optimization path is clear: codify the unique brand story into a powerful tagline and continue to weave the compelling 'why' into the 'what' of their product offerings.

Growth Readiness

Growth Foundation

Product Market Fit

Strong

Evidence

- •

Established in 1856, M&T is a top 20 U.S. commercial bank with a long history and significant market presence in the Northeast and Mid-Atlantic regions.

- •

Comprehensive product suite for personal, business, and wealth management clients (via Wilmington Trust), indicating a broad and deep market penetration.

- •

Successful large-scale acquisition and integration of People's United Financial, expanding its footprint into New England and increasing assets to over $200 billion.

- •

Strong community banking model, evidenced by significant investment in local communities and a focus on personalized customer service, which resonates well in regional markets.

Improvement Areas

- •

Enhancing the digital user experience to compete with digital-first neobanks and larger national competitors with greater technology investments.

- •

Improving product quality scores, as customer ratings lag behind some key competitors.

- •

Developing more personalized product offerings by leveraging data analytics to meet evolving customer expectations for tailored financial solutions.

Market Dynamics

Moderate

Mature

Market Trends

- Trend:

Digital Transformation and AI Adoption

Business Impact:Banks are leveraging technology to streamline operations, improve customer experience, and reduce costs. AI-powered tools are being used for everything from chatbots to fraud detection and personalized financial advice.

- Trend:

Competition from Fintech and Neobanks

Business Impact:Nimble, tech-focused firms are challenging traditional banks on user experience, speed, and cost, forcing incumbents to innovate rapidly.

- Trend:

Industry Consolidation (M&A)

Business Impact:The need to gain scale, invest in technology, and expand geographic reach is driving M&A activity, particularly among regional and community banks.

- Trend:

Emphasis on Personalization and Customer Experience

Business Impact:Customers expect seamless, omnichannel experiences and personalized advice, making data analytics and customer journey mapping critical for retention and growth.

Favorable. The current economic environment, with anticipated easing of regulatory constraints and a pro-growth outlook, presents a strong opportunity for regional banks to pursue expansion.

Business Model Scalability

Medium

High fixed costs associated with a large physical branch network, compliance, and core technology infrastructure. Digital channels offer a more variable and scalable cost structure.

Moderate. M&T has demonstrated a strong focus on controlling expenses and achieving positive operating leverage. Digital transformation can further enhance this by automating manual processes.

Scalability Constraints

- •

Dependence on physical branches for certain services limits rapid geographic expansion beyond M&A.

- •

Legacy core banking systems can hinder the agile development and deployment of new digital products.

- •

Regulatory compliance overhead increases with scale and complexity.

Team Readiness

Experienced. The leadership team has a proven track record of executing large-scale M&A, such as the People's United acquisition, demonstrating capability in strategic growth and integration.

Traditional for a regional bank. While stable, it may need to evolve to support more agile, digitally-focused growth initiatives by creating cross-functional 'growth teams'.

Key Capability Gaps

- •

Agile Product Development: Need for talent experienced in rapid, iterative development cycles for digital banking products.

- •

Data Science and Analytics: Deeper expertise required to translate vast customer data into personalized experiences and predictive insights.

- •

Digital Marketing: Specialized skills in performance marketing, SEO, and content strategy to drive digital customer acquisition effectively.

Growth Engine

Acquisition Channels

- Channel:

Branch Network

Effectiveness:High

Optimization Potential:Medium

Recommendation:Transform branches from transactional hubs to advisory centers, focusing on high-value services like wealth management, mortgages, and small business consulting. Leverage branch staff for local community engagement.

- Channel:

Digital (Website/SEO/PPC)

Effectiveness:Medium

Optimization Potential:High

Recommendation:Invest heavily in SEO to capture organic traffic for key products. Run targeted PPC campaigns for high-intent keywords and optimize landing pages for conversion, especially for digital account opening.

- Channel:

Referral Programs

Effectiveness:Low

Optimization Potential:High

Recommendation:Develop and promote a formalized, digitally-enabled referral program that rewards existing customers with tangible benefits (e.g., cash bonuses, fee waivers) for bringing in new clients.

- Channel:

Community Engagement & Sponsorships

Effectiveness:High

Optimization Potential:Medium

Recommendation:Systematically track and attribute lead generation and brand lift from community events. Partner with non-profits and local business associations to host financial literacy workshops, reinforcing the bank's role as a trusted advisor.

Customer Journey

The current digital path primarily funnels users to product pages for exploration, but the transition to application and onboarding is not fully optimized for a seamless, digital-first experience.

Friction Points

- •

Potentially lengthy or complex online application processes for products like mortgages or business loans.

- •

Disconnect between online information gathering and offline (in-branch) requirements for account finalization.

- •

Lack of immediate, 24/7 support via modern channels like advanced chatbots during the application process.

Journey Enhancement Priorities

{'area': 'Digital Account Opening', 'recommendation': 'Implement a best-in-class, fully online account opening process for core checking and savings products that can be completed in under 5 minutes on any device. '}

{'area': 'Omnichannel Handoff', 'recommendation': 'Create a seamless transition for customers who start an application online but need to finish in a branch or over the phone, ensuring data is not lost and the experience is cohesive.'}

Retention Mechanisms

- Mechanism:

Product Bundling

Effectiveness:High

Improvement Opportunity:Proactively use data analytics to identify and offer personalized product bundles to customers at key life moments (e.g., mortgage and wealth services for a new home buyer).

- Mechanism:

Digital Banking App

Effectiveness:Medium

Improvement Opportunity:Enhance the mobile app with value-added features beyond core banking, such as budgeting tools, spending analysis, and personalized financial health scores to increase daily engagement.

- Mechanism:

Customer Service & Relationships

Effectiveness:High

Improvement Opportunity:Empower branch and call center staff with better CRM tools that provide a 360-degree view of the customer relationship, enabling more personalized and proactive service.

Revenue Economics

Solid. As an established regional bank, M&T likely has strong unit economics driven by a stable, low-cost deposit base and a diversified loan portfolio. Key metrics like Net Interest Margin (3.6%) and a sufficient allowance for bad loans (1.2%) indicate financial health.

Estimated to be strong (likely >5:1). The average customer acquisition cost in banking is around $200 , while the lifetime value of a multi-product banking relationship can be several thousand dollars.

Moderate to High. The bank has a history of prudent expense management and a focus on credit quality. However, there is an opportunity to improve efficiency further through digitalization.

Optimization Recommendations

- •

Increase non-interest income by expanding wealth management and trust services, which have shown strength.

- •

Focus on acquiring 'primary banking relationships' rather than single-product customers to maximize lifetime value.

- •

Reduce cost-to-serve for mass-market customers by driving adoption of digital self-service channels.

Scale Barriers

Technical Limitations

- Limitation:

Legacy Core Banking Infrastructure

Impact:High

Solution Approach:Adopt a two-speed IT architecture: maintain the stable core for systems of record while building a more agile, API-driven layer on top for rapid development of customer-facing applications and fintech integrations.

- Limitation:

Siloed Customer Data

Impact:Medium

Solution Approach:Invest in a unified Customer Data Platform (CDP) to create a single source of truth for all customer interactions, enabling true personalization and omnichannel marketing.

Operational Bottlenecks

- Bottleneck:

Manual Underwriting and Loan Processing

Growth Impact:Limits the speed and volume of loan origination, particularly for small business and consumer loans.

Resolution Strategy:Implement Robotic Process Automation (RPA) for repetitive data entry and document processing tasks. Partner with fintechs for AI-powered credit assessment models to accelerate decisions.

- Bottleneck:

Post-Merger Systems Integration

Growth Impact:Integrating People's United systems fully is a complex, resource-intensive process that can temporarily divert focus from new growth initiatives.

Resolution Strategy:Continue the planned integration roadmap with a dedicated team, ensuring clear communication with customers to minimize disruption. Post-integration, conduct a thorough technology stack review to eliminate redundancies.

Market Penetration Challenges

- Challenge:

Intense Competition

Severity:Critical

Mitigation Strategy:Differentiate on the 'community bank at scale' value proposition. Compete with large national banks (like Bank of America, PNC) on personalized service and local expertise, and with smaller banks on product breadth and digital capabilities.

- Challenge:

Customer Inertia

Severity:Major

Mitigation Strategy:Develop compelling, data-driven promotional offers and a frictionless digital onboarding process to incentivize switching. Target specific customer segments (e.g., small businesses, young professionals) with tailored value propositions.

Resource Limitations

Talent Gaps

- •

Digital Product Managers

- •

Data Scientists / AI Specialists

- •

Cybersecurity Experts

Moderate. While well-capitalized (CET1 ratio of 11.67%) , future large-scale M&A or a complete technology overhaul would require significant capital allocation.

Infrastructure Needs

Modern, cloud-based data infrastructure to support real-time analytics and AI.

Open API platform to facilitate partnerships with third-party fintech services.

Growth Opportunities

Market Expansion

- Expansion Vector:

Deepen Penetration in New England Markets

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:Leverage the acquired People's United brand equity and customer base. Launch targeted marketing campaigns and community investment initiatives to establish M&T as the leading regional bank.

- Expansion Vector:

Targeted Small and Medium Business (SMB) Segments

Potential Impact:High

Implementation Complexity:Medium

Recommended Approach:As a top SBA lender, build on this strength. Develop industry-specific banking solutions (e.g., for healthcare practices, manufacturing) with tailored digital tools, cash management, and credit products.

Product Opportunities

- Opportunity:

Enhanced Digital Wealth Management (Robo-Advisory)

Market Demand Evidence:Growing demand from mass-affluent and younger investors for low-cost, digitally accessible investment solutions.

Strategic Fit:Complements existing high-touch wealth services from Wilmington Trust, allowing M&T to serve a broader segment of the market.

Development Recommendation:Partner with a leading B2B fintech provider to white-label a robo-advisory platform, enabling faster time-to-market.

- Opportunity:

Banking as a Service (BaaS)

Market Demand Evidence:Non-financial companies and fintechs increasingly want to embed financial products (payments, lending) into their own platforms.

Strategic Fit:Creates a new, high-margin revenue stream by leveraging M&T's banking license and regulatory infrastructure.

Development Recommendation:Start with a pilot program offering payment processing or deposit account APIs to a select few fintech partners to build capabilities and understand market needs.

Channel Diversification

- Channel:

Content Marketing & Financial Education

Fit Assessment:High

Implementation Strategy:Expand the 'Financial Education Center' into a robust content hub with articles, videos, and webinars targeting key customer questions around home buying, starting a business, and retirement planning. This builds trust and drives organic traffic.

- Channel:

Affiliate & Influencer Marketing

Fit Assessment:Medium

Implementation Strategy:Partner with reputable financial blogs (e.g., NerdWallet) and influencers who focus on personal finance and small business. This can be a highly effective channel for acquiring high-quality digital customers.

Strategic Partnerships

- Partnership Type:

Fintech Integration

Potential Partners

- •

Plaid (for data aggregation)

- •

Stripe (for payment processing)

- •

Upstart (for AI-based lending)

Expected Benefits:Accelerate innovation, enhance digital capabilities, and offer best-in-class services without having to build everything in-house.

- Partnership Type:

Corporate & Workplace Banking

Potential Partners

Large employers within M&T's geographic footprint

Expected Benefits:Acquire retail customers at scale by offering exclusive banking benefits and financial wellness programs to employees of partner companies.

Growth Strategy

North Star Metric

Number of Primary Banking Relationships

This metric shifts focus from single-product sales to measuring deep, multi-product customer relationships, which are more profitable, have higher retention, and are a true indicator of market share and customer trust.

Increase the proportion of new customers with 3+ products by 15% within 18 months.

Growth Model

Hybrid: Community-Led, Digitally-Enabled

Key Drivers

- •

Local market leadership and brand trust.

- •

Superior digital convenience for everyday banking.

- •

Proactive, relationship-based advisory for complex needs (business, wealth).

- •

Strategic M&A to enter new, adjacent markets.

Empower local market leaders with resources while centralizing digital product development. Ensure seamless integration between physical and digital channels to deliver a consistent brand promise.

Prioritized Initiatives

- Initiative:

Launch a fully digital, 5-minute account opening process.

Expected Impact:High

Implementation Effort:High

Timeframe:9-12 months

First Steps:Assemble a cross-functional team (product, tech, compliance, marketing). Evaluate and select a technology partner. Map the end-to-end customer journey.

- Initiative:

Develop a formalized digital referral program.

Expected Impact:Medium

Implementation Effort:Medium

Timeframe:4-6 months

First Steps:Benchmark competitor referral programs. Define incentive structure. Develop marketing collateral to promote the program to existing customers.

- Initiative:

Pilot an SMB Digital Onboarding Platform

Expected Impact:High

Implementation Effort:High

Timeframe:12-15 months

First Steps:Conduct voice-of-customer research with SMB owners. Define the MVP feature set. Start building a business case for investment.

Experimentation Plan

High Leverage Tests

{'test_name': 'Landing Page CTA A/B Test', 'hypothesis': "Changing the call-to-action on the main checking account page from 'Explore Checking' to 'Open an Account' will increase application starts by 10%."}

{'test_name': 'New Customer Onboarding Email Cadence', 'hypothesis': 'A 5-part educational email series for new checking account customers will increase digital service adoption (e.g., mobile deposit, bill pay) by 25% in the first 30 days.'}

Utilize a combination of web analytics (for conversion rates), product analytics (for feature adoption), and cohort analysis (for long-term value) to measure the impact of experiments on key business metrics.

Establish a bi-weekly 'Growth Sprint' where new experiments are launched and results from previous tests are reviewed.

Growth Team

A cross-functional 'Growth Tribe' led by a Head of Growth, with smaller squads focused on specific goals (e.g., Retail Acquisition, SMB Engagement, Digital Adoption). This team should operate with a high degree of autonomy.

Key Roles

- •

Head of Growth

- •

Digital Product Manager

- •

Data Analyst

- •

Performance Marketing Specialist

- •

UX/UI Designer

Invest in continuous training on agile methodologies, data analytics, and experimentation. Foster a 'test and learn' culture where failures are treated as learning opportunities. Encourage participation in industry conferences and workshops.

M&T Bank is a well-established regional banking powerhouse with a strong foundation for growth, built upon a successful, community-focused business model and a proven track record of strategic M&A, most notably the recent acquisition of People's United. This move significantly expanded its geographic footprint and asset base, positioning it for deeper penetration in attractive New England markets. The bank's product-market fit in its core segments is strong, and market timing is favorable for growth-oriented regional players.

The primary challenge and greatest opportunity for M&T lies in accelerating its digital transformation. While it offers digital banking services, it faces intense competition from larger national banks with massive tech budgets and nimble, digital-native fintechs. The bank's growth engine must be supercharged by optimizing digital acquisition channels, creating a truly seamless and frictionless digital onboarding experience, and leveraging its vast data to personalize customer interactions. Relying solely on its traditional strengths of community presence and M&A will not be sufficient to win in the next decade.

Key scale barriers are common to the industry: legacy technology, operational bottlenecks from manual processes, and the war for technical talent. Overcoming these requires a strategic commitment to modernizing the tech stack, embracing automation, and building an agile, data-driven culture.

Strategic Recommendations:

-

Win in Digital Onboarding: The highest priority should be creating a best-in-class, fully digital account opening process. This is the new 'front door' for the bank and the single most critical initiative to compete for new customers.

-

Deepen New Market Penetration: Aggressively invest in marketing and community engagement in the former People's United footprint to solidify M&T's brand and capture market share.

-

Innovate Through Partnerships: Instead of trying to build everything in-house, M&T should actively partner with fintechs to rapidly deploy new capabilities, such as robo-advisory services for wealth management or AI-powered underwriting for small business loans. This accelerates time-to-market and reduces risk.

By successfully integrating its recent acquisition while simultaneously accelerating its digital evolution, M&T Bank can fortify its position as a dominant 'community bank at scale,' creating a sustainable competitive advantage that blends the best of traditional relationship banking with modern digital convenience.

Legal Compliance

M&T Bank provides a comprehensive set of privacy notices accessible via a 'Policies, Notices and Important Information' link in the website footer. This central hub is a best practice for transparency. The primary 'US Consumer Privacy Notice' is aligned with the Gramm-Leach-Bliley Act (GLBA), detailing what personal information is collected, why it's collected, and how it's shared with affiliates and third parties. It clearly provides customers with the right to opt-out of certain information sharing, as mandated by GLBA, via a toll-free number or an online form. This demonstrates a strong foundational compliance with federal banking privacy laws. The policy also clarifies that for California residents, GLBA governs their data privacy over CCPA, which is a key distinction for financial institutions.

The 'Terms of Use' are clearly accessible from the footer, covering the use of websites and mobile apps. The terms are well-structured, defining the relationship between the user and M&T Bank, disclaiming warranties, and limiting liability. They include standard provisions regarding intellectual property, acceptable use, and governing law. The language is formal but generally understandable for a legal document. A key strength is the explicit inclusion of mobile apps within the scope, which is critical for a modern banking platform. The terms also incorporate an E-Sign Consent agreement, which is essential for facilitating digital transactions and account openings.

Upon visiting the site, a cookie consent banner appears at the bottom of the page. It provides a brief notice and links to 'Accept Cookies' and 'Manage Cookies.' The 'Manage Cookies' option allows users to granularly control their consent for different categories of cookies (e.g., Functional, Performance, Advertising), which is a strong practice aligned with modern data privacy expectations. The detailed 'M&T Bank Cookie Notice,' available in the Privacy & Preference Center, provides transparency by listing the specific cookies used, their purpose, and their duration. This level of control and transparency is a strategic asset, building user trust and demonstrating adherence to privacy principles.

M&T Bank demonstrates a robust approach to state-specific data protection laws, particularly the California Consumer Privacy Act (CCPA) / California Privacy Rights Act (CPRA). There is a dedicated 'California Consumer Privacy Notice' that acts as a 'Notice at Collection.' It details the categories of personal information collected, the business purposes for collection, and a clear statement that M&T Bank does not sell or share personal information as defined by the CCPA/CPRA. This 'no sale' stance significantly simplifies their compliance burden and reduces risk. The bank has established a 'Privacy & Preference Center' which provides a clear and centralized mechanism for California residents to submit consumer rights requests, demonstrating a mature operational process for handling such requests. While the bank has a presence in Canada, specific GDPR compliance measures are not explicitly detailed, as their primary focus is on US customers and regulations.

M&T Bank shows a strong and public commitment to accessibility. They provide a dedicated 'Accessible Banking' page detailing services for customers with disabilities, including in-branch features, accessible documents (Braille, large print), and talking ATMs. Critically, the policy states that their online accessibility efforts are based on the Web Content Accessibility Guidelines (WCAG) standard, which is the globally recognized benchmark. The website includes a 'Skip to Main Content' link, a fundamental accessibility feature. This public commitment and alignment with WCAG standards significantly mitigate the risk of ADA-related lawsuits, which are increasingly common for consumer-facing websites, especially in the financial sector.

As a major US bank, M&T's website correctly displays key industry-required disclosures. The 'Member FDIC' logo and statement are prominently displayed, confirming that deposits are insured by the federal government. The 'Equal Housing Lender' logo and policy are also present, which is mandatory for institutions offering mortgage products. The site includes necessary disclosures on product pages, such as Annual Percentage Rate (APR) for loans and mortgages, aligning with the Truth in Lending Act (TILA). Disclosures for investment products offered through their affiliates correctly state that these products are not FDIC insured and may lose value. The bank also provides information on Anti-Money Laundering (AML) programs and the SAFE Act, demonstrating a comprehensive approach to the complex web of banking regulations governed by agencies like the Federal Reserve, FDIC, and CFPB.

Compliance Gaps

- •

While disclosures are present on product pages, the APR and APY information for illustrative examples can be complex for the average consumer to find and interpret without navigating to deeper product detail pages.

- •

The cookie consent banner's default setting has all optional cookies (e.g., advertising) pre-selected as 'on' in the 'Manage Cookies' section, requiring users to actively opt-out. A more conservative, privacy-protective stance would be to have these defaulted to 'off'.

- •

While a Canadian privacy notice exists, the specific rights and protections for non-US customers (e.g., those under GDPR in the EU, if any) are not as clearly articulated or easy to find as the CCPA information.

Compliance Strengths

- •